![]()

![]()

![]()

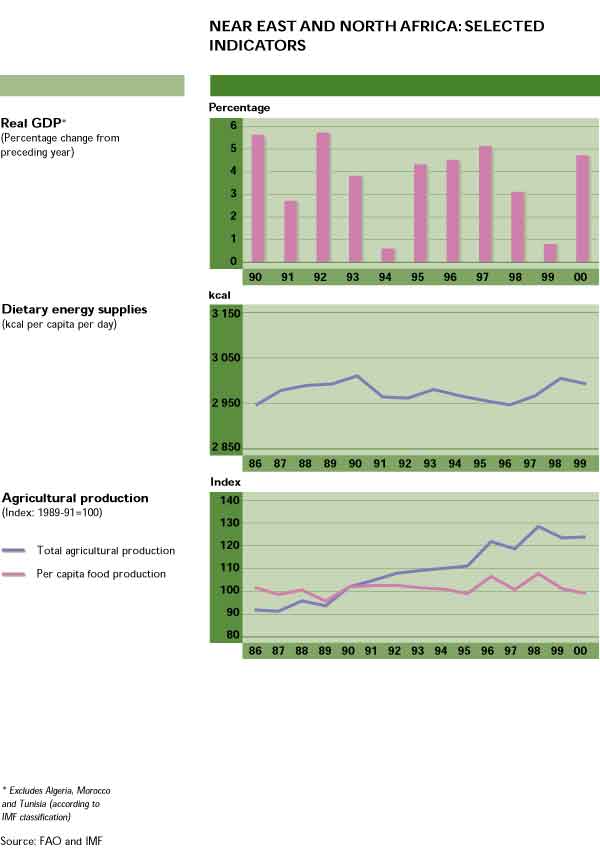

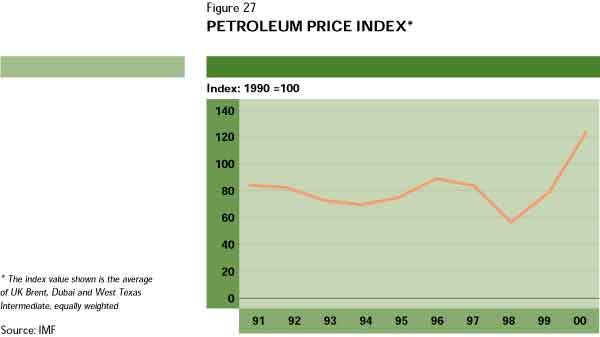

Over the last two years the economic situation in the Near East and North Africa has been shaped to a very large extent by sharp fluctuations in oil prices. Initially the oil price collapse of 1998 severely depressed the economic prospects for many of the oil-exporting countries and economic growth fell to only 0.8 percent in 1999. Moreover, severe drought in many North African and Near Eastern countries, together with the devastating earthquake in Turkey, undermined growth prospects in many of the non-oil-producing countries.

However, the recovery of oil prices from less than $12 per barrel in the first quarter of 1999 to almost $30 in the fourth quarter of 2000 helped to fuel a recovery in many countries of the region. Consequently, countries in the region showed a generally good economic performance in 2000, with regional real GDP growth estimated to be about 4.7 percent. In a number of countries, fiscal reform, privatization and increased foreign investment are key policy goals being pursued by governments. If carried through, these reform policies would improve economic prospects for the near future.

