![]()

![]()

![]()

The production of milk, swine, chicken and eggs has gone through deep transformations over the last three decades. They have all been through a professionalization process. In the swine and poultry raising for slaughter the process was more dramatic than that of the dairy cattle and egg-layers, which also modified their form and production structures, however less severely. A possible explanation for this may be the start point.

The swine and poultry raising have undergone several transformations, being no longer subsistence activities and becoming highly professionalized activities, based on productivity and technology. This change occurred through the action of the processing industries, which have searched for production technology and introduced it in the agricultural properties through the integration system, which began in 1960. This process sped up the adoption of technology by small producers, who received technical support in their farms.

The dairy cattle went through the adjustment process via market competition and many small producers left the activity because they were incapable of adapting to the new technologies. In this in case, the small farmers could not grow by using the technology packages offered by the industry, for the commercial relationship form was simply not based on integration. Small producers depended on their own efforts to get the technology and this was not always viable. The egg-layers raising had a process marked by the development of some very specific communities which were in the integrated trade. The production for subsistence opened space for the industrial-scale production, which was born without contracts and with the small scale commercialization.

The historical evolution of these sectors is devoid of data, for the official statistics are generic and the official data base, very recent, mainly in a process where the government action was distant and little intervening.

2.3.1 Dairy

There are two types of milk producers: the specialized ones and the non specialized one. The latter are the great majority. The Brazilian milk producers from these two groups are in different regions and conditions. For example, in the South, producers can have, with a few specialized cows, a similar production to Center West producers, with large number of cows and low productivity. The producer's production scale definition depends very much on the form of evaluation defined.

According FARINA & JANK (1998), specialized producers have milk production as their main activity, invest in know how, technology, scale economies and product differentiation, and have the activity based on specialized cows from European breeds, whose herd of pure animals is estimated at about one million heads. Although, the authors emphasized that not all the specialized producers reach high productivity or have an adequate return of the investments.

Non specialized producers are those for whom milk is a subproduct of beef cattle (or the contrary, depending on the season), what makes them capable of dealing with wide price oscillations. The mixed heard (milk and beef aptitude) total is about 17 million animals. Also, they work with rudimentary technology, and are the main responsible for the low quality surplus in the rainy season. (FARINA & JANK, 1998).

A clearer definition of this situation can be found in Table 2.11.

Table 2.11 Parameters of the milk production in Brazil (1985 and 1996)

|

DESCRIPTION |

1985 |

1996 |

% |

|

Annual production (Billions of liters) |

12.85 |

17.93 |

39,60 |

|

% of the production from milk cattle |

65.30 |

75.10 |

15,00 |

|

% of the production from slaughter and milk cattle |

11.50 |

7.30 |

-36,90 |

|

% of the production from slaughter cattle and others |

23.20 |

17.60 |

-23,80 |

|

No. milked cows (millions of heads) |

13.40 |

13.70 |

2,50 |

|

Liters/milked cow/day |

2.60 |

3.60 |

36,10 |

|

No. of milk producers (millions) |

1.87 |

1.81 |

-3,10 |

|

Liters/producer/day |

18.80 |

27.10 |

44,00 |

Source: Barros, et al. (2000)

We can notice that in the analyzed period the annual production increased 39.6%, whereas the number of producers fell 3.1%, showing the change in the primary production scale. Another interesting aspect is the increase of 36% in the number of liters/milked cows/day. The reduction in the number of producers and the increase in the average production per producer (which was 44%) are in accordance with the information of the field study carried out by BARROS et al (2000), which indicates that many producers have already abandoned the dairy activity in the areas analyzed in the study.

2.3.1.1 Characteristics of the initial structure of the dairy sector

The Brazilian milk agribusiness system has been through great institutional changes since the early 1990s, with important impacts on its structural organization. The "first revolution", as appointed in JANK (2000), started with the opening of the market and the consolidation of Mercosur, which increased competition with the imported products.

Simultaneously, there was a radical change in the role of the State: after four decades of market regulation, when product prices were controlled by the Federal Government, the prices were completely emancipated (since 1991), and new conditions of relative prices and costs emerged for all the milk agri-chain.

In the mid-1990s, another drastic change - "the second revolution" - took place in the dairy industry and brought on a dramatic impact on the milk system. At this time, the leading companies forced the adoption of a new system for the collection and transportation of raw milk, including milk refrigeration at farm level. As we will point out further ahead, the new technology will concentrate the production at farm level, with important impacts on small producers.

The milk production chain in Brazil is showed in Figure 2.6 and the five main market agents - producers, cooperatives, industries, distributors/representatives and retailers - and the main trade channels are identified.

Figure 2.6 Milk aribusiness in Brazil - trade channels

Source: Barros et al (2001)

The full lines represent the most common trade channels observed and the dotted lines, the alternative channels. The term industry comprises both large industries and industrial plants around the country and small cheese manufacturers and mini-mills (very informal).

The main characteristics of supply, demand, market structure, conduct and performance of this agroindustrial chain are discussed and three main links will be pointed out: the primary milk production, the industry and distribution, and the governmental policies which affect the sector.

2.3.1.2 Characteristics of the initial supply chain for the dairy sector

The milk production in Brazil adopts predominantly the pasture system, which is characterized by the low consumption of off-farm inputs. The inputs used in this activity can be divided into 4 large groups: pasture, food supplements, medicines and genetics.

The milk production is totally connected to the food production for the animals. In the past, pastures were not considered a culture in the agronomic point of view, and, therefore, were little cared for in terms of planting and handling. This view about pastures started to change in the 70s. According to Aronovich (1985), most of the grass used in Brazilian pastures were from the African continent and arrived here in the slave ships, where they were used as bedding.

The first grass to be commercially used in the country was the Melinis minutiflora, also called molasses grass. The easiness in the spreading and the advantage in its production attracted the producer, who accepted it as the first form of planted pasture. However, the improvement of production techniques and the increase in the land price made producers start to use other species of grass which were more productive and resistant to the cold and the draught.

Thatching grass, hyparrhenia rufa, became more popular and offered a new option to the national producer. Although its growth was more difficult than that of molasses grass, its resistance to draughts was higher, having expanded mainly in the first half of the 70s.

A considerable part of the soils where the pastures expanded was previously occupied by woods, and was, therefore, rich in organic matter. In the regions of Presidente Prudente and northern Parana, for instance, the pastures were formed by colonial grass - Panicum maximum. This grass is highly productive, but it is very demanding as to soil fertility, and, therefore, had excellent performances in deforested soils, which were rich in organic matter. However, without efficient nutrients reposition techniques, it lost its productivity.

In the late 70s, EMBRAPA[125] - Campo Grande introduced the Bracchiaria decumbens - bracchiaria -, a less soil-fertility-demanding variety of grass, which adapted even to acid soils and which is planted through seeding.

The production of the pastures had another evolution in the late 80s with the introduction of Bracchiaria brizantha developed by EMBRAPA-Campo Grande. This variety spread quickly due to its capacity of associating high productivity with low soil demand. The development of grass varieties adjusted to Brazilian characteristics and the multiplication easiness of the material resulted in a low adoption cost. This fact enabled the adoption by producers of all levels at very similar conditions. The same types of pastures are found in both small and large farms.

The feed supplementation of the animals is done in two different forms: mineral salts and silage in low productivity months (May the October).The consumption of these products is conditioned to climatic factors. The driest of coldest years demand larger volume of supplementation.

The mineral salt is an element that has had a qualitative evolution process, followed by a market desconcentration process. In the early 70s, producers used common salt (non-minerals-added salt). The formulated mineral salt was at an introductory process. The companies that were involved in this process were: Tortuga, Bayer, Serrana, Manah, Purina, etc. Along the following decade, the mineral salt went through a series of formulation evolutions, being adapted to regional characteristics and to the development of distinct products for the year seasons: draught/winter and summer/rainfall. In the winter the product is added to protein sources, such as animal urea. The large companies modified the participation in this market. Purina and Bayer no longer have this line of products and Manah was purchased by Serrana, which was, in turn, purchased by the Bunge Group. Tortuga remained with a market share of about 30%, having become the largest company in the sector. The other share of the market is supplied by a large number of small regional companies.

