![]()

![]()

![]()

Vijay Paul Sharma[32]

Raj Vir Singh[33]

Steve Staal[34]

Christopher L. Delgado[35]

June 2002

This paper was produced as part of Phase I of an IFPRI-FAO project entitled "Livestock Industrialization, Trade and Social-Health-Environment Impacts in Developing Countries", funded by the Department for International Development (DFID), U.K., through the Livestock, Environment and Development (LEAD) initiative at FAO. Correspondence may be addressed to the scientific coordinator for the project, Dr. Christopher Delgado, IFPRI, 2033 K St, N.W., Washington D.C. 20006, USA. Email: [email protected]

Milk production is the most important agricultural activity in the Indian agricultural sector. At the national level, around 17% of the total value of agricultural production is derived from this sector. Its importance is further highlighted if the closely linked other livestock (meat, poultry, wool and hair, etc.) sub-sectors (accounting for a further 8.3%) are also taken into consideration. The milk sector generates a high proportion of agricultural output, especially in the northern and western parts of the country.

Milk production in the country was stagnant during the 1950s and 1960s and per capita availability declined. However, with the implementation of the Operation Flood (OF) Program in 1970 and other dairy development programs implemented by the State and Central governments, increased demand driven by increased population, higher incomes and urbanization, and with tight controls on imports of dairy products, milk output increased substantially in the country. This evolution was accompanied by an even more marked improvement in milk yields. India has emerged today as the largest milk producer in the world, surpassing 80 million tones, and this success story of Indian milk production has been written primarily by millions of smallholder producers. The OF program was instrumental in creating strong linkages among millions of smallholder producers and urban consumers. Prior to OF, the link between the producer and consumer was completely missing. It is well known that all this happened under highly regulated domestic markets, where commercial imports and exports of almost all dairy products had been banned for most of the time, and processing activity had been controlled through licensing which favored cooperatives over private entrepreneurs. However, termination of licensing requirements for setting up milk processing and product manufacturing under the MMPO in 2002 made India's dairy industry arguably one of the most deregulated industries in the world. The unmanaged deregulation of the dairy industry combined with a rapid increase in demand (domestic as well as global) for milk and dairy products, and distortions in the world dairy markets, it is widely believed, would lead to economic and social problems. These developments (domestic and international) would influence the scale of operation in dairy sector and may lead to social-health-environmental problems. Milk production certainly would become concentrated on large farms and in peri-urban or urban areas as a result of deregulation, which could have major implications for smallholder dairy producers and larger goals of employment-led economic growth, poverty alleviation, and environmental sustainability.

Like nearly all developing countries, India exhibits co-existing "organized" and "unorganized/informal" sectors for marketing of milk and dairy products. The organized or formal sector is relatively new in historical terms, and consists of Western-style dairy processing based on pasteurization, although adapted to the Indian market in terms of products. In some cases the traditional sector is quite well organized, with a complex net of market agents, with a variation in numbers of and roles of market intermediaries. The reasons underlying the existence of a large informal or traditional sector are the same as found in other countries: consumers are unwilling to pay the additional costs of pasteurization and packaging, and consumers often regard raw milk and traditional products obtained from reliable vendors as of better quality than formally processed dairy products. The dairy cooperatives comprise the single largest formal organization in terms of market share, and its share in total milk procurement has increased over a period of time and is further expected to rise in the future. However, the informal sector may still play an important role in the Indian dairy sector. The repeal of industrial licensing under new economic policy provided the opportunity for private entrepreneurs and multinational companies to invest in new processing capacities, which may lead to some structural changes in the production sector whereby the private entrepreneurs would try to reduce transaction costs and may promote large commercial dairy farms.

Commercial imports of dairy products were substantial until the early 1970s, but declined significantly in the 1980s and 1990s. However, the imports of milk powders and butter/butter oil increased substantially in the late 1990s, mainly due to low import duties on these two products as a commitment under the WTO Agreement. India has also started exporting small quantities of dairy products during the last decade, but its exports are still in their infancy. However, India has the potential to become one of the leading players in milk and milk product exports, because India is located amidst major milk deficit countries in Asia and Africa; also, the cost of milk production in India is one of the lowest due to cheap labor and traditional feeding systems. Despite these positive factors, there is a long way to go in order to improve the quality of Indian milk and milk products. In order to become globally competitive, significant investment has to be made in the supply chain of milk procurement, processing, and marketing. Also, training has to be given to the farmers and processors to improve the quality of milk and dairy products to bring them up to international standards. Animal welfare, which includes establishing norms for animal protection on the farm, during transport, and at the time of slaughter, is not currently covered under the WTO, but these issues are coming under increasing public scrutiny. Therefore, attention should be given by national authorities to reducing negative effects of commercialization of livestock farming and trade on the welfare of the animals.

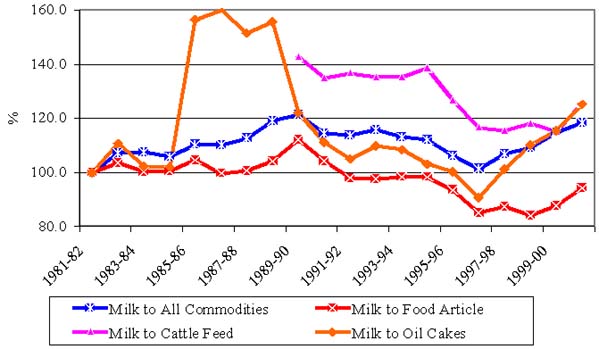

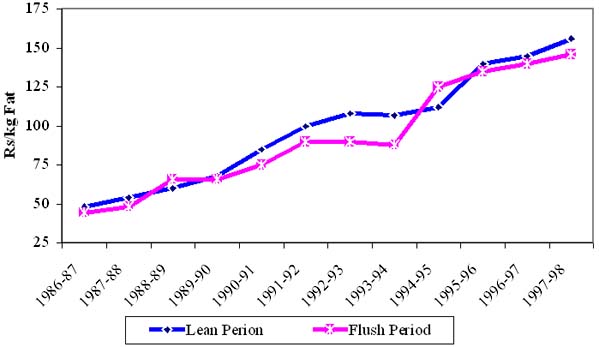

Seasonality in milk production is well known in the Indian dairy sector and is more pronounced for buffaloes. Such fluctuations in supply and demand result in fluctuations in prices (producer and consumer), thus subjecting milk producers and consumers to large variations in prices during a year. The procurement prices are marginally higher during the lean season compared with the flush period. The WPI of milk relative to the WPI of food articles and all commodities decreased during 1990s, which indicates increased production of milk and/or imports of dairy products in the post-reforms era. Milk prices relative to milk input prices such as oil cakes, fodder, and cattle feed show that input prices have increased faster than milk prices in the 1990s. These trends in input prices indicate that increased milk production should come from productivity enhancement; otherwise, increases in costs will make milk and dairy products costly and unaffordable to the masses.

Of all the agricultural products, dairy product prices are the most distorted by domestic and export subsidies in developed countries, especially the European Union and the USA. World dairy product prices were expected to increase as a result of lowered market intervention in the forms of lower export subsidies and support prices and less public stocks in the post-WTO period. Stronger demand for dairy products was expected from a rise in consumer income, as economic growth becomes more broad-based in developing countries; and the gaps between EU and world dairy product prices were expected to shrink. However, world dairy prices witnessed a declining trend in the post-WTO period due to high WTO-compatible export subsidies, large support prices, and other protections. The fall in world prices had an adverse impact on domestic prices in many developing countries, including India.

Diseases, along with the non-availability of feed resources and nutrition, are the most important constraints to milk production. However, with smallholder production systems, the situation is more serious because of inadequate knowledge and access to appropriate corrective measures and resources. In India, the government, cooperatives, the private sector, and a few non-governmental organizations (NGOs) provide veterinary services and artificial insemination facilities to the dairy farmers. However, it is well known that the quality of the veterinary services provided by public sector institutions is poor, and that institutions providing these services are highly inefficient. Therefore, there is a need to restructure and reorient the livestock health and breeding services and extension services providing institutions to make the Indian dairy sector globally competitive.

In the light of the fast-changing global trade regime, the outlook for technological development in the Indian dairy sector appears to be bright. In order to tap the global dairy market to India's advantage, more scientific management of dairy animals in terms of breeding, feeding, health care, and management needs to take place. More concentrated milk production and milk sheds may develop. Efforts for clean milk production and animal health and welfare issues will occupy special significance. The Indian dairy industry will focus on value creation through an integrated approach to the market and the development of a range of value-added products and production and processing methods. The strategic objectives will be to provide a range of products that enhance health and well-being; new product innovations that respond to changes in food habits, lifestyle, and design; sustainable dairy production systems (socially, economically, and environmentally); food safety and quality; market access; and improved animal health and welfare, with a focus on vertical integration of the value chain.

The increase in demand for dairy products will put increasing pressure on dairy production systems. Traditional breeds and feeding practices are likely to give way to high-yielding breeds, intensification of production systems, increased disease risks, pollution and animal health issues, and a greater reliance on feeds and concentrates. Currently, Indian dairy farming is dependent on crop residues, natural resources, and open grazing as sources of feed; however, expansion of these traditional sources of feeds and fodder to support a large increase in dairy production is unlikely as available grazing areas and other common property resources (CPRs) are shrinking and are already degraded. Therefore, if milk production is to increase, then additional output will have to come from modern systems that are based on stall-feeding and that use more concentrates.

Rising human needs for milk and other livestock products have placed the environment in conflict with livestock. The rapidly increasing demand for dairy products in urban areas has given rise to haphazard growth of production centers in peri-urban and urban areas that are essentially detached from their supporting land base, and often generate a large amount of waste that contaminates the soil and groundwater. Foul odors usually emanate from animal wastes if not treated or disposed of properly, leading to air pollution. Livestock product processing plants release large amounts of waste into the environment, polluting land and surface waters as well as posing a serious human health risk. Because of weak infrastructure such as rural roads and communication, processing plants operate in urban areas where discharge of waste material is uncontrollable. Pollution of the food chain is also a major issue, and pesticides, nutrients, feed additives, hormones, and veterinary drugs used in excessive quantities can contaminate the food chain.

