I. Current agricultural situation - facts and figures

1. CROP AND LIVESTOCK PRODUCTION1

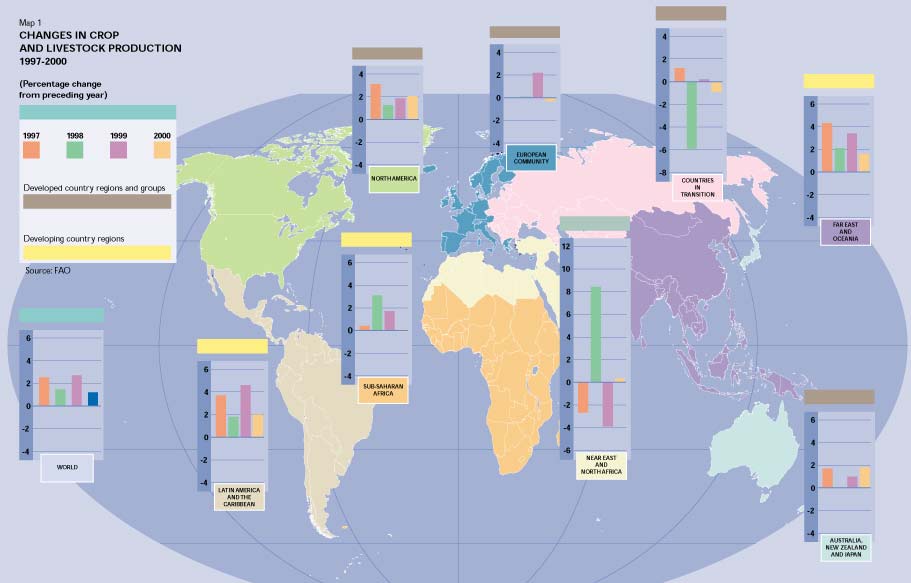

World agricultural output in 1999 is estimated to have increased by 2.3 percent, which is a modest improvement on the 1.4 percent growth rate achieved in 1998. Crop production, in particular, expanded more strongly in 1999 than in the previous year. The more favourable outcome is largely due to a rise in output in the developed countries, estimated to be 1.5 percent. This follows on from a 0.7 percent decline in overall output in 1998, when crop production fell by 3.4 percent. The performance of the developing countries as a group continued to be relatively disappointing during 1999. Their agricultural production increased by only 2.8 percent, which was about the same rate as in 1998 but lower than the 3.2 percent of 1997 and well below the high rates of between 4 and 5 percent recorded from 1993 to 1996.

Estimates of agricultural production in 2000 are still provisional but point to an expansion in agricultural production of about 1 percent. Crop production is estimated to increase by less than 1 percent, as in 1998. The slowdown is due to reduced growth in both developed and developing countries, with the former estimated to record growth of less than 1 percent and the latter about 1.5 percent in 2000. In the case of developing countries, the poor performance continues the trend of the last four years towards slower growth.

Among the developing country regions, the strongest performance in 1999 was recorded in Latin America and the Caribbean, where growth in agricultural output strengthened significantly to an estimated 4.6 percent, after a growth rate of only 1.8 percent in 1998, when the El Niño phenomenon had negatively affected agricultural activity, particularly in the Andean region, and Hurricane Mitch had caused severe damage in Central America. The main contributing factor behind the good performance in 1999 was the strong 5.1 percent growth in output in South America, where Brazil in particular increased its agricultural production by an estimated 7 percent. Growth in output was somewhat more modest in Central America but, at 3.4 percent, it represented a significant improvement on the 1.1 percent recorded in 1998. By contrast, agricultural production declined by about 1 percent in the Caribbean. For 2000, preliminary estimates suggest output growth in the region of only about 2 percent. Growth is expected to be somewhat higher in Central America than in the Caribbean and South America.

In developing East Asia and the Pacific, agricultural performance also improved somewhat in 1999, expanding by 3.4 percent after the lower 2.1 percent recorded in 1998. The rate of overall agricultural production growth in the region has nevertheless declined in the past few years, and output growth for 2000 is preliminarily estimated to be only 1 to 2 percent. The main factor behind the declining trend in the last few years is the slowdown in production growth in China which, from an annual average of about 6 percent in 1991-97, slowed to 4 percent in 1998 and 3 percent in 1999, with the provisional estimate for 2000 pointing to another increase of about 3 percent. After stagnating in 1998, Indian agriculture saw production expand by nearly 4 percent in 1999, while estimates for 2000 point to a small decline of less than 1 percent.

In sub-Saharan Africa, 1999 was another disappointing year in terms of agricultural output, as overall agricultural production lagged behind population growth rates for the third consecutive year. Output increased by 2.1 percent in 1999, after increasing by 0.4 and 2.3 percent in 1997 and 1998, respectively. In Nigeria, production growth slowed from more than 4 percent in 1998 to slightly less than 3 percent. The preliminary estimates for 2000 suggest no improvement in the sluggish performance of the last few years and overall agricultural production appears to have expanded by only 0.5 percent.

In the Near East and North Africa region, agricultural output fell by 3.9 percent in 1999 after recording growth of 8.4 percent in 1998. Drought was the dominant factor affecting agricultural output in the region in 1999, with cereal production recording particularly sharp falls in Afghanistan, Algeria, Iraq, the Islamic Republic of Iran, Jordan, Morocco, the Syrian Arab Republic and Tunisia. In Turkey, too, inadequate rainfall led to an agricultural production decline of nearly 5 percent. By contrast, overall output expanded strongly in Egypt. In 2000, drought conditions are expected to continue having an adverse effect on production in Afghanistan, Algeria, Iraq, the Islamic Republic of Iran, Morocco and Tunisia, while some recovery is expected in Jordan, the Syrian Arab Republic and Turkey. Provisional estimates suggest an increase of less than 0.5 percent in the region's overall agricultural production in 2000.

Among the developed countries, the transition countries recorded virtually unchanged agricultural production in 1999, following a 5.9 percent decline in 1998. The Russian Federation experienced a fall in output of 2.7 percent and most of the other larger agricultural producers in the region witnessed some minor declines in agricultural output in 1999, the major exceptions being Kazakhstan and Romania, both of which saw agricultural production rebound after the sharp drops experienced in 1998. Provisional estimates for 2000 suggest a small contraction of agricultural production of less than 1 percent. Among the major producers, positive performances are expected only in the Russian Federation and Ukraine.

