November 2007 November 2007 | ||

|

Food Outlook | |

| Global Market Analysis | ||

|

FISH AND FISHERY PRODUCTS

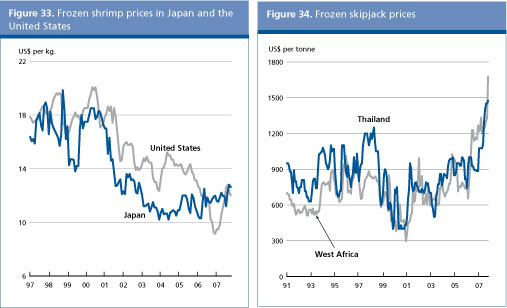

Prospects for prices of shrimp, the principal commodity in international fish trade, are rather subdued in 2007, reflecting a weakening of import demand globally. Lack of demand growth in the United States is expected to keep the level and value of imports to that market unchanged from last year, with some uncertainty arising from concerns over the quality of Chinese shrimp exports. In Japan, the tendency for fish imports to fall is not sparing shrimp. On the other hand, import demand in the European Union continues to grow, especially for warm water shrimp but, in general, ample supplies from aquaculture are putting shrimp prices under pressure, with capture shrimp fisheries showing more instability and price variation. In the next few months, prices in the United States market may firm somewhat, while they are likely to decline in the European Union and Japan. In 2008, projected increases in farmed shrimp production will put new downward pressure on prices.

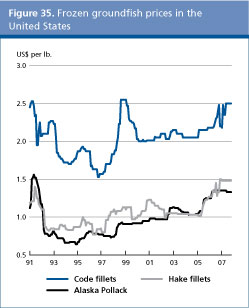

Reduced catches of tuna, especially in the Indian and Pacific Oceans , have resulted in a dramatic increase in prices, causing major concern to canneries. Higher fuel costs have only added to the difficulties of the tuna fleet. In the Eastern Pacific areas, the upcoming closure of the fishing season forced canneries to bid aggressively for raw material, causing prices to rise even higher. In the short term, there seems to be no end in sight to the upward spiral of tuna prices. With conflicting market pressures, predicting short- to medium-term price trends for frozen cod fillets remains challenging. On the one hand, tighter European cod quotas this year and next should keep prices along the upward trend that has been evident in recent years. However, increased supplies of whitefish products, such as Vietnamese pangasius fillets, are expected to dampen somewhat the tendency for cod prices to rise. As a result, price prospects for frozen groundfish fillets remain broadly stable.

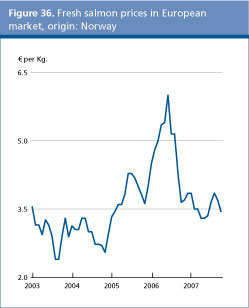

A situation of ample supply and dull demand is characterizing the European Union salmon market, with declining prices. At present, the current quotations are nearing the minimum import price set by the European Union at 2.80/kg live weight equivalent. For the January-September 2007 period, Norway, the principal farmed salmon producer, exported 390 000 tonnes of salmon (live weight equivalent), a 27 percent increase over the corresponding period of 2006. This increase in quantity was matched by a mere 4 percent increase in value, resulting in a substantial drop in the export unit value from the high levels of 2006, a year characterized by strong demand and limited supplies for both farmed and captured species.

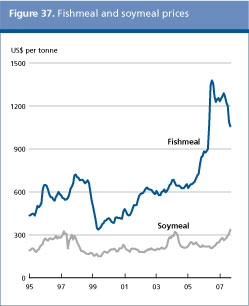

Despite lower production, prices of fishmeal declined in the course of 2007 from the sky-high levels reached in 2006. This fall was caused by falling imports by China, the main fishmeal market, which is holding huge inventories, forcing Peruvian producers to sell at discounted prices. However, prices are likely to have bottomed out at their present level of US$1 050/tonne and are likely to rebound as China is expected to resume purchasing fishmeal soon. Fishmeal is an extremely important feed ingredient for carnivorous aquaculture species and its price has an immediate impact on aquaculture production costs.

Table 11. World fish market at a glance

The world fish production is characterized by ever increasing aquaculture production, albeit at declining growth rates, while capture fisheries have fallen back, a tendency which is likely to prevail also in 2007. The contraction in capture fisheries reflects generalized over-fishing and reduced fish stocks, especially of groundfish resources, but also reduced anchoveta catches in Peru in 2006 and 2007. In addition, high fuel prices are influencing negatively the high sea fisheries, such as tuna fisheries. Shrimp trawling, which is a particularly fuel intensive fishing activity, was also negatively affected by the surge of oil prices in 2007. On the other hand, the aquaculture boom continued in 2007 for all major species produced for international trade, such as salmon, shrimp, catfish, tilapia, the production of which recorded two digit increases. Very soon, aquaculture will overtake capture fisheries as the main source of food fish supply. At the moment, its share is about 45 percent. For the coming year, the overall trend of rising aquaculture production, on the one hand, and weaker capture fisheries, on the other, is more than likely to proceed, although limited availability of fishmeal and fish oil, an essential ingredient to feed carnivorous species, may act as a constraint on the rapidly increasing aquaculture production. Indeed, most of the fishmeal/oil comes from capture fisheries of small pelagic fish, which declined in 2006 and 2007. To overcome the problem, the industry in all main aquaculture feed producing countries is looking for new feed formulations based on non-fish protein that still develops omega-3 in the cultured fish.

