![]()

![]()

![]()

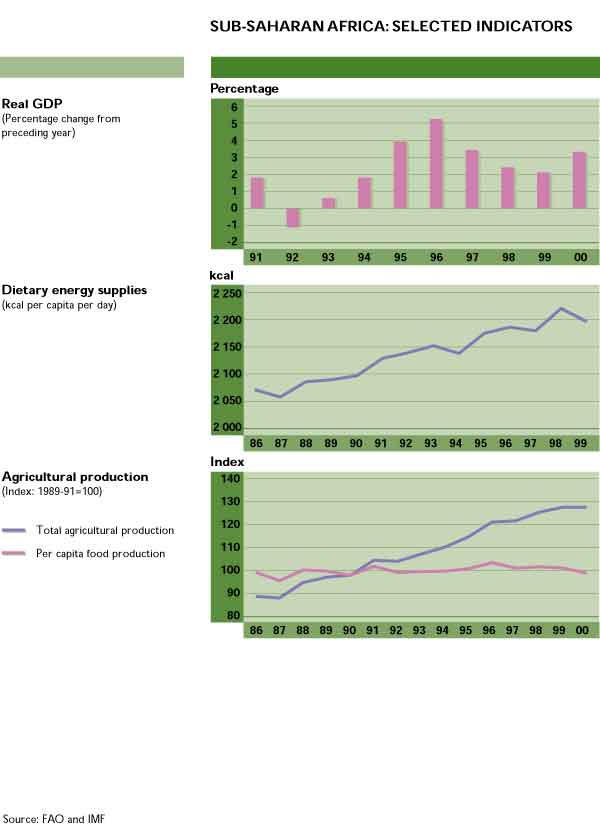

After an average annual GDP growth of only 0.4 percent between 1992 and 1994, economic performance in sub-Saharan Africa began to improve as of 1995.1 This positive trend continued in 1999, although at a reduced rate, with real GDP growing by 2.1 percent. The economic slowdown was largely due to the difficult global economic conditions of the second half of 1997 and most of 1998, rather than to domestic factors. For 2000, a growth rate of 3.3 percent is expected, rising to 4.3 percent in 2001. Strengthening economic activity in South Africa and the oil-exporting countries, in particular Nigeria, is driving the rebound. The rate of inflation increased from 11 to 15 percent between 1998 and 1999 and is expected to be about 16 percent in 2000. Malawi and Zimbabwe, in particular, experienced a large increase in inflation. Economic performance across the region was diverse: Cameroon, Ghana, Mozambique, Uganda and the United Republic of Tanzania are expected to continue to grow strongly as a result of macroeconomic and structural reforms, while in many other countries, economic growth and especially agricultural activity continue to be hampered by past, ongoing or new conflicts.

Table 6

ANNUAL REAL GDP GROWTH RATES IN SUB-SAHARAN AFRICA

Year |

Sub-Saharan Africa |

Nigeria |

South Africa | |

Including Nigeria and South Africa |

Excluding Nigeria and South Africa |

|||

(Percentage) | ||||

1996 |

5.2 |

5.5 |

6.4 |

4.2 |

1997 |

3.4 |

4.0 |

3.1 |

2.5 |

1998 |

2.4 |

3.5 |

1.9 |

0.6 |

1999 |

2.1 |

2.8 |

1.1 |

1.2 |

20001 |

3.3 |

3.5 |

3.5 |

3.0 |

20011 |

4.3 |

4.6 |

3.6 |

4.0 |

1Estimate. | ||||

The overall picture is strongly influenced by the performance of the economies of Nigeria and South Africa, which together account for about half of sub-Saharan Africa's GDP. Following the high growth rates of 1996, these two economies slowed to record, respectively, a 1.1 and 1.2 percent rate of real GDP growth in 1999. Over the 1996-99 period, sub-Saharan Africa grew at a rate of 4 percent, when excluding Nigeria and South Africa, and 3.3 percent when including these two countries. The South African economy is expected to grow by 3 to 4 percent in 2000 and 2001. The steep increase in petroleum prices is helping to lift Nigeria's fortunes, although robust growth in the longer term will depend on the government's ability both to restore macroeconomic stability and to improve governance.

In 1999, for the third consecutive year, overall agricultural production failed to keep up with the population growth rate (currently 2.5 percent per year) and rose by only 2.1 percent after increasing by 2.3 percent in 1998. Crop production is estimated to have increased by 2.2 percent in spite of a 0.4 percent drop in cereal production, while livestock production expanded by a more modest 1.7 percent. The estimated 2.4 percent increase in food production contrasts with a 1.8 percent drop for non-food items. Preliminary estimates for 2000 indicate that agricultural production will rise by only 0.5 percent and that only modest increases in crop, food and livestock production will be realized. Non-food production is estimated to have contracted for the second year in a row. On the other hand, cereal output is predicted to increase by 2.8 percent to 88.1 million tonnes, i.e. about 3.6 percent above the previous five-year average but 2.1 million tonnes short of the record crop achieved in 1996. In per capita terms, however, agricultural production continues to stagnate, with levels for agriculture, cereals and food items in 2000 being virtually identical to those attained in 1990.

In East Africa, drought and population displacements led to a fall in cereal production in 1999 compared with the previous year. Ethiopia, Kenya, Somalia and the United Republic of Tanzania experienced drought and erratic rainfall. Nevertheless, cereal production in Ethiopia is estimated to have recovered somewhat from the dramatic 27 percent decline experienced in 1998. Cereal output in Eritrea, Kenya, the Sudan and the United Republic of Tanzania fell by between 12 and 45 percent in 1999. Drought continued to plague this subregion in 2000, and it is estimated that about 18 million people faced serious food shortages at the beginning of 2001, a situation that will probably persist well into the year. Agricultural output in Kenya and the United Republic of Tanzania is estimated to have contracted by between 0.4 and 2 percent, and cereal production by between 13 and 17 percent, in 2000. In Ethiopia, improved rains are expected to have considerably improved the cereal harvest compared with that of 1999. Nevertheless, Ethiopia and Kenya face serious food shortages and require large cereal imports. In Eritrea, cereal production in 2000 was significantly hampered by the war, and the food supply situation is consequently very tight.

