![]()

![]()

![]()

by

Madard Modesta

Tanzanian Fisheries Research

Institute

Mwanza, Tanzania

|

Abstract Under modern conditions of product competition, it is becoming increasingly risky not to innovate and at the same time extremely expensive to innovate. Consumers always want a stream of new and improved products. Competition, among producers is another factor, which will certainly do its best to meet these desires. However, with all the initiatives, there are obstacles to new developments in the Nile perch export industry in Tanzania. It is from this perspective that this paper briefly examines the historical aspects of the emergence of the Nile Perch fillet industry in Tanzania, its main product types and trade routes, the obstacles in new product development and finally the perceived benefits of the factories to the nation. |

1. INTRODUCTION

The fisheries of Lake Victoria in Tanzania contributes significantly to the foreign exchange earnings of the country, earning it an estimated at US$ 14 million in 1994 (Maembe 1997). The Nile perch, the largest of the lake's fish, generate most of this value. Stocks of the species are limited and there is an indication of declining catches (Mkumbo and Cowx, 1999). Based on such findings it is unlikely that additional value will be derived from augmenting landings of the fish any further. An alternative route to improving the value of the fish is through its transformation into various forms. Presently, the extent of such transformation is restricted, and virtually all the Nile perch leaving Tanzania is either chilled or frozen fillet. This paper explores the development of Tanzania's Nile perch filleting industry, examines perceived obstacles to its operation, and considers the development of product lines within the industry.

2. HISTORICAL BACKGROUND

The Tanzanian Nile perch export business started in May 1991 by Mwanza-based companies. Principal buyers of the fish were Kenyan importers, whose equipment - such as insulated collection trucks, ice, weighing scales and selectors at landing beaches - all came from Kenya. At this early stage, ten small companies were involved, all of which exported whole Nile perch to Kenya for further processing and onward export to external markets, primarily Israel.

Prices on Tanzanian landing beaches ranged from US$ 0.08 to US$ 0.16 per kilo and sold to Kenyan buyers for between US$ 0.24 and US$ 0.28 a kilo. Twice a week, trucks with capacity for seven tonnes of fish crossed the border in to Kenya, representing a weekly export of 14 tonnes of fish, or an export from Tanzania to its northern neighbour of around 700 tonnes of Nile perch a year (Batenga, pers. comm.). In Kenya, Nile perch buyers negotiate their prices with landing site co-operatives. In Tanzania, however, there were no co-operatives thus Kenyan fish buyers and collectors found it difficult to deal with individual Tanzanian fishers. They thought it would have been much easier to negotiate the price with co-operative leaders rather than dealing with individual fishers. Tanzanian fishers were, however, only too aware of their poor local market, and had no realistic alternative but to accept the prices offered by the buyers.

It was from these early Kenyan buyers and collectors that pioneer Tanzanian buyers learned their trade, and from whom they adopted the techniques used. These involved the setting up informal credit schemes and incentive systems established with prominent fishers permanently resident on supply beaches. Buyers would make regular visits to potential beaches where they identified fishers with whom to establish supply arrangements. In this way, beaches such as Mwaloni Kirumba, Kayenze, Igombe and Nyashimo came to be known as reliable Nile perch supply points. It was also through this way that dependency relationships were forged between fishers and buyers. Under these arrangements, even slight arrival delays by collection trucks represented large losses to fishers. Conversely, because competition was, at this point, very limited, buyers were able to offer extremely low prices. These mobilisation strategies are still used today by agents for the industrial filleting factories.

These early purchasing companies represent the fore-runners of the Nile perch filleting industry in Tanzania. Low levels of expertise and poor knowledge about the international market for fish were some of the factors, which were responsible for the slow development of the sector. Nevertheless, the establishment of factories did occur and by 1992, there were five Nile perch filleting factories operating in Tanzania several of which had been established with Kenyan capital raised by sister companies located north of the border. Managers within the industry at this time came from a wide diversity of occupations and backgrounds, including cargo and transportation, hotel and manufacturing, marine fish business, a journalist, a publisher, a large bakery, a poultry farmer and a shop owner Additional expertise was obtained from Kenyan sister factories. The early nineties, therefore, represented a transition period for the nascent Tanzanian factories during which they consolidated, trained and established their presence on the local Nile perch markets.

Difficulties were also, at this time, being encountered by the institution in charge of regulating this process, the Tanzania Fisheries Department. Most of the problems that they encountered concerned the failure, by the processing factories, to declare correctly the value of fish exports (under-declaration of exports), failure to pay royalties and the unauthorised export of Tilapia. The relations between the Fisheries Department and the fish processing factories were, in the early 1990s, poor. One respondent for this study explained that the reasons for this were that the Fisheries Department had very limited resources, and were unable to field extension workers to monitor factory activities at landing sites. As a result, fish were loaded without first being inspected. These difficulties were compounded by the Fisheries Department's limited knowledge of the growing Nile perch business and the profit maximisation motives driving industrial owners resulting in the neglect of the required procedure and formalities.

In mid-1994 the export of whole fish and semi-processed fish was officially banned as part of a government policy for the nation's food security. The government decided to take such measures to ensure that maximum earnings to the nation were gained through various taxes and royalties imposed on value-added products, such as processed Nile perch. In addition, the export of Tilapia by processing factories was prohibited, so as to protect local consumers who were unable to compete with the Nile perch fishers the latter who had connections with fish processing factories and who had substantially greater access to all species of fish. These measures were also taken to ensure that Tilapia supplies to local markets were not threatened.

Pressure to establish the ban of whole fish Nile perch exports was brought to bear, in part, by Nile perch processors unable to withstand the competition with their counterparts in Kenya. Kenyan processing factories enjoyed several advantages over their Tanzanian counterparts, not least being physically closer to harbour facilities at Mombasa, as well as the comparatively better Kenyan road infrastructure.

The export of semi-processed fish was allowed until August 1994 so that Tanzanian factories could complete the installation of processing facilities, as well as bringing in refrigeration and food processing experts to guide the process.

3. NILE PERCH FILLET EXPORT ROUTES IN TANZANIA

During the course of the events described above, the principal export routes were road based. There was also some lake-based smuggling of fish from Tanzania in to Kenya, particularly in the Mara/Shirati area, close to the Kenyan border (Wilson, 1996). Presently, export routes within Tanzania depend on three main factors:

The product form: whether the fillet is chilled or frozen.

The availability and status of transport facilities (road, air, railway and water).

The costs associated with the export route (chilled fillet, for example, is more expensive to export than frozen fillet).

As such, distribution channels from Tanzania's Nile perch filleting factories can be categorised along the lines of product type:

The route of chilled fillet

Chilled fillets need to be moved from the factory to final destination as quickly as possible. This distribution channel is therefore characterised mainly by air transport. The country's fish processors have three main routings through which they send their products (Fig. 1). Firstly, the processors may independently or jointly (depending on the cargo volume involved) charter flights directly from Mwanza Airport to the destined foreign market. Secondly, processors may send their fish from Mwanza to Dar es Salaam on scheduled flights, where they can meet scheduled international flights for onward delivery. Four factories interviewed during this survey indicated that this was their principal export route. Thirdly, processors may fly or drive their cargo to Jomo Kenyatta International Airport in Nairobi.

|

Fig. 1 Chilled fish export routes from Tanzania |

The route of frozen fillet

Because of the durability of frozen fish and the development of refrigerated containers, Nile perch processors have several options for sending their frozen Nile perch abroad including by air, road, sea or rail. Three factories in Mwanza have been ferrying their fish to the port at Dar es Salaam using the Mwanza - Dar-es-Salaam rail link. Alternatively, processors can also get their fish to the harbour by road, either via Kenya and then through Arusha, or through central Tanzania, via Dodoma.

|

Fig. 2 The frozen fillet export |

Both rail and road networks can, however, be affected by severe weather. During the 1997-98 El-Nino rains, for example, parts of both the road and the railway to Dar-es-Salaam were washed away, obliging some processors to ferry their frozen fillets to Dodoma by rail, where it would be transferred to trucks for onward delivery to the port. Needless to say, the costs of off-loading and on loading increased considerably as a result.

