![]()

![]()

![]()

GDP in the countries in transition in Central and Eastern Europe and the Commonwealth of Independent States (CIS) grew at 2.4 percent in 1999, following the 0.8 percent contraction in 1998. This more robust GDP growth is largely a consequence of a change from negative to positive growth in the Russian Federation from 1998 to 1999 (from -4.9 to +3.2 percent).110 The Russian Federation accounts for over 40 percent of GDP in the region. The fastest-growing economies in the region in 1999 were Turkmenistan (16 percent), Bosnia and Herzegovina (8.6 percent), Azerbaijan (7.4 percent) and Albania (7.3 percent). A further acceleration of growth is projected for 2000, as GDP growth should reach almost 5 percent, again largely because of the Russian Federation's strong performance.

Agricultural production in the region did not follow the turnaround that occurred in GDP growth in 1999. Indeed, overall agricultural output stagnated (with an estimated increase of 0.1 percent), following the contraction of 5.9 percent in 1998. The Russian Federation saw a further decline in production of 2.7 percent, as livestock production was reduced by more than 10 percent, and a 14 percent increase in crop production was insufficient to make up for the 33 percent decline recorded in 1998. Most of the other larger agricultural producers in the region saw some minor declines in agricultural output in 1999. The major exceptions were Kazakhstan and Romania, where production expanded by 29 and 18 percent, respectively, which meant that both countries more than recovered from the sharp drops experienced in 1998.

The provisional estimates for agricultural production in 2000 suggest a very small decrease of 0.7 percent. Positive performances are expected in the Russian Federation and Ukraine, where overall agricultural output appears to have expanded by 5 and 6 percent, respectively. On the other hand, production appears to have contracted to varying degrees in most other major producer countries.

Whether macroeconomic or agricultural, growth statistics covering one or two years reveal few of the growing differences that have emerged over the past decade between Central and Eastern Europe and the CIS. From a relatively common starting point in the 1980s, policies and institutions of Central and Eastern European countries and the CIS grew progressively further apart in the 1990s.111 The effects of this institutional "parting of the ways" include noticeable differences in mean GDP growth between the two subregions as well as important differences in the growth of agricultural productivity. As the region enters the second decade of economic reforms, the earliest and deepest reformers are beginning to approach the income and agricultural productivity levels of EC countries, while others face a far more substantial income and agricultural productivity gap.

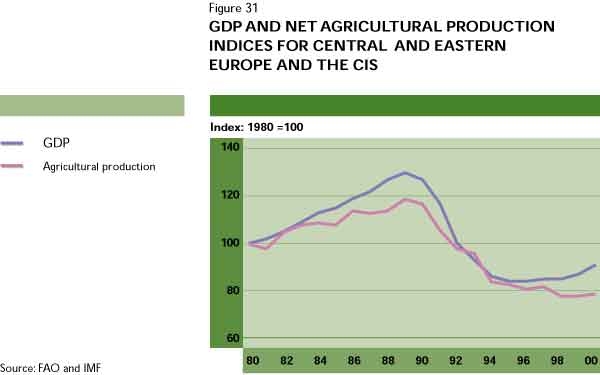

Until the end of the 1980s, allocation decisions within the economies of Central and Eastern Europe and the CIS were primarily bureaucratic rather than market-determined. Although there were many differences between the two subregions during this period, the centrally planned economy provided a common institutional background, which in many ways defines the starting point of the transition process. During the last years of central planning, the region showed moderate aggregate growth in GDP of approximately 2 to 3 percent per year (Figure 31). Growth in the value of net agricultural production generally followed GDP, although at a slower rate. Beginning in the late 1980s and early 1990s, Central and Eastern European and CIS countries experienced a general decline in output that was larger than any slowdown to be measured officially in modern peacetime history. This "transformational recession" is usually attributed to the removal of severe economic distortions that existed during the period of central planning and to the "institutional disorganization", or disruption of governance, which occurred in each of these countries as a result of the breakdown in the bureaucratic system of allocation.112

Reform policies of the 1990s were aimed at completing the dismantling of the bureaucratic-oriented economy and introducing new policies to support a market economy, both at the macroeconomic and sectoral levels. There has been a positive correlation between growth in GDP and the turnaround in agricultural production, which may point to the importance of general economic reforms for sectoral growth.