Table 7

NET PRODUCTION GROWTH RATES IN SUB-SAHARAN AFRICA

Year |

Agriculture |

Cereals |

Crops |

Food |

Livestock |

Non-food |

(Percentage) | ||||||

1991-95 |

2.6 |

2.7 |

3.2 |

2.7 |

1.2 |

1.5 |

1996 |

6.8 |

16.6 |

8.6 |

6.5 |

1.7 |

10.4 |

1997 |

0.4 |

-3.3 |

0.3 |

0.3 |

0.9 |

2.4 |

1998 |

2.3 |

-0.6 |

2.4 |

2.2 |

2.5 |

2.5 |

1999 |

2.1 |

-0.4 |

2.2 |

2.4 |

1.7 |

-1.8 |

20001 |

0.5 |

2.8 |

0.3 |

0.5 |

0.9 |

-0.6 |

1 Estimates. | ||||||

In western Africa, the Sahelian countries experienced record cereal production in 1999. The coastal countries along the Gulf of Guinea generally enjoyed good harvests, with the exception of Ghana and Nigeria, where flooding disrupted agricultural activity in some areas. In Ghana, cereal output fell by nearly 6 percent, although this was offset by an 11 to 12 percent increase in the country's roots and tubers output. In Nigeria, cereal output rose by 1.5 to 2 percent and overall agricultural output rose by almost 3 percent. In 2000, aggregate cereal production in the Sahelian countries is expected to be down significantly from the previous year. Below-average cereal production was recorded in Burkina Faso and Chad. However, Cape Verde, the Gambia, Guinea-Bissau and Senegal achieved above-average levels of production. In coastal countries along the Gulf of Guinea, growing conditions have been generally favourable. Côte d'Ivoire's agricultural output is expected to rise by about 3.5 percent in 2000, after increasing by almost 2 percent the previous year. Harvest prospects are also generally favourable in Ghana, Nigeria and Togo. Liberia's production is showing modest increases, with farming activities facilitated by the relative peace prevailing in most regions. Rice production is estimated to increase in Liberia. In Sierra Leone, however, production continues to suffer from insecurity and conflict, and prospects are likewise less favourable for Guinea which has been suffering from rebel activity.

Table 8

EXPORT DEPENDENCY AND TERMS OF TRADE OF SELECTED COUNTRIES IN SUB-SAHARAN AFRICA

Commodity/country |

Exports in 1998 |

Percentage share in total exports1 |

Change in terms of trade2 | ||

Quantity |

Value |

1999 |

2000 (first half) | ||

(Thousand tonnes) |

(Million $) |

(Percentage) | |||

COCOA BEANS |

|||||

Côte d'Ivoire |

837 |

1 284 |

30 |

-11 |

-16 |

Ghana |

271 |

505 |

24 |

-14 |

-22 |

Sao Tome and Principe |

4.5 |

7 |

44 |

-10 |

-28 |

Sub-Saharan Africa |

1 377 |

2 178 |

|||

COFFEE, GREEN |

|||||

Burundi |

22 |

51 |

70 |

-20 |

-33 |

Central African Republic |

6 |

10 |

9 |

||

Côte d'Ivoire |

315 |

495 |

8 |

||

Ethiopia |

115 |

380 |

60 |

-19 |

-32 |

Madagascar |

30 |

40 |

22 |

-6 |

-15 |

Rwanda |

14 |

26 |

45 |

-11 |

-25 |

Uganda |

197 |

314 |

56 |

-17 |

-34 |

United Rep. of Tanzania |

54 |

115 |

11 |

-7 |

-13 |

Sub-Saharan Africa |

926 |

1 902 |

|||

COTTON LINT |

|||||

Benin |

77 |

107 |

38 |

-14 |

-16 |

Burkina Faso |

74 |

107 |

39 |

-16 |

-25 |

Central African Republic |

15 |

23 |

12 |

-7 |

-12 |

Chad |

56 |

77 |

42 |

-15 |

-20 |

Côte d'Ivoire |

68 |

80 |

3 |

||

Mali |

119 |

130 |

46 |

-23 |

-28 |

Sudan |

94 |

106 |

18 |

-5 |

-23 |

Togo |

28 |

31 |

20 |

-9 |

-14 |

Uganda |

7 |

7 |

3 |

||

United Rep. of Tanzania |

38 |

54 |

10 |

||

Sub-Saharan Africa |

794 |

1 054 |

|||

TEA |

|||||

Burundi |

6 |

11 |

8 |

||

Rwanda |

4 |

6 |

12 |

||

United Rep. of Tanzania |

23 |

32 |

2 |

||

Sub-Saharan Africa |

374 |

787 |

|||

1 Exports of the specific commodity as a percentage of total exports of goods and services. | |||||

In central Africa, agricultural performance in 1999 was mixed, with many countries suffering from the adverse effects of civil conflict. Agricultural output fell in Cameroon, where cereal production fell by 14 percent. In the Central African Republic, cereal production increased by 17 percent in 1999 but overall agricultural output declined by about 1 percent. Angola, the Congo and the Democratic Republic of the Congo experienced output losses owing to the negative effects of civil conflict. Overall agricultural production in Cameroon was expected to stagnate in 2000. While the country experienced a sharp fall in non-food production, this is estimated to be offset by a 16 percent rise in cereal output. The food insecurity situation in the Democratic Republic of the Congo remains very serious, particularly in the eastern part of the country. Cereal production is expected to fall by 1 to 2 percent in 2000, and production and marketing activities are still hampered by the civil strife.

In 1999, southern African agricultural output rose marginally in Mozambique, Namibia and Zimbabwe. On the other hand, Botswana, South Africa, Malawi and Zambia experienced growth in output of 5, 5.5, 9 and 10 percent, respectively. While cereal output increased in Botswana, Mozambique, Namibia, Zambia and Zimbabwe, in South Africa it fell by about 2.5 percent after contracting by 24 percent in 1998. Southern African harvests were generally good in 2000, despite severe floods in some parts.