4. NILE PERCH EXPORT MARKETS AND CHALLENGES IN TANZANIA.

The main export markets for Tanzanian processed Nile perch are in Europe, in particular Holland, Italy and Germany. Other markets lie in the Far East, Middle East, Australia and the United States of America. Products to these markets include frozen and chilled fish and, more recently, head-on gutted fish. Additional Nile perch products, such as belly flaps, maws and off-cuts may also be exported. Maws have a ready market in the Far East, while belly flaps, off-cuts and Nile perch oil are exported to Kenya.

5. OBSTACLES

Transportation problems

Table 1: Tanzanian fish processing factories' major problems (SEDAWOG, 1999).

|

Problem |

Frequency in |

|

Poor infrastructure |

5 |

|

Taxes are too high |

6 |

|

No government assistance |

1 |

|

Poor handling at landings |

1 |

|

Fish supply fluctuations |

1 |

|

Lack of qualified personnel |

3 |

|

Other |

5 |

Many of the problems faced by the fish exporting companies are common to all commercial sectors in Tanzania, besides those problems associated with the perishability of the product. A poor road infrastructure is a major problem faced by fish filleting factories. During the rainy seasons many of the access roads around the Tanzanian part of Lake Victoria become impassable, resulting in delayed deliveries. As a result, rejection rates at the factory increase, a cost that is transferred back to the fisher. The poor quality of roads results in high vehicle maintenance costs.

The air transport and associated facilities are still inadequate in terms of quality and the efficiency of services required for export of fish fillets. The main problems encountered by Tanzanian Nile perch filleting factories are detailed in Table 1.

Water quality

There are three major sources of water for processing fish; namely, lake water, from boreholes, and municipal water. Factory owners reported that, lake water and municipal water are so expensive to purify. The fish factories in Tanzania treat their water by passing it through settling tanks, sand filtering, active carbon filtering and chlorination. Three factories in Mwanza have dug boreholes to the depth of 60-80 m to tap underground reservoirs. This water, the factories claim, is easier and less expensive to purify. The regional Water Department carries out bi-weekly inspections to ensure that all water used meets various health ad safety standards.

Electricity

The factories buy electricity from the Tanzania Electrical Supply Company (TANESCO), the only national power generation company in Tanzania. Electricity supplies to the factories are erratic because of the imbalance between the population growth and industrial growth. Over the past two years, however, supplies have tended to be more reliable. Nevertheless, all factories have stand-by generators in case the electricity supply should falter.

Export market information

Tanzanian Nile perch exporters will gauge the status of their markets from information obtained over the Internet, at international trade fairs, industry literature of the Ministry of Trade, the embassies of the exporting countries, the Fisheries Department and exhibitions. Additional information is also obtained from the buyers to whom the factories sell. Most factory owners claim that the fish market is "buyers market", where-by buyers dictate the standard of quality, the product form, fillet size, packaging requirements and so on. Two factories visited during this survey had experienced visits from their regular foreign buyers to demonstrate how to cut and pack the fish for specific products.

Skills

Factories have experienced considerable problems obtaining suitably qualified personnel for laboratory posts and fish quality control procedures. Five factories visited had their own laboratories. In three cases, the technicians employed came from Kenya, India and Greece. The remaining factories employed Tanzanians.

Employees doing filleting are expected have a basic secondary school education, and to have undergone ‘on the job' training. Training programs for fish filleters are available from the local fisheries training institute Nyegezi Freshwater Fisheries Institute. Some 2 400 filleters have been trained by the institute in fish handling, processing and marketing (Lupondije and Mbilinyi pers. comm.). Factory owners will send their employees to the institute for training, or may ask the institute to train them at the factories.

Export procedures and formalities

In order to export Nile perch products, processing factories have to fulfil a number of basic requirements, the main ones being:

- An export license issued by Ministry of Trade: a licensing procedure established to ensure that there are no restrictions on the product to be exported.

- Customs Entry Forms issued by the Tanzania Revenue Authority (TRA): these documents provide detailed information about the shipment (the export), including the name of the consignor, consignee, the importing country and the type of the cargo.

- Permit for export of fish issued by Fisheries Division: following the payment of export royalties, the Fisheries Division issues an export permit.

- Health certificates issued by the Fisheries Division: these are issued provided the Division is satisfied with the quality of the fish (determined through regular visits to the factories and microbiological analysis of products) and the implementation of Hazard Analysis and Critical Control Point (HACCP) (Lupondije, pers. comm.).

- Exchequer Receipt Voucher issued by the Ministry of Natural Resources: a receipt issued to indicate payment of all necessary export royalties.

The diversity of regulation and the multitude of different government organs to whom the processing factories must apply is problematical. Two of the factories visited suggested the need for a centralised office dedicated to processing fish export formalities. Nonetheless, the factories appear to have adapted to the system, and do not generally have difficulties obtaining the necessary clearances and documentation for fish exports.

The royalty fees

Royalty fees are taxes paid to the state by the processing factories, and which comprise a percentage of the declared f.o.b. price of various fish products. The international prices for Nile perch will vary over time, and hence the government and the factories agree upon a stable price against which the royalties are paid. Thus, it is agreed that, presently, the price for Nile perch fillets is US$ 2.50 per kilo, against which the factories pay 6% of the value of every kilo exported. Such predetermined prices are set against other products such as dried fish maws (US$ 6 per kilo), fish oil (US$ 0.30 a kilo), belly flaps (US$ 0.25), and other products such as fishmeal (US$ 0.20) and fish frames (US$ 0.15). The agreed upon price of the product is reviewed and altered as deemed necessary.

Fish processing factories complain that the royalty fees are too high, particularly when they must also pay other municipal taxes and industrial fees. Kenyan and Ugandan factories do not pay high taxes. The Tanzanian operators therefore complain that they are forced into a disadvantageous position vis a vis other Eastern African competitors.

6. NEW PRODUCT DEVELOPMENT

As mentioned earlier, the dominant products to emerge from the Tanzanian Nile perch processing industry are chilled and frozen Nile perch fillets. Manufacturers in this industry claim that theirs is a ‘buyers market' in which case customers determine the product form. To date, foreign customers have preferred chilled or frozen fillets. The respondents for this study provided several reasons why product development within the industry in Tanzania had focussed almost solely on fillets as opposed to other products, such as fish fingers. The reasons were:

Technology and investment needs for the products are completely different.

Markets were readily available for fish fillets.

Other products need more market survey and research

Buyers gave advice on this product.

It is too expensive to develop the associated communication and infrastructural requirements associated with new product lines.

Because of connections with Kenyan-based sister companies, the marketing of fillets was easier.

Too risky to develop alternative product lines, particularly given insecure foreign markets.

Fillets allow more room for the importing companies to handle consumers needs and preferences.

There have, however, been some developments in the production of alternative product lines. In 1997 the Industrial Fish Processors Association sought permission from the Tanzanian Government to export headed and gutted fish to various markets. Permission was granted by the state provided exports of gutted and headed fish never exceeded 15 per cent of the total export by each factory. This initiative was, in part, motivated by the hope that some degree of product diversification would reduce some of the risks of trading in a volatile global market. At the same time, however, the costs associated with product development are a deterrent to the processing factories, particularly when their production is so frequently subject to closure by EU markets due to the quality of the product.

The recurrent bans on exports of fish to EU markets - such as the most recent ban imposed in April 1999 - have shaken producers' confidence in these markets, with the result that the market is perceived as persistently risky. This perception in turn affects the factories' willingness to develop new product lines.

There are additional factors affecting factories' willingness to develop new product lines. The high fat content of the Nile perch was mentioned as a disincentive that makes it difficult to move away from the traditional fillet forms. The factories have not sought to develop Tilapia-based product lines because of the Tanzanian ban on the export of this fish.

Information on the growth rate, spawning time and fish abundance characteristics particularly of the Nile perch is highly demanded by the fish processors. There is inadequate information on the Lake's ecosystem, information which would enable one to verify if the current investments will be viable in the long-term, whether the resources can accommodate future product development.

