![]()

![]()

Discussion Draft for Comments:

Please do not cite or distribute

Nipon Poapongsakorn[139]

Viroj NaRanong

Uthai Kanto

Adis Israngkura

May 2002

This paper was produced as part of Phase I of an IFPRI-FAO project entitled "Livestock Industrialization, Trade and Social-Health-Environment Impacts in Developing Countries", funded by the Department for International Development (DFID), U.K., through the Livestock, Environment and Development (LEAD) initiative at FAO. Correspondence may be addressed to the scientific coordinator for the project, Dr. Christopher Delgado, IFPRI, 2033 K St, N.W., Washington D.C. 20006, USA. Email: [email protected]

This country report is part of the FAO-IFPRI led study “The on-going industrialisation of the livestock sector in the peri-urban areas of developing countries and its effects on the poor and on the environment.” The main purpose of the study is to analyze the on-going industrialization with a view to identifying the true costs and benefits in terms of the environment and equity and to device strategies for environmentally and socially more sustainable livestock development.

The study is divided into two phases. The first phase of the study (Phase I) comprises mainly descriptive and qualitative part of the study. The quantitative part, which will based on estimation of production frontier using data from field survey, and study on effects of scaling-up on livelihood, well-being, and poverty alleviation, would be carried on in Phase II.

Due to different nature of each livestock subsector, this report would deal with each subsector separately. The organization of this report is as follows. Section 1 provides an overview on effect of trade liberalization on agriculture and livestock in Thailand. Section 2 deals with poultry, specifically broilers and layers. Sections 3 and 4 deal with swine and dairy cattle, respectively. Each chapter covers the following issues: technological change in production in the last decade or two, effect of trade (or lack thereof) and trade negotiation, effect of government programs, distortions, and regulations, and characteristics of the firms, scale, and contractual arrangement. Section 5 discusses environmental issues and remedies. It analyzes effects of livestock industrialization on environment. When appropriate, it touches upon health-related requirements and effects on trade and consumer health as well as animal welfare requirements and their effects on production. It describes specific programs designed to remedy the environmental problem (e.g., in swine production). The last chapter syntheses the effect of technological changes (especially scaling-up) on production, contractual arrangement, and partly on environment and health.

Despite the rapid decline of the agricultural sector in the last two decades, agricultural exports have remained the significant source of foreign earnings as Thailand is still the world major exporter of rice, rubber, cassava, canned pineapple, sugar, chicken, shrimp and canned tuna, etc. Meanwhile the share of agricultural imports have risen as the expanding industries need to use more imported raw materials and the Thais have to import food and food products that cannot be competitively produced in Thailand. The importance of agricultural trade has been made possible by the outward oriented trade policy. However, the domestic pricing policy of agricultural products has a tendency to shift towards increasing subsidy in the form of trade distorted support measures

Since trade liberalization in Thai agriculture has been determined both by the government unilateral liberalization policy and the commitments under the Uruguay Round agreement on agriculture (AoA), this section will discuss both policy measures. The next section is an explanation of the implementation of the AoA. The key issues are what did Thailand give and get from the agreement. The discussion will emphasize the role of the livestock trade.

The Thai agriculture has long been open to foreign trade since 1855 when the Thailand was forced to sign the Bowring Treaty with the English government. Since export and import taxes were set at the rate not exceeding 5%, the Treaty resulted in the rapid expansion of agricultural trade and rice production in the late 19th Century. Today agricultural trade accounted for more than 85 percent of agricultural GDP. Meanwhile livestock trade accounted for more than 90 percent of livestock GDP. (see table 1.1).

Table 1-1 Degree of Trade Opening on Agriculture and Livestock sector

|

Year |

Degree of Trade Opening |

|

|

Agriculture |

Livestock |

|

|

1988 |

52.39 |

38.72 |

|

1989 |

55.66 |

36.49 |

|

1990 |

52.83 |

42.23 |

|

1991 |

52.18 |

44.14 |

|

1992 |

49.91 |

51.18 |

|

1993 |

55.20 |

48.46 |

|

1994 |

57.86 |

49.15 |

|

1995 |

56.77 |

45.98 |

|

1996 |

52.70 |

45.72 |

|

1997 |

58.15 |

68.53 |

|

1998 |

60.19 |

92.99 |

|

1999 |

61.63 |

71.41 |

|

2000 |

80.57 |

94.56 |

Sources : 1) NESDB 2) Department of Business Economics

Note: Calculated by TDRI

Beginning in the mid 1980s, there were a series of liberalization policies in response to both internal and external changes. In the mid 1980’s, the Thai agriculture began to rapidly lose its comparative advantage. Internally, the cost of production rose rapidly as the forest lands were exhausted, and the industrial booms began to attract large number of young workforce from the agricultural sector, resulting in an absolute decline in the size of agricultural labor force and rapid increase in real wage rate in the early 1990’s. Externally, there was a worldwide slump in agricultural prices. The Thai farmers were caught in a situation of cost-price squeeze. The situation was worsened when the Thai rice exports were seriously affected by the US subsidized rice export under the PL480 program. Moreover, the US government also used the super 301 law to sanction Thai exports if Thailand failed to strengthen the properly rights legislation and enforcement. The Thai government, therefore, decided to actively participate in the Uruguay Round in order to defend her interests. One of the major objectives of participation was to establish the multilateral trade disciplines governing world agricultural trade. To strengthening her position, Thailand joined the Cairns Group.

In the late 1980’s and early 1990’s, the globalization forces were at its height, thanks to the rapid world economic growth, particularly the miracle growth of the East Asian countries. While the Uruguay Round progressed slowly, many countries began to establish the free trade zone and regional economic cooperation. Thailand and her ASEAN neighbor decided to establish the ASEAN Free Trade Agreement (AFTA). In addition to the common preferential tariffs for manufacturing products AFTA has also been expanded to cover most of agricultural trade. In 1989, Thailand also joined the Asia-Pacific Economic Cooperation (APEC). In an attempt to reduce impediments to trade and investment, APEC has launched an Early Voluntary Sectoral Liberalization (EVSL) initiatives aimed at liberalizing trade in 15 sectors by 2005. But this initiative has not yet achieved the objective.

Before the conclusion of the UR, the government launched the major tariff reform. The objective of the 1994 reform is to improve the competitiveness of Thai exports by substantially reducing the average applied tariff rate from 30% in 1994 to 17% in 1997 and changing the tariff structure. The tariff structure reform is to reduce the number of tariff rates from almost 40 rates to 6 rates based on the value added escalation system. Several tariff reductions were made as part of this reform process in 1996, covering agricultural products, intermediate, parts and components and manufactured good. As a result, import duties fell from 19% of government revenue in 1994 to 13% in 1997.

In the wake of financial crisis in 1997, the government first reacted protectively by imposing high tariffs on imported luxuries and a 10 - percent surcharge on all goods subject to tariffs of 5% or more. But as part of the government’s package of measures to encourage investment, the surcharge was abolished and tariff rates on 600 tariff lines covering inputs used by Thailand’s main industries were reduced in August 1999. Then in August 2000, another round of tariff reductions of intermediate goods was made. As a result, the average applied MFN tariff was lowered to 17% in 1999 and 15% in 2000.

At the same time, Thailand has continued to streamline actual trade measures in order to facilitate international trade. The legislation on customs valuation was passed in 2000. The Customs Department has also streamlined the customs procedures, resulting in shorter time for customs clearance and valuation. Thailand maintains few quantitative restrictions on imports. It has also introduced few trade defense measures in accordance with the WTO rules, i.e., a new Anti-dumping and Countervailing Duty Act in 1999 to replace the old regulations. But it has not yet been able to make effective use of the new measures.