AIDS has created several million orphans in sub-Saharan Africa

An 18-year-old orphan looks after his eight siblings

FAO/17372/K. DUNN

Cereal production in the subregion was 19 percent higher than in 1999. Overall agricultural output is estimated to be up by 5 percent in South Africa, which signifies the second consecutive year of strong expansion. Namibia, Zambia and Zimbabwe are forecast to experience growth in agricultural output at a rate of 5, 10 and 14 percent, respectively. Cereal production in all four countries is estimated to have expanded very strongly, with rates exceeding 25 percent. In Zimbabwe, the overall food supply is expected to remain satisfactory, although the continuous devaluation of the national currency has increased prices for many basic commodities and agricultural inputs. In Mozambique, agricultural production contracted by an estimated 19 percent in 2000, and Madagascar also experienced lower harvests compared with 1999.

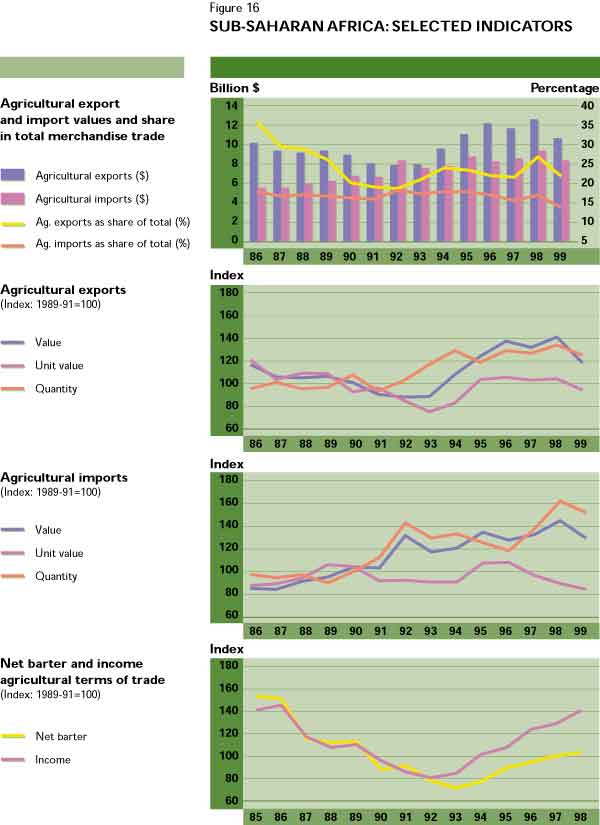

Many African countries rely on a few commodities to generate their foreign exchange earnings. Coffee, for example, accounts for 60 percent of Ethiopia's and 70 percent of Burundi's total exports of goods and services. As a consequence, many economies in sub-Saharan Africa are particularly vulnerable to adverse fluctuations in terms of trade which, for most countries, were severe in 1999 and 2000. For example, Côte d'Ivoire saw its terms of trade fall by 11 and 16 percent in 1999 and 2000, respectively, while Burundi, Ethiopia and Uganda, all heavily reliant on coffee, saw their terms of trade fall by 30 percent or more in 2000.

Between 1995-97 and 2000, ten African countries suffered terms of trade losses of more than 20 percent. A further six saw their terms of trade deteriorate by between 10 and 20 percent, and only oil-exporting countries experienced improvements in their terms of trade. Over half of the countries that were worst hit by falling commodity prices are in sub-Saharan Africa.

The epidemic of human immunodeficiency virus/acquired immunodeficiency syndrome (HIV/AIDS) is the focus of increasing concern in the sub-Saharan Africa region, not only with regard to the serious health and social implications of the disease, but also because of its negative effect on agricultural performance and food security. In 2000, of the total 36.1 million people estimated to have HIV/AIDS worldwide, 25.3 million, or 70 percent, live in sub-Saharan Africa.2 Today, there are 16 countries in the region with more than one-tenth of their adult population infected with HIV.

In 2000, 3.8 million adults and children in sub-Saharan Africa became infected with HIV, slightly fewer than the 4 million infections recorded in 1999. The rate of infection is stabilizing in this region, as the disease has already reached large numbers of people and because some countries are achieving effective prevention. Infections in the southern cone of Africa are still rising, however, and the overall trend will depend on how the epidemic develops in Nigeria. Deaths from AIDS in the region totalled 2.4 million in 2000, compared with 2.2 million in 1999. Tragically, the epidemic has already created 12.1 million orphans in sub-Saharan Africa. Before the emergence of AIDS, about 2 percent of all children in developing countries were orphans; by 1997, the figure was 7 percent in many African countries and, in some, it had reached 11 percent.

Table 9

PREVALENCE OF HIV/AIDS IN 2000

Region |

Number of adults and children living with HIV/AIDS (Thousands) |

Percentage of adults living with HIV/AIDS in 2000 |

North America |

920 |

0.60 |

Caribbean |

390 |

2.30 |

Latin America |

1 400 |

0.50 |

Western Europe |

540 |

0.24 |

Eastern Europe and Central Asia |

700 |

0.35 |

North Africa and the Near East |

400 |

0.20 |

Sub-Saharan Africa |

25 300 |

8.80 |

South and Southeast Asia |

5 800 |

0.56 |

East Asia and the Pacific |

640 |

0.07 |

Australia and New Zealand |

15 |

0.13 |

World |

36 100 |

1.10 |

Source: UNAIDS | ||

The population groups most at risk are those situated along truck routes to rural areas, i.e. people who live in areas such as rural market towns and have greater contact with urban centres. Rural zones that are sources of migrant labour and large infrastructure projects have also been identified as areas of high HIV prevalence. For example, HIV prevalence among pregnant women in Agomanya, the administrative centre of the district that abuts on Ghana's Volta dam, is five to ten times higher than in the rest of the country.3

While, in terms of absolute numbers, prevalence rates may be higher in urban centres, most of the people infected with HIV are rural dwellers. Women are also relatively worse affected. For every ten African men infected, there are between 12 and 13 African women infected, and the average rates among adolescent girls are three to five times higher than those among boys in the same age group.