As discussed in the main report, the study is based on numerous official documents, newspaper and journal articles, and several interviews that were conducted with various stakeholders in the Indian dairy sector. The interviews were conducted on a 'not for attribution' basis to encourage candour, and therefore individual comments are not attributed by name. The goal of this section is by no means to provide an evaluation of livestock industrialization and its implications for social-health-environment issues, and indeed, this method does not lend itself to such a policy exercise. Instead, we hope to shed light on circumstances, actors, and forces that guided reforms in this sector in a particular direction, and by so doing, improve understanding how international and domestic forces influence the scale of operations in milk production, processing, and marketing in India and how these changes influence the attainment of social-health-environment (SHE) objectives. The study has identified some of the key policy/structural issues that need to be investigated both at the macro- and the micro-level (based on farm data) to find out answers to some of the issues raised in this report.

Dairying is an important part of the Indian agricultural economy. At the national level, about 17% of the total value of output from agriculture derives from this sector, placing Indian milk sector in first place followed by rice (14.4%) and wheat (8.7%) in 1998-99 (CSO, 2001). From chronic shortages, India has now become the largest producer of milk in the world, with estimated production of about 81 million tons in 2001. This success story of Indian milk production has been written primarily by millions of rural producers, and the major share of credit goes to women dairy farmers. In India, dairying is dominated by smallholder production systems; almost 70% of the milk producers in India are landless small and marginal farmers who own one or two animals. It is well known that the Indian dairy sector has developed in a highly regulated and protectionist economy. However, India initiated major macro-economic reforms in the early 1990s that encourage the liberalization of all sectors of the economy, and the dairy sector was no exception. This was reinforced with the signing of the Uruguay Round Agreement on Agriculture (URAA) in 1994. This increasingly exposed the Indian dairy sector to world dairy markets that have been highly distorted by policies of high tariffs, domestic support, and export subsidies in developed countries. There is likely to be restructuring of the dairy sector around the world, and it would be interesting to examine the likely implications of these changes for the Indian dairy sector under the new economic environment of trade liberalization and globalization.

This paper analyzes the changes in dairy markets, policies, and trade over the past two decades and discusses what can be expected in the next decade. We analyze the changes in production, consumption and trade, as well as the changes in policies and the industry structure, and discuss how various factors have affected the market and trade situation. The paper is organized as follows: we first discuss the macro-view of the Indian dairy sector. Then we discuss policy changes and the expected effects of globalization and trade liberalization on the scale and scope of production. In the next section we discuss the changes in the cost and return structure of dairy production and the processing sector, trends in input and output prices, and breeding and health services. In the last section we discuss the impacts of commercialization of the dairy sector on socioeconomic-health-environment issues.

Dairy enterprise is considered a "treasure" of the Indian economy, particularly for rural systems. It provides nutrition, draft animal power, organic manure, supplementary employment, cash income, and a 'cushion' for 'drought proofing' in India (Patel, 1993; Paroda, 1998). The sector involves millions of resource-poor farmers, for whom animal ownership ensures critical livelihood, sustainable farming, and economic stability. Dairying in the recent decades has been considered a vital component in the diversification of Indian agriculture, where crop farming is beset with stagnating growth and low absorption of unskilled agricultural laborers. In order to alleviate the problem of unemployment/under-employment and to maintain domestic tranquility, diversification of crop production into non-crop enterprises like dairy farming is of vital importance (Pandey, 2000; Alagh, 2002).

At the macro-level, the gross domestic product (GDP) from livestock is estimated about Rs. 98,421 crore (current prices), contributing about 22% to the agricultural gross domestic product (GDP) and about 5.5% to the national GDP (CSO, 2001). Among various livestock products, milk constitutes the major share (67%) in value of outputs from the livestock sector (Figure 1.1) and is the single largest commodity contributing to the value of output from agriculture.

During the last several decades, the contribution of agriculture and allied sectors to the national GDP has declined. Agriculture, which used to account for about 55% of the GDP in 1951-52, now accounts for around 25% of the GDP (GOI, 2002). However, the livestock sector in general and the dairy sector in particular have been among the few growth sectors in India. Its contribution to national GDP has increased from 4.8% in 1980-81 to about 5.5% in 1999-2000 (Table 1.1). The share of livestock in agricultural GDP has also increased from about 14% in 1980-81 to about 22% in 1999-00. In developing countries like India, official statistics often underestimate the overall contribution of livestock, for obvious reasons.

Table 1.1 Share of agriculture and livestock in the Gross Domestic Product of India (at current prices)

|

Year |

GDP (Agriculture) |

GDP (Livestock sector) |

Share of Livestock sector in Agricultural GDP (%) |

||

|

Rs. crore |

% share |

Rs. crore |

% share |

||

|

1980-81 |

42,466 |

33.41 |

5,913 |

4.83 |

13.92 |

|

1995-96 |

277,846 |

26.0 |

64,961 |

6.09 |

23.38 |

|

1996-97 |

334,029 |

27.0 |

74,700 |

6.04 |

22.36 |

|

1997-98 |

352,753 |

25.5 |

84,072 |

6.07 |

23.83 |

|

1998-99 |

428,680 |

26.6 |

96,905 |

6.01 |

22.61 |

|

1999-00 |

443,923 |

24.8 |

98,421 |

5.51 |

22.17 |

Source: CSO (2001)

The livestock sector alone provides regular employment to 18.4 million people in principal/subsidiary status, constituting about 5% of the total workforce (GOI, 2002). Dairying at the micro-level provides employment and income to more than 70 million farm families directly in India. Studies conducted across the country have indicated that on average, a milch animal provides annual employment ranging from 90 to 150 days depending on the breed and region. Around 10% of agricultural laborers seek gainful employment in dairy farming. It is estimated that each 6-10 kg per day of additional milk processed in India generate one person-day of employment for feeding and health care (National Livestock Policy, 1996; Mishra, 1999). With regard to income, an annual income of Rs. 1,200-10,000 per milch animal is realized, depending on breed and region. Dairying is found to provide about 20% of farm employment and about 30% of family income (Ramasamy, 2000).

Indian dairy farming is basically a smallholder production system, characterized by milk production by the masses rather than mass production of milk. More than 80 million households (about 73% of rural households) keep some type of livestock. The base for Indian dairying is provided by millions of landless agricultural laborers and marginal and small farmers who maintain one or two milch animals of low genetic potential for milk production, primarily fed on crop residues and byproducts, and reared with the help of under-employed family members, mostly female workers. Although dairying is becoming more commercialized in some areas, it predominantly remains subsistence farming constituting a complementary/supplementary enterprise to crop farming, with regular sales of surplus production.

Dairy farmers in India are by and large illiterate, resource-poor, and low risk-bearers. They often exhibit a low level of farming innovation; in the majority of cases, they are either non-adapters or late adopters of modern technologies. Their average family size is moderate, around 5 persons. The marketable surplus of milk is about 60% of total milk production.

On marginal farms, it was estimated that the introduction of dairy enterprise increases the average farm income from Rs. 12,801 to Rs. 18,163 showing an increase of 42% per annum. On small farms, a similar trend was observed, with average farm increasing from Rs. 33,301 to Rs. 70,664 (an increase of 112%) resulting from the introduction of dairy (Kalra, et al., 2000). A similar trend was observed in other situations. In a well-planned project on integrated milk and crop production for increased productivity, employment, and farm income in the villages around Karnal, conducted by the National Dairy Research Institute from 1995 onward in 40 villages around Karnal, it was observed that labor absorption of different groups of households due to dairy farming increased differently, with an average increase of 21% in the project area (225 man-equivalent days) over the control area (187 man-equivalent days) (Table 1.2). Not only did dairy enterprise increase income and employment, but it also increased female labor utilization in different groups of rural households. On average, female labor utilization in dairy enterprise was 81 man-equivalent days, or 33% of the total labor employment of 242 man-equivalent days in dairy farming. The share of female labor utilization varied in different groups, being maximum in landless laborers (46%) followed by medium farms (32%) (Singh, et al. 1995). Within dairy operations, 47% of labor is utilized for bringing fodder, 12% for grazing, 10% for chaffing, 15% for feeding, 7% for cleaning, and 10% for milking (Singh and Kairon, 1996).

Table 1.2 Employment in dairy farming systems

(MED/Household/Annum)

|

Category of households |

Control area |

Project area |

Percentage change |

|

Landless |

120.45 |

172.01 |

42.81 |

|

Marginal |

144.63 |

177.48 |

22.71 |

|

Small |

196.19 |

204.86 |

4.42 |

|

Medium |

242.73 |

313.90 |

29.32 |

|

Large |

436.63 |

448.49 |

2.72 |

MED: man-equivalent days

Source: Singh C.B., D.S. Sohi and J.P. Dhaka (1995)

Owing to their poor financial condition and poor networks of organized financial institutions, farmers more often than not approach private money lenders for credit and enter into some sort of marketing contracts for selling milk, normally to the disadvantage of farmers. On the other hand, regular milk vendors (dudhias) often provide credit at reasonable terms, an important source of financing to small farmers. Village-level extension workers (Gram sevaks), elite farmers of the village, and peer groups are the normal sources of information and modern technology for dairy farmers in the country. Kisan/Dairy melas also serve as sources of information to the farmers in selected areas.

India owns one of the largest livestock populations in the world. It accounts for about 57% of the world's buffalo population and 16% of the cattle population (GOI, 2002). Between 1951 and 1992, the period for which data are available from the Livestock Census, the stock of cattle and buffaloes together increased from 198.7 million to 289 million (45.4%). Cattle population grew by about 0.76% per year between 1951 and 1992, while buffalo population almost doubled (2.24% per year) during the same period (Table 1.3). This trend was uniform during all the inter-census years of this period, and both cattle (1.35%/year) and buffalo stocks (2.39%/year) witnessed a significant acceleration in growth from 1977 to 1982, compared to the previous five years. Between 1956 and 1961, the rate of increase of cattle (2.04%/year) as well as of buffaloes (2.66%/year) was the highest among all the sub-periods considered. This period also saw increases in agricultural production by increasing crop areas, which in turn required greater animal draft power. Secondly, the farmers saw incentives for increased milk production in the form of rising milk prices. The turning point in the bovine working male population was 1977. The male cattle population declined by over 12 million from 73.22 million to 61.14 million between 1977 and 1982, and the corresponding decline among male buffalo population was over 1.96 million (GOI, 1999). This declining trend, however, is not uniform across the states. Agriculturally progressive states like Punjab, Haryana, Andhra Pradesh, Kerala, Tamil Nadu witnessed a sharp decline in working male numbers due to farm mechanization, while the less progressive states like Assam, Bihar, Madhya Pradesh, Orissa, West Bengal exhibited increasing dependence on work animals.