In the developed market economies, agricultural output expanded by an estimated 1.8 percent in 1999, following the more modest 0.8 percent recorded in 1998. Output grew the most (by 2.2 percent) in the European Community (EC) and slightly less in North America (by 1.9 percent), although Canada alone recorded an expansion of 6.2 percent after its already high rate of 5.9 percent in 1998. In the developed countries of Asia and the Pacific, overall output growth was estimated to be 1.0 percent, with Japan recording less than 1 percent, Australia at 1 percent, and with production actually declining by 5.1 percent in New Zealand. Estimates for 2000 point to a lower increase, of about 1 percent, in overall output, covering an anticipated rise of around 2 percent in North America, 1.8 percent in developed Asia and the Pacific and a marginal contraction in the EC.

2. INTERNATIONAL AGRICULTURAL PRICES

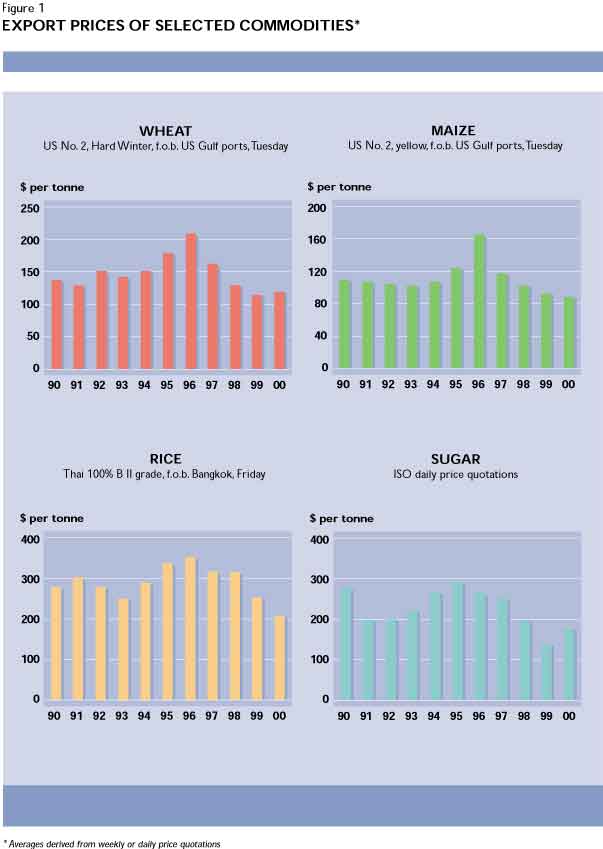

International wheat and coarse grain prices increased moderately during the first half of the 2000/01 season (July-December 2000), amid indications of lower production and prospects for a large drawdown of stocks among the major exporters. For wheat, the overall price increase proved limited because of the availability of large export supplies from a number of non-traditional sources such as India and Pakistan. Furthermore, in some importing countries such as China, where domestic production fell sharply, the decline was mostly met by a larger drawdown of their own stocks rather than by larger import volumes. For coarse grains, particularly for maize, the impact of the surge in world import demand was mitigated by a near-record crop in the United States, continued large sales from China and abundant supplies of the competing feed-quality wheat in international markets. Against this background, a stronger recovery in prices could not be envisaged for at least another season, and only in the event of a notable cutback in grain production in 2001.

Contrary to the developments in other major cereal markets, international prices of high-quality and low-quality grains as well as long and medium rice varieties fell during most of 2000, reaching their lowest level since 1987. The main reason for this was the type of policies adopted by many countries in the wake of the rice shortfalls and high international prices that were witnessed in 1998 and early 1999. The most important rice-importing countries reduced their import demand, while some exporters pursued aggressive export drives in order to cope with large stocks. Barring any unexpected shock, rice prices were expected to continue on a downward trend during the first quarter of 2001 as new rice crops from exporters in the Southern Hemisphere and in Viet Nam came on to the market. Moreover, the policy measures being considered by India - to boost exports - and in Indonesia, Malaysia and Nigeria - to raise import restrictions - could all contribute to an aggravation of the price weakness.

During the 1999/00 season (October-September), international prices for oils and fats were under downward pressure. The decline was largely the result of ample supplies. Stocks of oils and fats reached record levels, preventing a recovery of international prices. By contrast, prices for oilseeds and oilmeals strengthened as the expansion in global supplies of these products came to a halt despite a strengthening demand. Prices of oilseeds and products were forecast to continue moving in opposite directions in 2000/01. The anticipated ample supplies of oils and fats relative to demand were likely to limit the chances for a sustained recovery of prices for oils and fats. The tightening supply and demand situation for oilseeds, oilcakes and oilmeals could lend support to their prices.

World coffee prices fell throughout almost all of the 2000 calendar year, only showing a marginal increase for the month of December. The International Coffee Organization (ICO) composite price fell from $1 679 per tonne in January 2000 to $1 084 per tonne in December. For the year as a whole, the composite price averaged $1 416 per tonne compared with $1 890 in 1999, a fall of 25 percent. This continues the downward trend of 1999, when prices fell by 22 percent over the previous year's levels. Coffee prices in 2000 were at their lowest level since 1993, and at only half of their average level for the 1980s. In spite of slightly lower production in the 1999/00 coffee year (October-September), resulting from adverse weather in some major producing countries, exports continued to grow. In the absence of any significant increases in consumption, importers' stocks also continued to accumulate during the year. The market was further weakened by expectations of a recovery in production levels in excess of consumption growth for the 2000/01 coffee year. The persistence of historically low prices prompted the Association of Coffee Producing Countries (ACPC) to agree to the implementation of a coffee retention plan in May 2000. Participating countries will retain 20 percent of their coffee exports when the ICO indicator price (a 15-day moving average of the ICO composite price) falls below a specified lower limit, releasing the retained stocks on to the market when the price rises above a specified upper limit.

Cocoa bean prices fell by 22 percent in 2000, following the 32 percent fall in 1999 to reach levels not seen since the early 1970s. The International Cocoa Organization (ICCO) daily average price averaged $888 per tonne in 2000, compared with an average of $1 140 per tonne in 1999 and $1 465 per tonne over the previous five years. The depressed prices reflect a tendency for growth in production to outstrip growth in consumption. Production and consumption had been approximately in balance for the three previous years, but production in 1999/00 grew by almost 8 percent while consumption, as measured by grindings, grew by less than 6 percent. On the demand side, global per capita consumption has risen by less than 1 percent per year since 1990, reflecting sluggish growth in the United States, Western Europe and East Asia.