Despite these constraints, however, two factories visited had received queries concerning the development of consumer packed products such as breaded fillets or battered fish. While agreeing that it seemed a good idea, the factory owners were worried about the costs associated with such innovation. An important consideration in the development of new product lines lies in persuading a sufficient number of buyers that the product's quality has indeed improved to the extent necessary to motivate its purchase. This is necessary if the costs of the product's development are to be recouped.

Alternatively, improvements can be made to the product's features in terms of real or fancied user benefits, such as designing it in such a way that it offers more convenience, safety or/and efficiency to its consumers. While the styling and improvement of features for food products is difficult, Kotler (1967) points out that these may be ameliorated to some extent by effective packaging design.

Although product development necessarily involves risks, it is generally accepted that the higher the risk the greater the possible benefits or profits. There are also additional incentives to product development such as the future survival of the firms involved. Tanzania's fish firms may, therefore, consider a gradual modification of products rather than an abrupt one, so as to minimise the associated risk. Alternatively, risks might also be reduced by continuing traditional product lines alongside new ones, while also making adequate investments in marketing research.

7. BENEFITS TO THE NATION

Fish processors, feel that their activities are of considerable importance to Tanzania. By driving fish prices up, they argue, incomes to fishers and their communities have improved. Before full processing commenced in Tanzania, Nile perch could be bought at fish landings for as little as Tshs. 80 a kilo (ca. US$ 0.11 at 1999 rates). After processing commenced, prices rose to Tshs. 200 a kilo (ca. US$ 0.30 at 1999 rates). Recently there has been a drop in prices due to the EU ban on fish exports. In towns such as Dar-Es-Salaam a kilo of whole Nile perch (head-off) sells at T.Shs. 800 to 1 200.00 (that is $ 1.0 to 1.4).

The growth of the industry and the provision of both direct employment (within the factories) and indirect employment (in the fisheries as a result of increasing demand) are also viewed as benefits to the nation by the factories. In 1997, the ban on Nile perch exports arising from fears of contamination resulted in the loss of 500 000 jobs, from Tanzania. (The Business Times, 1997). This is equivalent to the total number of people employed directly and indirectly in Tanzania's Lake Victoria fishery (Maembe, 1997; Bwathondi 1998). Significant increases have occurred in Nile perch by-product sectors, such as the collection and drying of fish maws, in fishmeal industries, extraction of Nile perch oil and the processing of fish frames.

Table 2: Ways in which factories feel that they have contributed to national development

|

Developmental contribution |

Frequency |

|

Contributions to fishers' incomes |

6 |

|

Employment generation |

4 |

|

Provision of gear and other inputs |

3 |

|

By-products sold on to local markets |

1 |

|

Other |

3 |

(Source: SEDAWOG, 1999)

The factories' inputs to the fishery in the form of collection and fishing boats, money, ice, storage facilities, road construction to the beaches and collection trucks were also viewed as benefits to the fishery, and are viewed against a backdrop of general developmental benefits accruing to the fishery along with achievements in product handling and improvement. Respondents argued that advances in these ways have served to reduce the amount of post-harvest loss from the fishery, particularly those losses associated with the Nile perch fishery.

The ways in which factories feel that they have benefited the nation are summarised in Table 2.

8. CONCLUSIONS AND RECOMMENDATIONS

There are still challenges in the Nile perch processing industry in Tanzania. Fish stock dynamics within Lake Victoria and the ecological changes taking place in it are not so well known for reliable information to guide product development to be available to potential investors.

Currently, the international market for Nile perch has contributed much to in increasing the relative value of the fishery and has encouraged considerable economic in-migration to it. This has direct implications for over-fishing, and there is still no real information concerning the status of the lake's fish stocks, not least on Nile perch reserves.

Other concerns also exist. An estimated 80 per cent of the Nile perch landed from Lake Victoria is destined for the Nile perch processing factories. The combined whole fish intake of the eight factories visited for this study is an estimated 72 800 tonnes of Nile perch a year against 121 940 tonnes of regional annual fish intake (SEDAWOG, 1999). Adding to this the rise in the market for Nile perch carcasses, this demand has led some observers to speculate about the possible impacts on food security of the trade both within Tanzania (Wilson, 1993) and in Kenya (Abila and Jansen, 1997).

The Nile perch processing industry has created an air of dependency - when the markets close as a result of quality problems, the impacts locally are far-reaching and worrying, with incomes declining, the price of fish crashing and a significant part of the national economy effectively collapsing. There is clearly a need to develop markets outside of the European Union, as well as to consider ways of reducing the dependence on a single source of income for the many thousands of individuals involved in the industry.

The contribution of the industry to the national economy is considerable. Some 500 000 jobs have been created as a result of the industry, and the value of the combined output of the eight factories visited for this study is estimated to be US$ 81.9 million annually (SEDAWOG, 1999). In addition to this are the royalties paid to the state, along with the many indirect benefits in the form of employment or incomes to lake-side communities and the infrastructure developments for fish collection and handling in the fish landing sites.

9. ACKNOWLEDGEMENT

The author grateful acknowledges the support of Lake Victoria Fisheries Research Project (LVFRP) Phase II and Tanzania Fisheries Research Institute (TAFIRI) without these institutions this research would not have been possible. Thanks also go to Fisheries Department, Fresh water Fisheries Training Institute and Fish Processing Firms for enabling this work to be done.

Much is owed to to Prof. Philip Bwathondi, Dr Kim Geheb, Gillian Rodriguez, Oliva Mkumbo and Yohana Budeba for their helpful comments and encouragement in production of this work.

Finally, I cannot forget to express my gratitude to LVFRP-Regional Socio economic Data Working Group, Elizabeth Mlahagwa, in particular for data gathering and entry. The responsibility for all errors remains the author's.

10. REFERENCES

Abila, R.O. and Jansen, E.G. (1997). From local to global markets: the fish exporting and fishmeal industries of Lake Victoria - structure, strategies and socio-economic impacts in Kenya. IUCN Eastern Africa Programme. Socio-economics of the Lake Victoria fisheries: Report No. 2, September 1997. The World Conservation Union, Nairobi.

Business Times (1997). "Mwanza fish ban to cost 500,000 jobs" May 9-15th, 1997

Bwathondi, P.O.J. (1998). Potentials for Acquaculture in Tanzania: LVEMP/TAFIRI Acquaculture Sub-Component: Report submitted to LVEMP Secretariat, Dar Es Salaam, Tanzania.

The Guardian, "Move to avert loss of EU fish market" 27th August 1999

Maembe, T. (1997). Fisheries Management. Paper Presented at the National Workshop to Launch the Lake Victoria Environmental Management Program; Dar es Salaam: mimeo.

Mkumbo, O.C. and Cowx, I. Report on the 3rd FIDAWOG Workshop held at the Triangle Hotel Jinja, 29th March to 1st April 1999. LVFRP/TECH/99/05

SEDAWOG (1999). Marketing survey. LVFRP Technical Document No. 2. LVFRP/TECH/99/02. Jinja, Uganda: Socio-economic Data Working Group, Lake Victoria Fisheries Research Project.

Wilson, D.C. (1993). Fisheries management on Lake Victoria, Tanzania. Paper presented at the Annual Meeting of the African Studies Association, December 4th - 7th, 1993.

Wilson, D.C. (1996). The Critical of Human Ecology of the Lake Victoria Fishing Industry. PhD Dissertation, Michigan State University, U.S.A.

by

Yahya I. Mgawe

Mbegani Fisheries Development

Centre

Bagamoyo, Tanzania

|

Abstract It is generally agreed that bycatch should be utilised rather than discarded at sea. The question is why utilizing bycatch is no longer relevant, particularly to developing countries that are faced with severe food insecurity. Besides the technical difficulties in reducing bycatch in multi-species tropical fisheries, a decline in per capita fish supply in most of these countries justifies increased utilization of bycatch. So far a lot of effort has been made to promote bycatch utilization but with varied results. The basic issue that remains to be resolved is how bycatch could reach consumers in an economical way. This paper argues that a key to this problem in Tanzania and other countries similar in many facets lies with small-scale fish traders. Legal considerations, technical and institutional capacity building in adjacent fishing villages are major pre-requisites. |

1. INTRODUCTION

Tanzania mainland has a population of about 30 million people and occupies a land area estimated at 945 000 km2. Water bodies form 6 percent of the total area of the country, a situation that makes fishing an important activity in providing food fish, employment, income and export earnings. The fishing industry employs about 60 000 fishermen and 600 000 other people in fisheries related activities such as processing and fish distribution. The sector contributes 2-3 percent of the Gross Domestic Product (GDP) and is among the top-five export products in value terms.