Table 32

ANNUAL REAL GDP GROWTH RATES IN THE NEAR EAST AND NORTH AFRICA

Country/region |

1996 |

1997 |

1998 |

1999 |

2000 |

20011 |

(Percentage) | ||||||

Algeria |

3.8 |

1.1 |

5.1 |

3.3 |

4.3 |

4.2 |

Egypt |

4.9 |

5.5 |

5.6 |

6.0 |

5.0 |

4.5 |

Iran, Islamic Republic |

5.5 |

3.4 |

2.2 |

2.5 |

3.4 |

4.0 |

Morocco |

12.2 |

-2.2 |

6.8 |

-0.7 |

2.4 |

5.0 |

Saudi Arabia |

1.4 |

2.7 |

1.6 |

-1.0 |

3.5 |

2.9 |

Turkey |

6.9 |

7.6 |

3.1 |

-5.0 |

4.5 |

4.8 |

Near East and North Africa2 |

4.6 |

5.1 |

3.1 |

0.8 |

4.7 |

4.1 |

1Projections. | ||||||

The Arabian Peninsula and the Gulf states are those most affected by oil price swings. Their terms of trade showed a remarkable upturn in 2000, following two years of deterioration. Real GDP growth in this subregion is estimated to increase from about 2 percent in 1999 to 4 percent in 2000 with continued strong growth anticipated for 2001. Growth in Saudi Arabia is expected to recover from -1.0 percent in 1999 to 3.5 percent in 2000, while the Islamic Republic of Iran saw its real GDP growth rise from 2.5 percent in 1999 to 3.4 percent in 2000.

The Eastern Mediterranean region has continued with steady growth, reaching 3.9 percent in 2000. Egypt's real GDP is estimated to have grown by 5 percent in 2000 after a 6 percent growth rate in 1999. Growth in Jordan is likely to accelerate to 3 percent for 2000.

Economic growth in Turkey fell sharply to 3.1 percent in 1998, after being affected by the Russian financial crisis. The anticipated recovery in 1999 was quashed by the devastating earthquake that left approximately 17 000 dead and disrupted production and services. The poor performance of the agriculture and tourism sectors also contributed to the 5 percent contraction of GDP. For 2000, a moderate 4.5 percent recovery is estimated.

North African economies are expected to grow on average by 4.6 percent in 2000, after the 3.4 percent rise recorded in 1999. Strong growth in the oil and gas sector will lift Libyan output growth to 6.5 percent in 2000, after several years of weak growth. Algeria's growth accelerated to 4.3 percent in 2000, although its agriculture sector suffered severe drought.

Table 33

EXPORT DEPENDENCY AND TERMS OF TRADE OF OIL-EXPORTING COUNTRIES IN THE NEAR EAST AND NORTH AFRICA

Country |

Share in total exports |

Change in terms of trade | |||

Oil |

Natural gas |

1998 |

1999 |

2000 | |

(Percentage) |

|||||

Libyan Arab Jamahiriya |

91 |

... |

-28 |

-4 |

37 |

Oman |

90 |

... |

-28 |

-4 |

37 |

Yemen |

87 |

... |

-27 |

-4 |

36 |

Kuwait |

85 |

... |

-26 |

-4 |

35 |

Saudi Arabia |

83 |

... |

-26 |

-4 |

34 |

Iran, Islamic Republic |

78 |

... |

-24 |

-3 |

32 |

Syrian Arab Republic |

64 |

... |

-21 |

-4 |

25 |

Algeria |

63 |

27 |

-24 |

-12 |

30 |

Qatar |

63 |

... |

-20 |

-3 |

26 |

United Arab Emirates |

45 |

6 |

-15 |

-4 |

19 |

Bahrain |

27 |

... |

-9 |

-1 |

11 |

Source: IMF. | |||||

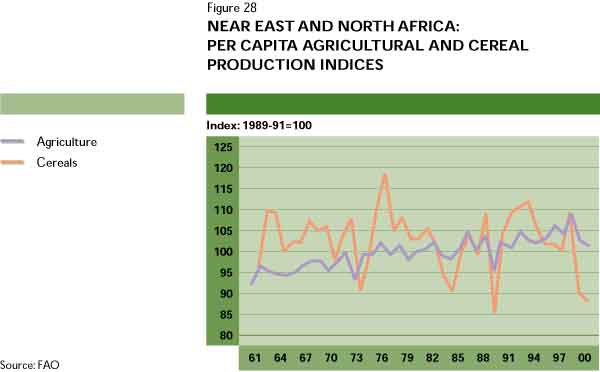

Drought is a recurring phenomenon in the region and causes sharp annual fluctuations in crop and livestock production in many countries, but its impact is most evident in cereal production (Figure 28). The region recorded strong agricultural output growth in 1998, with notable increases reported in Iran, the Syrian Arab Republic and Turkey and with Algeria, Morocco and Tunisia experiencing a significant recovery. However, in 1999 and 2000 the dominant factor in the region was again severe drought conditions.