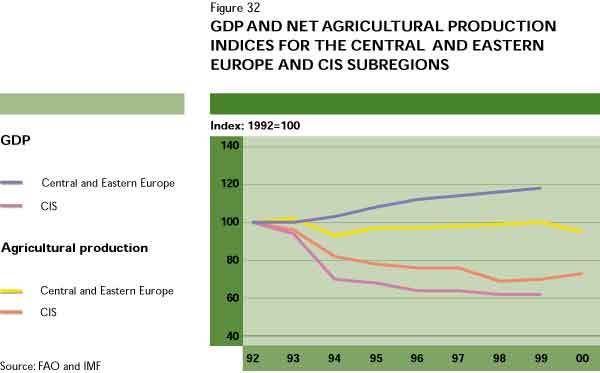

In spite of a common institutional starting point, differences between countries of Central and Eastern Europe and the CIS have been evident more or less since transition began in the

CIS in 1992 (Figure 32). The most profound gap between these two sets of countries has been in the growth of GDP, while agricultural production appears to have stagnated in both groupings.113 While the depth of the fall in GDP in these countries can be attributed to some extent to initial conditions, the differences in the speed of recovery are generally attributable to the speed and depth of reforms.

The magnitude of the initial decline in GDP in the transition countries was strongly correlated with the weight of industry in the economy and its reliance on trade within the former Council for Mutual Economic Assistance (CMEA) or with countries of the former Soviet Union before the beginning of the transition period.114 Indeed, industry had the greatest concentration of goods that became unprofitable in the new market economy, and it is on this account that countries of the former Soviet Union experienced deeper recessions than those of Central and Eastern Europe.

There were also considerable differences in the depth of general policy reforms introduced in Central and Eastern European countries and in the CIS. Most Eastern European countries introduced policy reform packages earlier, beginning in 1989-1990, while the countries of the former Soviet Union began between 1991 and 1994. In addition, reforms in Central and Eastern Europe were generally more rapid and more coherent than those in CIS countries. These factors led to a considerable divergence in GDP growth between the two regions during the recovery phase. The transition countries that implemented overall economic reforms most rapidly and thoroughly - such as Poland, Hungary, Slovenia, the Czech and Slovak Republics and Albania (i.e. the "advanced reformers") - performed much better than intermediate and slow reformers such as Belarus, the Russian Federation and Ukraine.115 The fall in GDP in the Central and Eastern European countries that implemented rapid and thorough reforms was short-lived and slight, whereas the fall in the slowly reforming CIS countries was far longer and deeper.116

While there seems to be a strong correlation between overall economic reforms and GDP growth, at the sectoral level there does not appear to be a similarly clear correlation between reforms of the agriculture sector and growth in agricultural production. Part of the explanation for this may be the role played by initial conditions in determining growth of agricultural production. In fact, before the 1990s in Slovenia, where agriculture was largely privately owned, and in Hungary, where much agricultural production was performed by reformed cooperatives, agricultural institutions differed strikingly from the more orthodox production and procurement systems of large state and collective farms in the former Soviet Union. Indeed, changes in agricultural output and labour productivity were strongly correlated with initial levels of "development" and "economic distortions" in countries of Central and Eastern Europe and the CIS.117 Another reason for the lack of correlation between the sectoral reforms and growth in agricultural production could be the more important influence of overall macroeconomic reforms and stabilization on agricultural performance.