Thailand has made commitments in three areas under the UR Agreement on Agriculture (AoA), i.e., market access, domestic subsidy and export subsidy.

a) Market Access: Thailand has committed to reduce tariffs on 740 tariff lines, resulting in a reduction of 24% over the 1995-2004 period. The average final bound rate will be 32% in 2004, down from pre-UR average rate of 49%. The share of tariff bindings in agriculture has risen to 100% from 98% in 1995. However, the applied tariff rates have been lower than the bound rates. Because of the tariff reductions between 1994 and 2000, the average applied tariff for agricultural products has declined from 43% in 1995 to 32% in 1999 and 28% in 2000 (see Table 1.2).

Table 1-2 Tariff rate for Agricultural product during 1995-2004

|

Products |

Tariff Rate |

Outquota Tariff Rate Reduction (%) |

||||||||||

|

In Quota |

Out Quota |

1995 |

1996 |

1997 |

1998 |

1999 |

2000 |

2001 |

2002 |

2003 |

2004 |

|

|

1. Fresh milk |

20 |

46 |

45.5 |

45.0 |

44.5 |

44.0 |

43.5 |

43.0 |

42.5 |

42.0 |

41.5 |

41.0 |

|

1.1 Flavoured milk |

20 |

93 |

92.1 |

91.2 |

90.3 |

89.4 |

88.5 |

87.6 |

86.7 |

85.8 |

84.9 |

84.0 |

|

2. Skim milk powder |

20 |

240 |

237.6 |

235.2 |

232.8 |

230.4 |

228.0 |

225.6 |

223.2 |

220.8 |

218.4 |

216.0 |

|

3. Potatoes, fresh & chilled |

27 |

139.0 |

137.6 |

136.2 |

134.8 |

133.4 |

132.0 |

130.6 |

129.2 |

127.8 |

126.4 |

125.0 |

|

4. Onions, shallots, fresh & chilled |

27 |

158.0 |

156.4 |

154.8 |

153.2 |

151.6 |

150.0 |

148.4 |

146.8 |

145.2 |

143.6 |

142.0 |

|

5. Garlic, fresh or chilled |

27 |

63.0 |

62.4 |

61.8 |

61.2 |

60.0 |

60.0 |

59.4 |

58.8 |

58.2 |

57.6 |

57.0 |

|

6. Coconut, fresh & dried |

20 |

60.0 |

59.4 |

58.8 |

58.2 |

57.6 |

57.0 |

56.4 |

55.8 |

55.2 |

54.6 |

54.0 |

|

7. Copra |

20 |

40.0 |

39.6 |

39.2 |

38.8 |

38.4 |

38.0 |

37.6 |

37.2 |

36.8 |

36.4 |

36.0 |

|

8. Coffee, coffee husks & skins |

30 |

100 |

99.0 |

98.0 |

97.0 |

96.0 |

95.0 |

94.0 |

93.0 |

92.0 |

91.0 |

90.0 |

|

9. Tea |

30 |

100 |

99.0 |

98.0 |

97.0 |

96.0 |

95.0 |

94.0 |

93.0 |

92.0 |

91.0 |

90.0 |

|

10. Pepper, dried |

27 |

57.0 |

56.4 |

55.8 |

55.2 |

54.6 |

54.0 |

53.4 |

52.8 |

52.2 |

51.6 |

51.0 |

|

11. Maize |

20 |

81.0 |

80.2 |

79.4 |

78.6 |

77.8 |

77.0 |

76.2 |

75.4 |

74.6 |

73.8 |

73.0 |

|

12. Rice, including paddy, broken |

30 |

58.0 |

57.4 |

56.8 |

56.2 |

55.6 |

55.0 |

54.4 |

53.8 |

53.2 |

52.6 |

52.0 |

|

13. Soya bean, edible & inedible |

20 |

89.0 |

88.1 |

87.2 |

86.3 |

85.4 |

84.5 |

83.6 |

82.7 |

81.8 |

80.9 |

80.0 |

|

14. Onion seeds |

30 |

242.0 |

239.6 |

237.2 |

234.8 |

232.4 |

230.0 |

227.6 |

225.2 |

222.8 |

220.4 |

218.0 |

|

15. Soyabean oil & its fractions |

20 |

162.0 |

160.4 |

158.8 |

157.2 |

155.6 |

154.0 |

152.4 |

150.8 |

149.2 |

147.6 |

146.0 |

|

16. Palm oil & its fractions |

20 |

159.0 |

157.4 |

155.8 |

154.2 |

152.6 |

151.0 |

149.4 |

147.8 |

146.2 |

144.6 |

143.0 |

|

17. Coconumt oil & its fractions |

20 |

58.0 |

57.4 |

56.8 |

56.2 |

55.6 |

55.0 |

54.4 |

53.8 |

53.2 |

52.6 |

52.0 |

|

18. Cane or beet sugar |

65 |

104.0 |

103.0 |

102.0 |

101.0 |

100.0 |

99.0 |

98.0 |

97.0 |

96.0 |

95.0 |

94.0 |

|

19. Instant coffee & other extracts |

40 |

55.0 |

54.4 |

53.8 |

53.2 |

52.6 |

52.0 |

51.4 |

50.8 |

50.2 |

49.6 |

49.0 |

|

20. Soyabean cake |

20 |

148.0 |

146.5 |

145.0 |

134.5 |

142.0 |

140.5 |

139.0 |

137.5 |

136.0 |

134.5 |

133.0 |

|

21. Non-manufactured tobacco |

60 |

80.0 |

79.2 |

78.4 |

77.6 |

76.8 |

76.0 |

75.2 |

74.4 |

73.6 |

72.8 |

72.0 |

|

22. Raw silk |

30 |

257.0 |

253.9 |

250.8 |

247.7 |

244.6 |

241.5 |

238.4 |

235.3 |

232.2 |

229.1 |

226.0 |

|

23. Longans, dried |

30 |

59.0 |

58.4 |

57.8 |

57.2 |

56.6 |

56.0 |

55.4 |

54.8 |

54.2 |

53.6 |

53.0 |

Source: Ministry of Commerce

Despite the reduction in average tariff, the average applied tariff rate is still higher than most countries in Asia because there are a large number of tariff peaks in agriculture. About three quarters of tariffs exceeding 50% are in agriculture. Although the applied tariff rates on some agri-food products (particularly those in the meat, dairy and animal products) are very high, the bound rates, which are relevant to imports from WTO members, are much lower.

Thailand has tariffied all of the import quotas for 23 agricultural product groups into the tariff quotas (see Table 1.2) Out of the 23 product groups, 5 groups are either the products in the livestock sector or inputs used for livestock production. Although Thailand has failed to fill the import quotas of 14-15 products, the administration of tariff quotas does not appear to constitute a significant barrier to trade (WTO, 2000). The 23 tariff quotas can be divided into 3 groups. The first group comprises a number of traditional export commodities in which Thailand has strong comparative advantage and hence no need for import protection. They are, for example, rice, sugar, maize, coffee, longan, and coconut. The second group consists of import competing products which are required in large quantities by the agro processing industry, i.e., oil seeds, maize and concentrated milk. The actual imports of these products have exceeded the committed quotas by several times, except in a few years where there are abundant domestic supplies. Moreover, the applied in quota tariffs are also lower than the bound rates. The third groups are also import-competing products which have too small amount of quotas (subject to the low in quota tariffs) to be profitably imported. They are, for example, garlic, coconut oil, and milk. But it is also possible that the Public Warehouse Organization, which is given the sole responsibility for the import of certain quantities of products under the tariff quota, may not be able to profitably carry out its responsibility. It should also be noted some of the products with no imports are actually smuggled through the border. They are onion and garlic.