The bulk of fish landings, about 85 percent, is obtained from inland water sources. According to FAO (1999), Tanzania is the largest producer of fish from inland capture fisheries in Africa and the fifth in the world after China, India, Bangladesh and Indonesia. Despite its possession of about 800 km of coastline, marine fisheries are less productive due to the narrow continental shelf and a lack of upwelling. As such marine fisheries produces less than 20 percent of the fish in the country. Total fish landings from both marine and fresh water capture fisheries range between 300 000 - 400 000 tonnes per annum. Production from aquaculture industry is very low, standing at about 1 500 tonnes per annum, from a total of about 7 241 ponds scattered all over the country. Artisanal fishermen using dugout and planked canoes are the major source of fish catches contributing more than 90 percent of total landings.

Although Tanzania as a tropical country has multi-species fisheries, only a few species dominate landings in terms of volume. The list includes the Nile perch (Lates niloticus) from Lake Victoria and a group of lake sardines locally known as "dagaa" (Rastrineobola argentea, Stolothrissa tanganicae, Limnothrissa miodon and Engraulicypris sardella) from different lakes. These species together contribute about 50-60 percent of the total fish landings in the country.

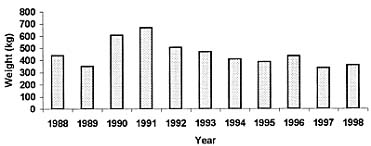

The trend of supply per capita of fish shows a decline over time due to stagnant overall fish supply, population growth rate of 2.8 percent per annum and an export trade that takes away about one third of the landings. Available statistics indicate that fish supplies have declined from a peak of 16 kg/person/year in 1986 to about 6.5 kg in 1998 (Mgawe 2000). There are two prospects for increasing food fish availability to people in the country. It is either to increase production to a level twice the amount being landed or to reduce export and post harvest fish losses.

To increase landings from capture fisheries or aquaculture would probably take longer because it entails resolving problems that have hampered such development projections in the past. Reducing the export trade may appear to be an easy option, but there are problems of low enforcement and institutional capabilities that would make it difficult to implement. The reduction of post harvest fish losses including discards appears to be one of possible immediate options for increasing food fish supply to people. The fisheries policy in Tanzania explicitly outlines the need to improve the utilization and marketability of fisheries products, in order to promote the availability of fish and fishery products particularly to low income group (URT 1997).

2. A GENERAL OVERVIEW OF BYCATCH IN TANZANIA

Bycatch has become a global fisheries management problem. It is estimated that it forms 27 percent of fish being caught globally (Alverson et al 1997). A substantial amount of bycatch is discarded at sea, as fishers concentrate on target species. The use of bycatch reduction devices (BRD) and other selectivity methods have rendered mixed results so far. In temperate areas, where there are a few species with wider size variation such methods have somehow proved effective (Mahika 1995, Larsern 1998). Probably one would not be wrong to suggest that it would take longer before we can have effective selectivity techniques for tropical multi-species fishery. The multitude of species in tropical populations and similarities in size and behaviour make it very difficult to apply the BRDs that are being used in temperate regions. Under these circumstances, the utilization of bycatches is at the moment the ideal proposition. In this regard, the FAO code of conduct for responsible fisheries calls for states to "encourage those involved in fish processing, distribution and marketing to improve the use of bycatch to the extent that this is consistent with responsible fisheries management practices" (FAO 1995:28-29).

In Tanzania, bycatch occurs in both marine and inland fisheries. Shrimp trawling, being the single largest bycatch producer in the country. While most of bycatch produced in the marine industrial fisheries is discarded, incidental catches in fresh water sources are more often retained as they command higher price in the market. For instance, during a period between 1972 and 1985 Nyanza Fishing and Processing Company (NFPC) in Lake Victoria was operating a fishing fleet of four semi-industrial trawlers. The target species was Haplochlomis spp as raw material for an associated fishmeal processing plant. Tilapia (Oreochromis spp), Nile perch (Lates niloticus) and other species were caught as bycatch. These were retained on board and sold at the end of a fishing trip. Similarly, during purse seining operations for "dagaa", (Stolothrissa tanganicae and Limnothrissa miodon,) on Lake Tanganyika, predators such as Luciolates spp are also caught. However, the latter fetches higher price compared to target species, thus they are retained on board. This has left the problem of discards to remain a domain of marine fisheries particularly shrimp trawling.

|

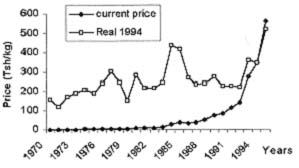

Figure 1: Trend in fish price - Marine fisheries |

|

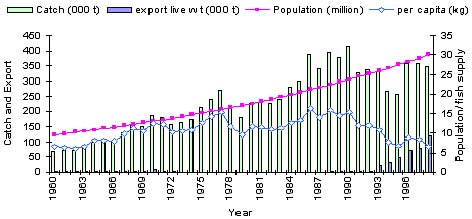

Figure 2: Per caput fish supplies in Tanzania |

With regard to the utilization of bycatch from shrimp trawling, there are indications that there has been a positive trend over the past few years. This could be attributed mainly to increased demand for fish in the country. For instance, the price of fish from the marine fisheries has been increasing both in nominal and real terms, particularly starting from the early 1990s (Figure 1).

As suggested earlier, stagnant supplies from capture fisheries, population growth and export trade of fish, are the main reasons behind increased domestic demand. In addition, an expansion in the global fish market has shifted the Nile perch (Lates niloticus) from domestic to export market. The species constitutes about 25-30 percent of total fish landings in the country. All these factors made fish supply per capita decline to about 6.5 kg/person/year by 1998 (Figure 2).

3. BYCATCH AND DISCARD LEVEL IN THE SHRIMP FISHERY

|

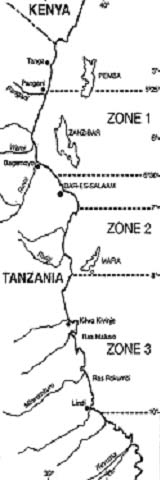

Figure 3: Shrimp fishing zones in Tanzania |

In Tanzania the shrimp fishery started long time ago. Up till 1950s artisanal fishermen were the only ones carrying out the activities. The defunct East African Marine Fisheries Research Organization (EAMFRO) first carried out experiments on shrimp trawling in 1959 (Austrand and Carles 1996). Today, both industrialists using trawlers on inshore waters and artisanal fishermen using dragnets in wading waters carry out shrimp fishing. The total annual shrimp catch is estimated at 2 000 tonnes, half from each of the two segments. Although the total volume seems small, the higher export price of shrimp makes it an economically important fishery to the country.

In the Tanzanian shrimp trawl fishery like many other countries, it is rather difficult to estimate the amount of fish caught as bycatch. Trawler owners and crew are more often unwilling to volunteer information with regard to bycatch for fear that it may jeopardise their trade. The main reason is that most of bycatch is discarded at sea, which is an illegal act. Again, reporting substantial amount of bycatch could lead to the institution of management measures that will be less appealing to short-term benefits of practitioners. Nonetheless, based on estimation that have been made by different researchers, it is evident that substantial amount of finfish is caught as bycatch. Species of fish being caught as bycatch include those of the families Ariidae, Carangidae, Mullidae, Mugilidae and Scianidae. Nkondokaya (1992) reported an average shrimp to bycatch ratio in Bagamoyo and Kisiju grounds (zone 1 and 2 - Figure 3) during August-November period to be in the order of 1:11 and 1:3 respectively. He also estimated the percentage bycatch discarded to be 74 and 82 percent for the two zones respectively. Others have provided rather general estimates with an average ratio of 1: 3- 6 for shrimp and bycatch respectively (Nhwani 1986, Ngoile and Subrimarium cited in Nhwani 1986, Mgawe 1995, 1998, FAO cited in Teutscher 1995).