Tea prices strengthened in 2000. The FAO composite price for tea (a weighted average price of tea traded in the major markets of India, Kenya and Sri Lanka) averaged $1 830 per tonne in the first quarter of 2000, weakened to $1 770 per tonne in the second quarter in line with seasonal demand trends, then increased to $1 880 per tonne in the third quarter before falling back to the level of the first quarter. The FAO composite price for tea in 2000 averaged $1 829 per tonne. This was 7 percent higher than the average of $1 707 per tonne in 1999, when weak demand kept prices lower than 1998 levels for most of the year. Tea prices in 2000 were 5 percent higher than the average for the previous five years but remained below the peak levels of nearly $2 000 per tonne reached in 1997.

After falling to $0.98 per kilogram in December 1999, their lowest level for 15 years, world cotton prices started to recover in 2000. The Cotlook "A" index, an indicator of world prices, reached $1.45 per kg in July and August 2000, about 15 percent higher than a year earlier, owing to slow growth in overall global production and strengthened demand. Demand for cotton has been stimulated by the implementation of the Agreement on Textiles and Clothing (ATC) and the North American Free Trade Agreement (NAFTA), which have increased trade in textiles. FAO and the International Cotton Advisory Committee predict that the ATC, which is intended to eliminate all quota restrictions on textile trade by 2005, will increase global cotton consumption by up to 3 percent. Growth in the world economy provided a further stimulus to higher import demand. The continuing recovery from the financial crisis of 1998 is expected to result in larger cotton imports by countries in Southeast Asia. World cotton prices in 2000 also benefited from the higher oil prices and higher synthetic fibre prices, as well as by the lower level of stocks in China.

After falling to their lowest point for a number of years in August 1999, rubber prices recovered on major world exchange markets. Prices of RSS1 rubber in the London and Malaysian markets in mid-2000 were about 20 percent higher than at the same time in 1999. This price recovery reflected the strengthened demand for natural rubber, together with the impact of higher oil prices, which made synthetic rubber more expensive. World rubber prices are expected to remain firm in the near future, largely as a result of high oil prices. However, no further substantial price improvement would be expected because of the great potential for increased supply from more intensive tapping and from the increased production capacities in new producer countries such as Viet Nam. In addition, the recent slowdown in economic growth in the United States may result in lower demand for natural rubber.

World sugar production increased by 4 percent to 135.8 million tonnes (raw sugar equivalent), another record level, in 1999/00. This resulted in unprecedented high global stocks as supply significantly outstripped consumption. Thus, after having fallen by 22 percent in 1998, and by a further 30 percent in 1999 to reach $138 per tonne, by March 2000 the annual average International Sugar Agreement (ISA) price had reached a 14-year low of $113 per tonne. However, estimates for 2000/01 point to a 4 to 5 percent reduction in production to 130 million tonnes, continued expansion in exports, a consequent decline in the high level of global sugar stocks and a continuing strengthening of prices. Prices followed an upward trend starting in April 2000 and, in spite of falling back slightly towards the end of the year, the annual average price for 2000 reached $180 per tonne, 30 percent up on 1999. However, average prices in 2000 were still 20 percent lower than in 1998.

In the first quarter of 2000, banana prices on major markets recovered from the record low levels they had reached at the end of 1999. This rise was partly due to the conjunction of lower production in several Latin American countries that were affected by adverse weather conditions and higher demand in several markets, notably Japan, China and Central and Eastern Europe. However, prices started to decline in May as production gradually recovered in countries that had been affected by Hurricane Mitch (notably Honduras) and demand was curtailed in Northern Hemisphere countries by competition from the domestic summer fruit harvests. Overall, the price average expressed in local currencies was higher in 2000 than in 1999 in the United States and Central and Eastern Europe, but lower in Western Europe and Japan. The combination of lower exports in Latin America and weak dollar prices in the European Community (EC), traditionally the most profitable of the major banana markets, led to a significant drop in export earnings for many developing countries. The profitability of the banana industry was further curtailed by higher input and transport costs in the wake of rising oil prices.

3. WORLD CEREAL SUPPLY SITUATION AND OUTLOOK2

Production

World cereal output in 2000 fell to 1 852 million tonnes (including rice in milled equivalent), which is nearly 2 percent below the previous year's level and also below the average for the past five years. A number of factors contributed to the contraction in cereal output in 2000, ranging from natural disasters and low prices prevailing in recent years to government policies aimed at cutting excess supply.

Global wheat production fell slightly to 586 million tonnes. This was mostly because of unfavourable weather, particularly severe drought in parts of Europe and North Africa as well as in several countries in Asia, including China, where policy changes also played an important role in reducing plantings.

World output of coarse grains in 2000 registered a drop of 2 percent to 869 million tonnes. The decline mostly resulted from weather-damaged crops in parts of Asia and Europe. A drought-plagued season sharply reduced China's maize output, which fell by 24 million tonnes. Drought conditions throughout most of Eastern Europe particularly affected maize and barley crops.

Global rice output fell to 397 million tonnes (in milled equivalent), down by almost 3 percent compared with 1999. Despite this sharp decline, rice production was still the second highest on record. The contraction was primarily induced by a decision on the part of farmers to diversify crops in response to the weak rice prices that had prevailed since 1999. In some instances, particularly in the case of China, government policies to cut surpluses contributed to the contraction.

Early indications for the 2001 wheat crop in the Northern Hemisphere which, as of February 2001, was mostly planted, suggest that output could at best remain close to the reduced level of 2000. In Asia, early indications pointed to smaller wheat crops in China, India and Pakistan. In Europe, the wheat area in the EC was expected to decrease while, elsewhere in Europe, some recovery in production could be expected after the drought-reduced output of 2000. In North Africa, conditions for the winter wheat crops were generally favourable and output was expected to recover somewhat. In the Southern Hemisphere, wheat planting for the 2001 harvest was to begin in April.

Regarding 2001 coarse grains, crops were already planted in some of the major Southern Hemisphere producer countries. In southern Africa, output could decline as result of a reduction in area. In South America, growing conditions were generally favourable. Planting of coarse grains in the Northern Hemisphere was to start from around April.

