![]()

![]()

![]()

In 1997 and 1998, the Asian financial crisis reduced wealth and incomes, increased unemployment and inflation and heightened food insecurity in the worst affected countries of the region. By the first quarter of 1999, most of the economies of the affected countries were recovering, and this recovery process was consolidated during 2000. According to IMF,57 real GDP growth in developing Asian countries had increased to 5.9 percent in 1999, up from 4.1 percent in 1998. For both 2000 and 2001, IMF projected GDP growth rates of slightly above 6.5 percent.

China's extraordinary economic growth tapered off in the late 1990s to settle at about 7 percent in 1999. However, economic growth is forecast to rise to 7.5 percent in 2000, owing both to stronger domestic demand and increased exports following the recovery of Asian economies. If growth is to continue at a stable rate, however, an important challenge is to achieve structural reforms in the state-owned enterprise and financial sectors and to develop a legal and regulatory framework necessary for a market economy.

Of the countries that were most severely affected by the region's financial crisis, the Republic of Korea has achieved the sharpest recovery. After a 7 percent contraction in 1998, its economic growth rate was 10 to 11 percent in 1999, with nearly 9 percent projected for 2000 before a fall to 6.5 percent in 2001.

Table 18

ANNUAL REAL GDP GROWTH RATES IN SELECTED COUNTRIES OF DEVELOPING ASIA

Country/region |

1996 |

1997 |

1998 |

1999 |

20001 |

20011 |

(Percentage) | ||||||

Bangladesh |

5.0 |

5.3 |

5.0 |

5.2 |

5.0 |

4.5 |

China2 |

9.6 |

8.8 |

7.8 |

7.1 |

7.5 |

7.3 |

India |

7.1 |

4.7 |

6.3 |

6.4 |

6.7 |

6.5 |

Indonesia |

8.0 |

4.5 |

-13.0 |

0.3 |

4.0 |

5.0 |

Malaysia |

10.0 |

7.3 |

-7.4 |

5.6 |

6.0 |

6.0 |

Pakistan |

4.9 |

1.0 |

2.6 |

2.7 |

5.6 |

5.3 |

Philippines |

5.8 |

5.2 |

-0.6 |

3.3 |

4.0 |

4.5 |

Thailand |

5.9 |

-1.7 |

-10.2 |

4.2 |

5.0 |

5.0 |

Republic of Korea |

6.8 |

5.0 |

-6.7 |

10.7 |

8.8 |

6.5 |

Viet Nam |

9.3 |

8.2 |

3.5 |

4.2 |

4.5 |

5.4 |

Asia3 |

8.3 |

6.5 |

4.1 |

5.9 |

6.7 |

6.6 |

1 Projections. | ||||||

In Southeast Asia, recovery from the region's financial crisis has been more rapid than generally expected, except in Indonesia. After a 13 percent decline in GDP and food price riots in 1998, the Indonesian economy stagnated in 1999, recording GDP growth of less than 0.5 percent. Economic recovery only commenced in 2000, for which GDP growth was projected to be 4 percent, accelerating to 5 percent in 2001. In Malaysia, after a 7 percent contraction in GDP in 1998, recovery commenced in 1999, with an expansion in GDP of an estimated 5.7 percent and a projected rate of 6 percent for 2000. A similar rate is projected for 2001. In the Philippines, the economic downturn in 1998 was less pronounced than in the most affected countries, as GDP contracted by less than 1 percent. On the other hand, the recovery has also been relatively slower, with GDP growing by 3.3 percent in 1999 and by a projected 4 percent in 2000.

After Indonesia, Thailand was the country to have suffered the sharpest economic setback from the financial crisis, with its GDP dropping by 10 percent in 1998. Recovery began in 1999, when the economy grew by about 4 percent, and this rate is projected to rise to 5 percent in 2000. In Viet Nam, the regional financial crisis only induced a slowdown in the rapid GDP growth experienced in the preceding years, and a limited acceleration in growth occurred in 1999 and 2000.

In South Asia, real GDP in India has been growing by between 6 and 7 percent each year since 1997. Current IMF projections point to GDP growth rates of about 6.5 percent in both 2000 and 2001 (6.7 percent in 2000, falling to 6.5 percent in 2001). However, the country's large fiscal deficit and resultant government borrowing requirements could present risks for the economy unless corrective

action is taken.

In Bangladesh, where agricultural output remains a driving factor behind overall economic performance, GDP growth has remained close to 5 percent since 1995. In Pakistan, macroeconomic imbalances stifled economic growth in 1998 and 1999 but recovery appeared to be under way in 2000, with a projected GDP growth rate of 5 to 6 percent.