These estimates are somehow in agreement with the historical catch data from the industry reported between 1984-1987. During this period the landing composition was 1:4 shrimp to fish. The situation, however, changed gradually and today landings comprise of more shrimp than finfish (Figure 4).

The discrepancies in successive years between the estimates of researchers and landing composition of the catch data from industry may have two explanations. It could be due to increased competition in the fishery compelling trawlers to discard more of bycatch or it could be that most of the bycatch being landed is not recorded.

3.1 Increased competition

Before the adoption of trade liberalization policies, in the Structural Adjustment Programme (SAP) of the late 1980s, there was virtually only one active shrimp fishing company in Tanzania, the Fishing Company (TAFICO). TAFICO is a government-owned, parastatal company. As was the case with other such companies in the country, TAFICO used to receive subsidies in different forms including technical and financial support from donors. In view of being a government-owned company and enjoying a monopolistic advantage, TAFICO adhered to the required fishing practices including retention of bycatch. It may be assumed that the 1:4 shrimp to fish ratio realised between 1984-1987 were favourable conditions for the company.

|

Figure 4: Percentages fish and shrimp from shrimp trawlers

in Tanzania |

Following the adoption of trade liberalization policies in late 1980s, many companies entered the shrimp fishery. The Directorate of Fisheries (DOF) instituted some management regulations including, limited licenses, zone system and closed season. These and other regulatory measures (also see Tab.3) made the competition in the industry become more intensive, each company striving to maximise number of fishing days. The competition was heightened by the uncertainties around the renewal of license for next fishing season. The licenses were issued on annual basis and no one was certain whether he would be able to get his fishing license renewed. Hence, each one tried to maximise profit in the current year. Sometimes shrimp trawlers would avoid periodical off-loading of catch in Dar-es-Salaam (Figure3) for fear of loosing time and advantage of good fishing zone. In such cases if a trawler needs to shift to a zone located on another side it would rather choose to discard its fish catch instead of offloading it in the harbour. In this situation the change in landing composition suggesting more shrimp than fish, as presented below (Fig 4), could be expected.

Based on statistics from DOF, the remaining TAFICO shrimp trawlers, MFV/mama TAFICO and MFV/Sadani are now landing the same pattern of shrimp/fish composition like private owned trawlers.

3.2 Under-recording of bycatch landings

|

Figure 5: Average shrimp catch per vessel per day in

Tanzania |

The catch and effort data from the shrimp trawling industry suggests that the shrimp catch per vessel per day started to decline in 1991 (Figure 5). Naturally this situation could have motivated the retention of more bycatch given that demand was increasing, low catches of shrimp naturally providing more room for storing bycatch on board.

Contrary to such expectations statistics from the Directorate of Fisheries (DOF) suggest that between 1991 and 1998 bycatch landings from trawlers have been about 400-1 000 tonnes per year and that the percentage of bycatch component was on the decline (Figure 4).

The official data, however, seems to be composed of bycatch that is landed by respective trawlers at the end of fishing trips (Appendix I & II) and to a certain extent the amount of fish that is collected at sea by authorized fish merchants. It hardly includes an amount collected at sea informally by artisanal fish traders. It is estimated that the latter group lands 700-750 tonnes of bycatch per annum (Mgawe 1995).

Based on the assumed 1:5 shrimp to bycatch estimates, it could be suggested that bycatch volume from both artisanal and industrial shrimp fisheries is in a range of 8 000-10 000 tonnes. Landed bycatch constitutes 25-30 percent of the total amount leaving 70-75 percent discarded at sea.

4. LANDING OF BYCATCH

There are three ways that are used in landing bycatch from shrimp trawlers in Tanzania. These are:

- Landing by a trawler at the end of a fishing trip.

- Collection at sea by authorized fish merchants.

- Collection at sea by artisanal bycatch traders.

4.1 Landing at the end of a fishing trip.

Preservation of bycatch on board a trawler up to the end of a fishing trip is the most acceptable mode of landing in terms of the existing legal framework. Under this system it is easy to monitor the trend in bycatch volume, species composition and size. On the other hand, keeping bycatch up to the end of a fishing trip has its own problems, which include the deterioration of the quality and flooding of the market with bycatch products at landing. Both of the two may lead to a fall in fish price, which demoralizes retention of bycatch in succeeding trips. The crew do not prefer retention of bycatch on board a trawler because in most cases there is no material incentive attached to the system unlike when bycatch is collected at sea.

4.2 Landing by authorized fish merchants.

Rich fish merchants residing in big towns particularly Dar-es-salaam (Figure 3) purchase bycatch from shrimp companies. The fish is collected either at sea or at the harbour when a trawler docks at the end of a fishing trip. Payment is either on cash or credit basis. Prior to embarking on a collection trip at sea, the merchant and trawler owner have to obtain a permit from DOF to allow them tranship the bycatch. Under this system the transactions are carried out in a rather smooth way, since the merchants are well organised and communication between a captain on board and the office at shore renders the operation efficient. This trade is however, very sporadic as merchants would only go to sea when the price of fish in the market is high.

Table.1 Average price of bycatch - 1998

(Tsh/25 kg

sack).

|

Grade |

Lable |

Pieces |

Cost price |

Selling price |

|

1 |

Sorted |

< 6 |

16 000 |

25 000 |

|

2 |

Mixture |

7 to 35 |

12 000 |

17 500 |

|

3 |

Small* |

> 35 |

7 000 |

10 000 |

Source: Adapted from Mgawe ( 1998).

4.3 Artisanal bycatch traders

Artisanal fish traders living adjacent to shrimp fishing grounds have been engaged in bycatch collection since commercial shrimp trawling began in 1960s. Initially, the transactions were primarily based on barter arrangements, whereby villagers would supply provisions such as vegetable, fruits and drinks to get bycatch in return. The fish was more often processed and sold or shared within a village. Sometimes it happened that cured bycatch was sold to nearby hinterland villages. With time however, demand for bycatch increased gradually Source: Adapted from Mgawe (1998). changing the barter arrangement to cash based transactions.

The supply of provisions especially in zone I (Figure 3) is nowadays being regarded as equivalent to cash with the issuance of receipts. This is done before a trader is provided with equivalent amount of fish based on standing price. In most cases the price is harmonised, with different trawlers operating in a particular zone (Table 1). In the southernmost zone (zone 3), however, artisanal bycatch traders may assist in processing fish on board in order to get bycatch.

Table 2: Cost-earnings of bycatch trade - 1998 (750 kg/trip). Unit: Tsh

|

Item |

Grade of fish (see table 1) |

||

|

|

sorted |

mixed |

small |

|

Average income/trip |

750 000 |

525 000 |

300 000 |

|

Purchase of bycatch |

480 000 |

360 000 |

210 000 |

|

Hiring of canoe |

15 000 |

15 000 |

15 000 |

|

Fuel |

5 000 |

5 000 |

5 000 |

|

Transport cost to market (road) |

15 000 |

15 000 |

15 000 |

|

Total variable cost |

515 000 |

395 000 |

245 000 |

|

Surplus to cover fixed cost |

235 000 |

130 000 |

55 000 |

Source:Adapted from Mgawe (1998).

The bycatch market is also shifting from cured fish in adjacent villages to fresh/frozen forms in Dar-es-salaam open market. The number of bycatch collectors is increasing over time particularly in Bagamoyo area (Figure 3). For instance, in 1995 there were 10 artisanal bycatch traders in this area, the number increased to 45 by 1998 (Mgawe 1998). These artisanal fish traders use hired motorized canoes for collection of bycatch at sea. Since there is no reliable communication between the captain on board and these artisanal traders, very frequently, the latter return to the village empty handed. From time to time such cases result in financial problems to the traders. Nevertheless, their presence near the fishing grounds provides artisanal fish traders with opportunity to reduce cost. The cost and earning estimates in bycatch collection suggests that in one trip artisanal traders may earn more than the monthly minimum wage in the country, which is set at Tsh. 35 000 (Table 2).