Table 10

PREVALENCE OF HIV/AIDS IN SUB-SAHARAN AFRICAN COUNTRIES, IN ASCENDING ORDER, 1999

Country |

Number of adults infected (15-49 years) |

Percentage of adult population |

Country |

Number of adults infected (15-49 years) |

Percentage of adult population |

(Thousands) |

(Thousands) |

||||

Sub-Saharan Africa |

23 400 |

5.57 |

|||

�1. Mauritius |

0.5 |

0.08 |

23. Congo |

82 |

6.43 |

�2. Comoros |

0.4 |

0.12 |

24. Burkina Faso |

330 |

6.44 |

�3. Madagascar |

10 |

0.15 |

25. Cameroon |

520 |

7.73 |

4. Equatorial Guinea |

1 |

0.51 |

26. United Rep. of Tanzania |

1 200 |

8.09 |

5. Mauritania |

6.3 |

0.52 |

27. Uganda |

770 |

8.30 |

6. Niger |

61 |

1.35 |

28. Ethiopia |

2 900 |

10.63 |

7. Guinea |

52 |

1.54 |

29. Côte d'Ivoire |

730 |

10.76 |

8. Senegal |

76 |

1.77 |

30. Rwanda |

370 |

11.21 |

9. Gambia |

12 |

1.95 |

31. Burundi |

340 |

11.32 |

10. Mali |

97 |

2.03 |

32. Djibouti |

35 |

11.75 |

11. Benin |

67 |

2.45 |

33. Mozambique |

1 100 |

13.22 |

12. Guinea-Bissau |

13 |

2.50 |

34. Central African Republic |

230 |

13.84 |

13. Chad |

88 |

2.69 |

35. Kenya |

2 000 |

13.95 |

14. Angola |

150 |

2.78 |

36. Malawi |

760 |

15.96 |

15. Liberia |

37 |

2.80 |

37. Namibia |

150 |

19.54 |

16. Eritrea |

49 |

2.87 |

38. South Africa |

4 100 |

19.94 |

17. Sierra Leone |

65 |

2.99 |

39. Zambia |

830 |

19.95 |

18. Ghana |

330 |

3.60 |

40. Lesotho |

240 |

23.57 |

19. Gabon |

22 |

4.16 |

41. Zimbabwe |

1 400 |

25.06 |

20. Nigeria |

2 600 |

5.06 |

42. Swaziland |

120 |

25.25 |

21. Dem. Rep. of the Congo |

1 100 |

5.07 |

43. Botswana |

280 |

35.80 |

22. Togo |

120 |

5.98 |

|||

Source: UNAIDS. | |||||

Some countries, such as Senegal and Uganda, have been successful in containing the prevalence rate by implementing strong prevention programmes as well as by generally recognizing that the problem exists and ensuring strong political leadership. Senegal has managed to contain the HIV/AIDS prevalence rate at low levels, while Uganda has brought its estimated prevalence rate down to about 8 percent from a peak of nearly 14 percent in the early 1990s.

The HIV/AIDS epidemic will undermine development through its negative impact on life expectancy. An average of 17 years of life expectancy has been lost in countries where the adult HIV/AIDS prevalence rate exceeds 10 percent.4 What is unique to HIV/AIDS is that it mainly affects the most productive age group - people aged between 15 and 49. The median time between infection and death is between eight and ten years, and it is with the gradual onset of AIDS in the last two of those years that declining labour productivity and health care costs are felt. Companies lose their workers and hours are lost to illness, death, overwork, stress, funeral attendance and home care.

The epidemic also affects economic growth indirectly, as private and public spending on education and infrastructure decrease owing to the increased demands from the health sector. In urban areas of Côte d'Ivoire, household expenditure on schooling has been found to fall by 50 percent when someone in the family dies from AIDS. Food consumption drops by 41 percent per capita, while spending on health care increases more than fourfold.5 AIDS not only lowers the demand for schooling but also affects the supply side; a shortage of teachers is therefore a threat in many African countries. In the Central African Republic, for example, there were an equal number of teachers who died as there were retirees over the 1996-98 period, and 85 percent of these deceased were HIV-positive.6

Table 11

THE COST OF AIDS IN SELECTED SUB-SAHARAN AFRICAN COUNTRIES

Country |

Direct cost of AIDS per case |

GDP per capita |

($) | ||

Kenya (1992) |

938 |

333 |

Malawi (1989) |

210 |

203 |

Rwanda (1989-90) |

358 |

269 |

United Rep. of Tanzania (1990) |

290 |

204 |

Zimbabwe (1991) |

614 |

648 |

Source: M. Ainsworth and M. Over. 1994. AIDS and African development. The World Bank Research Observer, 9(2): 203-240. | ||

HIV/AIDS is now the leading cause of death and one of the main factors in calculating disability-adjusted life years (DALYs)7 in sub-Saharan Africa. The epidemic is also linked with other infectious diseases, such as tuberculosis. Hospital records indicate that up to 40 percent of HIV-infected patients have tuberculosis.8 Treatment costs of HIV/AIDS patients are very high and the epidemic will lead to increased government expenditure in the health sector, thereby diverting funds from productive investments. The cost of treatment of AIDS and related infections is expected to exceed 30 percent of the budget for the Ministry of Health in Ethiopia by 2014, and 50 and 60 percent in Kenya and Zimbabwe, respectively, by 2005.9

Despite the harrowing statistics, the macroeconomic impact of the HIV/AIDS epidemic has been difficult to assess. Estimates are sensitive to assumptions regarding how AIDS affects savings and investment rates and whether or not better skilled and more educated people are more at risk. Moreover, in many African countries that have a labour surplus in their formal sectors, deaths from AIDS do not necessarily result in a proportional loss of productivity. Indeed, many authors point out that GDP per capita may be an inappropriate yardstick to use because it does not accurately capture the serious setback in development suffered by some countries. United Nations Development Programme (UNDP) estimates for South Africa suggest that the Human Development Index might be 15 percent lower in 2010 as a result of the HIV/AIDS epidemic.