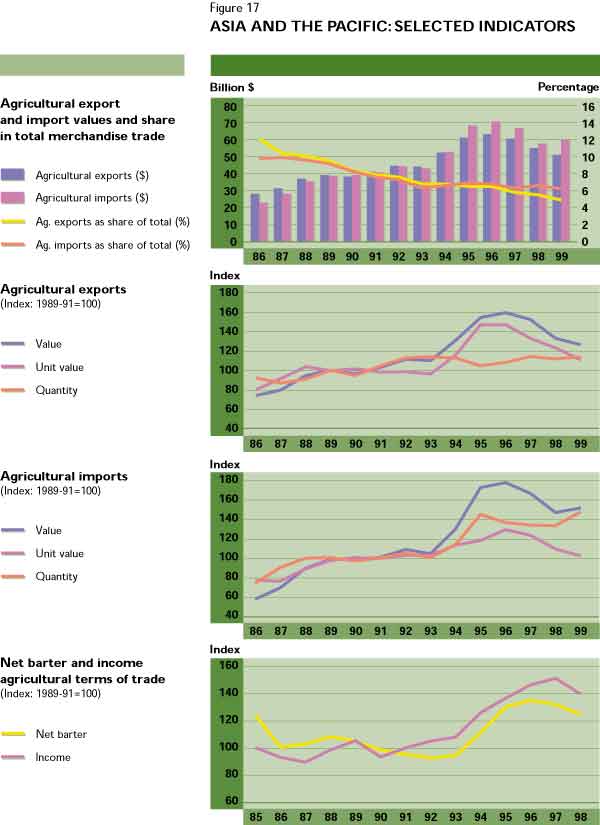

The rate of overall agricultural production growth in the Asia and Pacific region has declined in the past few years. The average annual rate of production growth for the period 1996-00 amounted to 3.2 percent compared with the average rate of 4.6 percent attained during the preceding five-year period. After having grown at a rate of more than 4 percent in four out of five years in the period 1991-1995, rates of expansion in output remained at 4.4 and 4.3 percent in 1996 and 1997, respectively, but dropped to 2.1 percent in 1998 and 3.4 percent in 1999. Provisional estimates of agricultural production in 2000 suggest an expansion in production of just 1 to 2 percent.

Recent poor agricultural performances and weather-related production shortfalls in various countries of the region have contributed to the lower agricultural output growth recorded over the last years. However, the slowdown in China's production growth is the single most important factor behind the trend. After maintaining high rates of growth throughout most of the 1990s, with an average annual rate of production increase of 6.3 percent for 1991-97, Chinese agricultural production growth has decelerated markedly to an estimated 4 percent in 1998 and 2.9 percent in 1999. Provisional estimates for 2000 point to an increase of about the same magnitude, i.e. about 3 percent. In particular, cereal production appears to have declined sharply in 2000, partly because of natural disasters but also because of a major contraction in harvested area in response to reductions in the prices and volumes of state purchases of lower-quality grains. This measure is aimed at encouraging grain farmers to adopt more market-oriented production practices and sell to satisfy local demand rather than depending on government procurement.

Table 19

NET PRODUCTION GROWTH RATES IN DEVELOPING ASIA AND THE PACIFIC

Year |

Agriculture |

Cereals |

Crops |

Food |

Livestock |

Non-food |

(Percentage) | ||||||

1991-95 |

4.6 |

1.2 |

3.4 |

4.8 |

8.0 |

1.9 |

1996 |

4.4 |

5.9 |

5.2 |

4.5 |

3.7 |

2.5 |

1997 |

4.3 |

0.6 |

1.8 |

4.2 |

7.3 |

4.3 |

1998 |

2.1 |

1.5 |

1.2 |

2.8 |

5.3 |

-8.1 |

1999 |

3.4 |

2.5 |

2.8 |

3.6 |

3.7 |

-0.9 |

20001 |

1.6 |

-3.2 |

0.5 |

1.8 |

2.0 |

-1.3 |

1 Estimates. | ||||||

In India, agricultural output has been increasing at fairly stable rates throughout the 1990s, with an average annual rate of about 2.5 percent. After stagnating in 1998 when output was negatively affected by damaging floods in the north of the country, agricultural production recorded a 3.7 percent growth rate in 1999, with a bumper production in foodgrains, and wheat in particular, thanks to favourable weather conditions during the winter crop sowing period. Preliminary estimates for 2000 point to a minor decline in production of less than 1 percent. A further increase in crop production, particularly cereals, appears to have been counterbalanced by a decline in livestock production.

Bangladesh, where floods are a constant threat, has seen strong but uneven agricultural production growth over the second half of the past five years. Bumper harvests in 1998 and 1999 fuelled increases in overall agricultural output, estimated to be 3.1 and 8.4 percent, respectively. Floods in 2000 implied significant crop losses in the areas affected, and agricultural output is estimated to have increased by less than 2 percent.

In 1998 and 1999, Pakistan experienced two consecutive years of agricultural output growth in the range of 4 to 4.5 percent. Wheat and cotton traditionally account for more than half of the output of major crops. In 1998, while the cotton crop suffered a decline as the combined result of bad weather and a leaf curl virus attack, cereal output expanded strongly. In 1999, cotton output expanded strongly and the previous year's high levels of cereal output were maintained. Estimates for 2000 point to a small increase in agricultural production, not exceeding 1 percent.

Agricultural production in Indonesia has shown a relatively poor performance over the past three to four years. In 1998, for the second consecutive year, overall output declined - by 1.5 percent - largely as a result of El Niño-induced drought conditions but also owing to the effects of the economic crisis. The subsequent recovery in production has nevertheless been slow; overall agricultural output increased by only 1.6 percent in 1999 and the preliminary estimates for 2000 show output to be almost stagnant.

After prolonged drought related to the El Niño phenomenon, which contributed to a contraction of more than 7 percent of agricultural production in 1998, the 1999 monsoon arrived in the Philippines about two months earlier than usual, boosting that year's agricultural growth to almost 9 percent. Rice and maize production gained in particular, following a sharp contraction the preceding year. An expansion in output of between 1 and 2 percent is the provisional estimate for 2000.

In Thailand also, agricultural production in 1998 suffered severely from El Niño-related weather effects and reduced import demand in other Southeast Asian nations. Overall agricultural production in 1998 declined by 3.5 percent. Recovery has since been only modest, with production increasing by about 1.5 percent in 1999 and probably by less than 1 percent in 2000.

In Malaysia, too, agricultural production in 1998 suffered from the negative effects of adverse weather as well as labour shortages caused by the departure of foreign workers. However, at 1.5 percent, the overall decline in production was more modest than in the Philippines and Thailand. Production rebounded by more than 5 percent in 1999, mainly owing to a strong expansion in oil crops, while rubber production continued to follow a downward trend. Overall agricultural production in 2000 appears to have remained almost unchanged from the level of 1999.