In the Southern Hemisphere and around the equatorial belt, the 2001 paddy season (main crops) was well advanced and harvesting of the crop was expected to begin around March. In the Northern Hemisphere, planting for the 2001 season was to begin only in April and May.

Utilization and stocks

World cereal utilization in 2000/01 was expected to outpace global production for the second consecutive year. Total cereal utilization was forecast to reach 1 909 million tonnes, up 0.6 percent from the previous season, although use for direct human consumption was expected to rise by around 1.2 percent. The most significant increases were anticipated for developing countries in Asia. The animal feed utilization of cereals in 2000/01, on the other hand, was forecast to expand slightly, by about 0.6 percent.

Estimates of the cereal carryover stocks in China (excluding Taiwan Province and Hong Kong Special Administrative Region) have undergone an upward revision since the last issue of The State of Food and Agriculture. The result has been a substantial increase in the estimates of China's inventories which, in turn, have led to noticeably higher figures than reported earlier for global stocks. This one-time adjustment made to the historical series of cereal stocks in China should not be perceived as either a reflection of, or cause for, changes in the market fundamentals.3 In fact, neither the volume nor the direction of annual variations in global stocks changed significantly because of this revision.

World cereal stocks by the close of the seasons ending in 2001 were forecast to approach 640 million tonnes, down by 52 million tonnes or 7 percent from their opening levels, and the lowest in four years. The expected drawdown during the 2000/01 season reflected lower 2000 cereal production and higher expected utilization. The biggest declines in cereal stocks were likely to be in countries where production was forecast to fall the most, namely China and the United States. Total ending cereal stocks in major exporting countries were put at 237 million tonnes, 12 million tonnes below their opening levels. Nevertheless, their share in total global stocks was forecast to rise slightly from the previous year to about 37 percent because of a larger drawdown in other countries.

World stocks of wheat for crop years ending in 2001 were 239 million tonnes, down 7 percent from the previous year. Lower carryovers were expected for all five major exporters, except for the EC. Total coarse grain inventories for crop years ending in 2001 were reported to be 246 million tonnes, down 10 percent from the previous year, mainly as a result of an expected sharp fall (21 million tonnes) in stocks held in China following a drastic decrease in its maize production in 2000. Total stocks in major exporting countries were likely to remain unchanged at around 77 million tonnes. Global rice inventories at the end of the seasons in 2001 were forecast to be 155 million tonnes, approximately 5 percent below their opening level. Most of the reduction was expected to be concentrated in China, following a sizeable cut in production in 2000.

Trade

World cereal trade in 2000/01 was forecast to peak at 236 million tonnes, slightly up from the previous year's record volume, mostly on account of higher demand for coarse grains and rice. The expansion in world cereal imports since 1999/00 would put world trade in cereals at about 25 million tonnes or 11 percent above the average for the previous decade.

World trade in coarse grains in 2000/01 (July/June) expanded to a record level of about 105 million tonnes, 2 percent higher than in 1999/2000. World rice trade in 2001 was also expected to increase by more than 3 percent to 23 million tonnes. By contrast, international trade in wheat and wheat flour (in grain equivalent) in 2000/01 was forecast to decline slightly to 108 million tonnes.

Total cereal imports by the developing countries in 2000/01 were expected to reach 168 million tonnes, which would be above average but slightly below the record volume reached in 1999/00. In value terms, the cereal imports bill of the developing countries was expected to total $23 billion in 2000/01, almost $2 billion or 9 percent more than in 1999/00. Total imports by the low-income food-deficit countries (LIFDCs) in 2000/01 were forecast to be about 70 million tonnes, slightly below the previous year's estimated level. Overall, total cereal import expenses for the LIFDCs as a group were forecast to be $9.5 billion, up by 8 percent from 1999/00, mostly because of relatively stronger prices during the 2000/01 marketing season.

4. FOOD SHORTAGES AND EMERGENCIES

Food shortages caused by natural and human-caused disasters continue to affect many countries in all regions of the world. As of early 2001, there were 33 countries and more than 60 million people facing food emergencies of varying intensity.

In eastern Africa, some 18 million people still rely on food assistance because of the lingering effects of last year's drought, coupled with conflict in some parts. The situation is particularly severe in Eritrea, Ethiopia, Kenya and the Sudan, where recent droughts have sharply reduced food production and killed large numbers of livestock. However, recent rains, and the near-normal rainfall forecast for most of eastern Africa during the March to May 2001 cropping season, have improved the food outlook for the subregion. In Kenya, the severe drought in 1999/00 seriously undermined the food security of nearly 4.4 million people. In Eritrea, more than 1.8 million people are in need of urgent assistance owing to displacement by the war with neighbouring Ethiopia and to drought. The outlook for the 2001 agricultural season remains bleak, with farmers so far unable to return to their farms and large tracts of land still inaccessible because of the risk of landmines. In the Sudan, serious food shortages have emerged in western and southern parts as a result of drought. The continuing civil conflict is aggravating the situation by impeding rural households' cultivation activities. In Ethiopia, a good main season crop has improved the country's overall food availability. However, some 6.5 million people, affected by drought and war with neighbouring Eritrea, are dependent on food assistance. In Somalia, a satisfactory secondary season, preceded by a favourable main harvest, has improved overall food prospects. Consequently, the number of people in need of food assistance has declined from 750 000 to 500 000.

Following severe floods in southern Africa, approximately 900 000 people in parts of Malawi, Mozambique, Zambia and Zimbabwe urgently need humanitarian assistance. Damage to infrastructure and housing as well as serious crop losses are reported in the affected areas. The damage is particularly serious in central Mozambique along the Zambezi Valley. Heavy rains and overflowing rivers have also displaced large numbers of people and damaged infrastructure and crops in Malawi, Zimbabwe and Zambia. In Angola, ravaged by civil-strife and where the number of internally displaced people is estimated to be more than 2.5 million, the food supply situation remains serious. For the subregion as a whole, aggregate cereal production is forecast to decline substantially, reflecting sharp reductions in plantings and lower yields following dry spells and excessive rains. Several countries, including Botswana, Lesotho, Namibia, South Africa and Zimbabwe, expect reduced harvests in 2001.

In central Africa, the food supply situation in the Democratic Republic of the Congo is critical for an estimated 2 million internally displaced people who urgently need food and other humanitarian assistance. However, insecurity continues to hamper relief distribution. In Burundi and Rwanda, despite improved production in the first season of 2001, food assistance is still needed in areas that suffered reduced harvests as a result of drought, and for large numbers of other vulnerable people.