The production of mineral salt is affected by the phosphate suppliers, which is the base of the product and is vital to animals, once the poor soils of Brazil lack this element. The phosphate market is dominated by Bunge (Serrana) and Cargill, which produce in Brazil and supply to lots of small companies. Tortuga is a phosphate importer and also has a its own brands and a distribution network.

Silage is basically made of corn and produced in the farms. In this segment, two factors are important: the evolution of production techniques and the varieties of corn developed for this purpose.

Research institutions - EMBRAPA and EPAMIG - and universities - ESALQ, UNESP and Federal Universities of Viçosa and Lavras - had an important role in the introduction and development of this technique in the country, having offered producers the technology and training.

The machines used in the production of silage were imported from Europe and adapted to Brazil and, for this reason, presented severe deficiencies. In the 90s, small Brazilian companies developed equipment for Brazilian conditions, improving the production output.

Varieties of corn were also adapted to the production of silage. EMBRAPA developed hybrids for mass production which were ideal for the silage production as well. The commercial process was made by national companies, amongst which the most important is Agroceres, which was the market leader. In the late 90s, this company lost market share due to appearance of other companies, such as Cargill, Pioneer, Braskalb, Seneca, Colorado, etc. The production pulverization and commercialization process changed in 2000, as several seeds producers were sold to chemicals companies. The highest point in the process was the sale of Agroceres to Monsanto. Other sales also occurred: Seneca and the Braskalb were sold to The Dow Chemical Company, and Colorado and Seneca, to Zeneca. The concentration process followed the same process verified in the chemical industry. Producers of all the sizes use improved corn seeds, once the gains in productivity compensate the higher price.

The genetic material used in the milk production in Brazil came from Europe and India, being the first the widest used one, mainly with the Dutch cattle. The animals' genetic materials were initially imported from the USA and Europe by large producers, who initiated the production of breeders in Brazil, with the support of official research agencies, and created a very small market. The genetic material was in the form of animals and semen. The popularization of the breed happened fast through the very importers, firstly through the sales of breeders. Currently, the import of genetic material occurs mainly through the purchase of semen, and the market leader is ABS. In the genetics market there is a difference between small and large producers. The small ones purchase animals without great concern with genetic description, whereas the large ones purchase semen and animals with a genetic history.

The performance improvement can also be associated with the largest use of mechanic milkers and the more intensive use of tractors and agricultural equipment in the farms. There are no official statistics showing the mechanization in the milk production, because, in Brazil, this activity generally occurs in properties where grains are also produced. But it is a fact that the production has grown exactly in regions were corn, soy and coffee are produced, and where machines and equipment are available. These machinery can also be used in the milk production. Besides the use of this machinery in the production of feed for the flock, the use of the mechanic milker has enabled family properties to remain competitive.

2.3.1.3 Changing structure of the dairy industry

The changing cooperative system. Up to the 1980's, the dairy sector in Brazil was based on a cooperative system, strongly supported by the State, which controlled both producer and consumer prices. With the deregulation and the opening of the economy, many cooperatives were not able to adapt and ended up being sold to entering companies.

In the current structure, unlike the U.S.A., Europe and Australia, milk cooperatives are not the majority in the collection, processing and distribution of dairy products in Brazil. Out of the 12 largest dairy companies only Itambé, CCL/SP and Centroleite are cooperatives. Even so, Itambé was transformed into a corporation and has tried to sell 49% of its stocks. CCL/SP sold part of its assets and brands to Danone; and Centroleite, a virtual cooperative that represents 13 small cooperatives in the state of Goiás, has had lots of difficulties to stay in business as it does not process raw material and its task is only the sale of milk production surplus generated by its member-cooperatives to the spot market.

Again regarding the 12 largest dairy companies, two others were cooperative until the early nineties. However, Elegê, the fourth largest milk collector in Brazil, was sold to the Chinese group Avipal, while Batavo, the sixth largest collector, was sold to Parmalat.

Some factors can be described to explain this Brazilian characteristic. The first one regards the behavior of the cooperated producer. As the price of the raw material oscillates very much along the years, truly private companies strategically act as collectors, considering their short-term necessities. Thus, when the product is scarce, these companies offer a better price for the raw material than cooperatives. When there is product surplus, these companies lower the price, stimulating the producer to supply to the cooperative. In turn, the cooperative has complicated the collection problem, for it is compelled to receive all the milk supplied by the producer. This situation elevates its transaction costs and hinders an effective long-term planning for to enlarge its market share.

A second explanation is related to the fact that the cooperatives delayed the adoption of differentiated prices paid for the raw material. Since the mid-nineties, private companies have paid the producer according to produced volume and cooled milk, paying different prices according to the supplier. In the cooperatives this procedure was controversial and Itambé, for example, was prosecuted in the CADE (Administrative Council of Economical Defense), the official agency in charge of decisions concerning market regulations in Brazil. In 1999, CADE was favorable to the payment of differentiated prices by cooperatives, as the private companies had done for five years. The payment of the same price to all producers made large producers leave the cooperatives and their production was absorbed by private companies. This elevated the cost of milk collection and caused a high instability in collected volume, since the producers with at lower output present a higher offer variation, because they posses less technology (they have difficulties in adopting techniques of feed supplementation).

One third motivation concerns the fact that, in general, the single cooperatives have small industrial plants and produce low-value-added products for a regional market with their own brands. The raw material surplus is taken to the central cooperative, which withholds competitive plants and national brands. With the changes in course in the Agro-industrial Milk System, the central cooperatives such as Itambé and CCL/SP, for example, have resisted to the adoption of logistic procedures, what would imply in the closing of cooling stations, small plants and find new collection routes, as well as extinguishing management positions and reducing costs with staff. When this is partially possible, the central cooperative must remunerate the single cooperative in 5 to 10% in the price of milk, even if it has not had any direct involvement in the collection stage. This increases the final cost of the raw material and, at the same time, lowers the value received by the producer, stimulating even more the leaving of larger producers.

The fourth factor is the definition of the prices paid to the producer. In private companies the prices adjustment is fast, considering the market conditions. In the cooperatives the price is defined by its directors, the producers, since they do not have professionals hired to manage them. The definition of prices takes in the market consideration, but has a strong influence from the producers, who only respect their own interests as to the best possible price. The fact is that the cooperatives pay the producer prices at least 10% above of the market price.

A fifth explanation for this loss of competitiveness of Brazilian milk cooperatives is its incapacity of getting the necessary amount of banking loans in order to make industries more automated and with enough working capital. In general, they become indebted and are pressured by the associates to distribute surplus in the end of the year, hindering reinvestments. This set of factors explains the weakening of the Brazilian cooperative system.

The associative system is common among the producers of the Rio Grande Do Sul, Santa Catarina and Paraná, especially among small producers. The production of corn, sorghum and winter forage is done collectively. Groups, generally compounded of five producers alternate in the preparation and the harvest in their properties, what contributes to the reduction in the feed cost. This practice is also used in the semen acquisition and conservation. The same cannot be said about the other Brazilian states, what makes the equipment idle, for example, and forces producers whose machinery is not immobilized to hire services. To solve these problems, producers frequently have to use mechanized patrols of the city halls, what is not satisfactory, for not all the cities have this service available and the other cannot supply all the producers' demand.

Finally the very aggressive and successful process of acquisitions by companies such as Parmalat should be mentioned. It started in 1990 and, in a few years, became the second largest milk collector in the Country, excelled only by Nestlé, who has been in Brazil since 1920. Parmalat changed the competition pattern in the fluid milk sector through massive investments in marketing to establish the brand. Other foreign companies followed Parmalat's steps, reducing even more the space for cooperatives and regional companies.