At the regional level net agricultural production fell by 3.9 percent in 1999, and 2000 saw little improvement as production rose by only 0.3 percent. Cereal production fell by 17.1 and 4.6 percent in the two years, respectively. The Maghreb countries as well as Afghanistan, Iran, Iraq, Jordan, the Syrian Arab Republic, Turkey and Yemen experienced falls in cereal production of between 16 and 80 percent. In per capita terms, agricultural production, and cereal production in particular, dropped off markedly in 1999 and 2000.

Table 34

NET PRODUCTION GROWTH RATES IN THE NEAR EAST AND NORTH AFRICA

Year |

Agriculture |

Cereals |

Crops |

Food |

Livestock |

Non-food |

(Percentage) | ||||||

1991-95 |

1.8 |

0.4 |

1.8 |

1.8 |

2.2 |

1.3 |

1996 |

9.8 |

17.1 |

12.6 |

10.1 |

2.9 |

5.0 |

1997 |

-2.7 |

-11.5 |

-6.3 |

-3.3 |

5.9 |

8.1 |

1998 |

8.4 |

17.0 |

10.5 |

9.4 |

2.9 |

-6.6 |

1999 |

-3.9 |

-17.1 |

-6.7 |

-4.2 |

2.3 |

0.8 |

20001 |

0.3 |

-4.6 |

0.3 |

0.3 |

0.0 |

0.2 |

1 Estimates. | ||||||

Afghanistan suffered two consecutive years of drought in 1999 and 2000, which exacerbated the already precarious food supply situation caused by ongoing civil strife. About half the country's population is affected and more than 3 million people are facing severe food shortages. Production of cereal crops declined by 16 percent in 1999 and is estimated to have declined by another 44 percent in 2000. Animal losses have also been heavy.

Iran suffered droughts in 1999 and 2000 that were even worse than the severe drought of 1964 and have affected more than half of the country's population. In 1999, wheat production declined by 3.3 million tonnes. While production in 2000 is estimated to have risen by 6.7 percent, it is still 2.7 million tonnes below the level of the 1998 harvest. Rice and barley output fell by 15 and 39 percent, respectively, between 1998 and 2000. Animal losses are estimated to be about

800 000. In neighbouring Iraq, drought also caused a large drop in cereal production, with the 1999 harvest 35 percent below that of 1998. Production in 2000 is estimated to be 795 000 tonnes, signifying a further drop of 52 percent owing to continued drought conditions and shortages of essential agricultural inputs.

Two consecutive years of drought have also seriously affected cereal and horticultural crops in Jordan. Wheat production fell sharply by 74 percent in 1999 and, although output is estimated to have recovered somewhat in 2000, it is still 20 percent below the 1998 level.

In the Syrian Arab Republic, the severe drought of 1999 reduced cereal production, which was 62 percent lower than the bumper crop of 1998. Wheat, barley and maize output in 1999 fell by between 35 and 51 percent. However, a modest recovery is expected in 2000, with cereal production expected to rise by about 16 percent. Inadequate rainfall contributed to an 8.7 percent fall in Turkey's cereal output in 1999, with wheat and barley production down by 14 and 24 percent, respectively. For 2000, some recovery in cereal production is expected.