Viet Nam continued the strong rate of agricultural production growth that characterized the 1990s, recording an expansion in agricultural production of 7 percent in 1999, the highest rate since 1992. The country's exceptional output performance in 1999 seems to have been followed by more modest growth in 2000, as preliminary estimates suggest an increase in overall agricultural production of about 2 percent (for an overview of Viet Nam's agriculture sector).

The financial crisis in Asia is an illustrative example of the instabilities that may confront the agriculture and rural sector, particularly given its growing intersectoral and world market linkages. Problems related to the financial crisis in Southeast Asia were compounded by drought conditions resulting from the El Niño phenomenon.

Table 20

INDICATORS OF THE SOCIAL IMPACT OF THE ASIAN CRISIS

Indicator |

China |

Indonesia |

Malaysia |

Philippines |

Rep. of Korea |

Thailand |

(Percentage) | ||||||

Annual growth in private consumption per capita |

||||||

1990-96 |

8.3 |

6.8 |

5.4 |

1.0 |

6.5 |

6.4 |

1998 |

5.5 |

-4.7 |

-12.6 |

1.3 |

-10.2 |

-15.1 |

Poverty incidence1 |

||||||

1996 |

4.7 |

11.3 |

8.2 |

37.5 |

9.6 |

11.4 |

1998 |

3.4 |

20.3 |

19.2 |

13.0 | ||

Unemployment rate |

||||||

1996 |

5.6 |

4.9 |

2.5 |

8.6 |

2.0 |

1.8 |

1998 |

9.1 |

5.5 |

3.2 |

10.1 |

6.8 |

4.5 |

1 Based on national poverty lines. | ||||||

Social impact. The social impact of the crisis has been significant but less severe than was feared at the height of the crisis. This is partly because the recovery has been faster than anticipated and partly because of the public transfer mechanisms that were set up in some of the countries affected. Furthermore, the absorption of unemployed urban dwellers into the agriculture sector and the existence of other informal safety nets have mitigated the impact. However, the Asian Development Bank (AsDB) reports that the social recovery is still slow and that it is causing a lag in the overall economic recovery.58

Poverty indicators deteriorated significantly in all the countries affected by the crisis.59 Indonesia, where the contraction in GDP was sharpest, experienced the greatest increase in poverty. It was estimated60 that a 12 percent contraction of GDP in 1998 would be accompanied by an increase in the poverty rate from 11.3 percent in January 1996 to 14.1 percent in March 1999, with the increase being relatively larger in urban areas. Real wages in Indonesia are estimated to have fallen by 41 percent in 1998. It is notable that the incidence of poverty increased more sharply in urban than in rural areas, although the largest absolute increase in the number of poor was in rural areas. In Thailand, the opposite pattern was discernible: rural poverty increased, while the percentage of poor in the urban areas remained unchanged. In countries where a sizeable share of the population is close to the poverty threshold, such as Indonesia and the Philippines, declining levels of income and consumption per capita lead to more immediate increases in the incidence and intensity of poverty. In these areas, the speed or slowness of recovery can make a crucial difference to the livelihood of many people.

The largest impact on labour markets occurred in Indonesia, the Republic of Korea and Thailand. The impact on employment was less pronounced in the Philippines, which had also experienced lower rates of growth prior to the crisis. In Malaysia, the group that was most affected was the foreign labour force.61 Youth unemployment rates generally rose faster than those for adults. In addition to increased unemployment rates, households were also affected by declining real wages. Indeed, most of the labour market adjustment affected earnings rather than creating open unemployment. In addition, there was a shift from formal to informal employment.

The crisis strongly affected the food security of the most vulnerable groups of society. Currency devaluations and rising food prices shifted internal terms of trade to the advantage of farmers with marketable surpluses. But the same higher prices put many staple foods out of the reach of low-income groups, thereby reducing food security. Changes in the prices of basic goods are very disruptive, especially for the poor. Even modest increases in food prices adversely affect people's nutritional status, particularly in the case of pregnant and lactating mothers, infants and pre-schoolchildren. The increase in agricultural prices during the Asian crisis negatively affected the welfare of the urban poor, as they use a large proportion of their income to buy food. In rural areas, where the poorest tend to be net buyers of food staples and access to safety net programmes is usually limited, if not absent, rising food prices likewise had adverse effects. In Indonesia, for instance, the amount of rice that could be purchased with the daily minimum wage fell by more than two-thirds between January 1997 and October 1998. FAO calculated that the number of undernourished in Indonesia certainly almost doubled from 6 percent of the population in 1995-97 to about 12 percent in 1999.62

Response to the crisis. The response to the crisis took a variety of forms. At the household level, various coping mechanisms have been observed, including adjustments in consumption, dissaving and use of family labour. On the consumption side, households reduced their food expenditure and substituted cheaper, lower-quality sources of calories, which has had a negative impact on the agriculture sector. Household savings that had been accumulated during the successive high-growth years helped many of the families who encountered unemployment or sharp cuts in wages.

Migration was also an important coping mechanism during the crisis.63 In the worst-affected countries, there was an unusual reverse migration from urban to rural areas. In Thailand, the government estimated that 188 000 urban unemployed left Bangkok in search of better prospects in the countryside. Significant shifts in employment from the non-farm to the farm sector were also observed in Indonesia and the Republic of Korea. At the same time, the higher degree of urban unemployment hurt rural families who depended on remittances from urban relatives.