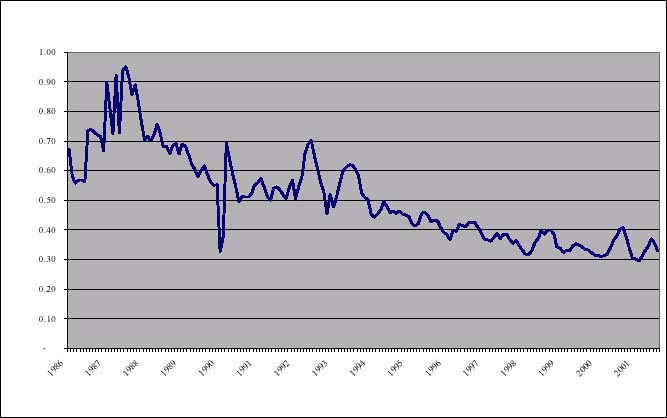

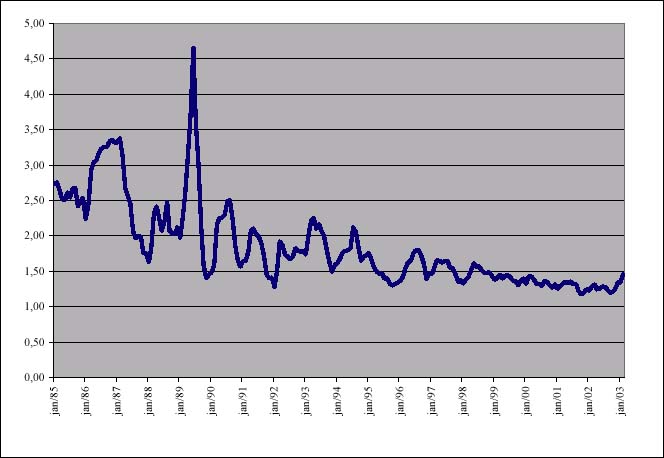

Effect of imports. The impacts of imports on the sector were strong, quick and comprehensive. The massive entrance of imported products, nearly always with more favorable financing conditions to the industry than those of the national product, practically sold at sight, reduced the prices, and promoted the banishment of the less efficient producers. As far as milk is concerned, the Southern region was more intensely affected, since it is closest to Argentina and Uruguay. Thousands of producers are said to have abandoned the activity, regional companies and cooperatives either shut down or were sold. It is important to emphasize that all adjustments were made at decreasing prices, as indicated in the figure.

Figure 2.7 Real milk prices - São Paulo State (R$)

Source: CEPEA/ESALQ/USP

The changes in the market with the commercial opening and the increase in competition led the companies to look for mechanisms to raise productive efficiency. One of the most used alternatives has been the fomentation to development of bulk shipment of refrigerated milk in the process of milk collection. Its advantages to the quality of the raw material and to the logistic efficiency of the industry are so evident that many companies finance the acquisition of the equipment to farmers at zero interest rate due to the reduction of costs in the collection and processing stages. Another option for the companies and cooperatives has been the increase in the average milk collection per farmer, so as to reduce the logistic and transaction costs and to obtain higher quality control by selecting the most professional and capitalized producers. This objective has been reached through the payment of positive price differentials to the larger scale producers, increasing their profitability and making new expansions feasible. The result is the reduction in number of suppliers with an increase in the volume per capita.

Policies government implemented to aid small producers to compete with imports. During the restructuring, not yet completed, especially at the level of the milk producers, financing conditions became a key factor. The main investments by the companies were in acquisitions, whose funds were obtained with the head offices, which were able to mobilize cheap resources in the international financial system. Faced with troubled companies and cooperatives, the banks stopped financing the sector, thus aggravating the farmer's lack of resources. In 1999, the Federal Government established the Pro-Milk, a Program for the Incentive to Modernize Milk Production, to finance with fixed interest rates the necessary investments to the cooling of milk in the farm and in transport. The financing only began to grow, however, when the cooperatives with stable financial situation began to borrow money to pass on to their members charging in product (milk), with no interest rates.

The transformations in all the productive chain have occurred in a quite fast rhythm, leading to the exclusion small and medium dairy producers. This phenomenon may have taken contours of a serious social crisis. However, this would prevent the import of low quality milk from other countries, and would enable Brazil to enter the international market as an exporter, what already happened in 2002 at a small rate. Secondly, inspection is necessary in order to restrain the informal market, which corresponds to 40% of the national production.

In order to avoid that these two actions increase the exclusion of producers from the activity, it is urgent to implant more aggressive programs of agricultural electrification, to permanently create of credit facilities at economically viable interests for investments in gains of productivity, to reduce of the burden of taxes and, basically. A system of price support has been a constant demand of milk farmers. All of these producers' demands are far from becoming a reality, once the government's budgetary restrictions are severe.

2.3.1.4 Effect of changes on dairy production

The impact of the re-structuring process also had an effect on production. Data on the primary milk production in Brazil from the 1985 and 1996 Agricultural census are in Table 2.12. The annual production increased 39.6% in the analyzed period, whereas the number of producers fell 3.1%, showing the change in the primary production scale. It is interesting to consider the 36% increase in the liters/milked cow/day and the increase in the average production per producer (44%).

Table 2.12 Parameters for milk production in Brazil (1985 and 1996)

|

DESCRIPTION |

1985 |

1996 |

% |

|

Annual production (billion liters) |

12.85 |

17.93 |

39.6 |

|

% of dairy cattle production |

65.3 |

75.1 |

15.0 |

|

% of beef and dairy cattle production |

11.5 |

7.3 |

-36.9 |

|

% of production of beef cattle and others |

23.2 |

17.6 |

-23.8 |

|

No. of milked cows. |

13.4 |

13.7 |

2.5 |

|

Liters/milked cow/day |

2.6 |

3.6 |

36.1 |

|

No. of milk producers (million) |

1.87 |

1.81 |

-3.1 |

|

Liters/producer/day |

18.8 |

27.1 |

44.0 |

Source: Barros et al (2000)

The main milk production areas in the country are in the states of Minas Gerais (30% of the national production), São Paulo (10.5% of the national production, especially in the areas of the Paraíba Valley and São Jose do Rio Preto), Rio Grande do Sul (10%), Paraná (10%), and most recently southern and south-eastern Goias (9%). The production in Goias' savannah started after the deregulation of the sector, and most of it was taken to the largest consumer centers of Brazil.

However, according to Barros et al (2000), the organization and relative importance of the production areas are subjected to changes in the increase of sterilized Long-life milk consumption (analyzed along the report). The areas that could be adapted to the new reality of lower prices brought on by the long-life milk were more able to survive and become more important in the national milk production, as southern Goias and São Jose do Rio Preto (SP). More traditional areas, such as the Paraiba Valley in the state of São Paulo and the southern area of Minas Gerais, went through a restructuring. These areas are sources of raw material for Grade C pasteurized milk, which had its market restricted by the industrial strategy of supply control and margin maintenance. Therefore, in traditional areas, where the highest producer price in the whole country has been maintained, a fast strong restructuring of the production systems has occurred, with the vanishing of technological packages that became infeasible with falling prices. In addition to that, there is the proximity of large consumer centers which help in the marketing of the products, but, at the same time, increase opportunity costs of factors of production such as land and labor.

On the other hand, because of the increase in long-life milk production and the demand for lower producer prices, the production amount in areas such as the states of Goias, Rio Grande do Sul or even the city of São Jose do Rio Preto (in the state of São Paulo) should increase steadily.

The number of producers with over 200 heads increased in practically all main areas of the country between 1985 and 1995. In the states of Santa Catarina, the growth is higher than in other areas of Brazil. This shows the growth in scale of Brazilian producers.

In Table 2.13, we can see that the form of scale growth of the two areas did not occur similarly. In the south, the highest growth occurred in the intermediate layer. Even so, almost half the small producers survive within the productive system. In the mid-west, the highest growth occurs in the layer of producers with more than 70 cows. Following the previous trend, in this region is large the participation of producers with a large numbers of cows.