Algeria, Morocco and Tunisia were also hit by severe drought conditions in 1999 and their combined cereal production declined by 36 percent compared with 1998, which was a normal year. Inadequate rainfall affected the winter crops for 2000 in these countries, whose combined output of cereals suffered a further decline of 39 percent. In Algeria, wheat production dropped from 2.3 million tonnes in 1998 to 1.1 million tonnes in 1999 and to an estimated 0.8 million tonnes in 2000. Barley output fell by 43 percent between 1998 and 2000. Wheat production in Morocco fell by 51 percent in 1999 and by a further 36 percent in 2000. Barley output contracted by 76 percent between 1998 and 2000. Tunisian wheat and barley output fell by 38 and 20 percent, respectively, between 1998 and 2000.

In contrast, Egyptian wheat production for the period was about 5 percent higher than the already above-average 1999 harvest. Rice production is estimated to have increased by 34 percent between 1998 and 2000, although maize and seed cotton output was up only marginally on 1998 figures.

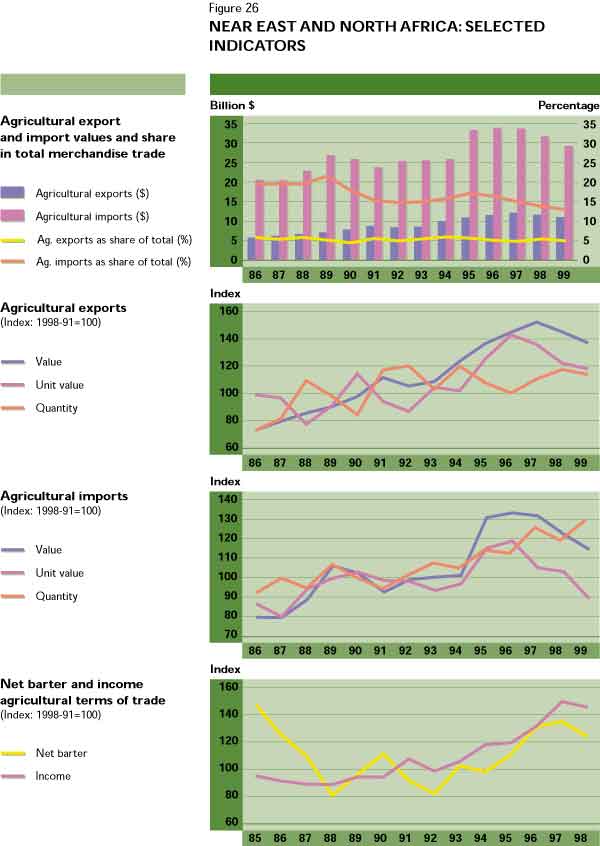

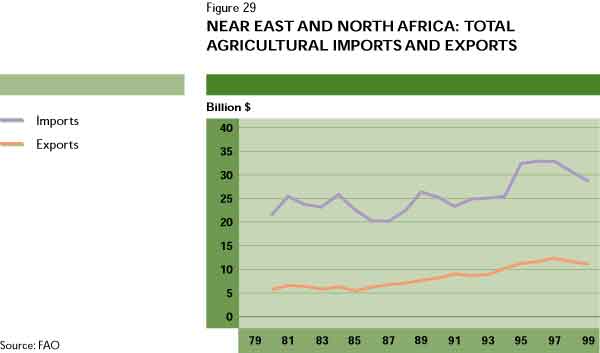

The Near East and North Africa region has remained a large net importer of agricultural commodities over the last two decades. The value of annual agricultural imports has been hovering around $30 billion, which is three times the value of the region's exports.

The share of agricultural imports in total imports has remained relatively stable at about 16 percent, but with considerable variations among countries. The region is becoming increasingly more dependent on imported food items, especially cereals, followed by dairy products, sugar and vegetable oil.

In 1999, about 55 million tonnes of cereals were imported. This is about one-fifth of world imports of these commodities and makes the region vulnerable to any sharp rise in the international prices of cereals.