HIV/AIDS affects the most productive age group. Furthermore, HIV-infected urban dwellers often return to their village, and rural households provide most of the care for AIDS patients. FAO has estimated that in the 25 most affected African countries, 7 million agricultural workers have died from AIDS since 1985; 16 million more could die within the next 20 years. FAO expects the HIV/AIDS epidemic to exacerbate food insecurity. According to recent FAO and UNAIDS studies, agricultural output of small farmers in some parts of Zimbabwe may have fallen by as much as 50 percent over the past five years, mainly as a result of AIDS.

Table 12

ESTIMATED LOSS IN AGRICULTURAL LABOUR FORCE THROUGH AIDS IN WORST-AFFECTED SUB-SAHARAN AFRICAN COUNTRIES

Country |

Percentage loss, 1985-2000 |

Namibia |

-26 |

Botswana |

-23 |

Zimbabwe |

-23 |

Mozambique |

-20 |

South Africa |

-20 |

Kenya |

-17 |

Malawi |

-14 |

Uganda |

-14 |

United Rep. of Tanzania |

-13 |

Source: FAO. | |

Labour shortages are particularly serious in agriculture, since production is seasonal and timing is generally crucial. Areas with less developed labour markets and a higher reliance on household labour are also likely to be relatively worse affected. The shortfall in household labour means that some land remains fallow and the household's output declines. An FAO study of several farming areas has shown decreasing yields per area owing to: a decline in soil fertility; an increase in pests and diseases; changes and delays in cropping practices; and less use of external production inputs. The shortage of labour may lead to less time being dedicated to weeding, mulching, pruning and the clearing of land. Moreover, farmers may switch to less labour-intensive crops. The decline in soil fertility is partly due to farmers not implementing soil conservation measures that may be labour-intensive and long-term in nature.10

The epidemic also has grave consequences for agricultural estates. Evidence from one sugar estate in Kenya suggests that the epidemic adds substantially to costs. Profitability has been undermined by increased absenteeism owing to sickness, substantially reduced productivity and higher overtime costs as other workers replace their sick colleagues. Over an eight-year period in the 1990s, spending on funerals and health costs rose fivefold and tenfold, respectively. The company has estimated that about three-quarters of all illness among employees was related to HIV infection.11

The impact on the livestock sector is also severe. Evidence from Namibia and Uganda indicates that livestock is often sold to support the sick and to pay for funeral expenses.12 Selling livestock eats into a household's savings, making them more vulnerable to new shocks. The drop in livestock numbers means a reduced availability of organic material and hence increased pressure on soil fertility.

HIV/AIDS creates a tremendous burden for households, and the medical and funeral expenses force many of the poorer households into debt. A World Bank study on Kagera district in the United Republic of Tanzania revealed that about 60 percent of the cost associated with an AIDS victim is used to cover funeral costs. The total cost of about $60 is probably close to the annual per capita income in Kagera.13 Recent evidence from the United Republic of Tanzania suggests that food expenditure by poor households can drop by nearly one-third during the six months after the death of a young adult.14

Finally, the epidemic also affects agricultural extension work. There may be a shortage of staff in this area, too, and extension programmes may need to be adapted to take into account the effect of the epidemic. A Ugandan extension officer noted that between 20 and 50 percent of all person-hours among extension staff was lost as a result of the disease.15

Africa accounts for about one-tenth of the world's population but for nine out of ten new cases of HIV infection. Eighty-three percent of all AIDS deaths are in Africa. The impact of AIDS on farming communities differs from village to village and from country to country. Nevertheless, it is clear that the epidemic is undermining the progress made in agricultural and rural development over the last 40 years. This presents governments, non-governmental organizations (NGOs) and the international community with an enormous challenge. The disease is no longer simply a health problem, it has become a major development issue.

Following the civil war and the subsequent change of government in 1991, political stability, prudent macroeconomic policies and reforms aimed at liberalizing Ethiopia's economy contributed to high rates of economic growth. The Government of Ethiopia is pursuing a multifaceted programme of economic development centred on the transformation of the agriculture sector. Although considerable progress has been achieved in many areas since the early 1990s, Ethiopia has very high levels of poverty and food insecurity and the country continues to rank among the poorest in the world.

Ethiopia covers 1 098 000 km2 and has 62.8 million inhabitants,16 85 percent of whom live in rural areas. The highlands, which extend over 40 percent of the land mass, are home to 80 percent of the human population and 75 percent of the country's livestock. A major feature of the climate is the unreliable nature of the rainfall. Ethiopia has suffered two large-scale, drought-induced famines in recent times (1973/74 and 1983/84), which claimed hundreds of thousands of lives. The situation is not uniform throughout Ethiopia: three-quarters of the drought-affected population are to be found in just three regions: Tigray, Wollo and Hararghe.17 Although Ethiopia imported food for the first time in 1959, very large inflows of food aid have been a feature since the late-1980s.

Following the defeat of the military regime in 1991,18 the Transitional Government of Ethiopia was formed and a programme of economic reform and regional devolution initiated. The nine regional states were formed largely on the basis of language. Federal and regional elections were held in 1995 and the Federal Democratic Republic of Ethiopia was created in that year. Under the new constitution, regional authorities have wide-ranging economic powers. Nevertheless, the impact of the regionalization policy is limited, as the central government raises 85 percent of domestic revenue and the regions, which are responsible for more than 40 percent of expenditure, rely on central government subsidies.19

FAO estimates that 49 percent of Ethiopia's population is undernourished.20 Daily per capita food availability is about 1 410 kilocalories (kcal) for the undernourished, which implies a daily deficit of 340 kcal per capita.21 A 1993 National Nutrition Survey22 found that 64 percent of children under the age of five suffer from chronic malnutrition (stunting), among the highest levels in the world, and that about 47 percent are underweight.23 Also of serious concern are the current levels of iodine and vitamin A deficiency among children under the age of six.