Table 1.3 Growth pattern of livestock population in India: 1951-1992

(Million)

|

Species |

1951 |

1956 |

1961 |

1966 |

1972 |

1977 |

1982 |

1987 |

1992 |

|

Cattle |

155.3 |

158.7 |

175.6 |

176.2 |

178.3 |

180.0 |

192.45 |

199.69 |

204.58 |

|

Adult female cattle |

54.4 |

47.3 |

51.0 |

51.8 |

53.4 |

54.6 |

59.21 |

62.07 |

64.36 |

|

Buffalo |

43.4 |

44.9 |

51.2 |

53.0 |

57.4 |

62.0 |

69.78 |

75.97 |

84.21 |

|

Adult female buffalo |

21.0 |

21.7 |

24.3 |

25.4 |

28.6 |

31.3 |

32.5 |

39.13 |

43.81 |

|

Total bovines |

198.7 |

203.6 |

226.8 |

229.2 |

235.7 |

242.0 |

262.36 |

257.82 |

289.0 |

|

Total livestock |

292.8 |

306.6 |

335.4 |

344.1 |

353.4 |

369.0 |

419.59 |

445.28 |

470.86 |

|

Annual growth rates (%) |

1951-56 |

1956-61 |

1961-66 |

1966-72 |

1972-77 |

1977-82 |

1982-87 |

1987-92 |

|

|

Cattle |

0.43 |

2.04 |

0.07 |

0.24 |

0.19 |

1.35 |

0.74 |

0.48 |

|

|

Adult female cattle |

-2.76 |

1.52 |

0.31 |

0.61 |

0.45 |

1.63 |

0.95 |

0.73 |

|

|

Buffalo |

0.68 |

2.66 |

0.69 |

1.61 |

1.55 |

2.39 |

1.71 |

2.08 |

|

|

Adult female buffalo |

0.66 |

2.29 |

0.89 |

2.40 |

1.82 |

0.76 |

3.78 |

2.28 |

|

|

Total bovines |

0.49 |

2.18 |

0.21 |

0.56 |

0.53 |

1.63 |

1.01 |

0.94 |

|

|

Total livestock |

0.93 |

1.81 |

0.51 |

0.53 |

0.87 |

2.60 |

1.20 |

1.12 |

|

Source: Basic Animal Husbandry Statistics 1999, Department of Animal Husbandry and Dairying, Ministry of Agriculture, Government of India

Within the cattle stock, the share of crossbred cattle increased from 5.7% in 1987 to about 7.5% in 1992 (Table 1.4). After an initial slow start during the 1960s, crossbreeding picked up very fast, and the successive rounds of livestock census clearly established the speed with which crossbreeding spread in different parts of the country. In 1992, crossbred cattle constituted about 4.5% of total cattle and about 9.5% of total cows in the country. In states like Punjab and Kerala, the proportion of crossbred cows is substantially higher compared to other states. The density of total and female cattle and buffalo population per hundred hectares for selected states is presented in Tables 1.5 and 1.6. The density of crossbred cows increased from 2.7 in 1982 to 5.7 in 1992 while in case of indigenous cows it declined from 52.8 in 1987 to 49.8 in 1992, which shows the increasing importance of crossbred cows over indigenous cows. The density of female buffaloes also increased significantly from 30.2 to 36 between 1982 and 1992.

Table 1.4 Share of crossbred cattle in total cattle, and share of crossbred milch cows in total milch cows in major states: 1987-1992

|

State |

Share of crossbred cattle in total cattle |

Share of crossbred breedable cattle in total cattle |

Annual growth rate (%) |

|||

|

1987 |

1992 |

1987 |

1992 |

Crossbred cows |

Indigenous cows |

|

|

Andhra Pradesh |

3.15 |

4.42 |

4.83 |

8.36 |

8.71 |

-3.56 |

|

Bihar |

0.83 |

0.86 |

1.21 |

1.21 |

1.05 |

1.22 |

|

Gujarat |

4.46 |

6.12 |

4.66 |

5.96 |

8.63 |

3.35 |

|

Haryana |

11.01 |

19.52 |

12.72 |

22.73 |

12.67 |

-1.97 |

|

Himachal Pradesh |

7.13 |

12.98 |

8.95 |

16.97 |

16.79 |

-1.22 |

|

Karnataka |

7.07 |

4.75 |

10.60 |

7.14 |

-6.29 |

3.29 |

|

Kerala |

49.91 |

49.91 |

52.30 |

52.28 |

0.68 |

0.70 |

|

Madhya Pradesh |

0.38 |

0.73 |

0.52 |

1.03 |

15.14 |

-0.18 |

|

Maharashtra |

NA |

10.16 |

NA |

15.54 |

NA |

-2.97 |

|

Orissa |

4.13 |

4.33 |

5.80 |

6.20 |

1.31 |

0.06 |

|

Punjab |

55.80 |

55.96 |

62.08 |

61.86 |

0.47 |

0.58 |

|

Rajasthan |

0.67 |

1.03 |

0.72 |

0.99 |

8.71 |

1.06 |

|

Tamil Nadu |

12.21 |

19.82 |

15.25 |

24.35 |

10.91 |

-1.29 |

|

Uttar Pradesh |

9.83 |

9.74 |

8.93 |

9.33 |

1.32 |

0.55 |

|

West Bengal |

3.51 |

5.50 |

4.93 |

7.56 |

7.70 |

-2.97 |

|

All India |

6.33 |

8.40 |

7.44 |

10.16 |

7.09 |

0.01 |

Source: Basic Animal Husbandry Statistics 1999, Department of Animal Husbandry and Dairying, Ministry of Agriculture, Government of India

Table 1.5 Density of cattle and buffalo population in selected states of India

(numbers/1000 hectares)

|

States |

Cattle |

Buffaloes |

Total Bovine |

||||||

|

1982 |

1987 |

1992 |

1982 |

1987 |

1992 |

1982 |

1987 |

1992 |

|

|

Andhra Pradesh |

101.3 |

101.8 |

85.8 |

66.7 |

72.1 |

71.7 |

168.0 |

173.9 |

157.6 |

|

Bihar |

152.1 |

201.8 |

236.8 |

43.7 |

47.2 |

57.2 |

195.8 |

249.0 |

294.0 |

|

Gujarat |

64.1 |

60.1 |

61.8 |

31.4 |

43.4 |

47.9 |

95.5 |

103.4 |

109.7 |

|

Haryana |

40.2 |

46.9 |

36.5 |

57.8 |

81.7 |

74.7 |

98.0 |

128.6 |

111.2 |

|

Himachal Pradesh |

229.1 |

230.2 |

222.5 |

64.9 |

81.4 |

72.0 |

294.0 |

311.6 |

294.6 |

|

Jammu & Kashmir |

237.7 |

265.1 |

284.5 |

57.6 |

54.2 |

67.9 |

295.3 |

319.3 |

352.3 |

|

Karnataka |

100.6 |

83.4 |

106.1 |

32.5 |

33.0 |

34.3 |

133.1 |

116.3 |

140.4 |

|

Kerala |

106.6 |

117.5 |

115.7 |

14.1 |

11.3 |

9.7 |

120.7 |

128.8 |

125.4 |

|

Madhya Pradesh |

124.6 |

125.8 |

120.5 |

25.0 |

28.0 |

33.5 |

149.6 |

153.8 |

154.0 |

|

Maharashtra |

79.3 |

81.9 |

83.0 |

19.5 |

22.9 |

25.9 |

98.8 |

104.8 |

108.9 |

|

Orissa |

147.9 |

150.0 |

147.0 |

15.2 |

16.6 |

16.3 |

163.1 |

166.5 |

163.3 |

|

Punjab |

NA |

38.6 |

38.5 |

66.0 |

76.1 |

79.6 |

NA |

114.7 |

118.1 |

|

Rajasthan |

72.6 |

82.1 |

58.0 |

32.5 |

47.6 |

38.2 |

105.1 |

129.7 |

96.2 |

|

Tamil Nadu |

150.0 |

138.9 |

131.3 |

46.5 |

46.5 |

39.8 |

196.5 |

185.4 |

171.1 |

|

Uttar Pradesh |

105.6 |

107.7 |

99.8 |

63.7 |

74.7 |

78.2 |

169.3 |

182.4 |

178.0 |

|

West Bengal |

211.5 |

242.4 |

200.2 |

13.3 |

13.9 |

11.9 |

224.9 |

256.3 |

212.0 |

|

All India |

108.7 |

115.5 |

110.3 |

39.4 |

43.9 |

45.4 |

148.1 |

159.5 |

155.7 |

NA: data not available

Source: Livestock Census (various issues)

Table 1.6 Density of female cattle and buffalo population in selected states of India

(number/1000 hectares)

|

States |

Crossbred Cattle |

Indigenous Cattle |

Buffaloes |

||||||

|

1982 |

1987 |

1992 |

1982 |

1987 |

1992 |

1982 |

1987 |

1992 |

|

|

Andhra Pradesh |

0.9 |

2.1 |

2.9 |

49.0 |

44.1 |

34.1 |

52.0 |

58.9 |

61.1 |

|

Bihar |

0.8 |

0.9 |

1.1 |

62.8 |

95.2 |

111.6 |

31.6 |

34.2 |

41.4 |

|

Gujarat |

0.3 |

1.3 |

1.8 |

27.2 |

25.0 |

27.5 |

28.3 |

40.3 |

44.3 |

|

Haryana |

2.4 |

3.4 |

4.8 |

17.7 |

21.7 |

15.7 |

47.3 |

67.3 |

59.9 |

|

Himachal Pradesh |

7.9 |

10.5 |

20.2 |

100.8 |

99.9 |

91.9 |

60.5 |

67.8 |

68.8 |

|

Jammu & Kashmir |

10.1 |

31.1 |

39.6 |

121.5 |

114.4 |

111.8 |

46.9 |

45.3 |

56.3 |

|

Karnataka |

3.7 |

4.9 |

3.9 |

48.8 |

40.2 |

51.5 |

26.8 |

27.9 |

28.3 |

|

Kerala |

42.5 |

51.8 |

51.0 |

41.4 |

48.2 |

47.5 |

6.6 |

6.9 |

5.9 |

|

Madhya Pradesh |

0.2 |

0.3 |

0.6 |

59.8 |

59.7 |

56.2 |

20.0 |

21.8 |

22.7 |

|

Maharashtra |

1.7 |

NA |

6.6 |

34.9 |

39.3 |

33.0 |

15.8 |

18.7 |

21.1 |

|

Orissa |

1.8 |

4.4 |

4.5 |

70.1 |

69.6 |

67.6 |

7.0 |

7.5 |

7.4 |

|

Punjab |

NA |

15.5 |

15.6 |

NA |

8.6 |

8.8 |

53.3 |

67.5 |

71.2 |

|

Rajasthan |

0.2 |

0.5 |

0.5 |

42.2 |

48.8 |

34.9 |

28.1 |

41.9 |

33.3 |

|

Tamil Nadu |

7.8 |

11.8 |

19.3 |

67.0 |

63.2 |

57.8 |

36.8 |

39.1 |

38.7 |

|

Uttar Pradesh |

3.5 |

3.8 |

4.1 |

36.1 |

39.3 |

38.6 |

47.4 |

55.6 |

59.2 |

|

West Bengal |

5.4 |

6.2 |

8.7 |

106.6 |

122.1 |

105.2 |

4.4 |

4.4 |

3.9 |

|

All India |

2.7 |

4.3 |

5.7 |

48.6 |

52.8 |

49.8 |

30.2 |

34.8 |

36.0 |

NA: data not available

Source: Livestock Census (various issues)