5. REQUIREMENTS FOR INCREASED BYCATCH UTILIZATION

The best approach to address the question "how to increase bycatch utilization" is probably to start by examining basic problems affecting the main actors. In Tanzanian context, this may include DOF, owners of shrimp trawlers (including crew) and fish traders. The prevailing problems in the present system could be classified into three categories; legal, institutional and technological. These need to be addressed if bycatch utilization has to be promoted further.

5.1 Legal requirements

Table. 3 Indicator and control measures for the industrial shrimp fishery in Tanzania

|

INDICATOR |

CONTROL MEASURE |

|

Catch controls: |

|

|

Monitoring of catches |

End of trip company reports/catch log submitted/.Also radio reports |

|

Landing, transhipments, exports |

Checked in ports by inspectors. Transhipment normally not permitted |

|

On-board inspection |

Observers on-board |

|

Bycatch |

Bycatch must be retained |

|

Effort controls: |

|

|

Limited licenses |

Limited number of licences issued |

|

Vessel sizes |

Size limit of 500 hp and 150 GRT |

|

Time control |

Industrial trawling permitted between 6a.m and 6 p.m only. |

|

Closed season |

December to February (recruitment) |

|

Gear controls |

Mesh size restriction in shrimp trawl fishery |

|

Closed areas/Fishing zones |

Three major fishing zones with more or less equal share of

fishing effort: |

Source: EBCD/GOPA consultants.

The fishing industry in Tanzania is regulated by the Fisheries Act of 1970 (No.6 of 1970), which provides the legal framework for the development and management of the sector. The main regulations in force are the Fisheries Principal Regulations 1989, which lay down different controls such as the licensing rules for fishing vessels, fishermen and fish dealers. It contains a number of prohibitions, restrictions and exemptions, and also deals with offences and penalties.

Despite having the necessary legal instrument, enforcement of regulations to the artisanal fisheries sub-sector has proven very difficult particularly due to lack of funds as well as logistical constraints. As such, it is only the shrimp fishery that is being managed according to conventional management regimes. There are additional specific controls on the shrimp fishery. Some of these management measures are as outlined below (Table 3). Basically the regulations tend to favour bycatch utilization. The only problem is the fact that the legal framework has relied on the vessels landing bycatch at the end of a fishing trip. Although it may theoretically sound ideal and orderly, in practice landing the whole lot of bycatch at the end of a fishing trip has not been easy due to factors outlined in the foregoing. Based on the experience in the country and that from other countries, it seems collecting bycatch at sea is a practical solution (Rakotondrasoa 1995; Mgawe 1995, 1999; López 1999; Suluda, 1999). In this case the present regulations particularly the one on transhipment ought to be re-considered in order to integrate prevailing realities. There is no doubt that permits being issued to fish merchants to allow them collect bycatch at sea, is an important step toward increased bycatch utilization. It should be remembered, however that those merchants are a small group among the traders involved in bycatch collection. The majority of these traders is made up of artisanal fish traders living in villages adjacent to shrimp fishing grounds. These have to be assisted in organising themselves before they could be expected to comply with legal requirements. Unfortunately the present legal framework does not make it possible for extension services to be given these artisanal bycatch traders because their operation remains illegal. This is actually one of the setbacks that has to be addressed if their trade is to be regularized for the promotion of bycatch utilization.

5.2 Institutional requirements

As suggested above, three institutions are directly linked to the promotion of bycatch utilization in Tanzania. These include the Directorate of Fisheries (DOF), Trawler owners (together with crew at sea) and bycatch traders. Each of the institutions has specific objectives and interest in bycatch utilization. The DOF has an obligation to ensure increased food fish availability along side employment opportunities in the fisheries sector. In this case, it is obliged according to her policy, to ensure rational utilization of what is being caught including the incidental catches. The policy and legal framework are consistent with the political will however it has been very difficult to enforce the regulations. The observers' programme on board shrimp trawlers is highly constrained by a lack of financial and human resources. In view of the present enforcement capabilities, discarding of bycatch at sea as well as informal collection by artisanal fish traders would continue. The promotion of institutional capacity building in villages adjacent to shrimp fishing grounds is one way of bringing about order in the trade for the mutual benefit of both parties. Once organised, adherence to rules could be through the application of social pressure of peer groups rather than relying on the more costly and less effective conventional methods of Monitoring, Control and Surveillance (MCS).

Following a decline in catch per unit effort, the shrimp companies would increasingly need the bycatch traders in order to offset production costs. Furthermore the involvement of young men in the bycatch trade would have a reducing effect in the number of those joining the artisanal shrimp fishing. This is very important in minimising the fishing effort on the limited stocks and reducing the inimical biological effects on the biomass. Although it is obvious that trawler owners would like to have more revenue from sales of bycatch, they tend to resent collection at sea by artisanal fish traders. There are many reasons behind such negative and non co-operative attitude. These include the pilfering of the shrimp, the contamination of export products on board and failure by trawler owners to receive the expected revenues due to collusion between untrustworthy crew at sea and traders. In this regard one may expect that the institution of attractive incentive packages may help to enhance collaboration between crew at sea and owners at shore. Such a move would evidently in turn promote the utilization of bycatch.

To fish traders, bycatch collection is a source of employment, income and food. There are differences between rich traders living in Dar-es-salaam and artisanal fish traders living in villages adjacent to fishing grounds. The former group is small, well organised and their trade is rather smooth. On the other hand the latter group comprises of several disorganised traders. Despite their disorganization, however, it is the artisanal traders who are likely to facilitate increased bycatch utilization due to their cost-effective mode of operation. In addition, the experiences from other developing countries confirm that the systems involving small-scale traders are more efficient in collection of bycatch compared to other systems. López (1999) gives an exemplary case whereby the "morralleros" or small-scale bycatch traders in El Salvador have proven to be more efficient compared to operations by a parastatal organization. Based on the experience from Mozambique, Suluda (1999) suggests that it is important to base strategies for the sustainable maintenance of bycatch enterprise at the local level. An FAO project in Madagascar came out with similar observations (Rakotondrasoa 1995). In the case of Tanzania, however artisanal fish traders need institutional support to enable them to be formally recognised thus allowed to operate under the same atmosphere as the rich merchants. This requires the provision of extension services in the respective villages.

5.3 Technological requirements

Regarding technological constraints, the problem of bycatch utilization starts with the limited space on board. Shrimp trawlers operating in Tanzania are small-sized; it is required by regulation that the maximum size should be 150 GRT and 500 HP. The capacities of cold rooms on board the vessels range between 10-30 tonnes. Based on existing storage capacity and average shrimp catch per vessel per day of about 300-400 kg (Figure 5), it is obvious that available space provides for more bycatch to be stored. But this has not been the case because fishers avoid regular off-loading of their catch. They would rather prefer to stay longer at sea in order to maximise the limited number of fishing days allowed per annum. This consequently translates into less space availability for the bycatch.

The preservation of bycatch on board has its own disadvantage particularly in terms of the quality of the product. Under normal operating conditions, the handling of bycatch comes after shrimp has been stored in cold rooms. The time spent on handling bycatch is quite often very short before hauling the next trawl. As a matter of fact washing and storage operations of bycatch are never done properly. The incompletely washed portion of bycatch is packed in sacks before stored in cold store, each sack containing about 25 kg of fish. The remaining fish mostly smaller in size is flushed over board as discards. The retained bycatch is off-loaded at the end of a fishing trip or sold to bycatch traders at sea. With regard to the quality of retained fish, the high bacterial load in the slime of the fish accelerates spoilage; furthermore the slime glues the fish together forming a very hard cluster inside sacks. Difficulties are encountered in thawing and the fish are discoloured both of which lower the quality and thus the price of the product. As a matter of fact, such consequences would demoralise any desire to keep bycatch for a prolonged length of time. The application of chilled seawater is one of other possible options, but the tanks that are needed may lower working space on board beyond the required limits for ensuring safety.