In western Africa, the food supply situation has tightened following reduced harvests in parts of the Sahel, notably in Chad and parts of Burkina Faso. Despite some improvement in food production, Liberia and Sierra Leone remain heavily dependent on international food assistance, while in Guinea rebel attacks in border areas are affecting agricultural activities and have caused population displacements.

In South and East Asia, the food supply situation remains very difficult in several countries, largely on account of natural disasters. In Mongolia, a succession of droughts and extremely cold winters have killed large numbers of livestock, which are the sole source of livelihood and income for more than one-third of the population - mainly nomadic herders. The UN has appealed for international assistance to be provided to the country. In the Democratic People's Republic of Korea, the coldest winter in decades and a reduced harvest in 2000 exacerbated the already precarious food situation that has affected the country for the past six years.

In several countries of the Near East, the livelihoods of millions of people have been affected by a prolonged, severe drought, followed by a harsh winter in some parts. In Afghanistan, freezing temperatures have caused loss of life and exacerbated the very serious food crisis that has emerged after two consecutive years of drought and continuing civil conflict. The drought has seriously affected crops and livestock across the country, leaving more than 3 million people in urgent need of assistance. In Iraq, two years of drought have seriously reduced food production, while in Jordan the drought has severely affected crops and pastures, leaving thousands of herders in need of assistance.

In central Asian countries of the Commonwealth of Independent States (CIS), the effects of the recent severe drought are still being felt. This is particularly true in Armenia, Georgia and Tajikistan, where food assistance continues to be needed for approximately 4 million people.

In Latin America, a series of earthquakes hit El Salvador between early January and mid-February, causing loss of life and extensively damaging homes and infrastructure. Food production and marketing in 2001 will be constrained by the damaged infrastructure. In Bolivia, torrential rains and drought caused localized damage, and the government declared a state of emergency in some of the affected departments. In Haiti, food assistance is needed as a result of chronic economic problems.

In Europe, food assistance continues to be needed for about 1 million vulnerable people in the Balkans, especially in Yugoslavia and the Russian Federation. The flare-up of conflict in The Former Yugoslav Republic of Macedonia is anticipated to increase the number of people in need of assistance.

5. FOOD AID FLOWS

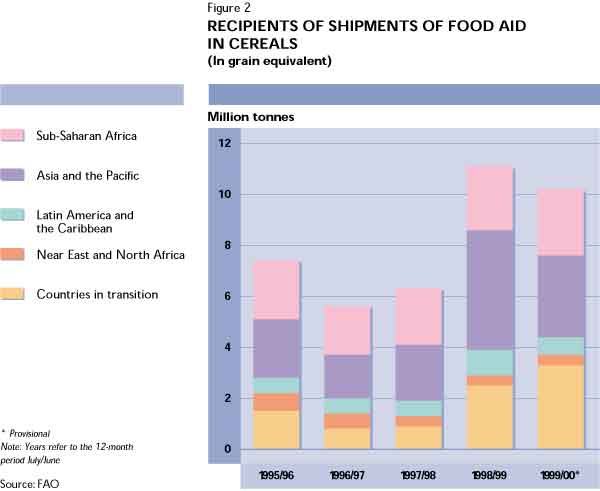

According to the latest information supplied by the World Food Programme (WFP), total cereal shipments in 1999/00 (1 July through 30 June) under programme, project and emergency food aid amounted to 10.2 million tonnes, 800 000 tonnes down from the previous year, despite larger shipments to the Russian Federation.

Cereal shipments from the United States rose to 6.7 million tonnes in 1999/2000, accounting for nearly 65 percent of the world total, up from 58 percent in 1998/99, largely on account of higher shipments to the Russian Federation. By contrast, cereal donations from Japan, mostly rice, declined sharply and those from the EC also fell. Shipments from most other origins remained close to 1998/99 levels.

On the recipient side, shipments to the Russian Federation in 1999/00 soared to 2.4 million tonnes, which was close to the record amount shipped in 1993/94 and up by nearly 500 000 tonnes from the already high level of the previous season.

Excluding the Russian Federation, total food aid shipments to the rest of the world in 1999/00 registered a decline of about 1.3 million tonnes, or 14 percent, to 7.7 million tonnes. Nevertheless, food aid by major donors exceeded the "minimum commitments" agreed under the 1999 Food Aid Convention (FAC) by at least 2.8 million tonnes. The 1999 FAC sets the minimum "guaranteed annual tonnage" at about 4.9 million tonnes (in wheat equivalent), but excludes the Russian Federation from the eligible food aid recipients.

Total cereal shipments as food aid to the LIFDCs in 1999/00 fell to about 7 million tonnes, down by 1.1 million tonnes from 1998/99. Most of the decline was in Asia, while shipments to Africa rose slightly. In Asia, Bangladesh was the largest recipient (964 000 tonnes) followed by the Democratic People's Republic of Korea (733 000 tonnes) and Indonesia (438 000 tonnes). Nevertheless, total shipments to these three countries registered a drop of about 1.4 million tonnes, or 39 percent, compared with 1998/99. By contrast, in Africa, shipments to Ethiopia in 1999/00 doubled from the previous year to 1.2 million tonnes. Rwanda (179 000 tonnes) and Kenya (120 000 tonnes) ranked as the second and third largest recipients in Africa. In Latin America and the Caribbean, cereal shipments to Cuba, Haiti and Honduras increased slightly. In Europe, smaller shipments were made to Albania and Bosnia-Herzegovina but shipments to The Former Yugoslav Republic of Macedonia increased from 6 000 tonnes in 1998/99 to 92 000 tonnes in 1999/00.

Preliminary indications suggest that cereal food aid shipments in 2000/01 could reach 10 million tonnes, close to the estimated volume for the previous year. Shipments to the Russian Federation are forecast to decrease sharply following the improved harvest in that country in 2000. However, food aid needs are expected to be larger, mostly in Africa, but also in the Democratic People's Republic of Korea and the southern countries of the CIS.

According to WFP, total shipments of non-cereals as food aid reached 1.6 million tonnes in 1999 (January-December), 700 000 tonnes, or 80 percent, more than in the previous year and the largest amount in five years. However, in the case of cereals, most of the increase was due to larger shipments to the Russian Federation, which soared from just 400 tonnes in 1998 to a record 800 000 tonnes in 1999. Most of this was accounted for by pulses (595 000 tonnes, mainly from the United States) and meat (159 000 tonnes, mainly from the EC). Total shipments to the LIFDCs rose slightly to 635 000 tonnes.