Although the tariff quota system does not result in significant trade barrier, the administration of quota allocation has always in favor of the large agro processing companies and the producer associations dominated by large - scale processing companies and large-scale commercial farms. As a result, the industrial structure has been affected since it is difficult for the new entrant to break into the markets, which are already dominated by a few oligopolists. In addition to tariff reduction and TRQ, the UR agreement also contains an agreement on trade related investment measures (TRIMS). Thailand used to impose the local requirements (LCR) on the production of a number of agricultural products, e.g., soybean oil, milk and silk. By 2000, only the importers of dairy products are subject to the LCR policy, which requires the importers of skim milk powder in local raw milk. In the case of prepared milk, the LCR is 2 to 1. Thailand was due to abolish the LCR for milk by the end of 1999. But the government has to request the CTG for an approval of an extension of the milk LCR policy until the end of 2003. The waiver is needed as the dairy farmers pressured the government.

b) Domestic Support: Thailand is one of a few developing countries that have notified large amount of trade-distorted domestic support (see Table 1.3). It has committed to reduce the Amber Box domestic support from 21,816 baht million in 1995 to 19,028 baht million in 2004. In addition to the Green Box support, Thailand is also allowed to provide product-specific support under the de minimis measures and support under the special and differential treatment measures which are exempt from the reduction commitment.

Table 1-3 Monetary value of distorting and non-distorting measures 1995 - 2004 and actual AMS 1995 - 1999

Unit: million Baht

|

Year |

Monetary value of measure commit to reduce1 |

Monetary value of measure exempt from the reduction commitment |

||||

|

Bound |

actual AMS |

Actual as a percentage of bound |

Green box2 |

subsidy on input of production 3 |

subsidy on investment4 |

|

|

(1) |

(2) |

(1) / (2) |

||||

|

1995 |

21,816.41 |

15,773.25 |

72.3 |

33,594.33 |

4,310.38 |

1,051.51 |

|

1996 |

21,506.64 |

12,932.47 |

60.1 |

41,145.31 |

9,323.35 |

2,893.96 |

|

1997 |

21,196.87 |

16,756.58 |

79.1 |

47,595.87 |

4,999.69 |

1,902.23 |

|

1998 |

20,887.10 |

16,402.10 |

78.5 |

42,826.82 |

4,600.43 |

529.28 |

|

19995 |

20,577.33 |

17,303.37 |

84.1 |

35,948.93 |

3,058.70 |

78.22 |

|

2000 |

20,267.56 |

(20,846.08)6 |

(100.0) |

- |

- |

- |

|

2001 |

19,957.79 |

N.A. |

(>100%)7 |

- |

- |

- |

|

2002 |

19,648.02 |

N.A. |

- |

- |

- |

- |

|

2003 |

19,338.25 |

N.A. |

- |

- |

- |

- |

|

2004 |

19,028.48 |

N.A. |

- |

- |

- |

- |

Source: Department of Business Economic, Ministry of Commerce

Notes:

1. This category refers to distorting measurements of support, such as price support, price intervention, etc.

2. This category refers to non-distorting measurements of support, such as subsidy on environmental conservation, research and development, establishing infrastructure, production restructuring, and rural development, etc.

3. This category refers to the special and differential treatment allowable for developing countries to provide input of production, such as the measure of financing on cheap seeds and fertilizer, etc.

4. This category refers to the special and differential treatment allowable for developing countries to encourage investment, such as the measure of financing on cheap machinery and appliances, etc.

5. The figure is a preliminary data.

6. Estimated by the author from the Farmer Assistance Fund (Bht 5,189.1 billion), BAAC (Bht 9,872.96 billion) and BOT (Bht 5,784.01). The number is still and overestimate.

7. Available data suggest that actual support might be much larger than the committed support. The proposed budget was Bht 5.2 billion from BOT, Bht 6.18 billion from FAF and Bht 19.96 billion from BAAC.

Tables 1.3 provides the committed and actual support between 1995 and 2001. The actual Amber Box support has steadily increased from 72% of the committed support in 1995 to more or less 100% in 2000. Although there is not yet complete information in 2001, it is believed that the actual support may exceed 100%. This is mainly because of the big jump in expenses for the rice price support program. In addition, Thailand also provide trade distorting subsidy under the de minimis category which jumped from 1,012 baht million in 1995 to 2,342 baht million in 1999.

The livestock sector receives very small amount of total trade distorting subsidy, most of which are in the de minimis category. The products that receive de minimis support are hen eggs, duck eggs, and swine, maize and soya beans. However, the subsidies for those products are only provided in the years of very low prices when there are farmers’ protests or requests.

Export Subsidy: Thailand has notified no export subsidy. However, the government has provided some exempt export subsidies in accordance with the AoA in some years. The subsidies are given only to certain products, particularly rice, in a form of packing credit facility, which are loans, provided to exporters at below-market interest rates. There are also Exim Bank’s credits, which finance the export of rice and other agricultural products.

Livestock Export: This paper will only discuss the performance of livestock trade after the UR agreement. The performance of the agricultural trade is beyond the scope of this paper and can be found in Poapongsakorn, et.al. 2002.

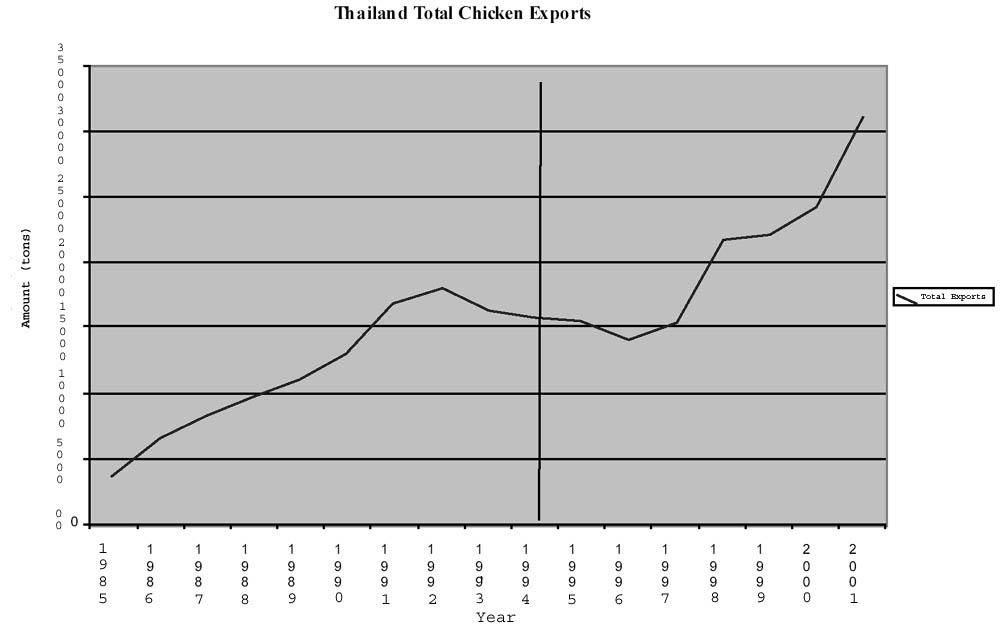

Thailand is one of the major exporters of frozen chicken, thank to the role of the agro-business companies which imported modern technology of chicken raising in the late 1970’s. Chicken exports jumped rapidly from about 40,000 tons in 1985 to almost 180,000 tons in 1992 and then declined to about 150,000 tons in the 1993-97 period. After that it surged rapidly to 220,000 tons in 1998 and jumped again from 245,000 tons in 2000 to more than 300,000 tons in 2001 (see Figure 1.1). Most of the chicken exports goes to Japan. But after 1997, exports to EU have surged rapidly.

Figure 1-1 Thailand’s total chicken exports

Although Thai exporters of chicken should have benefited from increased market access committed by the WTO members, the market access is not the major factor behind the sharp increase in Thai chicken export after 1997. It is true that after the UR Agreement, chicken export to the EU began to increase because Thailand receives export quotas from the EU as part of the compensation for the EU’s oil seeds policy. However, the major markets for Thai chicken exports are still Japan and the Asian market. But total chicken exports did not jump until 1998 after Thailand was badly hit by the financial crisis, which started in July 1997. As a result, the baht was floated and depreciated sharply by more than 40 percent since 1997. As a result, Thai chicken has become more competitive. Moreover, the BSE disease, which hit Europe in 1996 and 2001, has also significantly boosted the exports of Thai chicken to Europe. The flu disease which hit the Chinese chicken industry also helped increase Thai exports to Hong Kong and Japan because both countries import large amount of chicken from China.