Artisanal bycatch traders prefer to collect frozen fish that has not stayed long in cold rooms, in this way they are able to command high market prices. Sometimes, they are obliged to purchase fish from evening hauls, which is often not frozen compelling increased use of ice. Artisanal bycatch traders prefer to minimise the use of ice. The lack of insulated containers on board artisanal canoe and in the villages forces artisanal fish traders to send the fish to market as quickly as possible even if the market price has dropped. The number of operating days is highly affected by fluctuation of fish price in the open market and more importantly by lack of storage facilities. The use of locally made containers such as "Senegalese type container" could probably bring an improvement to the present situation. At the moment, the conversion of bycatch into value added products such as fish cake and balls seems not to be feasible in Tanzanian context. Not only do the artisanal bycatch traders lack the necessary technological skills but also the market for such products is very limited, confined to few tourist hotels.

6. CONCLUSION

The experience from Tanzania suggests that the utilization of bycatch from industrial shrimp fishery has increased over time as indicated by the number of people involved in the trade. The government has been encouraging bycatch utilization by making laws prohibiting discarding at sea, demanding the whole lot of bycatch to be landed. Certainly the policy and different regulations have made the situation conducive for promoting bycatch utilization. But more importantly, the increased utilization of bycatch in Tanzania has been catalysed by an increased demand for fish and the involvement of artisanal fish traders in collecting the product at sea.

Despite the achievements noted, there are still some legal, institutional and technological requirements that have to be met in order to foster increased bycatch utilization. At the moment, the trawler owners find it difficult to work with disorganised groups of artisanal traders for fear of theft and contamination of the shrimp products on board. In view of this situation, the further promotion of bycatch utilization will occur if the government would continue putting in place favourable regulations and assist local communities in institutional capacity building. The aim should be to organize the artisanal fish traders in such a way that social peer group pressure would act as the policing mechanism to ensure compliance to the code of conduct on bycatch trade. In this case, what is required for Tanzania is collaboration of the main actors in bycatch utilization. This includes the DOF, trawler owners (together with crew on board) and bycatch traders. With regard to technology, the use of improved technologies such as the "Senegalese type container" seems vital in improving the economic performance of artisanal fish traders.

7. REFERENCES

Alverson et al (1994). A global assessment of fisheries bycatch and discards. FAO Fisheries technical paper 339. ROME:FAO.

Austrand, M. and Carles, D. (1996). Tanzania coastline survey - For preliminary shrimp culture site selection (First preliminary report) Addis Ababa:UNECA.

Clucas, I. (1997). A study of options for utilization of bycatch and discards from marine capture fisheries. FAO Fisheries Circular No. 928 FIIU/C 928.ROME:FAO.

FAO (1999). Review of the state of World fisheries Resource: Inland Fisheries. Fisheries circular No.942. ROME:FAO

FAO (1995). Code of conduct for responsible Fisheries.ROME:FAO.

GOPA and EBCD (1996). Feasibility study for SADC Monitoring,Control and Surveillance of Fishing activities: Draft Country Report and Programme Proposal: TANZANIA. GOPA-consultants Hindenburgring 18, 61348 Bad Homburg,Germany/EBCD Rue de la Science 10, 1040 Bruxelles, Belgium.

Kasella, R. and Mgawe, Y. (1997). Bycatch from shrimp trawling in Tanzania. Mbegani FDC (mimeo).

Larsen, R. (1998). Bycatch in fisheries. Norwegian college of fishery science (mimeo) Tromso:NFH.

López, J. (1999). Bycatch utilization in the Americas: An overview. In Clucas, I and F. Teutscher (eds.) Report and proceedings of FAO/DFID Expert consultation on bycatch utilization in Tropical fisheries. Beijing China, Sept 1998. Chatham, UK: Natural Resource Institute.

Mahika, G. (1992). Bycatch reduction by rigid separator grids in Penaeid shrimp trawl fisheries: The case of Tanzania. MPh. Thesis. Norway: University of Bergen.

Mgawe, Y. (2000). Trade-offs in fisheries development: The case of Lake Victoria in Tanzania. MSc Thesis. Norway:University of Tromsø.

Mgawe, Y. (1999). Utilization of bycatch from the fishing Industry in Africa: An overview. In Clucas, I. and Teutscher, F. (eds.) Report and proceedings of FAO/DFID Expert consultation on bycatch utilization in Tropical fisheries. Beijing China, sept 1998. Chatham, UK: Natural Resource Institute.

Mgawe, Y. (1999). Potentials and constraints to increased utilization of bycatch from the shrimp fishery in Tanzania. In Clucas,I and Teutscher, F. (eds.) Report and proceedings of FAO/DFID Expert consultation on bycatch utilization in Tropical fisheries. Beijing China, sept 1998. Chatham, UK: Natural Resource Institute.

Mgawe, Y. (1995). Recent positive and negative experiences in Tanzania with regards to utilization of shrimp bycatch. In FAO/TCDC workshop report and proceedings on utilization of bycatch from shrimp trawlers. Norse Bé, Madagascar. ROME:FAO.

Nhwani, L. and Mwaiko, S. (1986). Monitoring of the Bycatch in the Prawn fishery: second progress report. In Research Bulletin No1 Dar-es-Salaam: TAFIRI

Nkondokaya, S. (1992). Bycatch in Tanzanian shallow-water shrimp fisheries, with special emphasis on finfish. MPh thesis. Norway:University of Bergen.

Rakotondrasoa, M. (1995). Récupération du poisson d'accompagnement de la pêche crevettière - L'expérience malgache. In FAO/TCDC workshop report and proceedings on utilization of bycatch from shrimp trawlers. Norse Bé, Madagascar. ROME FAO.

Suluda, S. (1998). Utilization of shrimp bycatch from the Sofala Bank- Mozambique: Current practices and trends.

Teutscher, F. (1995). Bycatch in tropical fisheries. In FAO/TCDC workshop proceedings on utilization of bycatch from shrimp trawlers. Norse Bé Madagascar. ROME FAO.

United Republic of Tanzania (1997). National fisheries sector policy and strategy statement.

United Republic of Tanzania (1984-1998). Fisheries statistics. Dar-es-Salaam: Fisheries Department.