The amount of milk produced by each farm can be slightly different, once, a southern property with a small number of cows can produce a more milk than a large mid-western property. As previously discussed, Center Western producers raise the flock for both milk and slaughter, therefore, losing productivity per cow.

Table 2.13 Number of farmers

|

Year |

Less than 50 - heads |

50 to 70 heads |

More than 70 - heads |

|||

|

|

South |

Midwest |

South |

Midwest |

South |

Midwest |

|

1985 |

74,00% |

15,00% |

9,00% |

17,00% |

18,00% |

69,00% |

|

1996 |

49,00% |

6,00% |

25,00% |

12,00% |

28,00% |

81,00% |

Source: IBGE, Census 1995/1996.

2.3.1.5 The dairy industry and commercial arrangements

Commercial relations. The milk producers' commercial system is different from that of other agricultural segments because producers have to practically deliver their production daily and the payment is received monthly.

On the other hand, the collective acquisition of inputs is not frequent among the producers. One of the factors that could justify this is the inexistence of standardized systems of production in Brazil, what allows producers to adopt different procedures and inputs in each property.

The commercial relations between the industry and milk suppliers are described in the topic about cooperatives and industries.

Current structure of the supply chain. The degree of concentration of the milk supply chain is such that of the total amount of milk produced in 2000 (20 million liters), about 25% were sourced by the 5 major national companies. If only the formal inspected volume is considered, this value goes up to 43%. Table 2.14 shows the sourcing of the major companies for the period of 1996-1998.

According to the data in Table 2.14, whereas formal production decreases in the studied period, there is a high increase in informal production (21%), which affects practically 50% of the total volume produced. Probably, many of the producers who went out of the formal market found the informal one as an alternative to remain in business.

Table 2.14 Evolution of the annual sourcing of the main dairy companies in Brazil liters.

|

|

|

1996 |

1998 |

Variation % (98/96) |

|

1st |

Nestle |

1.431.895 |

1.357.832 |

-5 |

|

2nd |

Parmalat |

795.136 |

814.224 |

2 |

|

3rd |

Itambé |

710.094 |

752.628 |

6 |

|

4th |

Paulista |

668.097 |

625.577 |

-6 |

|

5th |

Elege (Avipal) |

559.653 |

602.514 |

8 |

|

6th |

Grupo Vigor |

301.757 |

287.830 |

-5 |

|

7th |

Batavia/Agromilk |

268.330 |

274.022 |

2 |

|

8th |

Fleischmann Royal |

176.000 |

184.000 |

5 |

|

9th |

Danone |

172.692 |

144.429 |

-16 |

|

10th |

Laticínio Morrinhos |

87.098 |

121.297 |

39 |

|

11th |

SUDCOOP |

111.769 |

115.915 |

4 |

|

12th |

CCPL-RJ |

225.364 |

102.804 |

-54 |

|

Sub-Total (12) |

5.507.885 |

5.383.072 |

-2 |

|

|

Total |

General |

19.021.000 |

20.187.000 |

6 |

|

|

Formal |

11.366.000 |

10.932.000 |

-4 |

|

|

Informal |

7.655.000 |

9.225.000 |

21 |

Source: Jank & Galan (2000)

Over the last few years, there has been a sharp reduction in the number of milk producers. Many authors point out that small producers cannot remain in business due to the implantation, in 1995, of a bulk collection of refrigerated milk, which has lately become more intensive. Table 2.15 shows the evolution of the number of suppliers to the main dairy companies in Brazil.

Table 2.15 Number of suppliers to the main dairy companies in Brazil

|

|

|

1996 |

1998 |

Variation % (98/96) |

|

1st |

Nestle |

39.200 |

28.920 |

-26 |

|

2nd |

Parmalat |

35.846 |

16.052 |

-55 |

|

3rd |

Itambé |

19.927 |

15.369 |

-23 |

|

4th |

Paulista |

25.404 |

22.162 |

-13 |

|

5th |

Elege |

44.000 |

34.402 |

-22 |

|

6th |

Grupo Vigor |

8.368 |

6.442 |

-23 |

|

7th |

Batavia/Agromilk |

11.820 |

10.393 |

-12 |

|

8th |

Fleischmann Royal |

6.000 |

3.000 |

-50 |

|

9th |

Danone |

2.106 |

651 |

-69 |

|

10th |

Laticínio Morrinhos |

4.333 |

4.250 |

-2 |

|

11th |

SUDCOOP |

4.108 |

3.734 |

-9 |

|

12th |

CCPL-RJ |

2.654 |

499 |

-81 |

|

Sub-Total (12) |

203.766 |

145.874 |

-28 |

|

Source: Jank & Galan (2000)

Considering the data in Table 2.15, a large reduction (28%) in the number of suppliers can be seen, whereas there was a reduction of only 2% in the volume collected. In the three years analyzed, 58,000 producers stopped supplying to the twelve largest dairy industries in the country, while the average daily production per supplier increased 37%, as illustrated in Table 2.16.

Table 2.16 Daily volume per supplier of the main dairy companies in Brazil.

|

|

|

1996 |

1998 |

Variation % (98/96) |

|

1st |

Nestlé |

100 |

129 |

29 |

|

2nd |

Parmalat |

61 |

139 |

129 |

|

3rd |

Itambé |

98 |

134 |

37 |

|

4th |

Paulista |

72 |

77 |

7 |

|

5th |

Elege |

35 |

48 |

38 |

|

6th |

Grupo Vigor |

99 |

122 |

24 |

|

7th |

Batavia/Agromilk |

62 |

72 |

16 |

|

8th |

Fleischmann Royal |

80 |

168 |

109 |

|

9th |

Danone |

225 |

608 |

171 |

|

10th |

Laticínio Morrinhos |

55 |

78 |

42 |

|

11th |

SUDCOOP |

75 |

85 |

14 |

|

12th |

CCPL-RJ |

233 |

564 |

143 |

|

Average |

74 |

101 |

37 |

|

Source: Jank & Galan (2000)

Therefore, farmers able to deliver larger daily volumes have replaced smaller producers. Small producers have been going through difficulties due to the tendency to give more importance to the average volume per supplier reflected on the increase of the systems of rewards per volume and quality, and the bulk collection. Whereas the industries compete for the producers with the highest quality and production volume, there is little interest in small volumes due to the costs of collection (Barros et al., 2000).

According to the authors, most of the dairy companies analyzed pay the producers a basic price to which bonuses are added according to the quality and volume collected at the platform. The change in the suppliers' profiles to a smaller group of larger producers takes place, making the sourcing of raw material more efficient.

Impact of these changes and agreements on small-scale producers

Brazil stands out as the country with the highest number of producers and with the lowest average productivity, when compared to the other countries. Likewise, the productivity of the Brazilian herd is the lowest of them.

In the nineties, informal production rose considerably (52%) and the imports of dairy products increased as well (increase of 146%). On the other hand, the growth of formal production was lower. Another trend observed is the large-scale substitution of pasteurized milk (whose production fell 27% in the period) by sterilized milk (long life), which had a 895% increase in the studied period. Table 2.17 illustrates these facts.

Table 2.17 Brazilian market of milk and dairy products - 1990-1998 (in millions of liter equivalent to fluid milk)

|

|

1990 |

1998 |

Variation % (1996/98 over 1990/92) |

|

CONSUMPTION |

15.393 |

22.307 |

36 |

|

Per capita (l/inhabit/year) |

106 |

136 |

28 |

|

PRODUCTION |

14.484 |

20.087 |

29 |

|

Formal |

9.609 |

11.345 |

16 |

|

Pasteurized |

4.030 |

2.745 |

-27 |

|

Long Life |

184 |

3.100 |

895 |

|

Dairy |

5.395 |

5.500 |

9 |

|

Informal |

4.875 |

8.742 |

52 |

|

IMPORTS |

909 |

2.220 |

146 |

|

Long Life/Fluid |

4% |

53% |

|

|

Imports/Formal Market |

9% |

16% |

|

|

Size Informal Market |

34% |

44% |

|

Source: Jank & Galan (2000)

The Brazilian milk market can be divided in two according to data from table, the formal and the informal markets. The formal market is the one where the producer sells his production to organized companies and the product receives sanitary inspection. In this market producers sell their product to companies with the nearest collection station and monthly receive their payment for the production. There is no contract between the parts. Producers receive the price of milk based on the regularity of supply. If the volume is kept stable all through the year, the producer is awarded with a uniform price. If a production is more concentrated in the summer months, the volume that exceeds the winter production average will be paid with discount.

