Market indicators and food import bills

Sharp fall in the global cost of imported food anticipated in 2009

|

|

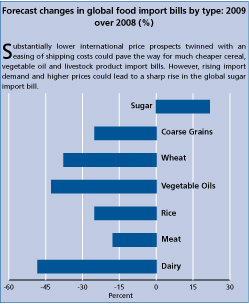

After reaching an unparalleled high in 2008, the global food import bill is expected to retreat from over USD 1 trillion to USD 790 billion by the end of the year. The prediction is conditioned on pervasive and sustained annual declines across international prices of foodstuffs as well as freight rates.

Of the estimated USD 226 billion global contraction from 2008, grain-based foodstuffs will account for over half of the decline, followed by a combined USD 115 billion fall in vegetable oil and dairy product bills. The exception to the trend is sugar, which is set to register a 22 percent rise to a record USD 39 billion.

Global import volumes remarkably firm

|

|

Declining import costs do not imply smaller volumes of food shipments. Physical deliveries held extremely firm last year, despite unprecedented surges in international quotations for food and freight, and are likely to do so this year, in spite of the economic downturn: record deliveries for wheat, vegetable oils, dairy products and meat were witnessed in 2008; as for this year, cereal import volumes are likely to remain robust while traded volumes of other commodities are expected to soar to new heights. Such resilience to price movements and to economic recession underscores the critical role of international trade to assure food consumption around the world.

Cost of importing food for the worlds poorest countries to fall

|

|

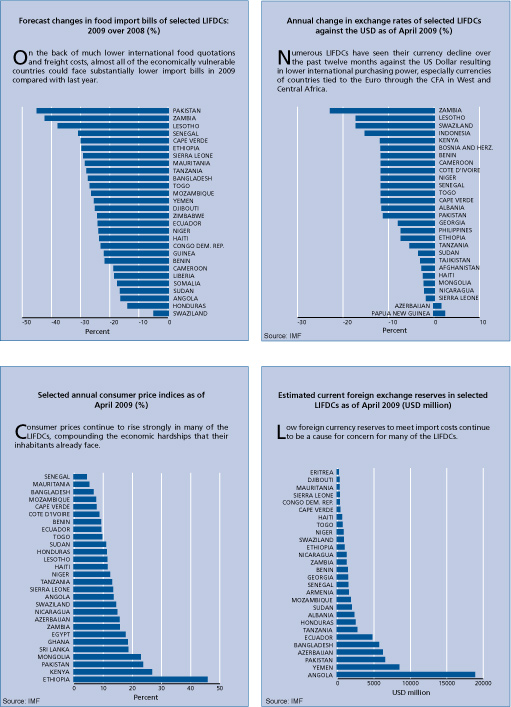

The cost of purchasing food on the international market place for the most economically vulnerable groups, LDCs and LIFDCs is set to fall by less than one-quarter for each from last year. Much of the respite comes by way of a one-third drop in their cereal import bills and an equally pronounced drop in vegetable oil purchases, in response to improved domestic supply prospects. Prospects in Sub-Saharan Africa are less optimistic. The subregion endured the largest rise in food import costs, when measured from the run-up to the peak of the high price event in 2008, but the expected decline in the overall bill this year, from USD 28.4 billion to USD 21.3 billion, is among the smallest of any geographic or economic group.

The encumbrance facing some of the worlds poorest countries in importing food can be contrasted against that falling on richer nations, whose food import bills peaked far less in 2008 and are expected to drop disproportionately more in 2009.

...but the burden remains heavy

|

|

Despite the welcome declines in food import bills, the deteriorating economic environment in which the falls are taking place is likely to offset much of the benefit. Eroding purchasing power in most LIFDCs through a combination of falling incomes and falling real exchange rates over much of the past 12 months afflicts the affordability of food however cheap it has become on the international market place.

Forecast import bills of total food and major foodstuffs (USD million)

| |

World |

Developed |

Developing |

LDC |

LIFDC | | |

2008 |

2009 |

2008 |

2009 |

2008 |

2009 |

2008 |

2009 |

2008 |

2009 | |

TOTAL FOOD | 1014 617 | 789 110 | 667 468 | 533 496 | 347 149 | 255 613 | 26 012 | 19 105 | 121 313 | 93 339 | | Cereals | 375 387 | 263 254 | 222 236 | 153 167 | 153 151 | 110 087 | 11 028 | 7 549 | 40 191 | 27 068 | | Vegetable Oils | 172 791 | 99 122 | 86 677 | 49 574 | 86 113 | 49 548 | 6 319 | 3 592 | 33 842 | 19 977 | | Dairy | 86 513 | 44 803 | 60 562 | 31 839 | 25 951 | 12 964 | 1 666 | 662 | 7 541 | 3 543 | | Meat | 104 567 | 86 134 | 78 261 | 64 317 | 26 306 | 21 817 | 895 | 733 | 3 992 | 3 127 | | Sugar | 31 836 | 38 743 | 17 502 | 21 523 | 14 333 | 17 220 | 2 026 | 2 182 | 5 527 | 7 173 |

|

June 2009

June 2009