The demand for livestock products, especially milk and meat, in India has increased considerably in the recent years, and has a strong potential for further growth. Several socioeconomic indicators underlie this trend. The per capita consumption of milk in many parts of the country is low compared to minimum nutritional standards and to that of many developed and developing countries. The demand for milk and dairy products is income-elastic, and growth in per capita income is expected to increase demand for milk and milk products. Empirical evidences show that the composition of the food basket of an average Indian is gradually shifting towards livestock products (Radhakrishan and Ravi, 1990; Kumar, 1998). Other socioeconomic and demographic factors such as urbanization, changing food habits, and lifestyle also reinforce growth in demand for dairy products.

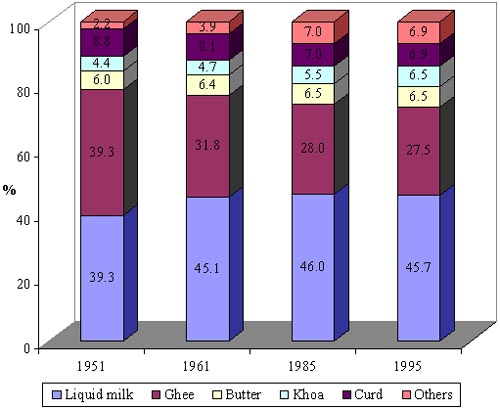

The per capita availability of milk in the country has grown at a rate of 3.02% per annum from 1980-81 to 1990-91, and at 2.19% per annum from 1990-91 to 1998-99, with an average annual growth rate of 2.52% from 1980-81 to 1998-99 (Saxena, 2000). The imports of milk products have declined over the years, while exports have slightly increased. However, net imports of milk equivalent have been very small in relation to total domestic milk production (0.01%). Therefore, domestic consumption of milk has remained more or less equal to the domestic production of milk. Milk consumption varies widely across regions and economic groups, and also between urban and rural households. The changing consumption pattern of milk in the country is presented in Figure 1.2. Liquid milk comprises the largest single share of the dairy product consumption profile. The share of fat-based products like ghee showed a declining share, and that of western products like cheese and ice cream witnessed an increasing trend and is expected to increase further due to changes in food habits, marketing strategies, income levels, changes in demographic factors, etc.

A study conducted by the National Council of Applied Economic Research (NCAER) in dairy cooperative societies in Operation Flood (OF) areas showed that milk consumption levels in OF areas vary across size groups and regions and are substantially higher than the national average (Table 1.7). Between 1988-89 and 1995-96, the per capita consumption of milk increased from 290 gms to 339 gms at the aggregate level. A similar trend was observed for individual zones. The consumption of fluid milk rose sharply in the southern and eastern zones and remained almost constant in the western zone and declined in the northern zone (Shukla and Brahmankar, 1999).

Table 1.7 Per capita milk consumption (gm/capita) in Operation Flood Areas: 1995-96

|

Zone |

Landless |

Marginal |

Small |

Semi-medium |

Medium |

Large |

|

North |

452 |

422 |

515 |

541 |

687 |

678 |

|

West |

212 |

212 |

234 |

236 |

226 |

208 |

|

South |

304 |

271 |

308 |

304 |

300 |

389 |

|

East |

224 |

264 |

239 |

243 |

237 |

245 |

|

All Zones |

318 |

285 |

339 |

348 |

444 |

445 |

Source: Shukla and Brahmankar (1999)

Figure 1.1 Consumption patterns of milk and milk products in India: 1951-95

Source: Dairy India (1997)

Given the high income elasticity of demand for milk, the demand for milk and milk products is expected to grow at a rapid rate. A study conducted by Saxena (2000) using NSS data for 1993-94 showed that the income elasticity of demand for milk and milk products is higher (1.96 national level) in rural areas (ranging from 1.24 in Punjab to 2.92 in Orissa) compared to urban areas (ranging from 0.99 in Punjab to 1.78 in Bihar). The northern region in general and Gujarat in the western region show low-income elasticity of demand for milk and milk products. The high values of income elasticity for different states in the Eastern region - varying from 2.5 to 2.9 in rural areas and from 1.5 to 1.8 in urban areas show a very strong preference for milk and milk products with an increase in income in these regions. Further increases in per capita income and changing consumption patterns would lead to acceleration in demand for milk and other livestock products in India and is thus expected to give a boost to this sector. Radhakrishna and Ravi (1992), Gandhi and Mani (1995), Kumar (1998), Dastagiri (2001) and many others have also estimated demand and income elasticity of demand for milk and milk products, which show similar patterns (Table 1.8).

Table 1.8 Income/expenditure elasticity of demand and projections of demand for milk in India

|

|

Rural |

Urban |

Demand 2020 (million tons) |

|

Radhakrishna & Ravi (1992) |

1.15 |

0.99 |

n.a. |

|

Gandhi and Mani (1995) |

1.70 |

1.06 |

n.a. |

|

Kumar (1998) |

n.a. |

n.a. |

126.0 - 182.8@ |

|

Saxena (2000) |

1.96 |

1.32 |

85.7# |

|

Delgado, et al. (2001) |

n.a. |

n.a. |

132.0 |

|

Dastagiri (2001) |

1.36 |

1.07 |

147.21 |

Note:

#: Estimates for 2007-08;

n.a.: not available;

@:estimates based on 4% growth in GDP (126.0), 5% growth (142.7) and 7% growth in GDP (182.8);

According to a study conducted by Delgado et al. (2001), the per capita consumption of milk products in developing countries is expected to be on average only one-third that of developed countries in 2020, yet in aggregate terms, 60% of the world's milk consumption will take place in the developing countries. This is a major change from the early 1990s when the developed countries consumed 59% of the world's milk. The projected annual growth rate for milk is 4.3% from 1993 to 2020. Kumar (1998) projects a 2020 demand for milk of 142.7 million tons at 5% growth in GDP and 182.8 million tons at 7% growth in GDP. However, Saxena (2000) projected the total national demand for milk to reach its peak at 85.7 million tons in 2007-08 and decline thereafter. He argued that the domestic market may expand if a rise in per capita income in the future is more favorable towards lower income groups and regions, as the income elasticity for such groups and regions (eastern) is much higher than the average. There are wide differences in these estimates, and the differences are mainly due to different assumptions of elasticity, population projections, and other parameters. However, it is clear that domestic demand for dairy products is going to increase substantially in the years to come. Apart from this, there may be good opportunities in the export market. In order to cater to both domestic and external markets, the production of milk and dairy products should be targeted for rapid growth.

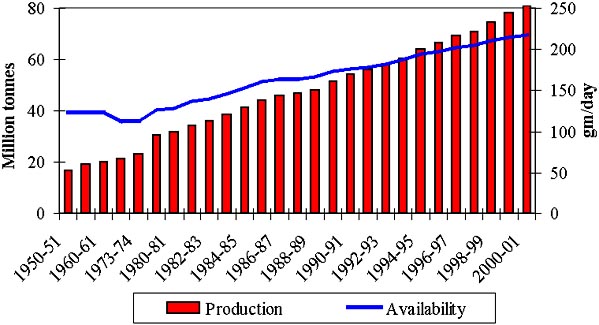

Milk production in the country was more or less stagnant during the 1950s and 1960s, and annual production growth was negative in many years. Milk production was estimated at about 17 million tons in 1950-51, rising to about 20 million tons in 1960-61 and 22 million tons in 1970-71. The annual compound growth rate during the first decade after independence was about 1.64% and this growth rate declined to 1.15% during the 1960s and the early 1970s. The performance of the Indian dairy sector over the last three decades has been extremely impressive. Milk production in the country has more than tripled to about 81 million tons between 1970-71 and 2000-01, with an average increase of about 4.5% per annum. The giant leap in milk production in the country is striking (Figure 1.3). It can be attributed mainly to increased demand driven by increased population, higher incomes and urbanization, and tight controls on imports of dairy products (Candler and Kumar, 1998). The period was also accompanied by the successful implementation of Operation Flood and other dairy development programs implemented by the State and Central governments, which although large in scale, only directly affected a small proportion of farmers. The growth in milk production during the decade of 1970s was about 4.5%, increasing to about 5.5% in the 1980s (Table 1.9). During the last decade (1990-91 to 2000-01), milk production in India increased at a growth rate of around 4.2%, which is much higher than the global rate of about 1%.