Thailand is also the largest exporter of cassava pellets and chips. More than 90% of the export go to EU under the bilateral voluntary export restrain agreement between Thailand and EU. But before the UR conclusion, the EU launched a reform of its Common Agricultural Policy (CAP) in order to reduce the subsidy and the domestic prices of agricultural products. After the reform, the bilateral agreement with Thailand was built into the UR agreement on tariff quota system. Since the CAP reform has resulted in lower prices of cereals, which are raw materials for animal feeds, the demand for Thai cassava pellets has declined significantly. Total exports of cassava pellets to EU have always been less than the 5.25 million ton quotas. Changes in exports will depend on the relative prices of wheat and soybeans, and the exchange rate between the baht and the Euro.

Thai agricultural exports, particularly chicken, have also been subject to complaints and detention by the importing countries that they do not meet the SPS requirements. It is true that the SPS problems faced by some Thai exporters are caused by the below-standard process of production. For example, there are cases in which the importing countries allow imports from Thailand after the problems have been solved, e.g. the problem of URE in frozen chicken export to the Czech Republic (Chulalongkorn University 2001). But there are also doubtful cases of SPS measures imposed by some importing countries. The EU imposes an unrealistic regulation on imported cut-up chicken. The regulation stipulates that the temperature of the meat being cut up must be lower than 4-degree celcius. The Australian government had also delayed in disclosing a report on imported chicken for some years. When bacteria was found in Thai frozen chicken, the Korean officials did not specify the details of the infection. Finally, the Philippines government sent officials to inspect the Thai exporting slaughterhouses in 1998 but has not yet disclosed its report and a decision.

These two cases show that Thailand has not reaped export benefits from the market access committed by the WTO members. Poapongsakorn, et.al. (2002) also shows that Thailand has not been able to exploit the full benefits from the market access granted by the WTO members for Thailand’s major exports of rice and sugar.

Thailand’s exports of oilseeds and their products (e.g., soya beans) are minimal, depending on their surplus supplies in some good years. Egg exports are also very negligible, although Thailand has begun to export egg powder products for almost ten years.

Imports of Dairy Products, Oilseeds and Maize Dairy products, particularly skim milk powder, are major import item, which totaled 64,360 tons in 2001. The actual imports have always exceeded the tariff quota volume, and the applied tariff of 5% is much lower than the bound rate of 20% (see Table 1.2 and 1.4). Despite such large amount of import, some WTO members have complained about the delay in official approval of import.

Table 1-4 Tariff Quota and Tariff rate of Skim milk powder

|

Year |

Skim Milk Powder (Tons) |

Skim Milk Powder Tariff rate (%) |

||||

|

WTO |

Market |

Actual |

In Quota |

Out Quota |

Actual |

|

|

1995 |

45,000 |

55,000 |

55,000 |

20 |

237.6 |

5.00 |

|

1996 |

46,111 |

88,000 |

87,891 |

20 |

235.2 |

5.00 |

|

1997 |

47,222 |

88,000 |

88,000 |

20 |

232.8 |

5.00 |

|

1998 |

48,333 |

88,000 |

78,000 |

20 |

230.4 |

5.00 |

|

1999 |

49,444 |

68,500 |

54,951 |

20 |

228.0 |

5.00 |

|

2000 |

50,556 |

55,600 |

57,117 |

20 |

225.6 |

5.00 |

|

2001 |

51,667 |

65,000 |

64,360 |

20 |

223.2 |

5.00 |

Source: Department of Foreign Trade, Ministry of Commerce

The quota of skim milk powder distributed to the group of five manufacturers (see Table 1.5). These are 1) flavored milk producer 2) the condensed milk producer 3) the other dairy product producer 4) trade company and 5) the exporter company. But in 1995, there are 3 groups; namely, 1) a company; have imported skim milk powder before 2) Dairy Farming Promotion Organization of Thailand and 3) a company; condensed milk. In addition, milk entrepreneurs also imported whole milk powder for the production. The import quotas of whole milk powder were neither limited nor bound to the WTO agreements and it was taxed on the same rate as skimmed milk powder, i.e., and 5 percent. This led to an excess supply of raw milk in 2000 which prompted the government to raise the import tax to 18 percent and pumped in the budget to finance milk in school milk project in order to reduce the excess supply (see Table 1.5)

A second tariff quota is non-concentrated milk and cream. There has been no import of the item since 1995, suggesting that the 20% applied in-quota tariff is prohibitive. It is also more profitable to import milk in concentrated form than in liquid form.

Table 1-5 Quota Allocation of Skim milk powder by group, 1998-2001

|

Year |

Quota quantity allocated (tons) |

Total |

||||

|

Group 1 |

Group 2 |

Group 3 |

Group 4 |

Group 5 |

||

|

1995 |

8,217 |

25,000 |

21,783 |

- |

- |

55,000 |

|

1996 |

35,200 |

32,590 |

14,416 |

5,685 |

- |

87,891 |

|

1997 |

32,800 |

34,800 |

14,700 |

5,700 |

- |

88,000 |

|

1998 |

26,940 |

31,740 |

14,000 |

5,320 |

- |

78,000 |

|

1999 |

14,035 |

27,096 |

10,430 |

3,390 |

- |

54,951 |

|

2000 |

10,849 |

27,589 |

16,830 |

1,850 |

- |

57,117 |

|

2001 |

11,663 |

19,938 |

18,000 |

2,770 |

11,989 |

64,360 |

Source: Department of Foreign Trade, Ministry of Commerce

Despite the LCR policy, Thailand still has to import large amount of skim milk. This means that the demand for milk has increased rapidly as the result of higher income and policy to promote milk consumption in school. Although milk production has also increased at the annual rate of almost 10%, the supply of raw milk is still not enough to meet demand. The phase out of the LCR policy, therefore, will not be expected to seriously disrupt the domestic production because skim milk is not the good substitute for whole milk. However, the world price of milk is still highly distorted by the heavy subsidy in EU. Unless such subsidy is not substantially reduced, Thailand will need to maintain high import tariff to protect the poor dairy farmers who will have difficulty in adjusting to the lower milk prices after the abolition of the LCR policy.

Thailand has also had to import large amount of soybeans, soybean cake and maize as it s livestock sector has been growing rapidly both in response to the larger domestic market and the expanding export markets. Although Thailand may have comparative advantage in maize production, as she used to export maize, the total production has fell short of the higher demand from the animal feed industry in the recent years. In case of soybeans and soybean cake, Thailand does not have much comparative advantage. Despite decades of aggressive promotion and protection, average yield per hectare of soya beans is still disappointingly low and there is serious problem of alfa tax in. Therefore, the government should abolish the tariff quotas for soyabeans, soybean cake and maize and impose as low tariff as possible. Such policy will help maintain the competitiveness of the livestock industry.

As mentioned above, applied tariffs on imports of fresh, chilled, or frozen meat and duck are higher than the WTO bound rates. Moreover, since 1995 tariffs have also been substantially reduced on meat preparation. Therefore, imports of meat and ducks have increased in the recent years.