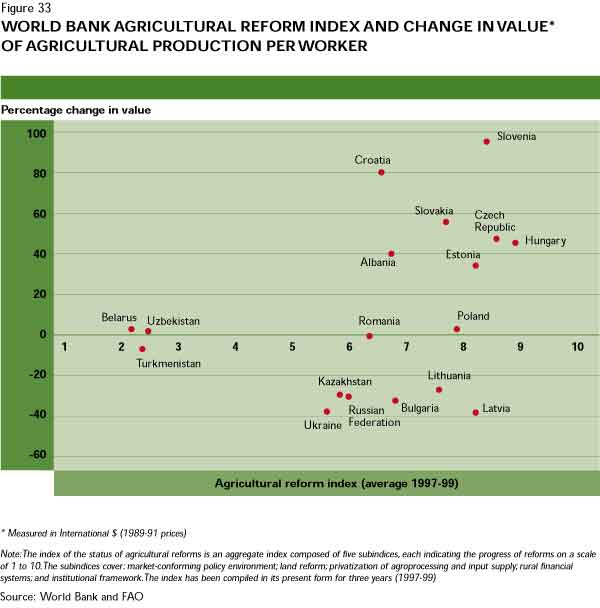

The depth and coherence of agricultural policy changes appear to have had a much more significant impact on the technical efficiency of agricultural production than on levels of agricultural production in Central and Eastern Europe and the CIS. This is illustrated in Figure 33, where the percentage change in the value of net production per agricultural worker between 1992 and 1998 is juxtaposed against an aggregate indicator of the status of agricultural reform compiled by the World Bank.118

Although caution is needed in drawing conclusions, the data in Figure 33 nevertheless seem to distinguish three groups of countries based on the agricultural reform index. The first group (Belarus, Turkmenistan and Uzbekistan) is that of non-reformers. These countries have retained their former agricultural institutions and have thus delayed the transition recession and resulting pressure to reduce the agricultural labour force. The moderate reformers (Bulgaria, Kazakhstan, the Russian Federation and Ukraine) have partially reformed their agriculture sectors, although their institutions tend to be a mixture of old and new. They have sustained sizeable production falls and their agricultural labour forces have often grown, rather than diminished. For these reasons, they have seen the value of production per worker decline. The fast reformers (the countries situated in the top right-hand part of Figure 33) have suffered the initial transition recession, as have the moderate reformers, but have moved rapidly to replace old agricultural production structures with new market economy institutions and have reformulated government policies. The new market-oriented producers have responded to recession by reducing the labour force engaged in agricultural production, and their production falls have been more moderate.

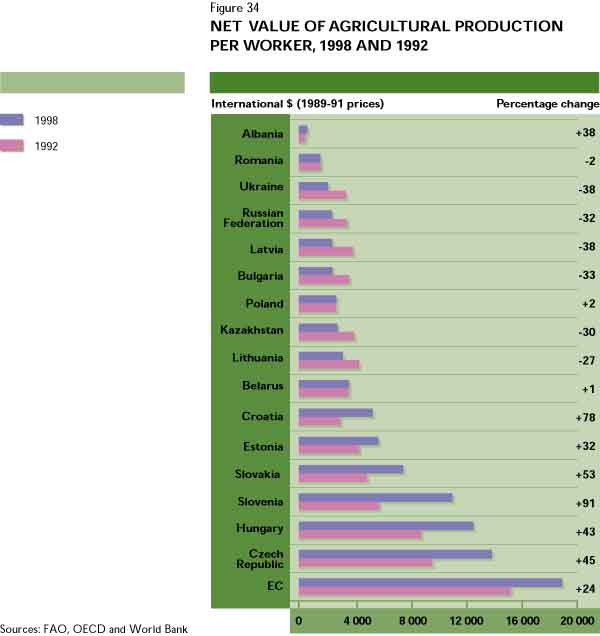

There is still a sizeable labour "productivity gap" between most countries in Central and Eastern Europe/CIS and those in the OECD, although in the most advanced reformers of Central and Eastern Europe, this gap is diminishing quickly (see Figure 34). The level of agricultural labour productivity in Central and Eastern European and CIS countries was between 3 and 73 percent of that of EC countries in 1998.119 Only three countries among those listed show labour productivity of more than 50 percent of that of the EC (the Czech Republic, Hungary and Slovenia), and productivity for Central and Eastern Europe as a whole was only 15 percent of the EC's level. For the largest CIS countries (the Russian Federation, Ukraine, Kazakhstan and Belarus), labour productivity was only 13 percent of the EC's level.

A more important indicator of the effectiveness of reforms is the change in agricultural labour productivity from 1992 to 1998. For this indicator, there are profound differences between the majority of Central and Eastern European countries and the CIS. Indeed, the growth in agricultural labour productivity from 1992 to 1998 was considerably more rapid in most of the Central and Eastern European countries than in the EC (the exceptions being Bulgaria, Latvia, Lithuania, Poland and Romania). The most impressive record is that of Slovenia, which nearly doubled its labour productivity in six years. The record of the Central and Eastern European countries is considerably poorer. In aggregate, labour productivity in these countries fell by 31 percent in the 1992-1998 period, and only Belarus recorded a positive labour productivity growth of 1 percent.