The informal market is the basis of the regional market. This milk is commercialized without the inspection of the federal agency and does not go through the large companies of the sector. Producers commercialize their production directly. The existence of this type of market guarantees a reduction in the power that large companies have on the prices of milk.

2.3.2 Poultry

2.3.2.1 Characteristics of the initial structure of industry

In this part, two considerations are made. The first analyzes the evolution of the chicken processing industry and, the second, the production in the farms. The understanding of the evolution of the industry is fundamental to explain the evolution process of the chicken production in Brazil, once all the process was directed by these companies. They searched the technology in the international market and brought it to the national producer. Moreover, within an extremely unstable economic environment, they guaranteed income stability. This way, the national poultry raising was developed in a productive chain coordinated by the industry, which from the beginning controlled everything including the degree of information of the sector. The public data are scarce and generic, depending much more on the memory of researchers and technicians than on the description of official data.

The production inside of the farm was essential for the maintenance of family agriculture in the south, especially in Santa Catarina and Rio Grande Do Sul, where, with small areas, the integrated producers could keep better standards of living than that offered in the outskirts of large cities (where a great part of people who abandon the rural zone go to). The producer kept a strong symbiotic relation with the integrating companies, therefore the survival of both was conditioned to this relation.

Southern producers had two options: participate of the integration with the companies or the cooperatives or sell the area and leave to the city or unknown Center West regions, where the infrastructure was precarious. In the 80s, the production of grains in the south was not enough to supply the southern demand and the region started to import corn from other regions. A question appeared: should the corn be brought from the Center West or should the chicken production move to the Center West? At first, the industry imported corn, but the growth of the activity in the south would only be viable through the improvement of productivity and not through expansion, which started to occur in the Center West.

In the Center West, the industry found governments that were interested in this expansion, but, at the same time, it found more structured and capitalized agricultural producers. The implantation of poultry farms is an option in the diversification process of the activities of the farm.

2.3.2.2 Characteristics of the initial supply chain for the poultry sector

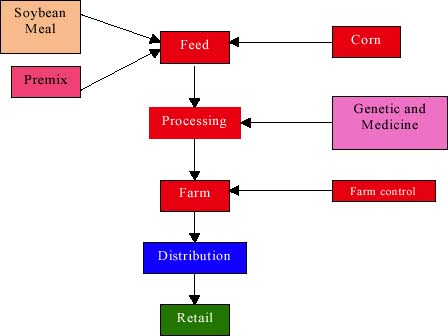

The chicken production process can be divided into the following stages: genetic selection, production of breeders and chicks, growing or fattening, slaughter and commercialization.

The genetic selection stage consists of the attainment of pedigree with individuals of desirable characteristics of weight, physical structure, rusticity, precocity, fertility, food conversion, slaughter age, and so on. This stage of production requires high investments with a long-term return.

According to Bittencourt (1996), this activity is not incorporated in the integration process that characterizes the other stages of production, being predominantly carried through abroad. Few companies do it in Brazil and they are linked to international groups.

The production of breeders and chicks can be divided in the production of two types of breeders: the grandparents and the parents. The grandparents are from the reproduction of the pedigree from the genetic selection process. They originate the breeders used as parents, which are used in the production of commercial young chickens which will become broilers. This activity is part of the vertical integration systems, and a few large companies are in charge of this stage.

Then, there is the growing or fattening stage, which occurs in the chicken farms, where the raising and fattening of the chicks from the earlier stage is done, for the production of broilers. In this segment, there is an intense costs control due to the great consumption of feed, medicines and use of specialized workmanship. In this stage, there is a trend for a non-concentrated production with a large number of integrated producers.

After the production, the chickens are carried to the slaughterhouses to be slaughtered and processed for consumer sale. Approximately 20% of the production is exported, and 80% are commercialized internally.

Through the integrated system of production, the slaughterhouses of the South, which belong to the large enterprise groups of the region, control the production flow along the whole productive chain, getting the chickens from the farms according to their needs. These groups commercialize the processed products, adopting enterprise strategies to increase their market-share (high investments in advertising and brand names, mergers, purchases, etc).

As to the inputs, feed is used from the beginning to the end of the process, representing about 60 to 70% of the total cost of the poultry raising. The feed is basically composed of corn and soy meal, what explains the development of the activity near places where these products are produced (southern Brazil and, more recently, in the Center West).

Figure 2.8 Flowchart of the Productive Chain of Chicken for slaughter

Source: Piedade (1996)

Other important inputs are the medicines and vaccines, which connected to the technical efficiency of the production, mainly to the mortality rate. The integrators to the producers supply all these products.

Scaling up in farm production

Traditionally, the commercial poultry production in Brazil has been based on the "integration" system where small and medium size farmers grow chickens for the large processing industries. In the state of Santa Catarina, for example, a typical farmer would have a building to house 6 ~ 15 thousand chickens [Helfand and Rezende (1998)].

However, as mentioned before, for newer constructions the scale of operation is much larger. Today, the standard building houses 24 thousand chickens, with automatic feeder and controls for temperature, humidity and light. In this sense, it seems that this sector also shows significant economies of scale/size. The trend in the future should be a processing industry integrated with a smaller number of larger farmers.

Table 2.18 presents the evolution of the estimated quantity of chicken in Brazil per stratum of flock size between 1985 and 1995/96. It is quite clear that most of the growth is observed in the larger farms on Center West. In the South the share of small farms grew. Indeed, the size of the chicken flock did not grow much in the strata of flocks smaller than 10 thousand chickens. And, the flock even declined in the strata of flock size smaller than 5 thousand chickens. This is an indication of is a significant increase of scale in this sector.

Table 2.18 Share of farmers by size

|

Year |

Less than 10000 - heads |

More than 10000 - heads |

||

|

South |

Midwest |

South |

Midwest |

|

|

1985 |

2500% |

57.00% |

75.10% |

42.00% |

|

1996 |

31.80% |

21.00% |

68.20% |

78.00% |

Source: IBGE, Census, 1995/1996.

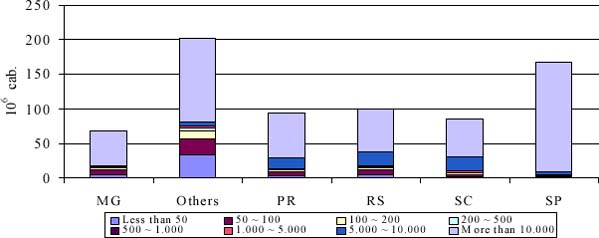

Similar conclusion may be drawn from the data for the major chicken producing states (Figures 2.9 and 2.10). The first point that is worth noticing is the production growth in all the states. Indeed, the expansion of this activity seems to be spread in all the country and not only in certain regions.

Second, in most states, a large part of the expansion is observed in the stratum of the largest flock size. In special, this is quite clear in the states of São Paulo, Minas Gerais and in the 'other states'. On the other hand, it is interesting to notice that the stratum of flock size between 5 and 10 thousand chicken has grown significantly in the states of Paraná, Santa Catarina and Rio Grande do Sul. This was expected, for the farm size in these states is smaller and the expansion of the chicken production in these states in this period targeted this type of farms.

Figure 2.9. Brazil: distribuition of chicken flock by stratum of flock size, per major chicken producing states, 1985.

Source: Censo Agropecuário, 1985. Instituto Brasileiro de Geografia e Estatística (IBGE)

Figure 2.10. Brazil: distribuition of chicken flock by stratum of flock size, per major chicken producing states, 1995/96.