Table 1-6 Tariff Quota of Maize, Soya bean, Soya bean cake and skim milk powder 1995-2002

|

Year |

Maize (tons) |

Soya bean (tons) |

Soya bean cake (tons) |

Skim Milk Powder (tons) |

||||

|

Bound |

Actual import |

Bound |

Actual import |

Bound |

Actual import |

Bound |

Actual import |

|

|

1995 |

52,096 |

383,209 |

10,402 |

278,934 |

219,580 |

648,035 |

45,000 |

55,000 |

|

1996 |

52,385 |

299,756 |

10,460 |

422,625 |

220,800 |

799,990 |

46,111 |

87,891 |

|

1997 |

52,675 |

194,116 |

10,518 |

655,013 |

222,020 |

916,223 |

47,222 |

88,000 |

|

1998 |

52,964 |

265,789 |

10,575 |

744,049 |

223,240 |

1,070,827 |

48,333 |

78,000 |

|

1999 |

53,253 |

51,528 |

10,633 |

1,264,799 |

224,460 |

1,382,196 |

49,444 |

54,951 |

|

2000 |

53,543 |

50,689 |

10,691 |

1,370,481 |

225,679 |

1,309,869 |

50,556 |

57,117 |

|

2001 |

53,832 |

na |

10,749 |

na |

226,899 |

na |

51,667 |

289,315 |

|

2002 |

54,121 |

na |

10,806 |

na |

228,119 |

na |

52,778 |

64,360 |

Source: Department of Foreign Trade, Ministry of Commerce

Note: Thailand abolished the quota system for soya bean on 1 November 1996

During the past two decades, broiler chicken has become the star of Thai livestock exports. Thailand has just begun to export broilers just over two decades ago and has become one of the leading exporters worldwide. At one point, the amount exported was more than the amount consumed domestically. Last year, Thailand became the fourth largest broiler exporter after the US, Brazil, and slightly behind China.

Broiler chicken has been the most revolutionized livestock sector in Thailand. The success of the broiler revolution is the key that has kept its price down. Three or four decades ago, chicken prices were on par with, or sometimes higher than, pork and fish prices. At present, however, chicken is the least expensive source of protein and Thailand is now a leading broiler exporter. Broiler development has been largely undertaken by the private sector, with little intervention or assistance from the Thai government. In fact, it is arguably the case that the government has impeded its growth by protecting the soybean industry. Unlike cattle, broiler chickens sold today are much smaller in size than in the past. However, the raising period has also been shortened substantially to around 40 days. At the same time, the feed conversion ratio has improved substantially.

One major change in raising broilers in the 1990’s is housing. The evaporative cooling house (“evap house”) - a semi-automatic housing which uses large fans and water to cool down the housing that holds more than 10,000 chickens to 28 degree Celsius or less during the hot season in a tropical country like Thailand - has been attributable to the industry’s cost saving. The evap house could save labor and housing costs. More importantly, it increases growth and survival rates substantially. Many private firms claim that, technology-wise, Thailand’s broiler industry could compete with anyone in the world.[140] According to them, the disadvantage of the Thai broiler industry today is largely due to the government’s policy to protect soybean farmers that has caused the feed prices to be artificially high.

One major disadvantage that has hampered the competitiveness of the broiler industry is feed prices. Thailand is a country where farmers are still the majority of population[141] and the notion of “farmers” in Thailand usually refers to small crop farmers rather than livestock “business”. Therefore, in the last two decades, the MOAC (and, to some extent, the Ministry of Commerce, MOC) has taken pains to protect soybean and maize farmers, resulting in high prices of major animal feeds in Thailand. That Thailand has become a leading broiler exporter was the result of her cheap labor in the past and decades of experience of her major exporters, some of which become transnational corporations that invest not only in Asia but also in the US livestock industry.

Table 2-1 Cost of Raising Broiler in Major Exporting Countries

|

|

Cost (Baht/Kg.) |

|

Brazil |

14.06 |

|

USA |

15.96 |

|

Thailand |

21.66 |

Source: Computed based on US Broiler Performance Data (cited in Jiros, 2002)

Because Thailand’s advantage used to lie on her cheap labor and not on feed price, the types of Thai broiler exports that were most competitive in the past were boneless chicken, which is more labor intensive than boned chicken. This advantage began to cease since the wage rate in Thailand had risen substantially in the 1990’s (up until the financial crisis in 1997) and other Asian countries with cheaper labor costs - especially China and Vietnam--began to catch up on broiler export. Moreover, Thailand began to lose another past advantage, i.e., proximity to Japan, to China, who has become a more increasingly important broiler exporter to Japan in recent years.

As Thailand’s wage rate of unskilled labor soared in the 1990’s, the industry began to realize that it could no longer rely on cheap labor. As a result, some exporters have transformed their broiler export from frozen boneless chickens to processed or precooked chicken (usually in ready-to-reheat or ready-to-eat form). Processed and precooked chicken has become an important part of broiler export and has continued to grow steadily since 1991. In 2000, Thailand export about 69,329 tons of processed chicken, approximately 22.5 percent of the export quantity (see Table 2.2). However, it accounts for 36 percent of the export value (see Table 2.3). Processed chicken, therefore, have become the future of the Thai broiler export, where more emphasis would be placed on value added rather than export quantity or market share.

Table 2-2 Broiler Export Quantity, 1994-1999 (ton)

|

Year |

Frozen Broiler |

Precooked Broiler |

Total Broiler |

|

1994 |

152,903 |

15,996 |

168,899 |

|

1995 |

149,935 |

22,124 |

172,059 |

|

1996 |

137,215 |

31,555 |

168,770 |

|

1997 |

151,120 |

41,641 |

192,761 |

|

1998 |

212,479 |

62,336 |

274,815 |

|

1999 |

217,735 |

47,496 |

265,231 |

|

2000 |

240,905 |

69,329 |

310,234 |

|

2001f |

260,000 |

80,000 |

340,000 |

|

Average Annual Growth Rate 1994-1996 (%) |

-5.3 |

40.3 |

-0.0 |

|

Average Annual Growth Rate 1996-1998 (%) |

26.8 |

39.0 |

29.2 |

|

Average Annual Growth Rate 1998-2000 (%) |

6.5 |

5.5 |

6.2 |

|

Average Annual Growth Rate 1996-2000 (%) |

15.1 |

21.7 |

16.4 |

Source: Department of Business Economics, MOC and Thai Broiler Processing Export Association

Table 2-3 Broiler Export Value, 1994-1999 (million baht)

|

Year |

Frozen Broiler |

Precooked Broiler |

Total Broiler |

|

1994 |

9,846 |

1,850 |

11,696 |

|

1995 |

9,662 |

3,088 |

12,750 |

|

1996 |

9,085 |

3,372 |

12,457 |

|

1997 |

10,951 |

4,951 |

15,902 |

|

1998 |

16,639 |

8,655 |

25,294 |

|

1999 |

15,260 |

5,936 |

21,196 |

|

2000 |

15,689 |

8,750 |

24,439 |

|

Average Annual Growth Rate 1994-1996 (%) |

-4.0 |

35.0 |

3.2 |

|

Average Annual Growth Rate 1996-1998 (%) |

26.8 |

39.0 |

29.2 |

|

Average Annual Growth Rate 1998-2000 (%) |

-2.9 |

0.5 |

-1.7 |

|

Average Annual Growth Rate 1996-2000 (%) |

14.6 |

26.9 |

18.3 |

Source: Department of Business Economics, MOC and Thai Broiler Processing Export Association

Table 2-4 Background of broiler industry in Thailand

|

|

1998 |

1999 |

2000 |

2001(p) |

2002(f) |

|

Number of chicken raised (million birds) |

780 |

855 |

884 |

958 |

978 |

|

Production (‘000 tons) |

883 |

968 |

1,070 |

1,205 |

1,290 |

|

Consumption (‘000 tons) |

609 |

694 |

737 |

785 |

830 |

|

Export (‘000 tons) |

275 |

274 |

333 |

420 |

460 |

|

Export growth (%) |

42.0 |

0.0 |

21.5 |

26.1 |

9.5 |

|

Share of Export (%) |

31.1 |

28.3 |

31.1 |

34.9 |

35.7 |

Source: Thai Broiler Processing Export Association

Table 2-5 Broiler export in 2001

|

Destination |

Quantity (ton) |

Share (%) |

% Growth from 2000 |

|

Japan |

218,400 |

52 |

22 |

|

EU |

151,200 |

36 |

44 |

|

Other countries |

50,400 |

12 |

3 |

|

Total |

420,000 |

100 |

26 |

Source: Thai Broiler Processing Export Association

Note: preliminary data

There are also other two major trends that have affected the future of Thai broiler export, and possibly the way broilers are raised. First, consumers in developed countries have given more recognition on animal welfare. At present, the European Union (EU) has taken this issue on both broilers and layers. Many Thai exporters view the measure as protectionism. However, since the EU has been Thailand’s most important export market for broilers, major Thai exporters tried to comply with those standards. Many large-scale firms are rather optimistic, since they believe that Thailand is in a better position to follow these guidelines than a major competitor like the US. Many also push the Department of Livestock Development (DLD), Ministry of Agriculture, to set farm standards that would comply with the EU’s White Paper on Food Safety and Directives on Animal Welfare. Consequently the DLD has announced the “Farm Standard”--based on the EU standard, which would become compulsory for all exporting broiler farms in October 2002. In addition, some veterinarians have pointed out that following animal welfare guidelines has resulted in an increase in survival and growth rate and hence productivity rather than decreasing efficiency as many have feared.