Governments responded through existing and new or expanded social safety nets. The instruments used differed among the countries. Indonesia launched a new programme of targeted cheap rice distribution in July 1998. The programme was planned to ensure 20 kg of rice at subsidized prices to households selected according to specified criteria and, by January 2000, it was reaching 10 million households. Indonesia, the Republic of Korea and Thailand introduced, expanded or redesigned public workfare schemes. In the Republic of Korea, the unemployment insurance scheme was expanded, while severance pay was increased in Thailand. Both Indonesia and Thailand relied on schemes to promote school enrolment (with scholarships and school fee waivers, etc.). Thailand expanded school lunch programmes. Active labour market policies were also important, particularly vocational training or job retraining (in Malaysia, the Philippines, the Republic of Korea and Thailand) and job placement programmes (in the Philippines and the Republic of Korea). Other instruments included subsidized health care (in Thailand) or essential drugs (in Indonesia), community-based social programmes (in Indonesia and Thailand) and various social- or income-support programmes (e.g. in the Republic of Korea and Thailand).

Challenges to the agriculture sector. The Asian economic crisis posed a number of challenges to the agriculture sector. More than ever, it was left to absorb displaced labour, contribute foreign exchange revenues, increase domestic food supply and generate resources for domestic investment.

The drastic currency depreciations that took place64 had a mixed impact on agriculture. They tended to correct the overvaluation of national currencies and enhance the relative prices of tradable agricultural goods, creating incentives for increased farm production and revenues. Export commodity production was encouraged while food and feed imports were depressed. To some extent, however, this positive effect was counterbalanced by the adverse effect of higher prices for imported inputs, such as fertilizer and fuel. The actual realization of potential increases in farm production was slow because structural rigidities and capital availability in poor areas often hampered the capacity of farm households to respond to price changes.

Restraints on government spending also reduced, at least in the initial stages of the crisis, the resources available for the provision of public goods to farmers. Cuts in government investment in rural areas were particularly severe in the worst-affected countries. Since investments in agricultural infrastructure and research often have long lead times, the effects of these cuts could be long-lasting and may also take time to become fully apparent.

The agricultural supply response was also restricted by high interest rates and the credit squeeze on operating capital, especially for essential inputs (e.g. seeds and fertilizer) and the marketing and distribution of agricultural produce, including export and import activities. With a sluggish supply response, food prices rose in the wake of currency devaluation. The increase in food prices was particularly sharp in Indonesia, where the monthly average market price for rice rose from about 1 500 rupiah per kg in March 1998 to 3 000 rupiah in September of the same year.

The effects on farm households through the employment channel were mostly negative. Urban demand fell, particularly for agricultural products with a high income elasticity such as livestock and horticultural products. Rural non-farm employment and remittances from family members in non-agriculture sectors declined. The reverse urban-rural labour migration triggered by the crisis depressed rural wage rates and partially offset any income gains through the exchange rate channel.

Lessons from the crisis. Many impacts of the Asian financial crisis will only be fully revealed with time. What is evident from the Asian crisis, however, is the capacity of society to protect consumption and welfare levels during transitory shocks in cases where increases in incomes have been sustained by economic growth during the preceding decades. Asia's past achievements in economic growth and poverty reduction have no parallel in recent history and have prevented many families from reverting to absolute poverty. At the same time, the special role of targeted employment and social sector programmes was amply demonstrated in alleviating the transitory hardships faced by the poor in a recessionary situation.

Agriculture is the most critical sector in poverty alleviation, since the poor are mainly to be found in rural areas and are predominantly employed in, or otherwise dependent on, agriculture. Although the sector has encountered difficulties in the wake of the crisis, for example in the form of higher input costs, reduced investment and lower domestic demand for high-value products, it demonstrated considerable resilience against the shocks of the crisis.

The long-term effects of the crisis on the agriculture sectors of affected countries are still uncertain. With the currency depreciations, the implicit taxation of agriculture was either reduced or eliminated, and economic recovery has begun in most parts of the crisis-stricken countries. This implies new opportunities for the agriculture and rural sector to contribute to economic growth and poverty alleviation. However, to allow the sector to reap the benefits of the improved incentives, its capacity to respond to changes should be further enhanced. The role of the public sector in improving marketing conditions, infrastructure, research and extension activities is fundamental in this regard.

Viet Nam covers a total land area of approximately 33 million ha. Three-quarters of the country is made up of mountains and hills, while the remainder consists of fertile river plains, the main ones being the Red River delta in the north and the Mekong River delta in the south.

Viet Nam is one of the poorest countries in the world. With a per capita GNP of only $350 in 1998, the country ranks 173rd on the World Bank's classification list.65 In spite of this, it compares very favourably with other developing countries when judged by a number of social indicators. Life expectancy at birth is 68 years, compared with an average of 60 years for the low-income countries (and 70 years for the middle-income countries), while the infant mortality rate is 34 per 1 000 live births, compared with the average of 68 for the low-income countries overall and 31 for the middle-income countries. Adult literacy rates are likewise much higher than usual for low-income countries. Thus, the youth illiteracy rate (for the age group of 15 to 24 years) is only 3 percent for both males and females.66

Agricultural land amounts to 7.9 million ha, 3 million of which are irrigated.67 The forest cover is estimated to be approximately 9.3 million ha.68 Most of the lowlands are under rice cultivation, while the uplands are planted to other annual crops (sweet potato, cassava, maize, groundnut, soybean, sugar cane and tobacco) or permanent crops (coffee, tea, rubber, mulberry, coconut and pepper).