Table 1.9 Estimates of milk production and the growth rate of milk production in India: 1950-51 to 2000-01

|

Year |

Milk production |

Year |

Milk production |

|

1950-51 |

17.0 |

1991-92 |

55.7 |

|

1955-56 |

19.0 |

1992-93 |

58.0 |

|

1960-61 |

20.0 |

1993-94 |

60.6 |

|

1968-69 |

21.2 |

1994-95 |

64.0 |

|

1973-74 |

23.2 |

1995-96 |

66.2 |

|

1980-81 |

31.6 |

1996-97 |

69.1 |

|

1985-86 |

44.0 |

1997-98 |

70.8 |

|

1986-87 |

46.1 |

1998-99 |

74.7 |

|

1988-89 |

48.4 |

1999-00 |

78.1 |

|

1990-91 |

53.9 |

2000-01 |

81.0 |

|

Cumulative growth rate (%/annum) |

|

||

|

1950-51 to 1960-61 |

1.64 |

||

|

1960-61 to 1973-74 |

1.15 |

||

|

1973-74 to 1980-81 |

4.51 |

||

|

1980-81 to 1990-91 |

5.50 |

||

|

1990-91 to 2000-01 |

4.21 |

||

Source: Basic Animal Husbandry Statistics 1999, Department of Animal Husbandry and Dairying, Ministry of Agriculture, Government of India

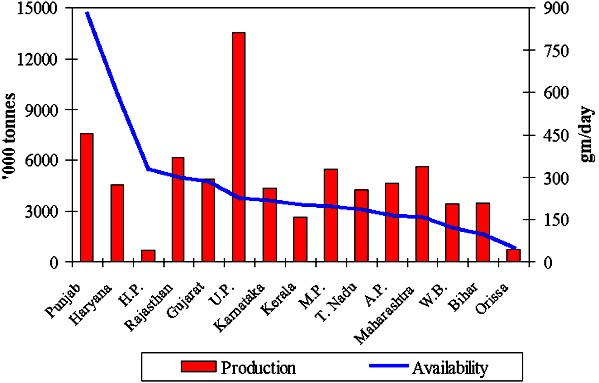

The major milk producing states in the country are Uttar Pradesh, Punjab, Rajasthan, Madhya Pradesh, Maharashtra, Gujarat, Andhra Pradesh, Haryana, Tamil Nadu, and Karnataka, accounting for about three-fourths of total milk production in the country. State-wise shares of Indian milk production for selected years in the 1980-97 period are shown in Table 1.10. Uttar Pradesh is the largest milk producing state, producing about 13.5 million tons of milk, followed by Punjab (7.6 million tons), Rajasthan (6.2 million tons), Maharashtra (5.6 million tons), and Madhya Pradesh (5.4 million tons) in 1998-99 (GOI, 1999). During 1982-83 (TE), the top five milk producing states were Uttar Pradesh (18.5%), Punjab (10.1%), Rajasthan (9.8%), Gujarat (6.8%), and Haryana (6.6%), accounting for more than half of total milk production (Figure 1.4). However, in the triennium ending 1998-99, Gujarat and Haryana lost their position among the top five producers. The top five milk producing states in 1998-99 were Uttar Pradesh (18.1%), Punjab (10.1%), Rajasthan (8.2%), Madhya Pradesh (7.5%), and Maharashtra (7.4%), and these states accounted for about 51% of milk produced in the country. The share of Karnataka, Kerala, Madhya Pradesh, Maharashtra, Tamil Nadu, and West Bengal in total milk production increased between 1980-82 and 1996-98. In contrast, the share of Bihar, Haryana, Rajasthan, Uttar Pradesh, and West Bengal declined during this period.

Table 1.10 State-wise shares of Indian milk production, selected years

|

State |

1980 |

1985 |

1990 |

1992 |

1993 |

1994 |

1995 |

1996 |

1997 |

|

Percent of total milk production |

|||||||||

|

Uttar Pradesh |

18.1 |

18.6 |

17.3 |

18.4 |

18.1 |

17.7 |

17.9 |

17.9 |

18.3 |

|

Rajasthan |

10.3 |

9.4 |

7.3 |

7.9 |

8.2 |

8.0 |

8.2 |

8.5 |

7.8 |

|

Punjab |

10.2 |

9.3 |

9.6 |

9.6 |

9.9 |

9.7 |

9.7 |

9.8 |

10.4 |

|

MP |

7.2 |

6.7 |

8.0 |

8.4 |

8.2 |

7.9 |

7.7 |

7.6 |

7.6 |

|

Gujarat |

6.8 |

7.8 |

6.2 |

6.5 |

6.5 |

7.0 |

7.0 |

7.0 |

6.9 |

|

Haryana |

6.9 |

5.9 |

6.3 |

6.4 |

6.4 |

6.4 |

6.1 |

6.1 |

5.8 |

|

Bihar |

6.1 |

5.6 |

5.1 |

5.5 |

5.3 |

5.1 |

5.0 |

4.9 |

4.9 |

|

Tamil Nadu |

5.5 |

6.9 |

6.0 |

6.0 |

5.8 |

5.8 |

5.7 |

5.8 |

5.6 |

|

AP |

6.4 |

6.4 |

5.3 |

5.4 |

6.2 |

6.6 |

6.4 |

6.5 |

6.4 |

|

Maharashtra |

5.6 |

5.7 |

6.8 |

7.1 |

7.0 |

7.5 |

7.5 |

7.4 |

7.4 |

|

Karnataka |

4.5 |

4.4 |

4.4 |

4.5 |

4.5 |

4.7 |

4.8 |

5.0 |

5.6 |

|

West Bengal |

4.1 |

5.3 |

5.4 |

5.2 |

5.1 |

5.1 |

5.0 |

4.9 |

4.8 |

|

Kerala |

2.9 |

2.9 |

3.0 |

3.3 |

3.3 |

3.3 |

3.3 |

3.3 |

3.3 |

|

Others |

5.4 |

5.0 |

9.4 |

5.9 |

5.5 |

5.1 |

5.4 |

5.4 |

5.3 |

Source: Basic Animal Husbandry Statistics 1999, Department of Animal Husbandry and Dairying, Ministry of Agriculture, Government of India

Per Capita Availability

Though India is the largest milk producer in the world, its position in terms of per capita availability is low compared to some countries. The per capita availability of milk declined during the pre-OF period. Per capita availability was about 124 gms per day in 1950-51, which declined to 112 gms per day in 1970-71. But the dairy sector took a leap forward during the 1970s, 1980s, and 1990s. The per capita availability of milk increased from 112 gms in 1970-71 to about 214 gms per day in 1999-2000 (Figure 1.3). However, the present level of per capita availability is well below the world average of 285 gms and also less than the 220 gms recommended by the Nutritional Advisory Committee of the Indian Council of Medical Research (ICMR). It remains well above the average for developing countries, and is even higher than some countries that exhibit higher average GDP. However, this must be seen in the context of relatively low levels of consumption of other animal proteins in the form of meat, so that total animal protein intake remains low for many segments of Indian society.

Figure 1.2 Trends in milk production and per capita availability in India; 1950-51 to 2000-01

Source: GOI (2001)

There are wide inter-state and inter-regional disparities in per capita availability of milk. The per capita availability of milk is higher in the northern states like Punjab (880 gms/day), Haryana (592 gms/day) and Himachal Pradesh (330 gms/day), whereas the eastern states have low availability of milk (51 gms in Orissa to 123 gms in West Bengal per person per day) in 1997-98 (Figure 1.5). The per capita availability of milk is highest in Punjab, followed by Haryana, Himachal Pradesh, Jammu, and Kashmir (282 gms/day) and Gujarat (269 gms/day). Considering the per capita milk requirement recommended by the ICMR at 220 gms per day, only seven states, namely Punjab, Haryana, Himachal Pradesh, Rajasthan, Gujarat, and Uttar Pradesh have per capita availability of milk above this level. There is also a wide disparity in consumption of milk between the rural and urban areas. The per capita consumption of milk in the rural areas is substantially lower (121 gms per day) as compared to urban areas (400 gms/day) (Initiatives, 1999).

Figure 1.3 Milk production and per capita availability of milk in selected states in India; 1998-99

Source: GOI (2001)

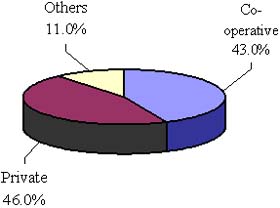

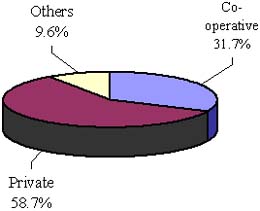

Like nearly all developing countries, India has co-existing "organized" and "unorganized" sectors for the marketing of milk and dairy products. Sometimes called the "informal" sector, the unorganized sector may be more usefully thought of as the traditional milk market sector, comprised of the marketing of raw milk and traditional products such as locally manufactured ghee, fresh cheese, and sweets. The organized or formal sector is relatively new in historical terms, and consists of Western-style dairy processing based on pasteurization, though adapted to the Indian market in terms of products. In some cases the traditional sector is quite well organized, with a complex net of market agents, and shows variation in numbers of and roles of market intermediaries. It may also be relatively formal, in that market agents may pay municipal fees and have vendor licenses, albeit not specifically registered for the dairy trade. The reasons underlying the existence of a large informal or traditional sector are the same as found in other countries: consumers are unwilling to pay the additional costs of pasteurization and packaging, which can raise retail prices by over 100%, and consumers often regard raw milk and traditional products obtained from reliable vendors as of better quality than formally processed dairy products. It should be noted that, unlike some countries, the Indian government has generally adopted a laissez-faire approach to the informal sector, which has allowed it to expand with the growth in demand, and serve both small farmers and resource-poor consumers. It is useful to get an overview of the broad aggregate of this sector and understand the type of "informal sector" which competes with the organized sector (cooperatives and modern-style private factories) in the field of processing, procurement, and marketing of milk and other dairy products. Of the estimated milk production during 1999-2000 of about 78 million tons of milk, the organized sector, primarily through the dairy cooperatives and organized private dairies, handled 10-12% of the total milk production, or 15% of the marketed surplus, and the rest finds its way into India's large, complex, highly differentiated traditional private trade in milk and dairy products (see Figure 1.6). The share of the organized sector in total procurement has increased from about 3.7% in the early 1960s to about 12% in the mid-1990s. There are large regional variations in the types of operators and their operating procedures. Cooperative milk marketing has a relatively strong hold in the states of Gujarat, Rajasthan, Maharashtra, Tamil Nadu, and Karnataka, yet is subservient to unorganized sector. Dairy cooperatives have a particularly low profile in the eastern and northern parts of the country. By and large, the informal sector comprising private milk vendors, traditional dudhias/halwais, and others continues to have the lion's share of the procurement and marketing of milk in India. This situation is unlikely to undergo a major shift, given consumer preferences. The informal sector is a large employment provider and has traditionally offered a wide range of services to households and institutional consumers. In metro cities - Delhi, Mumbai, Chennai, and Kolkatta- the introduction of bulk vending machines has given a strong advantage to cooperatives. With more focus on global trade and quality standards, the organized sector (cooperatives and the private sector, including multinationals) can be expected to play a greater role than at present. At some point in the future, it might handle about 25-30% of the total milk produced in the country, yet leaving the major share of milk procurement and marketing to the informal sector. This will require an increased willingness by consumers to pay for the additional processing. Hence, the informal sector has a major potential role to play in milk procurement and marketing in India. In recent years, added emphasis has been given to clean milk production and ensuring quality standards as per international norms, which calls for greater responsibility, particularly on the part of informal sector, in meeting the set quality standards.