Table 35

NET PRODUCTION GROWTH RATES IN SELECTED COUNTRIES OF THE NEAR EAST AND NORTH AFRICA

Year |

Algeria |

Egypt |

Iran, |

Morocco |

Syrian |

Tunisia |

Turkey | ||

(Percentage) | |||||||||

Agriculture |

|||||||||

1991-95 |

5.7 |

4.1 |

4.9 |

-2.0 |

5.1 |

-1.5 |

0.5 | ||

1996 |

17.6 |

10.5 |

5.3 |

54.4 |

11.7 |

72.9 |

4.4 | ||

1997 |

-19.9 |

5.1 |

-2.1 |

-15.0 |

-6.6 |

-31.4 |

-0.8 | ||

1998 |

12.1 |

-1.2 |

14.7 |

14.7 |

20.7 |

26.3 |

6.4 | ||

1999 |

4.6 |

6.4 |

-6.1 |

-11.2 |

-17.2 |

4.8 |

-4.7 | ||

20001 |

-4.1 |

1.0 |

3.4 |

-6.3 |

9.3 |

-1.4 |

-0.1 | ||

Cereals |

|||||||||

1991-95 |

30.7 |

4.4 |

4.5 |

25.6 |

15.1 |

-8.4 |

-1.0 | ||

1996 |

129.1 |

2.8 |

-5.6 |

466.6 |

-1.7 |

361.2 |

4.3 | ||

1997 |

-82.3 |

9.2 |

1.7 |

-59.4 |

-27.9 |

-63.2 |

1.4 | ||

1998 |

247.8 |

-0.6 |

20.0 |

61.8 |

22.0 |

57.9 |

11.6 | ||

1999 |

-49.1 |

7.9 |

-27.7 |

-41.8 |

-37.9 |

9.1 |

-15.4 | ||

20001 |

-20.4 |

3.4 |

4.2 |

-46.1 |

6.9 |

-39.8 |

0.0 | ||

Roots and tubers |

|||||||||

1991-95 |

13.5 |

13.8 |

4.4 |

1.1 |

4.5 |

1.7 |

2.2 | ||

1996 |

-4.2 |

1.3 |

2.1 |

39.8 |

-6.8 |

15.9 |

4.2 | ||

1997 |

-17.6 |

-28.6 |

4.6 |

-4.5 |

-39.5 |

7.0 |

3.0 | ||

1998 |

16.1 |

9.6 |

4.5 |

-6.0 |

85.4 |

2.1 |

4.2 | ||

1999 |

-9.4 |

-9.2 |

0.1 |

1.6 |

0.9 |

8.5 |

0.0 | ||

20001 |

-4.6 |

-0.3 |

0.5 |

-6.2 |

-9.4 |

-9.4 |

0.0 | ||

Vegetables |

|||||||||

1991-95 |

11.0 |

2.2 |

-0.3 |

-5.1 |

2.9 |

1.1 |

4.0 | ||

1996 |

-5.0 |

14.2 |

28.2 |

43.1 |

-7.8 |

13.4 |

1.5 | ||

1997 |

-0.5 |

5.1 |

3.6 |

-2.0 |

-6.7 |

-8.5 |

-5.5 | ||

1998 |

8.1 |

-0.9 |

12.3 |

15.0 |

24.3 |

10.2 |

3.9 | ||

1999 |

8.6 |

10.9 |

3.0 |

-8.8 |

-10.7 |

17.0 |

0.0 | ||

20001 |

-9.2 |

0.3 |

3.8 |

6.7 |

3.4 |

0.4 |

0.0 | ||

1 Estimates. | |||||||||

The region's agricultural performance, including its dependency on food imports, has been and continues to be affected by the recent policy reforms that many governments have been implementing.

In 1998, Turkey reduced its import duty on maize from 35 to 20 percent and continued to grant free entry for specified volumes of grain from the European Community (EC) on a year-by-year basis. In Egypt, the privatization of the farm inputs and agroprocessing industries has begun. In 1997, the nine-year ban on poultry imports was lifted, although an 80 percent duty was imposed to protect the local poultry industry. The efficiency of financial intermediation has been enhanced and some restrictions and subsidies have been removed. In Iran, the removal of subsidies on fertilizers and pesticides is proceeding, and Iraq has relaxed restrictions on the procurement of cereals.