Viet Nam has a population of 79 million, 80 percent of whom live in rural areas. Rural population densities are quite high, with a national average of 194 people per km2. Regional differences in population densities are, however, significant. The most heavily populated area is the Red River delta, where densities range from about 890 to 1 090 people per km2.69

Agriculture (including fisheries and forestry) is by far the most important sector in terms of its contribution to the population's livelihood. The total agricultural population amounts to 53 million people70 and the sector employs nearly 70 percent (68 percent in 1999) of the country's economically active population, although its contribution to GDP amounts to a more modest 26 percent.71

Viet Nam, which was formerly a centrally planned economy, has undertaken very significant economic reforms over the past decade in the direction of a market economy. Gradual economic reforms had in fact been initiated earlier;72 the first steps were taken in 1981, with the introduction of a contract system in agriculture as well as increased autonomy for state-owned enterprises.

A major impetus to the reform process came in 1986, when the Sixth National Congress of the Vietnamese Communist Party endorsed a comprehensive policy shift towards a market economy, based on the coexistence of a government sector and a private sector. The new policy direction was referred to as doi moi (renewal). Four major policy reforms were subsequently implemented as a result of the decisions made in 1986:73

In the face of a rapidly widening government deficit and the emergence of hyperinflation, in 1989 the Vietnamese Government embarked on a macroeconomic stabilization programme, which was modelled on traditional IMF-supported programmes but did not receive IMF financial support.74 The cornerstone of the programme was the liberalization of domestic markets, with almost all prices decontrolled (including those of rice), along with an exchange rate reform which led to a unification of the official and parallel exchange rates in 1982. At the same time, foreign trade was eased through, inter alia, easier access to foreign exchange, and positive real interest rates were introduced. A serious effort was also made to reduce the large budget deficit, for example by eliminating the previous direct subsidies to state-owned enterprises. A final important element in the macroeconomic reform was an overhaul of the tax system. This involved the introduction of a range of new taxes and equality of treatment for private and state-owned enterprises. Furthermore, the previous system of contributions from state enterprises to the budget was abolished in favour of regular taxation.

The following period, the 1990s, saw a consolidation of the reforms initiated in the 1980s. A fundamental component of those reforms has been Viet Nam's increased integration into the world economy. An important step was the country's accession to the Association of Southeast Asian Nations (ASEAN) in 1995 and to the ASEAN Free Trade Area (AFTA) in 1996, whereby it took on the commitment to abolish almost all quantitative trade restrictions and reduce tariffs imposed on other ASEAN members by 2006. In addition, a comprehensive trade agreement with the United States was signed in July 2000.

The response of the Vietnamese economy to economic reforms has been rapid and impressive (see Table 21).

Table 21

REAL GDP GROWTH AND CONSUMER PRICE INFLATION IN VIET NAM

Year |

Real GDP growth |

Annual inflation rate |

(Percentage) | ||

1979-88 |

4.9 |

118.4 |

1989 |

7.8 |

35 |

1990 |

4.9 |

67 |

1991 |

6.0 |

68.1 |

1992 |

8.6 |

18.2 |

1993 |

8.1 |

8.4 |

1994 |

8.8 |

9.4 |

1995 |

9.5 |

16.9 |

1996 |

9.3 |

5.6 |

1997 |

8.2 |

3.1 |

1998 |

3.5 |

7.9 |

1999 |

4.2 |

4.1 |

20001 |

4.5 |

0.5 |

1Projections. | ||

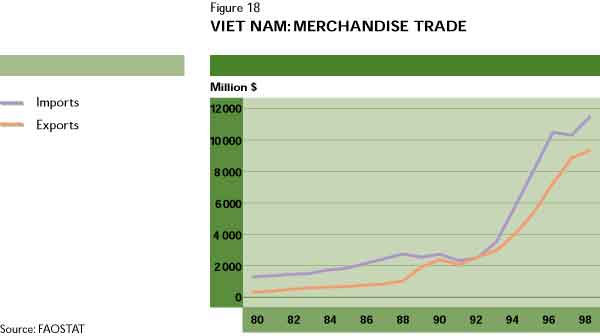

Real GDP growth averaged 7.9 percent per year in 1989-97, while inflation rates have been reduced and foreign trade has likewise expanded rapidly (Figure 18). A particularly important role in the development of the Vietnamese economy has been played

by FDI (Table 22).

Table 22

DISBURSEMENTS OF FOREIGN DIRECT INVESTMENT TO VIET NAM

Year |

Value |

Percentage of GDP |

1988-91 |

168 |

2.0 |

1992 |

316 |

3.9 |

1993 |

922 |

7.8 |

1994 |

1 636 |

11.2 |

1995 |

2 276 |

14.2 |

1996 |

1 813 |

12.3 |

1997 |

2 074 |

8.7 |

1998 |

800 |

6.7 |

19991 |

700 |

5.2 |

1 Preliminary estimates. | ||

After a number of years of very high growth, the Vietnamese economy slowed down significantly in 1998, as the country was hit by the financial crisis in Southeast Asia and flows of FDI also fell. In contrast with the situation in other countries of the region, this translated only into a slowdown in economic growth, to 3.5 percent in 1998, rather than an actual decline in GDP. Economic recovery commenced in mid-1999, with the GDP growth rate rising to an estimated 4.2 percent in 1999 and a projected 4.5 percent in 2000. These are still well below the rates experienced in the years preceding the slowdown, however.

Rapid economic growth, combined with a relatively equitable distribution of assets and services such as health care and education, has enabled a significant reduction in poverty. Surveys of living standards, conducted in 1992/93 and 1997/98 by the General Statistical Office with technical assistance from the World Bank, revealed a significant reduction in poverty levels over the five-year period. Based on a food poverty line (set at the income level required for purchasing enough food to provide 2 100 calories per capita per day) the survey results show a decline in the incidence of poverty from 24.9 percent in 1992 to 15 percent in 1997/98.75 Based on a broader general poverty indicator, which combines the food poverty line (representing 70 percent of expenditure level) with a 30 percent non-food expenditure component, the World Bank estimates the incidence of poverty to have declined from 58.1 percent in 1992/93 to 37.4 percent in 1997/98.