The second trend is the emerging market of antibiotic-free broilers - especially in Japan. The Japanese importers used to pay about 20% premium for the antibiotic-free broilers, which is sufficiently high to cover the increased costs. However, as more broiler farms in Thailand are capable of raising and exporting antibiotic-free broilers, the premium appears to decrease. The EU does not require antibiotic-free broilers. However, it requires that the growers stop using antibiotics and vaccines for a certain period before slaughter.[142] Both countries’ more stringent demand has resulted in better farm management that have led to a reduction of antibiotic use in the broiler industry.

“Farm to table” is another measure on trace-ability that has transformed the Thai broiler industry. Since most large scale farms rely heavily on export, this effective tracking scheme forces them to comply with the export standard to avoid heavy punishment if they fail to comply.

As for the domestic market, the success of the broiler industry in keeping chicken prices down has contributed to a continual increase in chicken consumption in Thailand. Domestic per-capita broiler consumption has increased gradually from 3.5kg per annum in 1973 to around 12kg per annum in 1997. Per capita consumption had decreased slightly after the financial crisis, but has since rebounded to the 12 kg per annum in the year 2000 (Table 2.6).

Table 2-6 Per Capita Chicken Consumption, 1973-2001 (Kg./year)

|

Year |

Per capita consumption (Kg./year) |

|

1973 |

3.5 |

|

1977 |

4.0 |

|

1981 |

5.0 |

|

1982 |

5.5 |

|

1987 |

7.0 |

|

1990 |

7.8 |

|

1991 |

8.2 |

|

1992 |

8.2 |

|

1993 |

8.7 |

|

1994 |

9.2 |

|

1995 |

10.3 |

|

1996 |

11.2 |

|

1997 |

11.8 |

|

1998 |

10.8 |

|

1999 |

11.5 |

|

2000 |

11.8 |

|

2001 |

12.6(p) |

Source: Thai Broiler Processing Export Association

In the past, stringent export standards have led to a dual standard system where the domestic market is flooded by lower quality chicken (including chicken with more residuals such as antibiotics). Since, however, the majority of export now is not the whole bird but of certain parts (e.g., white breast to the EU and tight to the Japan), the rest of the chicken sold in the supermarket are more likely to be of the same export standard. More importantly, technological changes induced by export demand have spilled over to the rest of the industry because of its superiority in terms of efficiency.

Technological changes in the past two decades could be summarized in three interrelated areas, namely, breeding stocks, housing, and farm management. Together these have improved efficiency substantially, via decreasing raising day per crop and feed conversion ratio.

Table 2-7 Changes in day required in raising chicken 1983-2001

|

Year |

Days required to raise chicken |

||

|

Size 1.5 kilogram |

Size 1.8 kilogram |

Size 2.4 kilogram |

|

|

1983 |

|

56 |

|

|

1989 |

|

49 |

|

|

1994 |

|

45 |

|

|

2001 |

30 |

38 |

50 |

Source: Personal correspondence with Dr. Kitti Supchusakul

Breeding stock improvement has been crucial. However, Thailand, like most other countries, has to rely on foreign know-how (although CP, a Thailand-based MNC, owns a share of Arbor Acres and use to own the Avian brand solely). At present, grandparent stocks are solely imported and domestic improvements are unlikely in the foreseeable horizon.

Evaporative housing has accounted for productivity improvement (see Table 2.8) and as a result, it has become standard housing in the commercial broiler farms. At present, the import content is still high, although there are an increasing number of modified models of evaporative housing that substitutes some expensive equipment with local equipment, which are more cost-effective.[143]

Table 2-8 Feed Conversion Ratio in Broiler Production

|

|

Feed Conversion Ratio |

|

1980 |

2.2 |

|

1990 (before Evap Housings) |

1.9 |

|

2002 Present |

1.75 |

Source: Personal correspondence with Dr. Kitti Supchusakul

For farm management, although most of the know-how comes from abroad, the main pecuniary elements are animal drugs and vaccines. These elements are of concern, both in terms of cost and food safety. It turns out, however, that the solutions also come from abroad. As the requirements on food safety are more stringent over time, farms are required to rely more on non-chemical solutions and less on drugs and vaccines. In this respect, the broiler sector, which is highly dependent on the export market, has moved in the right direction. At present, drugs and vaccines account for about 4-5% of the cost (1.8 Baht per broiler). This is still substantially higher than in the US (about 1%). However, the figure is much better than in the past and far better than in other non-tradable livestock in Thailand, specifically in the swine industry.

One management technique is all-in-all-out system where chickens from every housing within a farm would be brought in or out in a short window period. This technique helps reduce the chance of disease outbreak greatly. It should be noted that in order to use this technique, each major buyer/contractor would have to have large market and own, or have contracts with, several farms so that it would be able to deliver broilers on a continuous basis.

As most of the new technologies are imported, they have replaced most of the domestic or indigenous ones. There are nearly three million farmers who raise chickens in their backyards as a supplement product, mostly for household consumption. As for the commercial broiler farms, concentration has been increasingly immense as the top 14 players now account for about 80% of broiler production.

Unfortunately, the data on farm sizes and their distribution are rather shaky. Table 2.9 shows figures from the 1993 agricultural census and the 1998 intercensus survey. The way the data were reported could not distinguish broiler farms from layers farms or native chicken farms. According to these figures, the total number of farm holdings who raise chickens had increased between 1993-1998. However, the number of farm sizes of 500-999 and 10,000 birds and over had decreased.

Table 2-9 Distribution of Farm Size (from 1993 Agricultural Census and 1998 Intercensal Survey)

|

Chicken farm size distribution in 1993 (data from the 1993 Agricultural Census) |

|||||

|

Number of Chickens in holding |

Number of Chickens |

||||

|

Holdings |

Layers |

Broiler |

Native |

Total |

|

|

Total |

2,617,412 |

23,652,272 |

85,732,946 |

45,536,712 |

154,921,930 |

|

1 - 19 |

1,681,300 |

145,222 |

228,319 |

13,797,401 |

14,170,942 |

|

20 - 99 |

863,809 |

368,816 |

494,451 |

25,338,318 |

26,201,585 |

|

100 - 499 |

53,064 |

860,693 |

937,310 |

5,637,994 |

7,435,997 |

|

500 - 999 |

3,861 |

768,119 |

925,821 |

686,542 |

2,380,482 |

|

1,000 - 9,999 |

13,042 |

7,343,599 |

37,685,107 |

71,381 |

45,100,087 |

|

10,000 and over |

2,336 |

14,165,823 |

45,461,938 |

5,076 |

59,632,837 |

|

Chicken Farm Size Distribution in 1998 (Data from the 1998 Intercensal Survey) |

|||||

|

Number of Chickens in holding |

Number of Chickens |

||||

|

Holdings |

Layers |

Broiler |

Native |

Total |

|

|

Total |

3,174,410 |

33,830,791 |

78,103,454 |

57,168,254 |

169,102,499 |

|

1 - 19 |

1,947,507 |

190,478 |

218,401 |

16,753,480 |

17,162,359 |

|

20 - 99 |

1,145,746 |

604,529 |

632,623 |

32,835,685 |

34,072,837 |

|

100 - 499 |

63,262 |

514,985 |

895,493 |

6,984,260 |

8,394,738 |

|

500 - 999 |

2,562 |

538,982 |

609,656 |

540,112 |

1,688,750 |

|

1,000 - 9,999 |

13,275 |

10,735,346 |

41,909,323 |

47,339 |

52,692,008 |

|

10,000 and over |

2,058 |

21,246,471 |

33,837,958 |

7,378 |

55,091,807 |

Source: MOAC, 1993 Agricultural Census and 1998 Intercensal Survey of Agricultural Change

The other main source of data on farm size is the DLD which gathers information from its provincial offices throughout the country. Table 2.9 shows the distribution of broiler farm size in 1995 and 1999, according to the DLD. Although the figures are from the same source (DLD), the categories are not the same for both years. Furthermore, the farm size intervals are probably too crude for present standards, as there is no classification of farm size over 10,000 birds.