Current levels of health are very low. Infant and under five mortality stands at 118 and 176 per 1 000, respectively. Overall access to health care is severely limited and biased towards hospital-based curative services in urban areas. The fact that only 24 percent of the population has access to safe water exacerbates the problem.

The adult literacy rate in Ethiopia is only 35 percent. Gross school enrolment ratios are 29 percent at primary level (less than half the sub-Saharan average of 72 percent), 19 percent at junior secondary level, 9 percent at senior secondary level and less than 1 percent at tertiary level. Significant rural-urban differences exist, with Addis Ababa and other urban centres enjoying almost universal primary education while rural areas have an enrolment rate of 18 percent.

Spending on health and education has increased from 2.8 and 7 percent of the government budget in 1989 to 6.5 and 14 percent in 1998, respectively. Reforms in the fields of health and education are aimed at raising the level of service and coverage and at addressing rural-urban and regional disparities.

Ethiopia's GDP per capita is approximately $106. After relatively poor macroeconomic performances during the 1970s and 1980s, when average real GDP growth rates were 2.6 and 2.3 percent, respectively, economic growth averaged 5.9 percent during the period 1993-1999 (Table 13). The recovery largely resulted from the economic reform programme launched in 1992 (outlined below) as well as from favourable weather and harvests. However, negative growth was recorded in 1998, largely owing to drought caused by the El Niño phenomenon. In 1999, GDP growth rebounded to 6.3 percent, although the forecast for 2000 was a more modest 2 percent, largely reflecting a weaker expected agricultural output. Rapid growth was accompanied by a low average level of inflation of 3.9 percent over the 1993-1999 period.

Table 13

REAL GDP GROWTH AND CONSUMER PRICE INFLATION IN ETHIOPIA

Year |

Real GDP growth |

Annual inflation rate |

(Percentage) | ||

1993 |

12.0 |

10.0 |

1994 |

1.6 |

1.2 |

1995 |

6.2 |

13.4 |

1996 |

10.6 |

0.9 |

1997 |

5.2 |

-6.4 |

1998 |

-0.5 |

3.7 |

1999 |

6.3 |

4.2 |

20001 |

2.0 |

5.0 |

1EIU estimate. | ||

Ethiopia's main economic sector is agriculture, which provides employment for about 90 percent of the population and accounts for about 46 percent of GDP. Growth in services, which contributes 30 percent of GDP, has occurred mainly in transport and tourism. Manufacturing contributes 12 percent of GDP, with industry accounting for 5 percent. Finally, public administration and defence account for about 13 percent of GDP.26 External debt is estimated to be about $9.3 billion, or 142 percent of GDP.27

From 1992 onwards, there has been a reorientation of economic policy. As part of the reform programme, the Ethiopian currency - the birr - was devalued by 60 percent in October 1992 and fortnightly foreign exchange auctions started in 1993. A medium-term adjustment programme, supported by the International Monetary Fund (IMF), was introduced in 1996 for the period 1996/97-1998/99. Further exchange market liberalization followed in August 1998. Trade has been liberalized by reducing import tariffs and by removing restrictions on external account transactions. The maximum tariff is now 40 percent and the average is still quite high at 19.5.28 One important achievement has been the markedly improved revenue collection, with tax receipts up from 2.2 billion to 5.3 billion Ethiopian birr between 1992/93 and 1997/98.29

The first privatizations were conducted in 1995. As is the case for the reform process in general, the speed of the privatization of state assets has been very gradual. The government has sought the assistance of the World Bank to accelerate the programme for privatizing the remaining 115 large enterprises and state farms by the end of 2000/01.

The investment code has been liberalized and, between 1993 and 1998, 21 foreign direct investment (FDI) projects were approved for a value of 8.3 billion birr.30 However, the implementation process is slow; foreign investment remains low and the government is now actively encouraging "foreign" investment by Ethiopians living abroad.

The government has now moved towards implementing sectoral investment programmes (SIPs) in the key sectors of agriculture and food security, health, education and transport, which are meant to foster the country's medium- to long-term development. Increased government expenditure (Table 14) has been made possible by the reduction in defence expenditure since the change in government in 1991. Defence spending fell from 24 percent of government expenditure in 1989 to 7 percent in 1995.31 Although the recent armed conflict with Eritrea (1998-2000) resulted in increased defence expenditures and a larger fiscal deficit, a drastic cut in expenditure for the SIPs is not expected. With the end of the war, renewed donor support is very likely. IMF's projection of external financing requirements for the period 1998/99-2000/01 is $8.6 billion (or 131 percent of the country's GDP in 1998), part of which has already been pledged.32

Table 14

GOVERNMENT EXPENDITURE ON DEFENCE, EDUCATION, HEALTH AND CAPITAL IN ETHIOPIA

Year |

Expenditure by sector |

Total expenditure for all sectors | |||

Defence |

Education1 |

Health1 |

Capital |

||

(Billion birr) | |||||

1994/95 |

0.74 |

1.13 |

0.43 |

3.16 |

8.41 |

1995/96 |

0.77 |

1.38 |

0.48 |

3.56 |

9.21 |

1996/97 |

0.84 |

1.46 |

0.60 |

4.30 |

10.08 |

1997/98 |

2.09 |

1.60 |

0.74 |

4.27 |

11.41 |

1 Includes current and capital expenditure. | |||||

The liberalization and restructuring of the economy, together with the implementation of the SIPs, is a challenge for the public sector. Regional institutions, which are responsible for a wide range of development programmes and projects, lack technical capacity and need to be strengthened. Realizing the public administration's limitations, the government has nearly completed a broad civil service reform, encompassing judicial, legal and financial management reforms.