Among the non-cereal food categories, shipments of nearly all commodities, except for edible fats and vegetable oils, rose in 1999 compared with 1998. Shipments of pulses surged to

1 million tonnes, 133 percent more than in 1998. At this level, food aid in pulses, 85 percent of which originated in the United States, represented 62 percent of the overall total food aid in non-cereals in 1999 and accounted for almost 13 percent of world trade of pulses.

Another major non-cereal food category is meat and meat products. Shipments of these products showed a dramatic increase, from only 4 000 tonnes in 1998 to 163 000 tonnes in 1999, mostly accounted for by larger shipments from the EC.

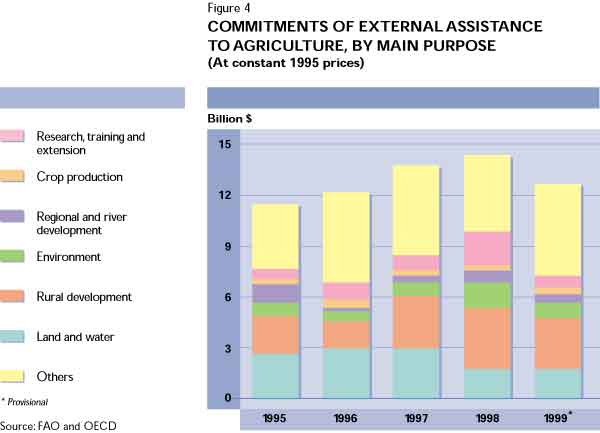

6. EXTERNAL ASSISTANCE TO AGRICULTURE

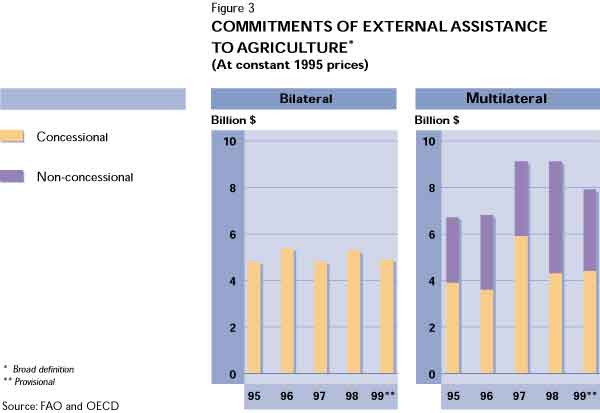

Data available as of February 2001 indicate that, in 1999, $10.7 billion were committed by the major bilateral and multilateral donors to developing countries as official development assistance (ODA) for agricultural development. (At present, the data for 1999 are provisional because complete details regarding the commitments made by Development Assistance Committee [DAC] member countries are not yet available.)

Relative to the $12.6 billion of external assistance committed to agriculture in 1998, the estimate for 1999 constitutes a decline of approximately $2 billion, inverting the upward trend begun in 1995. When measured in real terms (constant 1995 prices), the decline amounts to 12 percent.

About 76 percent of this fall in external commitments to agriculture is attributable to declining assistance from multilateral donors. Overall multilateral assistance, which represents slightly more than 60 percent of the total, appears to have declined from $8 billion in 1998 to 6.6 billion in 1999, a nominal decline of 17 percent. This is largely accounted for by a $1.6 billion (or 33 percent) decline in commitments from the World Bank, which is the main multilateral donor, only partly compensated by an increase of $0.4 billion (or 26 percent) in commitments from the regional development banks.

On the bilateral side, the data indicate a nominal reduction in commitments from $4.6 billion in 1998 to $4.1 billion in 1999, meaning a decline of 11 percent. Australia, Austria, Denmark, Norway and the United Kingdom significantly increased their commitments. However, several countries, including France, Germany, Japan, the Netherlands and Sweden, recorded declining levels of commitments to agriculture in 1999.

In spite of a 9 percent decline in its commitments to agriculture in 1999, Japan remains by far the largest bilateral agricultural donor, while the United Kingdom (after expanding its commitments to agriculture by 25 percent in 1999) overtook the United States and Germany to take second place, leaving those two countries in third and fourth position, respectively. Between them, these four bilateral donors contributed about 72 percent of total DAC bilateral commitments to agriculture in 1999, with Japan accounting for the lion's share (41 percent), and the United Kingdom, the United States and Germany accounting for 12, 11 and 7 percent, respectively.

When external assistance to agriculture is classified in terms of concessionality, the largest part of the decline is accounted for by non-concessional assistance, despite the fact that it has traditionally represented significantly less than 50 percent of total commitments. Thus, non-concessional commitments, all of which were multilateral, declined from $4.2 billion in 1998 to 3 billion in 1999, corresponding to a reduction of 29 percent. Almost all the decline was due to reduced concessional commitments from the World Bank (specifically the International Bank for Reconstruction and Development [IBRD]). At this level, non-concessional commitments corresponded to 28 percent of total commitments to agriculture, compared with 33 percent

in 1998.

Concessional commitments, which represented 72 percent of the total in 1999, declined by 8 percent in 1999 to $7.8 billion, less than the non-concessional commitments, thereby increasing their share of total commitments from 67 to 72 percent. The bilateral part of the concessional commitments declined most sharply, falling by 11 percent to $4.1 billion, while the multilateral part declined by only 4 percent, to $3.6 billion.

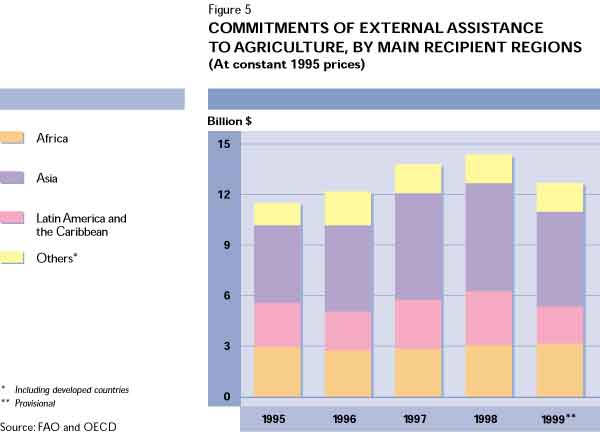

In terms of the destination of assistance, commitments to developing countries, which in 1999 represented 94 percent of the total, declined from $12 billion in 1998 to $10.3 billion in 1999, representing a reduction of 11 percent when measured in real terms. Among the developing country regions, in 1999 Africa experienced an increase in real terms of 6 percent, while levels of assistance in Asia and Latin America and the Caribbean declined by 11 and 33 respectively. Assistance to the transition countries declined for the third consecutive year, falling from about $600 million in 1998 to about 450 million in 1999.