Source: Censo Agropecuário, 1995-1996. Instituto Brasileiro de Geografia e Estatística (IBGE)

Small producers use chicken production as an income complement, combining the production with other activities. The combination of activities depends very much on the localization of the farm, but the range of activities involves corn, milk and slaughter cattle, fruit growing and other annual-cycle agricultural activities.

Technological changes

The expansion and consolidation of the aviculture complex can be explained, mainly, by the diffusion of advanced technology in the areas of genetics, nutrition, handling, health and equipment, which transformed poultry raising into a quite developed industrial activity. The good performance of the chicken production comes, thus, from the constant falls in the prices of the inputs and/or gains of efficiency in the productive chain.

The technological innovations are important both in the bird production phase and in the elaboration of new products. In the first phase, the technology involves processes of genetic development of the pedigree of birds that provide better results of food conversion. Producers, whether integrated or independent, have to search for these technologies in specialized companies.

Table 2.19 Evolution of the food conversion for slaughter chicken

|

Year |

Weight of the chicken (g) |

Feed conversion |

Age (weeks/day) |

|

1930 |

1,500 |

3.50 |

15 weeks |

|

1940 |

1,550 |

3.00 |

14 weeks |

|

1950 |

1,800 |

2.50 |

10 weeks |

|

1960 |

1,600 |

2.25 |

8 weeks |

|

1970 |

1,800 |

2.00 |

7 weeks |

|

1980 |

1,700 |

2.00 |

7 weeks |

|

1984 |

1,860 |

1.98 |

45 days |

|

1989 |

1,940 |

1.96 |

45 days |

|

2001 |

2,240 |

1.78 |

41 days |

Source: Aves e Ovos

The process is initiated with the fertile egg import, which originate the grandparents. The following stage is the parents production phase, which, in turn, give birth to the broilers (commercial birds). The grandparents are normally imported from Europe or the U.S.A. by a major representative company in the country - integrating or independent company. The most significant product in the technological package of the production is the one-day chick, which have a significant weight in the process for they determine the income of the activity through the food conversion.

We can observed extraordinary results in the food conversion, which has been one of the main efficiency indexes of the productive chain. Whereas, in 1930, 3.5 kg of feed was necessary to get 1 kg of poultry, today only 1.96 kg of feed producers for 1 kg of poultry, what was possible thanks to genetically-modified and high-yield parents.

The technology also is present in the process of elaboration (processing and development) of new products. The processing techniques are essential for the maintenance, or even, expansion of the companies market share. Over the last decades, only the large companies of the sector have been able to work in this segment, reducing the commercialization of whole animals and prioritizing the process of products differentiation.

A considerable share of the revenues of the companies of this sector depends on the existing variety of products and by-products of the domestic market. The process of technological evolution in the industry offered the sector the chance to improve the field of by-products, which became value added. The best example of this is the use of carcasses of back, rib, neck and other small cuts in the sausages manufacture.

The industry tries to supply the specific demand of each market. For the Brazilian market, the standard is a 2.5-kg bird (producer level); the international market prefers slaughter or whole chickens. In Table 2.20, the chicken export data from the largest Brazilian companies are presented.

Table 2.20 Participation of the main products exported by company

|

Companies |

Whole chicken % |

Parts % |

Total % |

|

Sadia Concórdia |

28,3 |

13,4 |

22,1 |

|

Perdigão Agroindustrial - SC |

16,7 |

18,9 |

17,7 |

|

Ceval Alimentos S/A |

9,9 |

24,3 |

15,9 |

|

Frangosul S/A |

11,1 |

5,7 |

8,8 |

|

Chapecó CIA Ind. Alimentos |

10,2 |

6,4 |

8,7 |

|

Frigobrás |

8,5 |

5,1 |

7,1 |

|

Perdigão Agroindustrial - RS |

3,6 |

9,2 |

6,0 |

|

Cia. Minuano de Alimentos |

1,5 |

5,7 |

3,3 |

|

Diplomata LTDA |

4,5 |

0,1 |

2,7 |

Source: ABEF

Current structure of the to broiler industry

Amongst the growth strategies of the broiler and swine processing industries is the moving towards savannah areas were large corn and soy producers can be found.

As pointed out before, the feeding of the flock has a great importance in the costs of production (about 2/3 of the total costs), and the search for new regions mainly aims at the supply of grains in more favorable conditions.

Amongst some agroindustries projects, Ceval's (in Barreiras, Bahia), Avipal's (Feira de Santana, Bahia), and Perdigão's Buriti Project, which consists of a full poultry and swine raising integration system in the area of Rio Verde, in Goias are distinguished

Figure 2.11 brings the map with the localization of the chicken and swine slaughterhouses on the space distribution of the annual average production of corn in the Center West, from 1995 to 1999.

Figure 2.11. Map of localization of the chicken and swine slaughterhouses on the space distribution of the annual average production of corn in the Midwest, from 1995 to 1999

Source: Saboya (2001)

The figure shows that the localization of slaughter houses coincide with the main productive areas of corn (especially Goiás and Mato Grosso do Sul).

The analysis of the Buriti project, by Perdigão, made by Favaret & Paula (2000) is interesting because it presents the main decision elements the company considered when looking for the new production expansion region. The main factors for the choice of the place were: availability of grains (basically, corn and soy), supply and quality of the labor, proximity of the consumer market, availability of bovine meat, tax incentives, climatic conditions and infrastructure.

According to Favaret & Paula (2000), the sizing of the projects considered that the original system implanted in the South region - integration with small diversified production farms, using family labor - is depleted. Both the management costs of the thousands of contracts and logistic costs involved (Perdigão has 7,000 integrated producers in the South region) are incompatible with reduced-margins businesses.

Thus, the logistic and technological factors point at significantly higher scale units than the ones of the pioneering regions. In the southern systems, farms keep 6 to 15 thousand chickens, while in the Rio Verde region, farms are bigger, with an average capacity 24 thousand chickens.

One poultry slaughterhouse with capacity to slaughter 281 thousand heads/day; a swine slaughterhouse for 3,500 heads/day; a feed plant for 60 thousand t/month; two breeders farms (1,738,000 eggs/week); a incubator (1,460,000 chicks/week); and 810 integration modules (poultry and swine) are in construction. We can see a sharp fall in the number of integrated producers and the difference in behavior compared to the integrated producers from the South.

The adoption of border technologies (such as automated feeding and climatization) is expected to by homogeneous (since farms will be so), unlike the diversity found in the South, which means contracts standardized and, therefore, lower administrative costs.

Contractual arrangements

There are two production organization systems in the sector of chicken meat: the integrated and the independent one. The size of each system in the productive chain is very questionable, for it depends on the region, but there is an estimate that about 90% of the market it is organized through vertical integration.

Independent poultry raising

The independent breeder has a production system in which each stage of the productive process is not related to the others. In this in case, the producer purchases the necessary inputs to the activity in the market and sells the animals to the slaughterhouses offering the best price, that is, it is a production system, which is typical of other meats, with the inherent market risks.

The commercialization of chicken is done through a direct negotiation between the producer and the slaughterhouse. The purchase prices are gotten by means of direct consultations to the slaughterhouses and some specialized publications. The producer also has bulletins issued by their associations with information on costs and prices of inputs.

Vertical integration

The structure of the poultry raising activity began in the mid-1960s, with the initiative of foreign pedigree-producer companies, which, associated to national groups, brought a developed technology.

A more advanced structure occurred initially in some regions of the South, colonized by European immigrants, thus, initiating the integrated poultry raising in the state of Santa Catarina. In the early 80s, with the retraction of the domestic market and the difficulties of the international market, a generalized decrease in profit margins forced a reorganization towards a production integration in the states of São Paulo and Rio Grande do Sul as well, where a large part of the production was still not integrated.