Table 15

NET OFFICIAL DEVELOPMENT ASSISTANCE TO ETHIOPIA

Year |

Total net ODA | |

Million $ |

Percentage of GDP | |

1994 |

1 071 |

19.3 |

1995 |

883 |

15.3 |

1996 |

817 |

13.6 |

1997 |

572 |

9.0 |

1998 |

648 |

9.9 |

1999 |

633 |

9.7 |

Source: OECD and IMF. | ||

As noted earlier, agriculture is Ethiopia's main economic activity. More than 95 percent of the country's agricultural output is generated by subsistence farmers, using traditional methods. Eighty-four percent of crop area in 1998/99 was planted to cereal crops, such as teff,33 wheat, barley, maize, sorghum and millet.34 Ethiopia also has the largest livestock herd in sub-Saharan Africa, with 17 percent of the continent's cattle and 14 percent of its ruminants (cattle, sheep, goats) supported by 3 percent of its permanent pasture.35 Cattle stocks expanded at an average rate of 1.1 percent over the period 1970-95,36 as productivity was limited by a high incidence of disease and poor nutrition.

The agricultural export sector is highly concentrated on a few commodities. Two-thirds of export revenues are generated by coffee alone. Coffee, hides and skins, qat,37 pulses and oilseeds generate more than 80 percent of the country's export earnings (Table 16). A fall in the value of hide and skin exports in 1998 is attributed to the Asian and Russian financial crises.

Table 16

ETHIOPIA'S MAIN EXPORTS AND IMPORTS

Year |

Exports |

Imports |

Trade balance | |||||

Coffee1 |

Hides and skins |

Pulses and oilseeds |

Qat |

Total |

Cereals |

Total |

||

(Million $) | ||||||||

1993 |

125.8 (57) |

31.5 |

1.3 |

15.4 |

222.4 |

-82 |

-1 051.8 |

-829.4 |

1994 |

158.3 (57) |

35.1 |

12.4 |

18.7 |

279.6 |

-245 |

-914.6 |

-635 |

1995 |

287.8 (64) |

59.8 |

24.5 |

27.6 |

453.6 |

-164 |

-1 063.0 |

-609.4 |

1996 |

272.9 (67) |

50.8 |

18.8 |

27.6 |

410.2 |

-110 |

-1 412.9 |

-1 002.7 |

1997 |

355.0 (59) |

57.3 |

23.3 |

33.5 |

598.7 |

-57 |

-1 403.1 |

-804.4 |

1998 |

420.0 (70) |

50.5 |

60.7 |

39.6 |

602.1 |

-113 |

-1 518.8 |

-916.7 |

1 Numbers in parentheses refer to the percentage of total exports. | ||||||||

Ethiopian agriculture is dependent on an unreliable rainfall. Irrigated land accounts for less than 1 percent of total cropland38 and agricultural production may fall by up to 20 percent in years of drought. Untimely and/or excessive rainfall in many areas can also affect grain production negatively.

Despite the importance of agriculture in its economy, Ethiopia has been a food-deficit country for several decades, with cereal food aid averaging 14 percent of total cereal production in the period 1984-99.39 With a growth rate of 3 percent per year, the country's population will double in less than 25 years. Unless action is taken urgently, therefore, the gap between food supply and demand will widen further and food insecurity will become even more pervasive.

Increasing human and livestock population pressures have contributed to extensive soil degradation in Ethiopia. According to an FAO study,40 out of 54 million ha (including Eritrea) in the highlands: 14 million ha had experienced serious degradation, 13 million ha had experienced moderate degradation and 2 million ha had too shallow a soil cover to cultivate crops. The degradation has continued, and between 1.5 billion and 2 billion tonnes of topsoil41 are lost every year. At the root of Ethiopia's large food deficit is its low agricultural productivity. Cereal yields stagnated at around 1.2 tonnes per hectare between 1980 and 1997.42 The decreasing size of farms has led to shorter fallow periods and even continuous cropping, and limited efforts to recycle crop residues or other organic matter into the soil have resulted in farmers having to invest in chemical fertilizer to produce enough for their subsistence requirements. With little room for further significant increases in the area under cultivation, the solution to the country's food supply problem hinges on raising yields, which in turn are determined by sustainable growth in the use of external inputs, particularly fertilizer and improved seeds.

The use of fertilizer in Ethiopia has been suboptimal for a number of reasons,43 including a lack of complementary external inputs. For example, fertilizer efficiency is negatively affected by competition from weeds, insect attack and disease infestation but, in 1997/98, only 12 percent of the area planted to cereal was treated with pesticides (mainly insecticides) and herbicides.44 Improved seeds have been lacking: while 39 percent of the area under cereals was fertilized in 1996/97, only 2.4 percent of this area was planted with improved seeds.45 The quality of improved seeds is also low in many instances. For example, most of the improved wheat varieties used were found to be susceptible to rust during the 1998/99 cropping season.46 The seed industry, dominated by the parastatal Ethiopian Seed Enterprise, is unable to multiply and distribute sufficient quantities of hybrid maize, which is very popular in areas of high rainfall. Greater attention, therefore, needs to be paid to location-specific agricultural research and to the seed industry.

Since 1992, the government has taken several measures aimed at improving smallholders' productivity, removing government monopolies and restrictions on private trading and encouraging private sector participation in the agricultural input market.

The Participatory Demonstration and Training Extension System (PADETES) was launched in 1994/95, mainly to increase farmers' use of fertilizers. Supported by World Bank funding, PADETES is based on an extension package developed by Sasakawa-Global 2000 and the Ministry of Agriculture's Extension Department. From 35 000 farmer-managed demonstration plots in 1995, the programme grew to include nearly 4 million plots (measuring 0.25 to 0.5 ha) in 1999.47 Substantial resources for expanding credit were also made available.48

Agricultural input as well as output markets have been liberalized, and in 1998 price controls and input subsidies were abolished in an effort to remove market distortions.

With the new policy in force, fertilizer consumption increased from 153 000 tonnes in 1992 to 286 000 tonnes by August 1999.49 Farmers participating in the PADETES programme, and who adopted the complete package of improved seeds and fertilizer together with the recommended agronomic practices, reportedly achieved high yields - particularly in the case of maize.50

Nevertheless, the transition from public to private sector participation has been slow and cereal yields have remained low. With the exception of Oromia region,51 where relatively competitive market conditions prevail, regional fertilizer markets are dominated by public companies or firms affiliated with regional governments. At the national level, the impact of PADETES is more positive, but still limited. It is clear that much remains to be done, although recent trends give cause for positive expectations. A very positive trend in agricultural output was recorded between 1994 and 1997, mainly as a result of favourable weather from 1995 to 1997 and the increase in area under cultivation (Table 17).