Table 2-10 Broiler Commercial Farm Size by Region, 1995 and 1999

| |

Farm Size Distribution 1995 |

|||||

|

500-2,000 |

2,001-5,000 |

5,001-10,000 |

10,000+ |

Total |

||

|

Central |

358 |

883 |

527 |

300 |

2,068 |

|

|

North |

18 |

48 |

51 |

15 |

132 |

|

|

Northeast |

41 |

239 |

161 |

32 |

473 |

|

|

South |

186 |

83 |

18 |

10 |

297 |

|

|

Whole Country |

603 |

1,253 |

757 |

357 |

2,970 |

|

|

Avg. farm size in group |

1,375 |

3,954 |

7,685 |

43,590 |

|

|

| |

Farm Size Distribution 1999 |

|||||

|

50-1,000 |

1,001-2,000 |

2,001-5,000 |

5000+ |

Total |

||

|

Central |

773 |

652 |

2,438 |

1,792 |

5,655 |

|

|

North |

128 |

80 |

483 |

312 |

1,003 |

|

|

Northeast |

127 |

101 |

970 |

540 |

1,738 |

|

|

South |

162 |

299 |

563 |

251 |

1,275 |

|

|

Whole Country |

1,190 |

1,132 |

4,454 |

2,895 |

9,671 |

|

Source: DLD

Based on Table 2.10, the number of farms of every size has increased substantially between 1995 and 1999. A recent press release by the DLD in February 2002 stated that the number of exportable broiler farms was then 17,037, also a huge increase from the DLD’s 2001 figure (15,036 farms) and almost twice the 1999 figure. My reservation on these figures is that the low-level officials in the DLD might find it compelling to report continual increasing number of farms in every size, since they believe that their performance would be evaluated based on these figures.

Even when the official figures indicate that the number of small broiler farms continue to increase, most experts in the field agree that, as the commercial sector become more and more industrialized, small farms are going out of the business. At present, the farm sizes considered “too small” to compete in this industry are the ones with 50,000 birds or less. In most cases, the owners of these farms are middle class businessmen rather than traditional farmers. Although there has been no systematic survey on how these outgoing firms doing after leaving the business, people in the business I have interviewed informally believe that these businessmen simply switch to other business - mainly agro-business, with various level of successes (and failures) in their new businesses.

The layer industry is much smaller than broilers. During the last 5 years, the stock of hen layers is in the range of 41-42 million (including approximately 10 million chicks), compared to approximately 100 million of broiler stock. Total egg production is approximately 8-9 billion annually. During the last five years, more than 99 percent of hen eggs were consumed domestically. The remaining, which is generally less than or around one percent, is exported (see Table 2.11). Most of exported eggs go to Hong Kong, the Middle East, and to a lesser extent, Japan.[144] The export venue is use to dump surplus eggs abroad to stabilize the domestic price. Usually the export prices of eggs are considerably less than domestic prices.

Table 2-11 Number of Hens, Hen Egg Production, Export, and Per Capita Consumption, 1989-2001.

|

Year |

Number of Layers and Young Hens |

Total Hen Egg

Production |

Total Hen Egg Export |

Per Capita Consumption |

|

1989 |

31.8 |

6,682 |

51.7 |

120 |

|

1990 |

36.5 |

8,165 |

85.3 |

145 |

|

1991 |

41.5 |

8,609 |

102.4 |

150 |

|

1992 |

38.9 |

8,154 |

41.8 |

142 |

|

1993 |

35.2 |

7,336 |

11.6 |

126 |

|

1994 |

37.4 |

7,728 |

17.1 |

131 |

|

1995 |

41.5 |

8,609 |

24.2 |

145 |

|

1996 |

41.0 |

8,619 |

64.6 |

142 |

|

1997 |

42.0 |

9,023 |

49.2 |

142 |

|

1998 |

41.8 |

8,675 |

99.2 |

140 |

|

1999 |

40.8 |

7,943 |

27.8 |

135 |

|

2000 |

41.7(f) |

8,233(f) |

88.6 |

141(e) |

|

2001 |

39.6(f) |

7,923(f) |

80(e) |

139(e) |

Source: Office of Agricultural Economics (OAE), MOAC

Note: f=forecast, e=estimate

In the past, there were numbers of small hen farmers throughout the country. That should not be surprising since almost all the eggs produced are for domestic consumption, which is fairly distributed to various regions, except for big cities like Bangkok where demand for eggs is much larger. However, the yields in those small farms are relatively low (less than 260 eggs/hen-year) compared with those of high-tech farm that use “Evap Houses” to keep the inside-temperature down and could increase the yield per chicken to more than 280 or even more than 300 eggs/hen-year. Consequently, smaller farms with 20,000 layers or less began to disappear and are replaced by farms with high technology, especially in Nakorn Pathom and Nakorn Nayok where almost all new farms has more than 2 million layers per farm. The number of farms has decreased. As of today, according to experts in the field, there are about a dozen of large farms (each of which has more than one million layers) whose market shares combined are about two-thirds of the egg market. Again, the official figures of farm size distribution are shaky. The DLD is the only source that publishes the data occasionally. According to the DLD figures, the number of small commercial farms (100-1,000 hen) decreased substantially in 2001, but numbers of larger farms of all sizes increased.

Table 2-12 Layer Farm Size, 2001

| |

Year |

|||

|

2000 |

2001 |

|||

|

Farm Size (# of hens) |

Number of Farms |

% |

Number of Farms |

% |

|

< 100 |

n.a. |

n.a. |

2,219 |

35 |

|

100-1,000 |

2,779 |

54 |

1,502 |

24 |

|

1,001-10,000 |

2,053 |

40 |

2,170 |

34 |

|

10,001-100,000 |

241 |

5 |

373 |

6 |

|

>100,000 |

29 |

0.6 |

40 |

0.7 |

|

Total |

5,102 |

100 |

6,304 |

100 |

Source: DLD

The fact that some eggs are exported at a price below domestic ones involves some type of export subsidy. In some occasions, part of the subsidy comes from the government in terms of low-interest loans or, to a lesser extent, outright export subsidy. However, in many occasions, it is the large players’ agreement (through professional associations) to take a cut in order to stabilize the domestic price. Furthermore, the fact that less than one percent of eggs was exported each year suggests that these associations have been fairly successful in controlling the supply of eggs controlling the number of breeding stock. This is possible because there are less than a dozen large players whose farm sizes are more than one million layers and who also import, raise, and supply the breeding stock, even though their market shares of eggs combined is about two-thirds of the total egg supply.

Domestic per capita consumption of eggs had increased continuously to 142 eggs per year in 1997. After the crisis hit, per capita consumption of eggs decreased slightly in 1998 and 1999, but appear to rebound back in the year 2000.

Technological changes in the layer subsector resembled the changes in the broiler industry, albeit slower. The “Evap Houses” continue to replace open-house farms to increase productivity. Smaller farms with 20,000 layers or less, as well as the ones in which yields are below 260 eggs/hen-year continue to disappear and are replaced by larger farms with high technology. As with broilers, the owners of those smaller farms who are out of this business often switch to other businesses, especially to another agro-businesses (including many shrimp farms in the eastern region).