Regarding the sectoral distribution of assistance, commitments to agriculture, narrowly defined,4 increased by 10 percent to $6.3 billion. This represented 59 percent of the total. In the broader definition of agriculture, the most important component is assistance to rural development and infrastructure, which accounted for 24 percent of the total although it underwent an absolute decline of 18 percent from $3.1 billion in 1998 to $2.6 billion in 1999.

7. FISHERIES: PRODUCTION AND TRADE

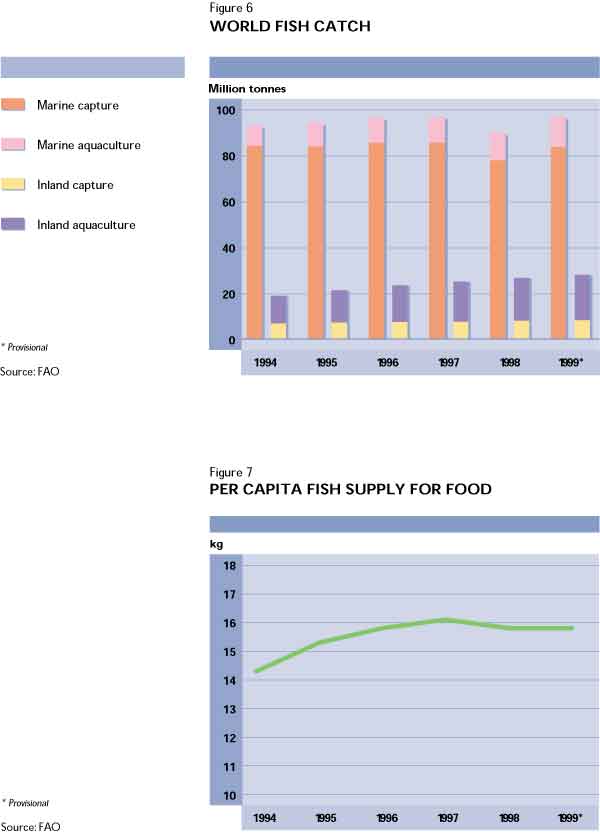

World production of fish, shellfish and other aquatic animals increased from 117 million tonnes in 1998 to 125 million tonnes in 1999. Capture fisheries production amounted to 92.3 million tonnes; although this represents an increase of 7 percent compared with 1998, it is still 1.4 million tonnes below the record levels reached in 1996 and 1997. Aquaculture increased by 2 million tonnes to reach 32.9 million tonnes in 1999.

The increase in landings from capture fisheries occurred as fish stocks in the Southeast Pacific recovered from the effects of the El Niño atmospheric phenomenon, which affected those stocks in 1997/98. Landings of Peruvian anchovy and Chilean jack mackerel, which had decreased to a low of 3.7 million tonnes in 1998, amounted to 10.1 million tonnes in 1999. China reported capture fisheries production of nearly 17 million tonnes in 1999. Other major fish producers were Peru (8.4 million tonnes), Japan (5.2 million tonnes) and Chile (5 million tonnes).

Aquaculture production from both inland and marine waters continued to increase in 1999. The Asian region (particularly China) continued to dominate world production.

In 1999, about 30.4 million tonnes of fish were used for reduction, 6.5 million tonnes more than in the preceding year. Availability of fish for human consumption fell slightly to an estimated 15.8 kg per capita (liveweight equivalent).

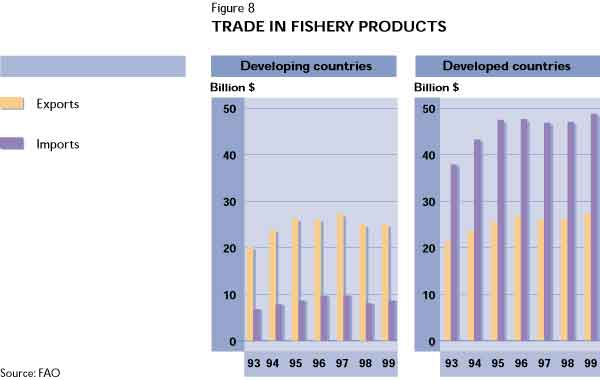

Exports of fish products expanded to $52 200 million in 1999. Developed countries accounted for nearly 85 percent of the value of total imports of fishery products. Japan was again the biggest importer of fishery products, accounting for some 25 percent of the global total, which is a substantial decline from the 30 percent share that this country used to have. Japanese imports of fish and fishery products declined in 1997 and 1998 as a result of the economic recession and have not fully recovered yet. The EC further increased its dependency on imports for its fish supply. Its share in total world imports of fishery products in value terms expanded to 35 percent; however, about half of the EC's imports originate from intra-Community trade. The United States, besides being the world's fourth major exporting country, was the second biggest importer of fish and fishery products in 1999, accounting for 16 percent of the total.

Thailand and Norway are the world's major exporters of fish products in value terms. Together their exports accounted for 15 percent of total world exports. Developing countries continue to record an impressive trade surplus in fish products. The value of their fish exports less the value of their fish imports has now stabilized at between $16 billion and $17 billion per year. Thus, for many developing nations, fish trade represents a significant source of foreign currency earnings.

Shrimp is the most important commodity, accounting for about 20 percent of international trade in value terms. This share remained stable over the past 20 years, despite the substantial changes in trade patterns and supply of fish and fishery products to the world market. Groundfish (i.e. demersal fish) is another important group of species. It accounts for 12 percent of fishery trade. Tuna - traded fresh, frozen or canned - represented 9 percent of the total in 1999. The relative importance of fishmeal and of squid, cuttlefish and octopus has decreased over the past years to reach 3 and 4 percent, respectively, of the value of world exports in 1999. At the same time, however, exports of fresh, frozen, smoked and canned salmon have been increasing, and represented 7 percent of the total in 1999.