Reductions in poverty levels have been evident in both rural and urban areas. However, poverty in rural areas - where 94 percent of the poor live - remains much more significant and has been reduced at a slower rate than urban poverty (see Table 23).

Table 23

INCIDENCE OF RURAL AND URBAN POVERTY IN VIET NAM

Population group |

1992/93 |

1997/98 |

(Percentage) | ||

Urban poverty incidence |

25.1 |

9.0 |

Rural poverty incidence |

66.4 |

44.9 |

Rural poor as share of total poor |

91.0 |

94.0 |

Rural population as share of total population |

80.0 |

76.5 |

Source: Vietnamese General Statistical Office and World Bank. | ||

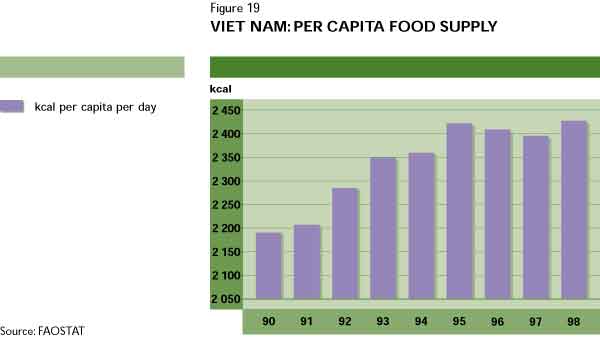

The gains in per capita income, along with booming performances by the agriculture sector since the beginning of the economic reform process (discussed in the following section), enabled significant progress to be made in food security. After having declined in the latter part of the 1980s, per capita food supplies increased from 2 200 kcal per day in 1990 to more than 2 400 in 1998. The prevalence of undernourishment has likewise been significantly reduced, as a result of the reduction in the incidence of poverty. The estimated percentage of undernourished in the total population fell from 33 percent in 1979-81 to 28 percent in 1990-92 and 22 percent in 1996-98.

The agriculture sector is central to the Vietnamese economy and hence to the country's reform efforts. Prior to the beginning of the doi moi reforms, the sector was characterized by a pronounced geographical dichotomy in its organization. In the northern part of the country, the collectivization of agriculture had been introduced after independence in 1954.76 A drive for full-scale collectivization of agriculture commenced in the north in 1958. By 1960, more than 40 000 production cooperatives had already been established, covering 85 percent of the farm population.77 Despite the relative failure of the cooperatives, which resulted in decreasing farm incomes and per capita food availability, the collectivization was still pushed further in the direction of larger units and more specialized organization of production.

With reunification in 1975, the collectivization process was extended to the southern part of the country, where it faced problems and major resistance that prevented it from functioning effectively, and a large number of cooperatives were merely nominal. Poor production performances and stagnating per capita food production continued to characterize the agriculture sector.

The failure of collectivization was among the driving forces behind the subsequent reform efforts. As mentioned earlier, the first efforts to carry out reform in agriculture were made in 1981 but more profound reform was only introduced in 1988. For the agriculture sector, the reforms implied first and foremost a departure from the collective organization of production and a return to the farm household as the basic unit of production. Farmers were allowed to own farm machinery, instruments and animals and were granted the right to farm land that was contracted from the cooperatives. The marketing of agricultural products was likewise liberalized; producers were allowed to market their produce freely and state procurement was abolished.

A strengthening of the reforms was initiated in 1993, following the adoption of Resolution 5 at the Seventh Party Congress. The decisions made under the Resolution called for: the promotion of rural development in general, with recognition and encouragement of the private sector's role in the rural economy; and for the renovation of cooperatives and state-owned enterprises, emphasizing their self-government.

With the revised Land Law of 1993, farmers were granted long-term land use rights (20 years for annual crops and 50 years for perennial crops), together with the right to transfer, exchange and inherit land and to use land as collateral. Through a revision of the Land Law in 1998, land use rights were further expanded, with an extension of lease rights and the possibility of granting land use rights to people other than farmers. On the basis of the new land legislation, land has been distributed and land use certificates issued. The distribution has been based on principles of equitable distribution within localities. By late 1999, the process of distribution was basically finished in the case of agricultural land, and 60 percent of the land use certificates applied for had been awarded.78

A further important reform element was that of agricultural taxation based on land use. Six different tax rates for paddy were established according to soil fertility and converted into monetary terms at the market price of paddy at the time of payment. Under the reform of credit policy, lending to farm households by the commercial banking sector has been introduced, notably by the Viet Nam Bank for Agriculture.

The reform process has implied the transformation of cooperatives from units for the organization of production into units for the provision of services to farmers. The new role envisaged is embodied in the new law on cooperatives, which was enacted in January 1997 and is in the process of being implemented. The law requires the traditional cooperatives to restructure and to elect new managers. In spite of some difficulties, in late 1999 government officials estimated that about 60 percent of the 10 000 or so cooperatives had conformed to these requirements, and approximately 100 new cooperatives had been created by July 1997. While the cooperatives are prevalent mainly in the Red River delta and the central coastal area, other types of farmers' associations (of which there are an estimated 10 000) are prevalent in the Mekong River delta.