Table 17

CEREAL SUPPLY IN ETHIOPIA

Year |

Area under cereals |

Average yield for cereals |

Total cereal production |

Cereal imports |

Cereal food aid |

(Thousand ha) |

(Tonnes/ha) |

(Thousand tonnes) | |||

1993 |

4 034 |

1.31 |

5 295 |

450 |

652 |

1994 |

5 387 |

0.97 |

5 245 |

1 023 |

787 |

1995 |

6 527 |

1.03 |

6 740 |

647 |

525 |

1996 |

7 731 |

1.21 |

9 379 |

399 |

298 |

1997 |

7 498 |

1.26 |

9 473 |

256 |

653 |

1998 |

6 313 |

1.14 |

7 197 |

585 |

626 |

1999 |

7 426 |

1.13 |

8 407 |

656 |

1 205 |

2000 |

6 817 |

1.15 |

7 845 |

n.a. |

n.a. |

n.a. = data not available. | |||||

Among the major constraints to low-cost input supplies and distribution in Ethiopia are perceived policy uncertainties, inadequate institutional capacity in implementing reform, a lack of effective credit and saving groups and poor market information. Two major barriers are the country's weak extension service and inadequate physical infrastructure:

Agricultural extension in Ethiopia is entirely in the hands of the public sector and farmers' participation is limited. Under the new extension approach, 15 000 development agents are expected to transfer technology packages, designed by Ministry of Agriculture experts. An agent is basically a supervisor, whose main task is to ensure that farmers selected for demonstration are applying the package according to blanket recommendations issued by the authorities. With only a few months' training, agents often lack the capacity to modify recommendations to local conditions. Since the extension system does not encompass adaptive research, farmers are often required to adopt technologies of unknown profitability and adaptability.

Agricultural marketing in Ethiopia is also hampered by a number of obstacles, one of which is infrastructure. The average road density is only 21 km per 1 000 km2 or 0.44 km per

1 000 people, one of the lowest rates in Africa.52 Grain marketing is largely handled by small-scale traders with limited storage capacity. Low prices after harvest and high seasonal price fluctuations have discouraged investment in vital inputs such as fertilizers and improved seeds. A Road Sector Development Programme was recently introduced to increase the accessibility of all-weather roads. The aim is to reduce the proportion of farms that are more than half a day's walk from the nearest all-weather road from 75 to 25 percent within ten years. Substantial government resources, more than 20 percent of the capital budget, are allocated for road construction and maintenance.53

It is the Ethiopian Government's priority to fight widespread poverty and food insecurity, and it is a tribute to the administration's commitment that there have been no repeats of the 1983/84 famine, even though droughts occurred in 1991/92 and 1993/94. Another major crisis emerged in 1999 and 2000, as the less abundant Belg�54 (February-April) rains failed in both years and the rainfall pattern for the Meher (May/September) season continued to be abnormal. An estimated 10.2 million people were in need of assistance in mid-2000, requiring an estimated 1.3 million tonnes of emergency food aid.55 However, early warning efforts, supplies from the Emergency Food Security Reserve (EFSR)56 and substantial assistance from the World Food Programme (WFP) as well as other agencies and donors have made it possible to prevent widespread famine.

The severe crisis highlights how much Ethiopia is still at the mercy of the weather. In the light of the large number of people affected, food aid may not have been targeted broadly enough. Many households that do not qualify for assistance, but that may nevertheless be drawing on their assets to make up their deficits each year, are very vulnerable in times of drought. WFP's Vulnerability Analysis Mapping, which provides information pertaining to food security, is seen as a valuable effort towards the improved targeting of aid.

The overarching, long-term strategy is that of agricultural development-led industrialization (ADLI), which views agriculture as the main engine of growth. As mentioned earlier, a more comprehensive SIP is currently being implemented for the agriculture and food security sector. The programme focuses on:

The programme is accompanied by a population policy aimed at reducing fertility from a rate of 7.7 to 4 children per woman by 2025.

Land tenure is a politically-sensitive issue. Currently, all land is public and will remain so for the foreseeable future. The transfer of land through long-term lease or sales has been forbidden and redistribution has been carried out regularly. Smallholder farmers perceive their tenancy rights to be insecure, and this has a negative impact on investment in land improvements. The land policy has reinforced fragmentation and reduced the average farm size to less than 1 ha in many areas. Land policy reform would encourage the formation of viable farms and enhance agricultural transformation in Ethiopia.

The government is also focusing on soil and water conservation and reforestation programmes. It has established an Environmental Protection Agency and initiated a National Conservation Action Plan that includes measures for selective reforestation. Much more needs to be done, however, to guarantee the sustainability of rural communities in many parts of the country.

The high instability of coffee prices has made the diversification of exports a priority, and the government has set up an Export Promotion Agency for this purpose. Nevertheless conditions are far from ideal. The uncompetitive nature of the domestic service sector adds to the cost of exporting, and inadequate infrastructure is a further constraint.

An important area that has been neglected in the past is the livestock sector. Given the size of this sector, not to mention its substantial forward and backward linkages at all levels of the economy, the scope for developing livestock resources is considerable, as are the multiplier effects that can be expected. A Leather Technology Institute and a Livestock Marketing Authority are now being established to promote the export of livestock and livestock products.

Ethiopia is one of the poorest countries of the world. The end of many years of civil war has brought to office a government that is at once focused on agriculture and dedicated to fighting poverty and food insecurity. Achievements to date have been impressive, particularly with regard to macroeconomic performance and famine prevention. However, continued building and strengthening of the country's institutions is needed to ensure the efficient, transparent and accountable public administration required for the successful implementation of reform and investment programmes. With more than 2 million chronically food-insecure people, the challenge for Ethiopia is still daunting.

![]()

![]()

![]()