Figure 1.4 Relative shares of

main milk marketing channels in formal and informal markets in

India

As % of marketed surplus of milk:

Formal: 15%; Informal/traditional: 85%

Source: Dairy India (1997)

Governments' protectionist policies affect the prices received by producers, and the impact of such policy measures is reflected in the gap between domestic prices and the world price of a commodity. This gap shows the level of protection for the producers. It is well known that Indian agricultural policies have been strongly influenced by the need to achieve self-sufficiency in foodgrains since the 1960s, and in the dairy sector since the early 1970s. The import and export of dairy products was restricted through various non-tariff measures (NTBs) like quantitative restrictions (QRs) and canalization until the early 1990s. Competition within the country was also restricted through industrial licensing by restricting the entry of the formal private sector, including multi-national companies (MNCs), in the milk processing and the product manufacturing sector. Cooperatives were given preferential treatment for setting up milk processing plants. However, since the early 1990s, India has embarked upon a more liberal policy framework, which was reinforced with India becoming member of the WTO, exposing the Indian dairy sector to the world markets.

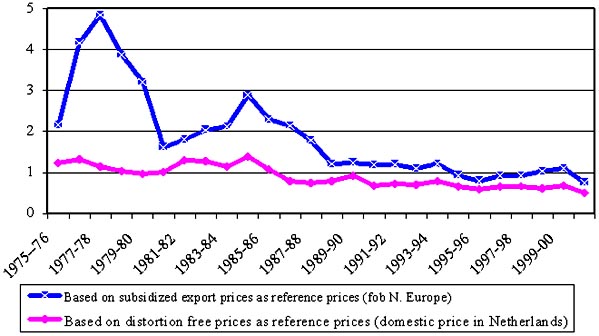

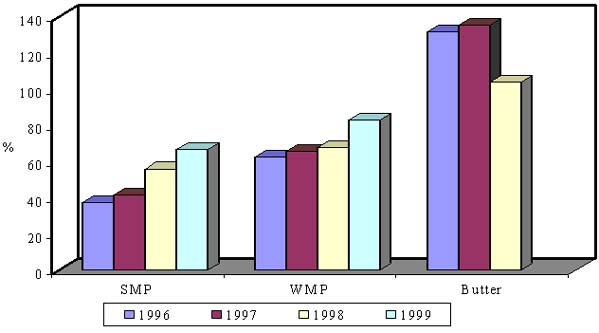

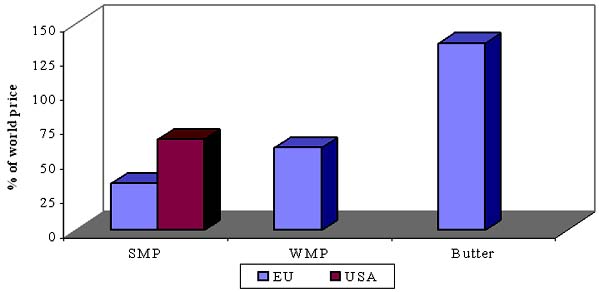

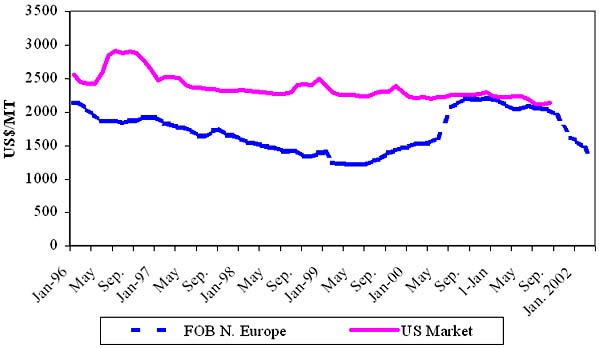

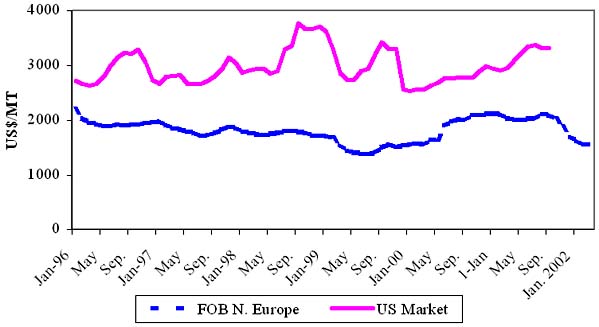

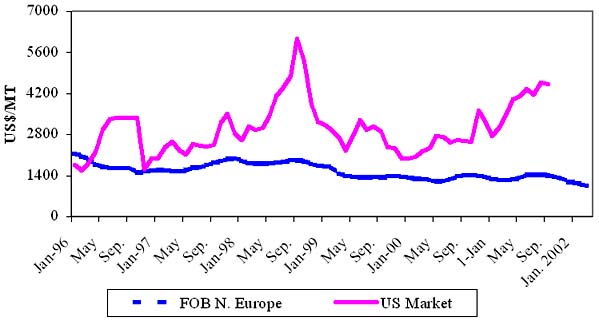

A comparison of nominal protection coefficients (NPCs) for the 1975-2000 period shows that the level of NPCs (at the official exchange rate) for major dairy products, namely skim milk powder (SMP), butter, butter oil and recombined milk, were well above unity for the average 26-year period of 1975-2000, and remained above unity even if estimates are considered at the shadow exchange rate (Figures 1.7-1.10). The trend in the estimates of incentive indicators is declining and estimates are much lower in the 1990s than the average of the entire period. This temporal behavior of NPCs is somewhat similar for all products. It is high during the late 1970s, declines during the early 1980s, again rises in the mid-1980s, and then gradually falls, and tends to approach unity and even goes below unity in the 1990s. It is important to note that the level of protection during the second half of the 1990s is only one-fifth of the level of protection during the second half of the 1970s. The gradual reductions in NPCs, especially after the second half of the 1980s, have been largely due to an improvement in world prices, and partially due to the falling exchange rate of the rupee. These results of NPCs indicate that India has not been an efficient import substituter of dairy products, if one compares Indian dairy prices with the world prices. However, the reason for this largely can be ascribed to the nature of world prices of dairy products, which have been highly distorted by the large export subsidies of the EU and the US. For example, the average export price (FOB) of SMP was about US$ 1,444 per ton in 1999; and the EU and the US paid about US$ 867 and US$ 950 per ton, respectively, as subsidies on SMP exports, more than 60% of the world prices (Sharma, 2001). There was some decline in the export subsidy to comply with commitments made under WTO, but the export subsidy as a percentage of world market prices showed an upward trend (Figure1. 11). If international prices were not artificially depressed by the policies of the EU and the USA, protection levels for Indian dairy products would have been much lower and even less than unity in most of the years. The estimates of NPCs at distortion-free prices (Netherlands domestic prices) are significantly lower, and even less than unity, in most of the cases for all dairy products considered in the study.

Figure 1.5 NPCs of skim milk powder (SMP) under importable hypothesis; 1975-76 to 2000-01

Source: Sharma and Gulati (2002)

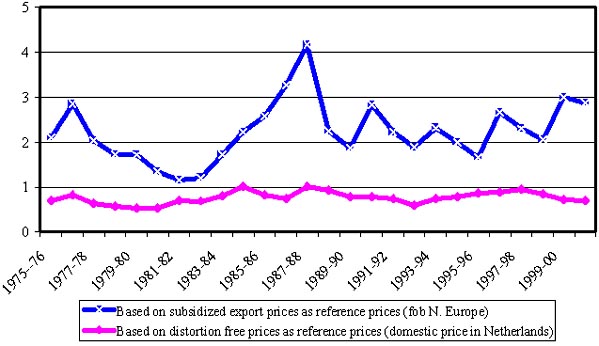

Figure 1.6 NPCs of whole milk powder (WMP) under importable hypothesis; 1975-76 to 2000-01

Source: Sharma and Gulati (2002)

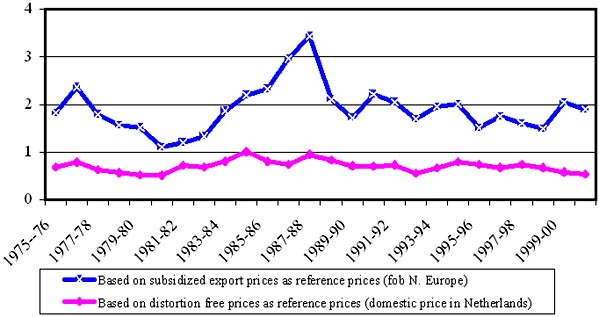

Figure 1.7 NPCs of butter oil/ghee under importable hypothesis; 1975-76 to 2000-01

Source: Sharma and Gulati (2002)

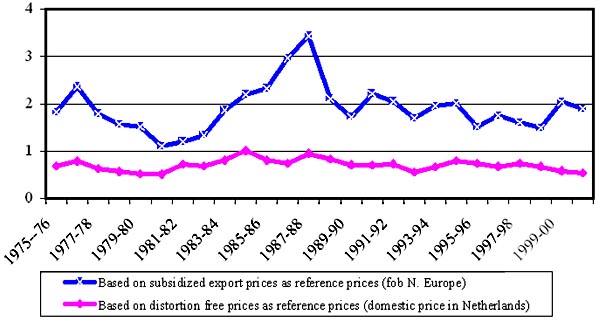

Figure 1.8 NPCs of liquid milk under importable hypothesis; 1975-76 to 2000-01

Source: Sharma and Gulati (2002)

Source: OECD (2001)