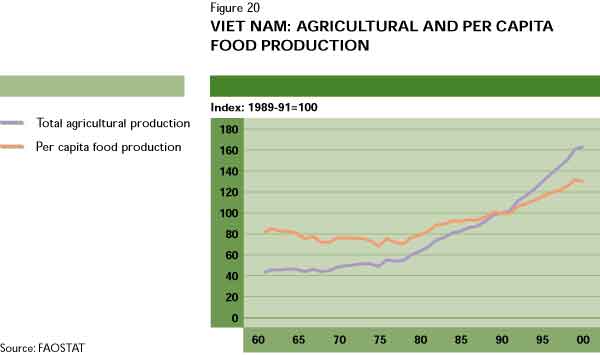

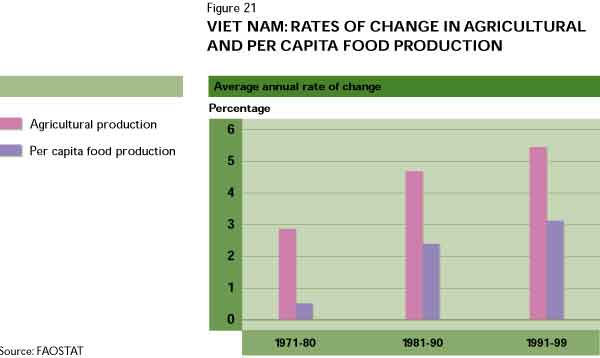

Vietnamese agriculture has responded dynamically to the policy reforms (see Figure 21). Overall agricultural production expanded at an average annual rate of 5.4 percent over the ten-year period 1991-99, with per capita food production increasing by an annual 3.1 percent over the same period. Most important has been the rapid expansion in rice production, the main staple crop, since the late 1980s. This has allowed Viet Nam not only to turn from a small net importer to a large net exporter of rice from 1989 onwards (see Table 24), but to become the world's third largest rice exporter in terms of volume after Thailand and India, and the fourth largest in value terms after Thailand, India and the United States.

Table 24

VIET NAM'S NET RICE IMPORTS AND EXPORTS

Imports |

Exports |

Net exports | |

(Thousand tonnes) | |||

1985 |

336 |

59 |

-277 |

1986 |

483 |

132 |

-351 |

1987 |

323 |

120 |

-202 |

1988 |

200 |

91 |

-108 |

1989 |

55 |

1 420 |

1 365 |

1990 |

2 |

1 624 |

1 622 |

1991 |

6 |

1 033 |

1 027 |

1992 |

2 |

1 946 |

1 944 |

1993 |

1 |

1 722 |

1 721 |

1994 |

0 |

1 983 |

1 983 |

1995 |

11 |

1 988 |

1 977 |

1996 |

0 |

3 500 |

3 500 |

1997 |

0 |

3 575 |

3 575 |

1998 |

0 |

3 800 |

3 800 |

Source: FAOSTAT. | |||

In 1998, Vietnamese rice exports represented 13 percent of the world total in volume terms and 10 percent in value terms. The lower share in value terms is due to the generally lower quality of Vietnamese rice, a result of inadequacies in the processing phase.

Production has also expanded impressively for a range of other crops, leading to an increased diversification of Vietnamese agriculture (see Table 25).

Table 25

PRODUCTION OF SELECTED CROPS IN VIET NAM

Crop |

1989 |

1998 |

Percentage change |

(Thousand tonnes) | |||

Rice, paddy |

18 996 |

29 142 |

53.4 |

Maize |

838 |

1 612 |

92.4 |

Coffee, green |

41 |

409 |

903.2 |

Tea |

30 |

51 |

68.8 |

Natural rubber |

51 |

226 |

346.0 |

Total fruit1 |

3 124 |

3 886 |

24.4 |

Bananas |

1 227 |

1 315 |

7.2 |

Oranges |

101 |

379 |

275.2 |

Vegetable, primary |

3 384 |

4 575 |

35.2 |

Groundnuts, in shell |

206 |

386 |

87.6 |

Coconuts |

922 |

1 271 |

37.9 |

1 Excluding melons. | |||

Export earnings from agriculture have increased dramatically since the late 1980s (see Table 26), with rice remaining the most dynamic and important agricultural export product throughout the period. Coffee exports expanded rapidly in the course of the 1990s, becoming the second most important agricultural export product. As evidenced in Table 26, several other products have also shown a dynamic export performance over the last decade.

Table 26

AGRICULTURAL EXPORTS FROM VIET NAM

Export product |

1988 |

1993 |

1998 |

(Million $) | |||

Total merchandise trade |

1 038 |

2 985 |

9 361 |

Total agricultural products |

332 |

731 |

2 281 |

Rice |

27 |

310 |

1 024 |

Coffee, green |

58 |

91 |

594 |

Fruit and vegetables |

51 |

53 |

155 |

Natural rubber |

32 |

77 |

127 |

Cashew nuts |

7 |

30 |

117 |

Pepper, white/long/black |

7 |

9 |

64 |

Groundnuts, shelled |

36 |

46 |

42 |

Maize |

6 |

9 |

40 |

Source: FAOSTAT. | |||

Government policies currently emphasize the improvement of agricultural market linkages and the promotion of rural development. Improving market linkages in agriculture implies, among other measures, a shift away from the traditional emphasis on rice production for food security towards more commercial agricultural production, in particular for exports.

Rural development is the other cornerstone of current government policies. Rural poverty remains pervasive and rural-urban income gaps have been increasing. There is a need to generate off-farm income and employment opportunities as well as to further the process of rural industrialization. This, however, requires rural development based on diversification within agriculture, in order to make agricultural production more responsive to market forces, as well as diversification to other economic activities.

Probably the most serious constraint to rural development in Viet Nam is the underdevelopment of rural infrastructure, including roads, irrigation, drainage, flood control facilities, clean drinking-water, permanent marketplaces and electricity. In particular, the paucity of good transport networks seriously limits the rural population's access to markets. Infrastructure is particularly inadequate in the poorest and most isolated regions.