The Syrian Arab Republic is implementing a series of policy reforms, involving the pricing of farm produce and marketing and trade regulations for agricultural commodities. To promote output and exports, the government abolished its 21 percent tax on cotton and cotton textiles. In Morocco, quantitative restrictions on external trade have been eliminated and replaced by tariff protection, which in turn is to decline by 2.4 percent annually in compliance with the WTO Agreement on Agriculture. In Tunisia, the Partnership Agreement with the EC foresaw major trade liberalization to be implemented by the year 2000.

Table 36

TOTAL CEREAL IMPORTS FOR THE NEAR EAST AND NORTH AFRICA

Imports | ||

Year |

Volume |

Value |

(Thousand tonnes) |

(Million $) | |

1990 |

41 888 |

7 790 |

1991 |

37 177 |

6 004 |

1992 |

39 090 |

7 005 |

1993 |

39 784 |

7 129 |

1994 |

40 232 |

6 686 |

1995 |

44 365 |

9 214 |

1996 |

42 868 |

10 118 |

1997 |

53 695 |

10 359 |

1998 |

49 769 |

8 331 |

1999 |

54 860 |

7 856 |

Source: FAOSTAT. | ||

Such policy reforms will certainly have a positive impact on the regional economy but may have negative implications for the food security of individual countries in the short term. A number of countries have been seeking group arrangements in the form of trade areas or common markets.106 Cyprus and Turkey have signed a customs union agreement with the EC and are preparing for membership. Efforts to establish a Euro-Mediterranean partnership for the creation of a free trade area by 2010 are intensifying. An EC agreement has been reached with Morocco, Tunisia, Israel and Jordan, and negotiations are continuing with Egypt, Algeria, Lebanon, the Palestinian Authority and the Syrian Arab Republic. The establishment of an Arab Free Trade Area is another promising development.

The Near East and North Africa region has 6.2 percent of the world's population, 8.6 percent of its arable land and 11 percent of its irrigated land, but only 1.5 percent of its renewable freshwater resources. The region relies heavily on surface and underground water. Agriculture is the main user of renewable freshwater: at present, of the 18 countries for which data are available, nine use more than 90 percent, four use from 80 to 90 percent and only five use 80 percent or less of their renewable freshwater supply for agriculture.

Installign an irrigation network

Irrigation has a vital role to play in management fo the region's scarce renewable freshwater resources

FAO/20844/R. MESSORI

It is well recognized that the availability of water for agriculture in the region is extremely low. For the region as whole, annual renewable freshwater resources are estimated to be 698 billion m3. Table 37 shows its distribution by country groupings.

Several countries of the region depend entirely on internal sources for renewable freshwater (e.g. Morocco, the United Arab Emirates and Yemen). The dependency ratio is very high for the most important Arab food-producing countries (e.g. Egypt, Iraq, the Sudan and the Syrian Arab Republic) and very low for the non-Arab food-producing countries such as Iran and Turkey. In the three Maghreb countries where rainfed agriculture is practised (Algeria, Morocco and Tunisia), the ratio of irrigated land to arable land is relatively low.

Table 37

SUPPLY AND WITHDRAWAL OF ANNUAL RENEWABLE FRESHWATER RESOURCES IN THE NEAR EAST AND NORTH AFRICA

Country grouping | ||||

Maghreb |

GCC |

Arab |

Non-Arab | |

Renewable freshwater resources (million m3) |

49 020 |

3 724 |

258 867 |

387 172 |

Population in 1998 (millions) |

72.3 |

28.9 |

155.4 |

151.3 |

Renewable freshwater resources per capita (m3) |

678 |

129 |

1 659 |

2 559 |

Annual renewable freshwater withdrawal (million m3) |

23 220 |

21 410 |

135 309 |

127 955 |

Withdrawal as a percentage of renewable freshwater resources |

47.4 |

574.9 |

52.3 |

33.0 |

Irrigated land (thousand ha) |

2 661 |

1 777 |

10 820 |

14 305 |

1 The Maghreb countries include Algeria, the Libyan Arab Jamahiriya, Morocco and Tunisia. | ||||

If 1 500 m3 of renewable freshwater resources per capita per annum is considered as the threshold, then 15 out of 21 countries in the region were below the threshold in 1995 and six countries remained above it. Six countries had less than 200 m3 of renewable freshwater per capita per annum, which may be adequate for drinking-water and household use but leaves very little for agriculture.