With 79 percent of the world production of fish and fishery products (capture plus aquaculture) taking place in developing countries, it is only natural that these play a major role in international trade. In fact, half of world fish exports of US$86 billion (2006) now originates in developing countries. Net export revenues continue to be of vital importance to the economy of many fish exporting developing countries, amounting to more than US$22 billion per year. Imports are mostly by developed countries, which are responsible for about 80 percent of the total import value of US$90 billion (2006). International trade in fish and fishery products continues to grow strongly, reflecting rising consumption not only in the European Union and the United States but in all other regions, including Asia with the notable exception of Japan. Rising trade volumes (except for fish meal) and values also testify to the increasing globalization of the fisheries value chain, in which processing is being outsourced to Asia (e.g. China, Thailand and Viet Nam) and, to a lesser degree, Central and Eastern Europe (e.g. Poland and Baltic countries) and North Africa ( Morocco). It is noteworthy that, many species, such as salmon, tuna and tilapia, are increasingly traded in the processed form (fillets or loins).

China1/ is the largest fish exporter at US$8.9 billion (2006) but its imports are also growing, reaching US$4.2 billion (2006). The increase in Chinas imports is partly a result of outsourcing, as Chinese processors now import raw material from all major regions, including South and North America and Europe, for re-processing and export, but it also reflects Chinas growing domestic consumption of species not available from local sources. Chinas trade in 2007 (six months) shows strong growth in both exports and imports (see table). At the present trend, China will soon overtake Spain as the worlds third largest importing country2/ after Japan and the United States. Table 12. Imports and exports of aquatic products in China (Jan June 2007 6 months)

Source: Chinese Customs (INFOYU)

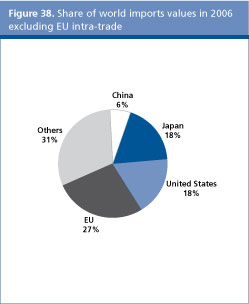

The European Union is by far the largest single market for imported fish and fishery products. This reflects both its growing domestic consumption but also the fact that the European Union itself has enlarged to include 27 member countries. The 2006 imports (EU-25) reached US$38 billion, up 16 percent from 2005, or 42 percent of total world imports. However, official statistics also include trade among European Union partners. If intraregional trade is excluded, the European Union imported US$20.5 billion worth of fish and fishery products from non-European Union suppliers, an increase of 16 percent from 2005. This still makes the European Union the largest market in the world with about 27 percent of world imports. Partial figures for 2007 confirm the present upward trend of European Union imports, with a 3 percent increase in values recorded in the January-July period. Japan is the largest single country market for fish, but import volumes have been declining in recent years, due to weaker domestic demand associated with a long-term shift towards reduced fish consumption. In 2006, imports, which mainly consist of shrimp, tuna and salmon showed a 3.5 percent decline from 2005 to below US$14 billion, and a 5.6 percent reduction in volume to 3.2 million tonnes. Figures in 2007 confirm the downward trend, with a further 5.5 percent drop in import value. The United States is the second largest single country import market after Japan. With a growing population and a long-term positive trend in seafood consumption, imports reached US$13.3 billion in 2006, 1.5 percent more than in 2005. In 2007, they are likely to overtake those of Japan, converting the United States into the largest single country market. Imported quantities of edible fish products reached 2.5 million tonnes in 2006. 2007 figures (8 months) show a small increase in volume of 0.7 percent, whereas import values increased more strongly, by 5.6 percent. The largest import item in value is shrimp followed by salmon, crab and tuna. Of note is the strong increase in tilapia imports in 2007 (volume +17 percent, value +21 percent) and crab (volume +12 percent, value +22 percent).

World per caput consumption of fish and fishery products has risen steadily over the last decades from an average for the decade of 11.5 kg during the 1970s, 12.8 kg in the 1980s to 14.8 kg in the 1990s. It has continued to grow in the 2000s, to an average of 16.4 kg per caput in 2001-2003. Figures at the world level, however, are strongly influenced by Chinas dominance. In fact, Chinas domestic consumption of fish and fishery products per caput has risen from less than 5 kg in the 1970s to the present 26 kg, which given the size of the Chinese population, have contributed to much of the increase in the world per caput consumption. Excluding China, per caput consumption averaged 13.5 kg in the 1970s, 14.3 kg in the 1980s, falling in the 1990s to 13.2 kg per caput. The average for the 2001-2003 period points to a new increase to 14.0 kg per caput. Based on FAOs estimates for the most recent years, per caput food fish consumption is set to rise further and average 17.2 kg in 2006 and 17.4 kg in 2007. However, there are wide differences in fish consumption per caput across regions, with below-average and stable levels in South America and Africa. In many ways, it is the region of Africa which gives major causes for concern given the low absolute levels of consumption and the strong growth in projected population. On the other hand, Africa has a significant potential in aquaculture which at present is hardly exploited at all. 1. Excluding Hong Kong SAR and Taiwan Province of China 2. Including Hong Kong SAR and Taiwan Province of China makes China already the third largest importer. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GIEWS | global information and early warning system on food and agriculture |