The government has begun to increase investment in rural infrastructure and services, and one of the instruments it is using is the Poor Communes programme, launched in 1998. Under this programme, funding in the order of 400 million dong (approximately US$30 000) per commune is to be provided for infrastructure projects (irrigation, bridges, roads, schools, health clinics, marketplaces) at the choice of the recipient communes. The programme was originally planned to reach more than 1 700 poor communes, but the target has since been reduced to between 850 and 900 communes.

There are a number of policy-related constraints to Viet Nam's economic development and, above all, rural development. Many of these constraints are related to the country's transition from a centrally planned to a market economy and, in particular, to the still incomplete nature of the economic reform process. Some are of a macroeconomic nature or are general to the overall economy; others are specific to agriculture or rural areas.79

Rural labourers engaged in rice cultivation

Current policies encourage a shift away from food production towards export-oriented agricultural production

FAO/16254/P. JOHNSON

Constraints in the macroeconomic sphere. Although important steps have been taken in the liberalization of foreign trade, Viet Nam's trade regime remains quite restrictive.80 In 1999, based on its own index of trade restrictiveness,81 IMF rated Viet Nam ninth on a scale of one to ten (where ten is the most restrictive).

Protection takes numerous forms, such as restrictions on foreign trading rights, quotas and licence requirements, relatively high tariffs and restricted access to foreign exchange for imports of products that compete with domestic production. Such protection has imposed heavy penalties on the rest of the economy. The effect on the agriculture sector has been to raise the cost of protected inputs. Furthermore, restrictions and government control of rice and other agricultural exports have resulted in reduced prices for primary producers and/or restricted export potential.

A further vestige of the centrally planned economy is the still predominant position of state-owned enterprises, which account for about 30 percent of GDP and 15 percent of non-agricultural employment.82 Preferential treatment and advantages enjoyed by state enterprises tend to incur costs on other sectors of the economy. The restrictive trade regime is geared towards protecting the state enterprise sector, which also absorbs 68 percent (as at end-1998) of total non-government credit. Policies favouring the country's state enterprises have tended to promote capital-intensive and urban industrial development to the detriment of more labour-intensive and rural-based economic activities.

Another cause for concern is the poor economic performance of the state enterprise sector, as this threatens the stability of the banking system as well as the macroeconomic situation. Reform of the sector would appear to be crucial for improved economic performance but has so far been limited.83 It is accelerating, however, and received a special stimulus in December 1999 when an AsDB loan totalling $100 million was approved for the State-owned Enterprise Reform and Corporate Governance Programme.

Sector-specific constraints to agricultural and rural development. Although significant progress has been made,

Viet Nam's agriculture sector is still being constrained by insufficiently competitive markets - a situation caused by remaining market and trade controls and inadequate private sector participation in marketing and trade. Thus, the most important subsector, rice, has traditionally been subject to export controls, which have been justified on the basis of food security considerations. Export quotas, while still in place, have however been gradually increased, so they do not constitute an effective limitation to exports at present.

What may be more serious is the still pervasive role of state-owned enterprises in rice marketing and exports, for which the granting of trading rights is required. The number of companies allowed to export rice nevertheless increased from 17 in 1995 to 47 in 1999, including four private exporters. In June 2000, the Ministries of Trade and Agriculture were charged to revise the system.

Other specific distortions facing the agricultural sector are the high tariffs on sugar, accompanied by occasional import bans, and restrictions on seed and feed imports, which tend to raise the cost of these inputs. Overall, continued liberalization of both domestic trading and international trade, together with more involvement of the private sector in marketing and trade, should enhance competition to the advantage of farmers and allow them to reap greater benefits from their productive efforts.

Land tenure policies are critical to development of both agriculture and the non-farm rural sector. Although the granting of long-term land use rights was institutionalized with the Land Law of 1993 and its revision in 1998, the implementation of the new rules has been and remains difficult. The process has been hampered by implementation problems at the local level. In addition, a lack of clear guidelines on the implementation of land use rights has created uncertainty, particularly with regard to the transfer and mortgage of land, although the issuing of guidelines in 1999 should have led to an improvement. The lack of a liberalized land market, combined with restrictions on land use, acts as an impediment to efficient land allocation, both within agriculture and between farm and non-farm activities in rural areas.

As a consequence of constraints in the credit system, the rural private sector - both agricultural and non-agricultural - has been facing a situation of inadequate financing. Most credit to the rural areas has been provided by the Viet Nam Bank for Agriculture and Rural Development, supplemented by the Bank for the Poor, which was established in 1995 to provide subsidized credit for the poor. The government has been promoting People's Credit Funds, or local savings and credit cooperatives, and a number of microcredit schemes are run by NGOs. In spite of this, access to formal credit, and in particular medium- and long-term credit, remains problematic.

Viet Nam has been making significant economic progress over the last decade through a process of gradual economic reform, but has recently suffered a slowdown under the impact of the Asian financial crisis. The high rates of economic growth realized have nevertheless allowed the country to take major steps towards reducing the incidence of poverty and undernourishment.

The agriculture sector has made an important contribution to the country's economic progress and has responded strongly to economic liberalization and improved incentives. In spite of the reforms already undertaken, Viet Nam's agriculture and rural sector as well as its economy overall still face a number of structural impediments and inadequacies in the legal and institutional framework necessary for an advanced market economy. Whether Viet Nam will resume the high-growth path of the last decade, or instead remain on a lower rate of growth, may depend on its ability to continue and deepen the reform process and to eliminate or ease some of these impediments - which are well recognized by the country's officials.

![]()

![]()

![]()