APPENDIX - I Landings from shrimp trawling

|

Year |

No. of |

Total |

Total |

Total |

Nominal |

Real (=1994) |

|

1984 |

8 |

542 100 |

114 600 |

656 700 |

21 375 400 |

333 990 625 |

|

1985 |

7 |

307 700 |

89 700 |

397 400 |

12 339 205 |

132 679 624 |

|

1986 |

6 |

613 600 |

146 100 |

759 700 |

33 622 830 |

254 718 409 |

|

1987 |

9 |

620 500 |

146 800 |

767 300 |

54 182 740 |

324 447 545 |

|

1988 |

20 |

1 529 786 |

660 239 |

2 190 025 |

318 872 304 |

1 476 260 667 |

|

1989 |

21 |

1 513 696 |

923 919 |

2 437 615 |

486 751 643 |

1 726 069 656 |

|

1990 |

16 |

1 033 248 |

981 956 |

2 015 204 |

475 013 255 |

1 280 359 178 |

|

1991 |

19 |

683 866 |

894 641 |

1 578 507 |

684 102 550 |

1 351 981 324 |

|

1992 |

15 |

533 815 |

585 270 |

1 119 085 |

499 222 560 |

800 036 154 |

|

1993 |

13 |

437 575 |

785 169 |

1 222 744 |

580 371 850 |

756 677 771 |

|

1994 |

16 |

760 236 |

1 026 630 |

1 786 866 |

2 733 826 920 |

2 733 826 920 |

|

1995 |

19 |

974 932 |

958 152 |

1 933 084 |

2 977 394 460 |

2 774 831 743 |

|

1996 |

13 |

649 012 |

782 430 |

1 431 442 |

|

|

|

1997 |

16 |

610 498 |

699 059 |

1 309 557 |

2 463 757 865 |

1 793 127 995 |

|

1998 |

16 |

537 875 |

995 564 |

1 533 439 |

3 734 603 960 |

2 544 008 147 |

Source: Fisheries Division

APPENDIX - II Landings of fish and shrimp by shrimp trawlers in 1998

|

Name of |

Vessel |

Quantity of fish |

Quantity of shrimp |

Total |

Total value |

||

|

wt (kg) |

Value Tsh. |

wt (kg) |

value Tsh |

wt (kg) |

Tsh. |

||

|

Heltanco |

Arusha |

74 675 |

67 207 500 |

87 313 |

285 076 945 |

161 988 |

352 284 445 |

|

Heltanco |

Odysseas |

19 065 |

17 158 500 |

58 220 |

190 088 300 |

77 285 |

207 246 800 |

|

Hondablue |

M/Bahari |

9 250 |

8 325 000 |

19 800 |

64 647 000 |

29 050 |

72 972 000 |

|

Tangol Fisheries |

Banuso II |

34 140 |

30 726 000 |

35 167 |

114 820 255 |

69 307 |

145 546 255 |

|

Tangol Fisheries |

Banuso III |

29 600 |

26 640 000 |

11 795 |

38 510 675 |

41 395 |

65 150 675 |

|

African fishing |

Maendeleo |

33 713 |

30 341 700 |

43 836 |

143 124 540 |

77 549 |

173 466 240 |

|

African fishing |

Marietha |

70 114 |

63 102 600 |

53 129 |

173 466 185 |

123 243 |

236 568 785 |

|

TAFICO |

Mama Tafico |

17 450 |

15 705 000 |

52 006 |

169 799 590 |

69 456 |

185 504 590 |

|

TAFICO |

Sadani |

53 880 |

48 492 000 |

43 291 |

141 345 115 |

97 171 |

189 837 115 |

|

TRAMICO |

Mama Leda |

40 990 |

36 891 000 |

104 485 |

341 143 525 |

145 475 |

378 034 525 |

|

Oceanic |

Tonnes |

93 610 |

84 249 000 |

113 824 |

371 635 360 |

207 434 |

455 884 360 |

|

Fruit der mer |

Sea shore I |

0 |

0 |

65 266 |

213 093 490 |

65 266 |

213 093 490 |

|

Fruit der le mer |

Sea shore II |

7 208 |

6 487 200 |

55 289 |

180 518 585 |

62 497 |

187 005 785 |

|

Fruit der le mer |

Al waly |

45 100 |

40 590 000 |

89 456 |

292 073 840 |

134 556 |

332 663 840 |

|

Sherally |

Victoria IV |

2 370 |

2 133 000 |

38 489 |

125 666 585 |

40 859 |

127 799 585 |

|

Sherally |

Victoria V |

2 140 |

1 926 000 |

60 422 |

197 277 830 |

62 562 |

199 203 830 |

|

Sherally |

Victoria VI |

4 570 |

4 113 000 |

63 776 |

208 228 640 |

68 346 |

212 341 640 |

|

Total 1998 |

16 vessels |

537 875 |

484 087 500 |

995 564 |

3 250 516 460 |

1 533 439 |

3 734 603 960 |

|

Total 1997 |

16 vessels |

610 498 |

366 298 800 |

699 059 |

2 866 141 900 |

1 309 557 |

3 232 440 700 |

Source: URT Fisheries statistics

APPENDIX - III: TANZANIA - Total fish landing, export, import and per caput supply.

|

Year |

Catch |

Population |

Export |

Imports |

For feed |

Per caput |

|

1957 |

63 800 |

8 704 948 |

1 700 |

3 000 |

6 380 |

6.7 |

|

1958 |

63 800 |

8 983 435 |

900 |

3 300 |

6 380 |

6.7 |

|

1959 |

68 800 |

9 270 830 |

1 400 |

2 600 |

6 880 |

6.8 |

|

1960 |

69 100 |

9 567 421 |

2 900 |

3 000 |

6 910 |

6.5 |

|

1961 |

70 700 |

9 873 499 |

2 900 |

2 500 |

7 070 |

6.4 |

|

1962 |

70 800 |

10 178 865 |

3 100 |

2 200 |

7 080 |

6.2 |

|

1963 |

76 600 |

10 493 676 |

2 200 |

1 600 |

7 660 |

6.5 |

|

1964 |

100 200 |

10 818 222 |

2 000 |

1 400 |

10 020 |

8.3 |

|

1965 |

102 900 |

11 152 806 |

2 100 |

1 700 |

10 290 |

8.3 |

|

1966 |

102 000 |

11 497 739 |

2 400 |

1 800 |

10 200 |

7.9 |

|

1967 |

128 400 |

11 853 339 |

2 100 |

2 000 |

12 840 |

9.7 |

|

1968 |

152 100 |

12 219 937 |

2 600 |

2 500 |

15 210 |

11.2 |

|

1969 |

150 200 |

12 597 873 |

4 500 |

2 000 |

15 020 |

10.5 |

|

1970 |

185 000 |

12 987 498 |

8 600 |

2 200 |

18 500 |

12.3 |

|

1971 |

181 400 |

13 389 173 |

4 500 |

2 500 |

18 140 |

12.1 |

|

1972 |

156 900 |

13 803 271 |

2 500 |

2 500 |

15 690 |

10.2 |

|

1973 |

163 300 |

14 230 177 |

1 500 |

4 500 |

16 330 |

10.5 |

|

1974 |

174 059 |

14 670 285 |

1 000 |

2 900 |

17 406 |

10.8 |

|

1975 |

211 506 |

15 124 005 |

800 |

1 900 |

21 151 |

12.7 |

|

1976 |

240 753 |

15 591 758 |

400 |

5 200 |

24 075 |

14.2 |

|

1977 |

270 867 |

16 073 977 |

270 |

3 292 |

27 087 |

15.4 |

|

1978 |

211 098 |

16 571 111 |

154 |

3 689 |

21 110 |

11.7 |

|

1979 |

180 289 |

17 083 619 |

159 |

1 451 |

18 029 |

9.6 |

|

1980 |

227 894 |

17 611 979 |

127 |

804 |

22 789 |

11.7 |

|

1981 |

230 673 |

18 156 679 |

157 |

478 |

23 067 |

11.5 |

|

1982 |

227 779 |

18 718 226 |

91 |

130 |

22 778 |

11.1 |

|

1983 |

239 185 |

19 297 140 |

468 |

195 |

23 919 |

11.1 |

|

1984 |

278 093 |

19 893 959 |

488 |

800 |

27 809 |

12.6 |

|

1985 |

300 752 |

20 509 236 |

664 |

630 |

30 075 |

13.2 |

|

1986 |

386 092 |

21 143 542 |

872 |

na |

38 609 |

16.4 |

|

1987 |

342 528 |

21 797 466 |

1 161 |

na |

34 253 |

14.1 |

|

1988 |

396 924 |

22 471 614 |

2 175 |

na |

39 692 |

15.8 |

|

1989 |

377 773 |

23 166 613 |

2 665 |

na |

37 777 |

14.6 |

|

1990 |

414 112 |

23 883 106 |

2 492 |

128 |

41 411 |

15.5 |

|

1991 |

326 713 |

24 561 283 |

1 850 |

45 |

32 671 |

11.9 |

|

1992 |

335 501 |

25 258 717 |

1 848 |

na |

33 550 |

11.9 |

|

1993 |

331 467 |

25 975 956 |

20 825 |

na |

33 147 |

10.7 |

|

1994 |

268 000 |

26 713 561 |

33 987 |

na |

26 800 |

7.8 |

|

1995 |

258 211 |

27 472 111 |

46 910 |

31 |

25 821 |

6.8 |

|

1996 |

356 800 |

28 252 200 |

71 839 |

19 |

35 680 |

8.8 |

|

1997 |

356 960 |

29 121 322 |

78 792 |

3 |

35 696 |

8.3 |

|

1998 |

348 224 |

30 019 511 |

118 855 |

na |

34 822 |

6.5 |

Sources: Bagachwa et al (1994), Reynolds and Greboval (1989), URT Fisheries statistics, URT- Planning commission (1999), Mgawe (2000). (LWE= live weight equivalent; na = not available).

![]()

![]()

![]()