Irrigation has a vital role to play in the management of renewable freshwater resources. At present, approximately 25 percent of the arable land in the region is under irrigation, including both modern and traditional systems (Table 38). The proportion is relatively high in the Gulf Cooperation Council (GCC) countries,107 where water is most scarce and where rainfed agriculture is least feasible.

Table 38

RENEWABLE FRESHWATER RESOURCES BY COUNTRY IN THE NEAR EAST AND NORTH AFRICA, 1995 AND 2025

1995 |

2025 projection | |||

Quantity |

Dependency ratio1 |

Quantity | ||

Countries with >1 500 m3per capita |

(m3) |

(Percentage) |

Countries with >1 500 m3 per capita |

(m3) |

Iraq |

3 688 |

53.3 |

Turkey |

2 090 |

Afghanistan |

3 227 |

15.4 |

Iraq |

1 840 |

Sudan |

3 150 |

77.3 |

||

Turkey |

2 967 |

1.8 |

||

Iran, Islamic Republic |

2 044 |

6.6 |

||

Syrian Arab Republic |

1 791 |

80.3 |

||

Countries with <1 500 m3 per capita |

Countries with <1 500 m3 per capita |

|||

Lebanon |

1 465 |

0.8 |

Iran, Islamic Republic |

1 455 |

Cyprus |

1 213 |

0 |

Afghanistan |

1 448 |

Morocco |

1 110 |

0 |

Lebanon |

1 022 |

Egypt |

926 |

96.9 |

Cyprus |

1 000 |

Algeria |

512 |

2.8 |

Syrian Arab Republic |

999 |

Tunisia |

463 |

14.6 |

Morocco |

775 |

Oman |

455 |

0 |

Egypt |

610 |

Yemen |

283 |

0 |

Tunisia |

322 |

Bahrain |

206 |

96.6 |

Algeria |

307 |

Jordan |

161 |

22.7 |

Oman |

182 |

Saudi Arabia |

134 |

0 |

Bahrain |

134 |

Libyan Arab Jamahiriya |

111 |

0 |

Yemen |

105 |

Qatar |

96 |

3.8 |

Jordan |

73 |

United Arab Emirates |

79 |

0 |

Libyan Arab Jamahiriya |

70 |

Kuwait |

13 |

100.0 |

Qatar |

68 |

Saudi Arabia |

60 | |||

United Arab Emirates |

45 | |||

Kuwait |

7 | |||

1 The dependency ratio is the percentage of renewable freshwater received from sources outside the country. | ||||

Investment in irrigation continues to receive priority among the countries of the region. Egypt continues with its South Valley project as well as making greater use of drainage water for irrigation in the eastern delta and north Sinai. The upstream development of the Nile waters depends on agreement with upstream countries, and the Nile River Basin Action Plan is a promising development in this regard. Egypt also needs to pay greater attention to environmental hazards caused by drainage water. Turkey is investing heavily in irrigation through its South East Anatolia Project (GAP). With an estimated cost of $32 billion, this project involves the construction of 13 major structures, seven in the Euphrates Basin and six in the Tigris Basin. When completed, the GAP scheme is expected to irrigate 1.7 million ha by 2015. However, the downstream effect of the GAP schemes is of major concern to the Syrian Arab Republic and Iraq and no formal agreement has yet been reached on this question.