Table 40

AGRICULTURAL EMPLOYMENT IN 1998

Agricultural employment | |||||

(1) |

(2) |

(1) |

(2) | ||

As a percentage of total employment |

As a percentage of agricultural employment |

As a percentage of total employment in 1990 |

As a percentage of agricultural employment in 1990 | ||

Central and Eastern |

OECD |

||||

Albania |

64.0 |

121.8 |

Australia |

4.8 |

- |

Belarus |

15.9 |

83.1 |

Canada |

5.0 |

- |

Bulgaria |

24.7 |

130.7 |

Japan |

5.3 |

- |

Croatia |

9.9 |

61.4 |

New Zealand |

8.5 |

- |

Czech Republic |

4.2 |

45.9 |

Republic of Korea |

12.2 |

- |

Estonia |

6.8 |

53.3 |

Switzerland |

4.7 |

- |

Hungary |

7.7 |

43.8 |

United States |

2.7 |

- |

Kazakhstan |

15.8 |

68.1 |

OECD average |

7.9 |

- |

Latvia |

15.7 |

91.2 |

EC |

4.8 |

- |

Lithuania |

20.0 |

111.8 |

|||

Poland |

25.1 |

100.4 |

|||

Romania |

35.6 |

125.1 |

|||

Russian Federation |

13.7 |

107.2 |

|||

Slovakia |

8.2 |

73.8 |

|||

Slovenia |

5.6 |

99.6 |

|||

Ukraine |

22.1 |

109.8 |

|||

Sources: OECD 20/20 Database for Central and Eastern European and CIS countries, and OECD. 2000. Agricultural Policies in OECD Countries: Monitoring and Evaluation 2000 (for percentage of labour force in agriculture). OECD 20/20 Database for Central and Eastern European and CIS countries (for agricultural labour force in 1998 as percentage of 1990). | |||||

The agricultural labour productivity gap between Central and Eastern Europe/CIS and the OECD countries is largely explained by the relatively large labour force employed in agriculture in the former. Column 1 of Table 40 illustrates the differences in the share of the labour force employed in agriculture in Central and Eastern Europe/CIS and OECD countries. Some transition countries saw dramatic reductions in the agricultural labour force as a result of land reform and farm privatization, but most did not. Column 2 of Table 40 shows that Hungary, Estonia and the Czech Republic were the most successful in reducing their agricultural labour force. It is not accidental that agricultural labour productivity in these countries grew exceptionally quickly in these years.

A second reason for the productivity gap is the inability of many Central and Eastern European and CIS producers to produce for export in significant quantities. This situation is due to a number of factors, which vary from country to country. For example, in Ukraine, where most tradable agricultural commodities are produced in large, collectively managed farms, low prices (resulting from government barriers to trade), high costs of production and transport, high risk as well as significant governance and financial difficulties combine to limit producers' competitiveness in production and exports. In Romania, tradable commodities are produced on inefficient, small plots, limiting capacity for the production of significant market surpluses.

The labour "productivity gap" is of particular significance for Central and Eastern Europe because of the large weight of the agriculture sector in its economies in comparison with most OECD countries. Consequently, productivity improvements would have a far greater impact on GDP and income. For instance, 4.8 percent of GDP in Poland (1998 data) is derived from agriculture, whereas this figure is only 2 percent in the EC.120 The discrepancy is even greater for the countries of the Caucasus, Central Asia and the Balkans; for example, 54.4 percent of Albania's GDP (1998) derives from agriculture.

The productivity gap also means that agricultural producers of Central and Eastern Europe and the CIS are performing at a level that is far below the region's technological potential. With productivity improvements, the region could decrease net food imports and eventually contribute to meeting the world's growing food demand in the longer term. Narrowing this gap is critical for the countries of the region to be able to compete with the producers of OECD countries, increase export earnings and raise rural incomes. It is clear that the countries that have been most successful in bridging the productivity gap are those that have implemented the deepest and most stable reforms.

![]()

![]()

![]()