The Sadia group, leader in the poultry and swine segment (and the fifth largest group worldwide), situated in Concordia, Santa Catarina, pioneered the adoption of the integrated system of poultry production (in 1961), currently having 18,000 (eighteen thousand) integrated producers. Perdigão, the second Brazilian largest poultry and swine producer wines has 7,000 (seven thousand) integrated producers.

According to Favaret Filho & Paula (2000), in the southern states, the integration systems are based on the small-diversified-farm-and-family-labor combination, which allowed the growth of the system to low cost, despite small producers' lack of capital.

However, according to the authors, this integration standard starts to present exhaustion signals, due to logistics costs and the large number of integrated farmers: transporting feed, collecting animals and providing technical support to thousands of integrated farmers, as well as contracts administration and supervision costs have forced large integrating companies to expand the production in new regions.

The system of integrated production propitiated the diffusion of technology along the productive chain, playing a fundamental role in the growth of chicken raising production and productivity in Brazil and around the world; therefore, it is a common system for practically all large producers.

There are some variations in the adopted systems of vertical integration, which are determined within the regional reality. The main variations concern the degree of action of the integrating company and the degree of freedom of the producer within the productive process. The integrator is generally responsible for the technological package, that is, it controls the genetics of the chickens, feed, medicine, technical support and the commercialization. In general, in vertical integrated systems, companies are committed to:

a) supply one-day chicks, feed and medicines;

b) supply technical support;

c) transport chickens and feed;

d) remunerate the integrated farmers in accordance to technical parameters.

The producer is in charge of the fattening of the animals, the physical installation, the services, and water and power supply. The payments normally are based on the market value of the product and in the productivity of the lots. The producer also has the chicken bedding as a source of income, since it is used as fertilizer or animal feed.

There are both advantages and disadvantages in the vertical integration system. As a coordination element of the productive chain, the vertical integration presents the advantage of allowing a fast adaptation process of all the productive chain, given an external shock: decisions about inputs purchase, production volume, products mix and market segmentation are made faster than in the independent production.

For the integrator, the system allows a bigger control of the supply of raw material, assuring the quality and delivery. For the integrated farmer, the advantages are the reduction of the risk of prices, improving in the cash flow, and access to the new technologies, since the technical support given by the integrators is much better than the one given by governmental offices.

On the other hand, some distribution conflicts along the productive chain appeared. The prices paid are normally stipulated by the integrator, and even though they respect the contracts, the producer is not always pleased. The bargain power of the industry is very big, due to the oligopsonist market existing in the chicken market, what can indicate exercise of market power.

The existing integration contracts sometimes hinder the access of new slaughterhouses to the market, since these would not have access to the raw material.

2.3.2.3 Changing the structure of the poultry industry

The initial landmark of the real development of the activity was in the 50s, but one of the sampled industries was founded in 1934 and another one, 1944 - both these units belong to the oldest national companies of the sector. Among the others, two began operations in the 70s, two were implanted in the 80s and one in the 90s, that is, only one of the sampled units was constructed in last the 15 years (see Table 2.21). This panorama shows that the southern industry is relatively old, and that companies have invested little in new plants in the region, having invested only in enlargements and equipment in the existing units.

Table 2.22 shows the age of the industrial slaughter, processing and packing equipment of each sampled industrial unit. We verified that the equipment of the slaughtering sector is about 10 years old, the processing equipment, about 10.3 years old, and the equipment of the packing sector, 8.3 years old. These numbers indicate that, old as the southern industrial units may be, they invested in new equipment in the last decade.

In the Center West, poultry raising for slaughter started to develop only after the late 80s. However, among the five showed industrial units of the Center West, three of them initiated their activities in the 90s, while industry 11 initiated its activities in the 70s and industry 10 initiated the slaughtering in 2000, in contrast with the structure of the southern region. Because of this, the industrial equipment is relatively new.

Table 2.21 Year when Southern and CenterWest agroindustries went into business

|

Company |

Year |

Year |

|

Industry 1 |

1975 |

|

|

Industry 2 |

1934 |

|

|

Industry 3 |

1980 |

|

|

Industry 4 |

1974 |

|

|

Industry 5 |

1972 |

|

|

Industry 6 |

1982 |

|

|

Industry 7 |

N/a |

|

|

Industry 8 |

1944 |

|

|

Industry 9 |

|

1996 |

|

Industry 10 |

|

1992 |

|

Industry 11 |

|

1996 |

|

Industry 12 |

|

2002 |

|

Industry 13 |

|

1972 |

Source: Research data supplied by the companies - N/A = Not available

Table 2.22 Age of the industrial equipment per production sector - southern industries - in years

|

|

Slaughtering |

Processing |

Packing |

|

Industry 1 |

5 |

15 |

6 |

|

Industry 2 |

15 |

5 |

5 |

|

Industry 3 |

20 |

20 |

20 |

|

Industry 4 |

12 |

12 |

12 |

|

Industry 5 |

9 |

5 |

5 |

|

Industry 6 |

4 |

3 |

5 |

|

Industry 7 |

5 |

5 |

5 |

|

Industry 8 |

n/a |

n/a |

N/a |

|

Average |

10 |

10,7 |

8,3 |

Source: research data supplied by the companies - N/A = Not available

The slaughter equipment is about 5.2 years old, the processing equipment, 4.2 years old, and the packing equipment 5.2 years old. We can see, then, that the equipment of the Center West agroindustries is four to five years newer than of that of the southern industries, representing a relevant technological advantage, for if we consider that the lifetime of this equipment is approximately 5 years, on the average, they are all already depreciated. This does not mean they cannot be used for the work, but a possible loss o f competitiveness may happen.

Table 2.23 Age of the industrial equipment per production sector - Center West industries - in years

|

|

Slaughtering |

Processing |

Packing |

|

Industry 9 |

N/a |

N/a |

N/a |

|

Industry 10 |

10 |

10 |

10 |

|

Industry 11 |

1 |

6 |

6 |

|

Industry 12 |

2 |

1 |

1 |

|

Industry 13 |

13 |

4 |

4 |

|

Average |

5,2 |

4,2 |

5,2 |

Source: research data supplied by the companies - N/A = Not available

Although BNDES[126] Sector Report (1995) shows that in the south of Brazil production expansion through large plants did not occur, because of usual fast changes on demand and, therefore, smaller and more flexible plants are preferable, we observe in fact that southern industries present large production scales (Table 2.24).

Table 2.24 Potential and effective daily slaughters of chicken, swine and quail per industry - southern industries

|

|

Potential chicken/day |

Effective Chicken/day |

Potential swine/day |

Effective Swine/day |

Potential quails/day |

Effective quails/day |

|

Industry 1 |

200,000 |

200,000 |

- |

- |

- |

- |

|

Industry 2 |

334,000 |

334,000 |

3,300 |

3,200 |

24,700 |

24,700 |

|

Industry 3 |

261,000 |

261,000 |

1,800 |

1,800 |

- |

- |

|

Industry 4 |

270,000 |

250,000 |

1,700 |

1,500 |

- |

- |

|

Industry 5 |

320,000 |

320,000 |

- |

- |

- |

- |

|

Industry 6 |

280,000 |

200,000 |

- |

- |

- |

- |

|

Industry 7 |

325,000 |

325,000 |

- |

- |

- |

- |

|

Industry 8 |

217,000 |

217,000 |

N/A |

3,300 |

- |

- |

|

Average |

275,875 |

263,375 |

2,267 |

2,450 |

24,700 |

24,700 |

Source: research data supplied by the companies - N/A = Not available

The high production levels point at industries that search scale economies. The southern industries slaughter effectively, in average, 263,375 birds/day; the ones that also slaughter swine reach 2,450 heads/day. Two of them are not using full capacity of production and processing, and industry 4 operates with 92.6% of the productive capacity and industry 6, with 71%. These percentages show that the idleness of the industry is not a relevant question for the sector at the moment, but these are companies which, according to the direction, have projects of increasing participation in the markets where they act. But for this to occur it is necessary to reduce the existing idleness, to improve the physical structures, and the distribution channels.