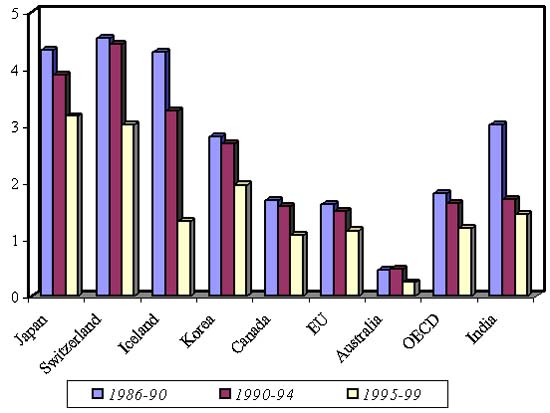

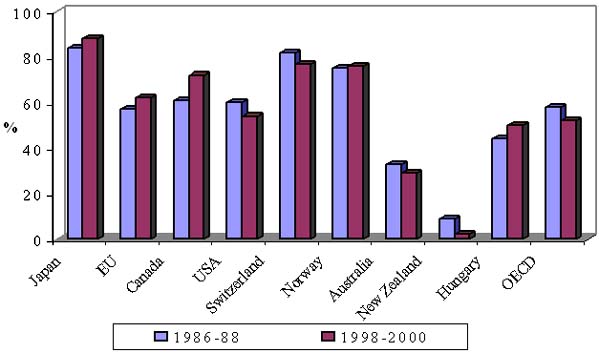

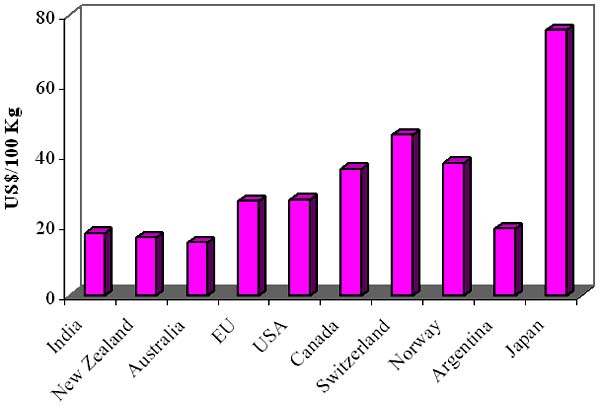

The comparison of NPCs for other important milk producing/consuming countries compared with Indian estimates provides very good insights about the distortions in the world dairy markets. Japan stands at the top with the highest protection (3.16 in 1995-99) given to its milk producers, followed by Switzerland (3.01), Korea (1.95), and the OECD region as a whole (1.19). India stands fourth with a NPC level of 1.45 at the given world market prices (Figure 1.12). However, if we compare the NPC figures calculated at distortion-free world prices for India, the NPC value drops to nearly 0.76, which is much lower than Canada and the EU levels. Comparison of NPCs of dairy products among different countries indicates that the dairy sector has been one of the most highly protected sectors in the developed countries. There is, however, a silver lining during the 1990s. The protection for dairy products in India has drastically come down, and in commodities like SMP, it has even become negative in some years during the 1990s. The high NPCs for Indian dairy products reveal that under a liberalized atmosphere, the sector may face difficulties in adjustment.

Figure 1.10 Estimates of NPCs of milk for selected countries: 1986-90 to 1995-99

Source: OECD (2001); For India: Sharma and Gulati (2002)

With the growth in demand and production, the protectionist policies of the 1970s and 1980s, followed by the economic policies of trade liberalization during the 1990s, the Indian dairy sector witnessed some marginal structural changes in milk production, processing, and marketing.

Among milch cattle, the population of low-yielding nondescript milch cattle showed a considerable decline, while the population of crossbred milch cattle exhibited a sharp increase, indicating farmers' preference for crossbreds for milk production. The marked shift in the sex composition of both the breeds of cattle in favor of females highlighted the declining importance of draft animals and the increased importance given to milk production. By and large, buffaloes continued to be the predominant milch animals contributing to milk production in India. The northern and western parts of the country have a predominance of buffaloes in milk production, while the eastern and southern parts are predominantly cow-milk-producing regions. In the southern region and parts of northern India, the crossbred population is on a steady rise, contributing to milk production.

With regard to management practices, owing to diminishing common property resources and pastures, the grazing of animals is on the decline and stall-feeding is on the rise. With regard to reproductive management, natural services are declining and artificial insemination is becoming popular in cattle and buffaloes. Along with rural dairy farming, urban and peri-urban dairy farming is being taken up to cater to urban milk demand through the informal market. The urban and peri-urban dairy farming involves rearing of crossbred cows and high-yielding buffaloes maintained on purchased feeds and fodders in stall-fed conditions, and following most of the modern dairy farming practices. This sub-sector has been contributing to milk production in selected areas of the country. But growing environmental concerns and health consciousness might impose checks on their extension and intensification and need to be investigated thoroughly.

In the formal sector, the industrial structure that emerged as a result of Operation Flood involved an organized sector consisting of dairy cooperatives, government milk schemes, and formal private processors. The informal sector, largely untouched, continued to be composed of small traders (dudhias, local halwais), urban milk producers, and intra-village trade directly from producers to consumers. Although dairy cooperatives comprise the single largest formal organization in terms of market share, they are engaged in active competition with the informal sector in small towns and peri-urban villages and with some private companies in urban milk centers. The share of the organized sector in total milk procurement has increased over a period of time and is further expected to rise in the new economic environment of liberalization and globalization. The repeal of industrial licensing under new economic policy provided opportunity for private entrepreneurs and multinational companies to invest in new processing capacities.

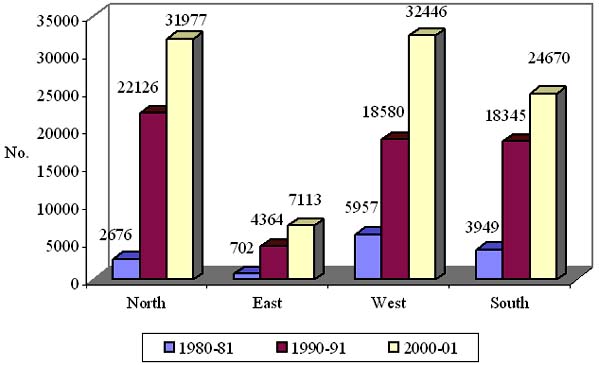

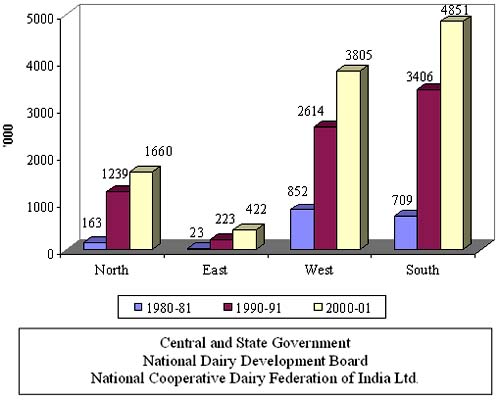

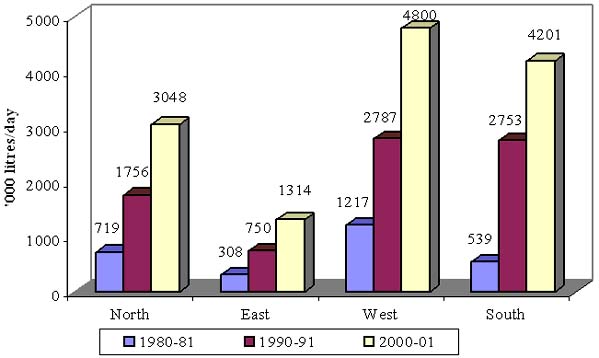

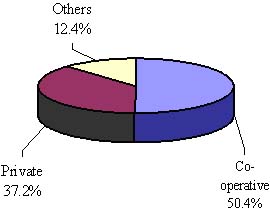

The share of organized sector in total milk procurement has increased from 3.68% in 1961 to about 10-12% in the mid-1990s (Table 1.11). These estimates are not very reliable, due to poor information for the unorganized sector and those plants below 10,000 litres per day capacity. Within the organized sector, the share of cooperatives is higher than private companies. The total milk procured by the cooperative sector has increased from 2,562 thousand kg per day in 1980-81 to 16,504 thousand kg per day in 2000-01 (Figure 1.13). The share of the western region was highest (47.85%) followed by southern region (3.75%) and lowest in the eastern region (3.89%). Among the states, the procurement by cooperatives is highest in Gujarat (4567 thousand kg/day) followed by Maharashtra (2,979 thousand kg/day), and low in the eastern states like Bihar (330 thousand kg), Orissa (94 thousand kg), and West Bengal (204 thousand kg). The number of dairy cooperative societies has also increased significantly from 13,284 in 1980-81 to 96,206 in 2000-01 (Figure 1.14). The number of farmer members has risen from 1.7 million to 10.7 million during the same period (Figure 1.15). The Anand pattern multi-tier cooperatives have strong backward linkages with the farmers and collect milk from rural producers through village dairy cooperative societies (Figure 1.16). The majority of private processors depend on contractors (through informal or formal contracts) and traders to procure milk from farmers (Figure 1.17). The private sector has the advantage of flexibility in pricing and in business policy decisions.

Table 1.11 National milk procurement by Operation Flood and other organized and informal sectors in India

(million tons and%)

|

|

1972 |

1980-81 |

1988-89 |

1994-95 |

1995-96 |

2000-01p |

|

Milk production |

23.00 |

31.60 |

53.70 |

64.10 |

66.10 |

81.00 |

|

Organized sector |

1.30 |

3.10 |

5.80 |

6.40 |

n.a. |

n.a. |

|

O-F Cooperatives |

0.24 |

1.01 |

3.58 |

3.75 |

4.00 |

6.02 |

|

Non-OF organized sector |

1.04 |

2.12 |

2.46 |

2.63 |

n.a. |

n.a. |

|

Share of co- operatives as % of organized sector |

18.56 |

32.33 |

61.33 |

58.77 |

n.a. |

n.a. |

|

Handled by informal sector |

19.65 |

21.73 |

28.46 |

56.72 |

n.a. |

n.a. |

Note: p: provisional figures; Figures in parentheses indicate%ages to total milk production

Source: Candler and Kumar (1998); NDDB (2001)

Figure 1.11 Trends in growth of dairy cooperative societies: 1980-2000

Source: NDDB, Annual Report 2000-01

Figure 1.12 Trends in Farmer members of dairy cooperative societies: 1980-2000

Figure 1.13 Anand Pattern Model

Source: NDDB (1987)

Figure 1.14 Milk procurement channels for private sector plants

With the recent changes in domestic policy (the repealing of licensing requirements under the MMPO) and trade policy (the removal of QRs on imports and exports of dairy products) the share of the private sector in milk procurement is expected to increase. This could lead to some structural changes in production sector, whereby the private processors will try to reduce transaction costs and may promote large commercial dairy farms.