8. PRODUCTION AND TRADE OF FOREST PRODUCTS

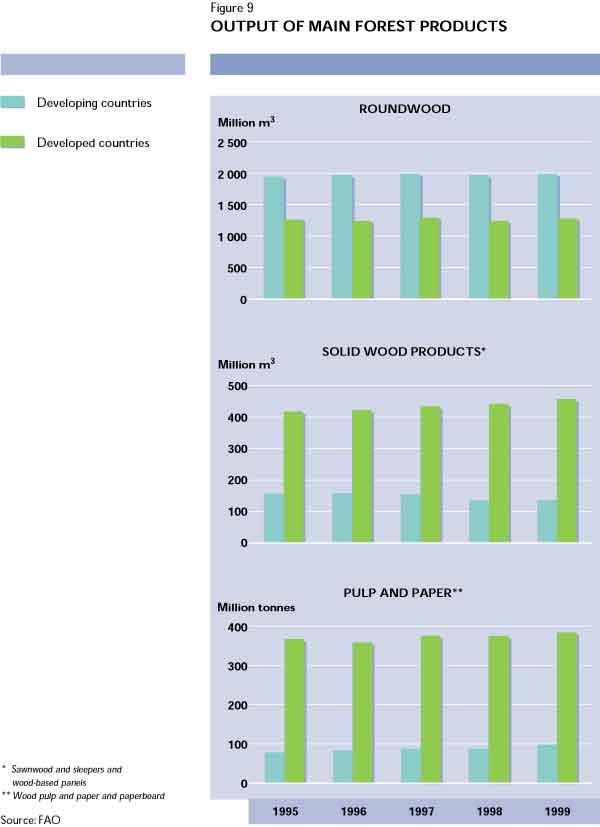

Global markets for forest products recovered slightly in 1999, owing to strong growth in the developed countries and the start of economic recovery in Asia. Overall, global roundwood production increased by 1.5 percent to 3 275 million m3. In the developing countries, which account for about 60 percent of total roundwood production, production increased by 0.9 percent, while the developed countries' production increased by 2.6 percent.

Industrial roundwood production (which excludes the production of wood used for fuel) accounted for about 47 percent of total roundwood production in 1999 and increased by 1.4 percent to 1 525 million m3. Developed countries account for the largest share of industrial roundwood production (about 73 percent) and production in these countries rose by 2.4 percent to 1 117 million m3. Developing countries' production fell slightly from 413 million to 409 million m3.

Global production of solid wood products (which includes sawnwood and wood-based panels) also increased during 1999, rising by 3.2 percent to 590 million m3. Sawnwood production increased by 3.1 percent to 430 million m3, while wood-based panel production increased by 3.5 percent to 160 million m3. Again, the increase in production was led by the developed countries, where production increased by 3.7 percent as opposed to an increase of only 1.6 percent in the developing countries.

Production of pulp and paper also increased in 1999. Overall, global output of pulp and paper products increased by 4.2 percent in 1999 to 480 million tonnes. However, in contrast to the previous year, the developing countries led the recovery. Production of pulp and paper products in the developing countries increased by 11.2 percent in 1999 to just under 100 million tonnes. In the developed countries, there was only a 2.6 percent increase to 380 million tonnes.

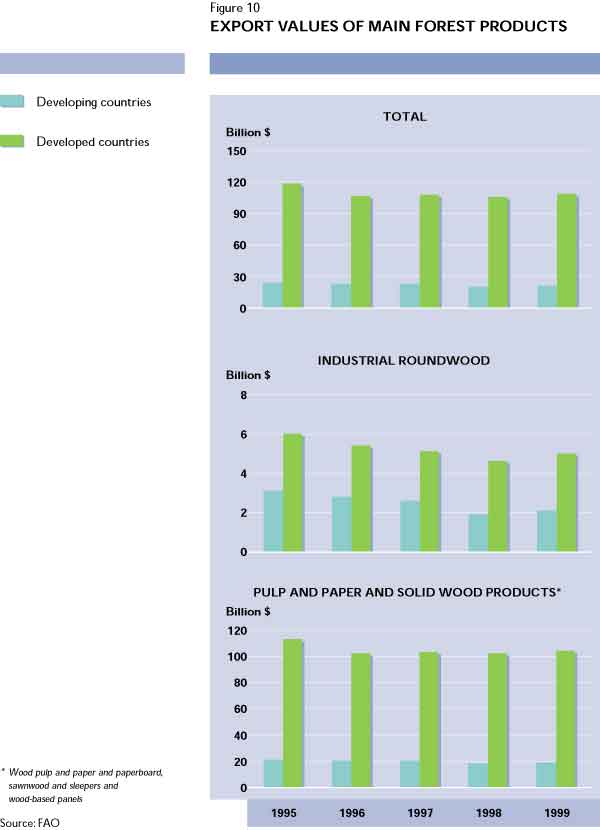

Global trade in forest products also recovered from the poor performance experienced the previous year. A significant proportion of forest products output is traded on international markets each year, including - in 1999 - 30 to 35 percent of sawnwood, wood-based panel and paper production in the developed countries and 40 percent of wood-based panel and wood pulp production in the developing countries. During 1999, exports increased across all regions in the solid wood sector but remained flat in the pulp and paper sector.

The value of global industrial roundwood exports in 1999 increased by 10 percent to $7.2 billion. Exports from the developing countries increased by 12.4 percent in 1999 to $2.1 billion, while exports from the developed countries increased by 8.8 percent to more than $5 billion. These export levels are still well below the averages for previous years.

Exports of sawnwood increased by 6.8 percent to $23.7 billion. Exports from the developed countries increased by 7.9 percent to $20.6 billion and accounted for nearly all of this growth. By contrast, exports from the developing countries increased by only 0.3 percent. In the wood-based panels sector, the opposite situation occurred. Exports increased overall by 11.9 percent to $17.6 billion and developing countries led the way. Exports from the developing countries increased by 25.2 percent to $6.5 billion, while exports from the developed countries increased by only 5.3 percent. Economic recovery in Southeast Asian economies such as Indonesia and Malaysia accounted for much of this growth.

Exports of wood pulp, paper and paperboard in 1999 amounted to just over $81 billion and remained unchanged from the previous year. This situation of zero growth occurred both in developed and developing countries. The volume of exports increased slightly in 1999, but the value of exports remained unchanged because of a slight fall in prices.

{kind=link}