Some industries search scale profits through the diversification of production in a industrial unit. In the south, industries are characterized for conjugated slaughter of chicken and swine and, in some cases, other animals. Among the sample industries, only two conjugate chicken and swine slaughter, three slaughter chickens only, while only one slaughter chickens, swine and quails.

The slaughter scale in the Center West industrial units is lower than in the south. Table 2.25 indicates that such plants effectively slaughter an average of 165,600 birds a day, practically half of the average effective slaughter of the southern industrial units. Among the interviewed Center West industries, only two plants operate with full productive capacity; the rest operate with an average capacity of 80%, basically due to the existing conditions in these regions, which need cultural adaptations for the handling of the production.

Table 2.25 Potential and effect daily slaughters of chicken, swine and quail per industry - Midwestern industries

|

|

Potential Chicken/day |

Effective Chicken/day |

Potential swine/day |

Effective Swine/day |

|

Industry 9 |

140,000 |

125,000 |

- |

- |

|

Industry 10 |

140,000 |

140,000 |

- |

- |

|

Industry 11 |

70,000 |

60,000 |

- |

- |

|

Industry 12 |

320,000 |

200,000 |

7,000 |

2,800 |

|

Industry 13 |

165,000 |

165,000 |

- |

- |

|

Average |

167,000 |

165,600 |

7,000 |

2,800 |

Source: research data supplied by the companies. N/A - Not available.

The slaughtered birds per day average shows that most Center West industries work with large scales, however not in the rate of the southern industries. However, we must remember that the chicken activity is new in these regions, but tends to grow due to the availability of grains, especially corn and soy, which represent approximately 70% of the chicken production costs. Industry 9, with a small slaughter scale is an example of what can currently be observed in the region: new agroindustries installed in Mato Grosso, Mato Grosso of Sul and Goiás, working in smaller markets which are less accessed by the main companies of the field.

As to the diversification of the plants, we observe that only industry 12 conjugates the slaughter of both chicken and swine. In this case, 2,800 hog heads are slaughtered per day, although the potential is for 7,000 heads/day. Therefore, this is the only company among the interviewed ones that looks for scale profits using this strategy.

Structural changes and policies government implemented to aid small producer to compete

The industry is highly competitive, but the expanding market shows possibilities for the entrance and/or permanence of smaller competitors through product differentiation of specific niches or by geographical questions.

Besides, with the introduction of new technologies, these companies can increase their production, cut costs and improve productivity, what, along with freight costs, will allow them to meet local market preferences of regional consumers in a personalized manner.

The most important national companies are established in market of value-added products or in the international market.

Today, chicken production, as well as the slaughterhouse, which is generally situated near productive areas, are mainly concentrated in the South, most precisely in Santa Catarina, where the traditional leading industries can be found: SADIA, PERDIGÃO, CHAPECO, and CEVAL. In Rio Grande do Sul, we have FRANGOSUL, AVIPAL, and MINUANO.

The distribution of chicken slaughter capacity at national level is shown in Table 2.25, where we can observe that, besides the five largest companies, only two companies have units in areas other than the south and the southeast.

Table 2.26 shows the evolution of the concentration of poultry-swine slaughterhouses in terms of poultry production since 1980. There was an increase in concentration until 1985 and after that a decrease due to small slaughterhouses in São Paulo and Minas Gerais could compete in the domestic market with the larger companies faced financial difficulties related with the economic plans designed to fight inflation.

Table 2.26 Twenty largest poultry companies, 1994.

|

Companies |

State |

Chickens (1000 HEADS) |

Share % |

|

Sadia |

SC, PR, SP, MT |

306.839 |

14,26 |

|

Perdigão |

RS, SC, SP |

140.059 |

6,51 |

|

Ceval |

SC, PR, SP |

103.722 |

4,82 |

|

Frangosul |

RS |

100.950 |

4,69 |

|

Avipal |

RS |

79.569 |

3,70 |

|

Pena Branca |

RS, SP, PA, MA, PE |

70.975 |

3,30 |

|

Chapecó |

SC, SP |

67.201 |

3,12 |

|

Dagranja |

PR, MG |

54.606 |

2,54 |

|

Aurora |

SC |

34.921 |

1,62 |

|

Minuano |

RS |

32.462 |

1,51 |

|

Copacol |

PR |

30.510 |

1,42 |

|

Pif Paf |

MG |

25.938 |

1,21 |

|

Sertanejo |

SP |

25.848 |

1,20 |

|

Batavo |

PR |

24.560 |

1,14 |

|

Agroeliane |

SC |

22.867 |

1,06 |

|

Só Frango |

DF |

17.051 |

0,79 |

|

Coroaves |

PR |

12.808 |

0,60 |

|

Holambra |

SP |

12.700 |

0,59 |

|

Francap |

MG |

12.689 |

0,59 |

|

Languiru |

RS |

11.607 |

0,54 |

|

SUBTOTAL |

|

1.187.884 |

55,20 |

|

Others |

|

964.050 |

44,80 |

|

TOTAL |

|

2.151.934 |

100,00 |

Source: ANAB - Associação Nacional de Abatedouros

Table 2.26. Concentration on poultry industry - the capacity of 4 biggest.

|

1980 |

29,80% |

|

1985 |

48,40% |

|

1990 |

30,20% |

|

1995 |

30,30% |

|

1997 |

26,90% |

|

1998 |

25,90% |

Source: ANAB, in Favaret,2001.

Brazil present large competitiveness in both poultry and swine sectors, which, contrary to what happen to the milk sector, were not affected by negatively foreign competition in the 1990's. The growth of the domestic market after the Real Plan permitted a large expansion of the production thus stimulating investments in this sector. These sectors were the leaders in BNDES financings to the food industry during the second half of the 1990's. Major companies as well as regional companies and cooperatives expanded their production units. The growth of the productive capacity was directed to attend initially the domestic market, and, from 1999 on, to increase exports, due to the exchange rate devaluation. All these changes took place at stable or somewhat decreasing prices.

Merger and acquisitions

The Sadia group is one of the largest foods complexes in Latin America, having a solid reputation of brand quality, leadership in the meats segments, high production scale and an efficient net distribution. It is a leader in the poultry and swine segment in the country, and ranks as fifth largest producer in the world.

The group is formed by 14 companies and 24 industrial units grouped in three business-oriented units: grains and derivatives (commodities), fresh meats and industrialized products. In 2000 it has about 30,000 employees. It has 20 distribution centers in Brazil and 5 abroad (1 in Mercosur). The distribution of its products reaches 150 thousand sales spots in Brazil. As previously said, it is associated through vertical integration with 18,000 agricultural producers.

The process of internationalization of the activities of the group was initiated in the early 90s, when it formed a joint-venture with the largest chickens producer on Argentina (Three Arroyos Farm), forming Sadia Sur. In the same period it opened a commercial office in the United States and inaugurated a distribution center in Argentina.

In 1999, the Sadia group also acquired the Rezende Farm, increasing its share in the market of swine and poultry, and starting to work in the market of genetic development of broiler parents. In 2000, it acquired the assets of Miss Daisy, and started to participate in the frozen dessert market as well.

Sadia's main competitor is the Perdigão group, whose headquarters are located in São Paulo, withholding 24% of the market of industrialized meat products, working both in the poultry and swine markets.

The Perdigão group has 12 units for slaughter and industrialization, and soy crushing, 7 feed producing plants and 8 parents and poultry farms, having in the process of vertical integration 7,000 integrated agricultural producers. Regarding the distribution of the products, it has 14 distribution centers and 48,000 sales spots.

In 2000, Perdigão established a joint-venture with Batavo (a company located in Paraná, which belongs to Parmalat) to jointly act in the market of fresh poultry and pork, sausages, hot dogs, hams, bolognas and salamis. Perdigão (as other companies of the sector), is also extending its production towards the Center West.

Two others companies that merged in 1999 were Chapecó (located in Santa Catarina) and Prenda (located in Rio Grande Do Sul). They started to work jointly in the market of poultry and swine.