In many areas of the country, dairy farms located within the city or in its periphery (peri-urban and urban dairy farms) still have a major sway over their traditional customers. These give cooperative as well as commercial dairies in many cities a good run for their money (Shah, et al., 1995). Customers often have a long association with the farm owner, and the quality and purity of milk is perceived to be the major advantage of these farms. Private vendors (dudhias) are dominant in the periphery of the cities and typically serve low- and middle-income consumers. They are not particularly known for good quality of milk, but nevertheless offer the lowest retail prices to consumers. These vendors collect milk from the doorsteps of milk producers of interior villages and offer sale to consumers first, and the remaining is supplied to halwais (sweet makers) or contractors, whichever is nearest at hand. In contrast to these operators in the unorganized sector, the cooperatives and some private units sell through the network of retailers. The commission offered by the cooperatives to these retailers is significantly lower than what is offered to them by private sector units.

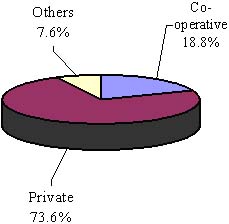

India has an age-old tradition of drinking milk. About 89% of households consume loose milk whereas only 9% of households consume packaged milk (Roy, 2002). The penetration of branded milk is highest among high-income people and towns having a population of more than ten lakh. The acceptance of packaged milk is high in Maharashtra, Gujarat, West Bengal, Kerala, and Karnataka, and states with the potential for expanding the market for packaged branded milk (Orissa, Assam, Punjab, Haryana, Bihar, and Rajasthan). The quantity of liquid milk marketed by cooperatives has increased significantly from 2.8 million litres per day in 1980-81 to 13.4 million litres in 2000-01 (Figure 1.18). The share of the western region is highest (35.92%), followed by the south (31.44%), the north (22.81%), and the eastern part of the country (9.83%). The penetration of packaged branded liquid milk is expected to increase due to increased awareness about food safety and quality standards.

Figure 1.15 Trends in liquid milk marketing by cooperative dairy plants: 1980-2000

Source: NDDB, Annual Report 2000-01

Dairy has long been a highly regulated industry in India and in many other countries. However, in the early 1990s, the Indian dairy industry entered a period of domestic and trade policy reforms. Two major policy events - 1991 macro-economic reforms and the 1995 Uruguay Round Agreement (URA) - represented a significant modification of previous policies by opening up markets and limiting government restrictions. Although the extent to which such efforts would be carried forward in future policies (e.g., the next rounds of WTO negotiations) of the developed countries like the EU, USA, Japan, and Canada is uncertain, these changes retain significant potential to influence world dairy trade. The political importance of the dairy sector in most countries has resulted in a plethora of government interventions in dairy production, marketing, and trade. In addition to trade and domestic policy reforms, technological developments in the dairy and food processing industries will take on a greater importance in coming years.

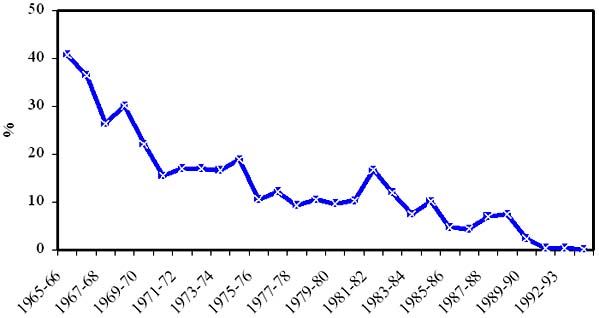

Despite being the largest milk producer in the world, India is a minor player in the global trade of dairy products. The country was primarily an import-dependent country until the early 1970s, and most of the demand-supply gap of liquid milk was met by importing butter/butter oil and milk powders under food aid programs as gifts. The share of skim milk powder and butter oil imports in total milk throughput declined from about 41% during the mid-1960s to less than 1% during the early 1990s (Figure 1.19). This transition of the Indian dairy industry from a position of net importer to that of surplus was induced by strict import controls, growth in domestic production, and the efforts of Operation Flood and other dairy development programs. India started exporting surplus dairy products such as milk powders, ghee, butter, and cheese in the 1990s, however, the exports are negligible compared to both domestic production and international trade. The exports and imports of most dairy products were regulated through the Agricultural and Processed Food Products Export Development Agency (APEDA) and the National Dairy Development Board (NDDB) until the early 1990s; however, steps to liberalize dairy trade were initiated in the mid-1990s when imports of milk powder and butter oil were de-canalized and de-licensed. In the new Exim policy announced on March 31, 2002, the government removed all restrictions on the import and export of all dairy products (Economic Times, 2002).

Source: Dairy India (1995)

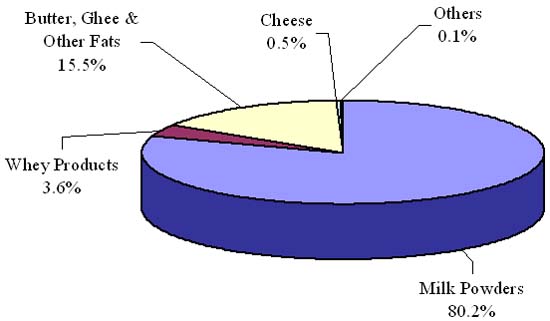

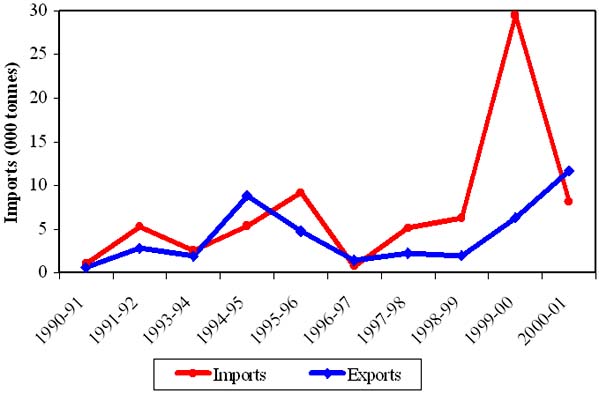

India's dairy product exports are occasional and primarily in the flush season. Although India exports a wide variety of dairy products, milk powder (80.2%) and butter, ghee, and other fat-based products (15.5%) remain the major export items (Figure 1.20). Imports of dairy products increased from nearly 1,000 tons (valued at Rs. 3.76 crore) in 1990-91 to as high as 29,500 tons (Rs. 18.1 crore) in 1999-00, and declined during 2000-01 to about 8,000 tons (Figure 1.21), while the exports of dairy products increased from 604 tons to about 6,327 tons during the same period, leading to a condition of essentially zero net imports. The major destinations for Indian dairy products are Bangladesh, UAE, the United States, and the Philippines. These export figures clearly demonstrate that Indian exports are still in their infancy. However, the country has the potential to become one of the leading players in dairy product exports, since India is located amidst major milk-deficit countries in Asia and Africa. Secondly, milk production in India is scale-neutral and labor-intensive. Due to low labor costs, the cost of milk production in the country is significantly low. Despite these positive factors, there is a long way to go in order to improve the quality of Indian milk and milk products. In order to become globally competitive, significant investment has to be made in the supply chain of milk procurement, processing, and marketing. Also, training has to be given to the farmers and processors to improve the quality of milk and dairy products to bring them up to international standards.

Figure 1.17 Share of major dairy products in India's exports of dairy products during 2000-01

Source: DGCIS (2001)

Figure 1.18 Trends in imports and exports of dairy products in India: 1990-2000

Source: DGCIS (various issues)

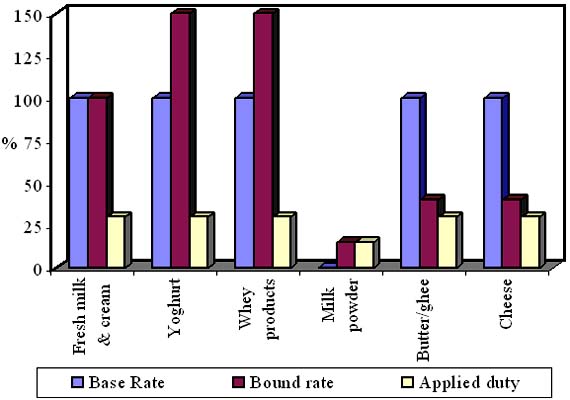

Commercial imports of dairy commodities were significant until the early 1970s, comprising of about 50% to 60% of throughput, but declined significantly in the 1980s and 1990s. However, the imports of milk powders and butter/butter oil increased substantially in the late 1990s, mainly due to low import duties on these two products as a commitment under the WTO Agreement. India is among the few countries who has low bound rates of duty for major dairy products like milk powders, butter, butter oil, and cheese (15-40%) as opposed to relatively high tariffs (100-150%) on less sensitive products like milk, cream, butter milk, and yoghurt (Figure 1.22). The small flow of cheap imports in the second half of the 1990s, mainly due to low import tariffs on the milk powders and other major dairy products, may have hurt some segments of the domestic industry, but was negligible in scale compared to the overall domestic market. Although imports of cheese are still low, they grew at a rapid rate during the 1990s.

Figure 1.19 Base (1986-88), bound (2004) and applied (2002-03) rates of duties for dairy products[36] in India

Source: GOI (2002)

The dairy sector can be represented by three separate segments/activities. The first activity, farm production, consists of milk production and transportation to milk plants. In the formal sector, processing is the second activity, with raw milk as the input and pasteurized milk and dairy products as the outputs. Transportation of products to the wholesale market and marketing (domestic and export markets) is the third activity.

The major stakeholders in the Indian dairy policy are milk producers, processors (cooperative, private, government, etc.), traders, wholesalers, retailers, informal sector processors and sellers, middlemen/contractors, consumers, the non-dairy industries, the government (central and state), veterinary drug manufacturing and marketing companies, as well as households without dairy animals (Figure 1.23). In what follows, we attempt to focus on the interests and concerns/problems raised by the producers, processors, and consumers in the context of the new policy environment that is emerging.