Iran is paying greater attention to improving water use at the farm level by shifting from surface to pressurized irrigation. It has also signed an agreement with Turkmenistan for the development of the Tedzhen River. Iraq completed the irrigation project known as the Third River, which is 565 km long and collects drainage water for reclaiming new land. In the Libyan Arab Jamahiriya, the Great Man-Made River Project is expected to transfer fossil water to the Mediterranean coast to irrigate 200 000 ha and meet urban water needs. In the other three Maghreb countries the emphasis continues to be placed on the construction of large and small dams and canals to expand irrigation. In Afghanistan, the rehabilitation of war-damaged irrigation facilities is the highest priority for the coming years.

Table 39

IRRIGATED ARABLE LAND IN THE NEAR EAST AND NORTH AFRICA

Country grouping |

Total arable land |

Irrigated arable land |

Irrigated land as a percentage of total |

(Thousand ha) | |||

Maghreb countries |

20 989 |

2 661 |

12.7 |

GCC countries |

3 779 |

1 777 |

47.0 |

Arab Near East |

41 392 |

10 820 |

26.1 |

Non-Arab Near East |

52 336 |

14 305 |

27.3 |

Total |

118 496 |

29 563 |

24.9 |

Source: FAOSTAT. | |||

The region's irrigation systems are under strain. In nearly all countries of the region, irrigated agriculture is adversely affected by salinity and waterlogging. It is estimated that 50 percent of irrigated land in Iraq, 37 percent in Egypt and 29 percent in Iran suffers from some degree of salinity. The siltation of dams and canals is also a common phenomenon. Another serious issue is the overexploitation of groundwater, particularly in the GCC countries as well as in Afghanistan, Iran, Jordan, Morocco and the Syrian Arab Republic.

The efficient use of water is not adequately addressed by the countries of the region, despite the fact that water is a scarce factor in agricultural production. Sustainability of the irrigation systems is also at stake: at present, water for irrigation is practically free in most of the countries, mainly because farmers cannot afford to pay water charges, even to cover the operating and maintenance costs. There are also social obstacles to charging a fee on water for irrigation and even for other uses.

Low-priced water provides little incentive for farmers to invest in water-saving technologies such as drip irrigation. Rather it encourages farmers to overuse water, thereby exacerbating the problems of waterlogging and salinity. It fails to give local communities the necessary incentives to participate in responsible water management decisions.

The high level of water scarcity in the region is best reflected in the level of purchases of what is known as "virtual water". This refers to the volume of water embedded in commodities that are imported, both food and non-food. As 1 tonne of wheat production requires approximately 1 000 m3 of water, the importation of 1 million tonnes of wheat would correspond to the purchase of 1 billion m3 of water from abroad. It is estimated that the flow of virtual water into the region equals the annual flow of the Nile River into Egypt.108 A study has shown that, in 1994, food imported into the region was equivalent to 83 billion m3 of virtual water, or 11.9 percent of the region's annual renewable water resources.109 For selected countries,the percentage was much higher: Egypt (31 percent), Algeria (87 percent), Jordan (398 percent), the Libyan Arab Jamahiriya (530 percent) and Saudi Arabia (580 percent). As food imports into the region are increasing by as much as 5 percent per year, the role of virtual water in postponing the challenge of water stress is important for the national authorities.

The capacity to buy virtual water is largely determined by export earnings, notably oil revenues, which are often unpredictable. At the same time, however, the alternative of having less reliance on this course of action is costly and probably unsustainable. The pumping and piping of fossil

and/or desalinated water over long distances for cereals and fodder production, as attempted in the Libyan Arab Jamahiriya, Saudi Arabia and the United Arab Emirates, is an exceptional occurrence and would not be sustainable over the long term.

The region is the most water-scarce region in the world and significant efforts are being made in many countries to improve the management of water resources. Although there is still room for further progress, particularly regarding irrigation efficiency, the region appears to be structurally unable to feed its increasing population and will probably need to rely more and more on virtual water, i.e. external food production.

![]()

![]()

![]()