In very early days, pig farming in Thailand always meant backyard pig farming where farmers kept a few native pigs for piggery saving and for utilization of household waste. Thai-native pigs were black in color, with an arched back, slow growth, fatty carcass and attained market size at 70kg body weight in approximately 12 months. Although they were high prolificacy, they are inappropriate and uneconomical to employ for commercial pig production.

Development of the pig industry began in 1960 when DLD, introduced modern exotic pig breeds including Large White, Berkshire and Tamworth from England for breeding and improvement of pigs in the country. The animals were multiplied and distributed to pig farmers in the rural via regional livestock breeding and improvement stations of the DLD and via the pig breeding farms co-operated to the DLD. The animals significantly upgraded the Thai-native pigs and the up-graded crossbreds had improved performance, better conformation and better carcass quality. Because of the results farmers have moved towards modern pig production technology and have initiated pig production development of the country. However, only Large White and Tamworth were widely accepted by the farmers since Berkshire are black in color which is not favored by the Thai consumers.

Department of Animal Science, Kasetsart University has introduced American Landrace and Duroc Jersey for the university's pig breeding program. The animals were multiplied and distributed to farmers for further upgrading of native pigs. The animals were very sturdy and had good adaptability for tropical environment and to the farm management practices of the backyard farmers in the country. The animals also had superior performance to those earlier imported by DLD and made US pigs become popular until the end of the 80’s.

The up-graded crossbreds or the improved breed animals had better performance including higher average daily gain, better feed efficiency and carcass quality (higher lean content), and required better nutrition, better farm management practices and more a complicated vaccination program than ever. It took many years for farmers to learn and to understand the logic and the situation has caused some painful experiences to farmers in the country.

Commercial protein concentrate feeds and feed supplements had supplied better nutrition for the improved performance animals and have greatly helped to facilitate the success of pig industry development in those days.

DLD and Co-operatives provided training courses on modern pig production and farm management to farmers and organized certified pig breeding farms to be provincial pig breeding centers for further pig breeding and improvement, and for distribution of the genetic improved pigs to farmers in the area. The practice has significantly improved and helped the development of the national pig industry.

In 1975, DLD and Kasetsart University had a joint cooperation in the National Pig Improvement Project and National Swine Research and Training Center located at Kasetsart University, Kampaengsaen, Nakhon Pathom was setup as the body of the project. The program was aimed at making a sustainable pig industry development in the country and the center’s activities to attain the objectives of the program included:

Pig breeding and improvement and distribution of the improved pig breeds to the farmers.

Research of improvement of pig production under Thai condition including nutrition, feed ingredients utilization, farm management, diseases control programs, etc.

Extension working including farmer training courses consisting of 1) Pig production training courses (21 days); 2) Pig nutrition and feed production training course (7 days); 3) Artificial insemination (5 days); 4) Pig health and farm sanitation training course (7 days); 5) Pig production short course (2 - 3 days) conducted at provinces throughout the country, and together with technical publications i.e. Pig Magazine and text books and general consultation to the farmers.

Promotion of provincial pig co-operatives activities including the co-op member swine production training, and advice on operation of co-op breeder farms, feed mill and pork outlets.

The Center has produced more than 5,000 farmers who passed the training courses; a large number of genetically improved pigs were distributed to farmers for breeding and improvement of the farms; more than 250 topics of research topics dealing with pig production improvement and the knowledge was transferred to farmers via the farmer training courses and publications. Farmers who passed the training course have been served as the leading farmers in the area and have contributed a significant improvement to the national pig industry. Promotion of provincial pig co-operatives activities is aimed at improving pig production practice of small-scale pig holders and to provide survival of the farmers in the pig industry. Although the results of the activities are not fully satisfied at a moment, a few pig co-operatives have gained some successful and have proved the feasibility of pig co-operatives system in Thailand.

During 1975 - 1979, Chareonphokpand Co., Ltd. (CP) have introduced modern pig breeds (Zegher and Hy-Por) and more intensive pig housing and management system from Belgium to farmers in Thailand. Although the pig breeds were not accepted by pig farmers due to more sensitivity to stress conditions in the country, the practices have excited the farmers for high performance and high lean European pigs as well as for the more advanced and more intensive modern pig production. Introductory of European pig breeds and pig farm management systems have influenced the changing of pig production in Thailand and have subsequently caused a number of developments in the pig industry of the country.

Pig production in Thailand is an open competitive business among pig producers which include independent private farmers ranging from small scale to extra - large scale pig holders, feed mill companies’ dependent farmers as well as the feed mill companies pig farms. There are apparently minimum supports or protection from the government for independent farmers especially small-scale holders to be survived in the business. It is necessary for every class of pig producer to be knowledgeable, highly developed and highly efficient in order to minimize the cost of production and to survive in the industry.

There have been tremendous changes in pig production technology in Thailand in the past 15 years, which are influenced by the changing consumer preferences, the degree of competition of the industry and the public concern for environmental pollution by the pig farms. The changes include breeds of animals, nutrition, housing and farm management systems, vaccination program as well as waste treatment and disposal system.

High performance/high lean European pigs dominated by Danish Landrace and Duroc and British Large White have been widely adopted by pig production industry. Animals from other sources i.e. Ireland and Norway have also been introduced but popularity is still limited. European pigs have high growth rate, efficient feed conversion and high lean content in the carcass. Results of performance testing of European pigs conducted by National Swine Research and Training Center, Kasetsart University have indicated that the animals that have been bred and selected in Thailand have production performances and carcass quality close to those reported from the original country (Table 3.1). The data have indicated the ability of the animals to adapt for the tropical region and the suitability for commercial pig production.

Table 3-1 Growth rate (g/d) of purebred pigs, which have been bred and selected in Thailand tested at National Swine Research and Training Center, Kasetsart University, Kampaengsaen, Nakhon Pathom in 1994

|

Body wt. (kg) |

Landrace |

Large White |

Duroc |

Average |

|

50 |

848 |

802 |

844 |

834 |

|

60 |

718 |

775 |

726 |

737 |

|

70 |

879 |

753 |

901 |

854 |

|

90 |

732 |

909 |

756 |

788 |

|

Average |

794 |

809 |

806 |

803 |

Source: Kanto (1994)

The classical three - way crossbreds, Landrace (Large White (Duroc, for market pigs is still popular and widely accepted in the industry. The crossbreds generally produced by the crossing of Duroc boar which is meaty and sturdy with the two - ways crossbred, Large White (Landrace sows which is high prolific and has good carcass quality. The crossbreds, which are quite sturdy under hot climate condition and have quite satisfactory carcass quality, have been proved to be appropriate for the tropical country. The two-ways crossbred gilts normally produced by pig breeding farm or companies and sold to fattening pig farms for production of three - ways crossbred market pigs. Commercial fattening pig farms always have farrow to finish facilities and produce their own three-ways crossbred for the marketing pigs. The practice is not only allowed the steady supply of the feeder pigs for fattening but also facilitate the control of feeder pigs quality of the farms. Purchasing of feeder pigs from outside is very risky for market pig production due to unsteady supply, uncontrollable genetic background, poor quality and poor health status of the animals, which lead to unsuccessful of fattening pigs production.

Artificial insemination by using fresh semen produced in the farm has been widely accepted by commercial pig farms ranging from medium to extra-large scale holders. The practice have been continuously developed and not only provide high conception rate comparable to the natural mating but also require minimum number of boars used and allow better utilization of high quality boars for market pig production in the farms. Artificial insemination can provide farrowing rate ranging from 75-90 % and require a boar for 45 - 60 sows. The practice also allows the uses of external high quality semen or imported semen for breeding and herd improvement of the farms. National Swine Research and Training Center, Kasetsart University, Kampaengsaen, Nakhon Pathom have provided a training course in swine artificial insemination and more than 1,500 farmer have attended and passed the training course since 1987. The activities have stimulated the acceptance of AI in the pig farms and also have provided a continuous development of AI technology to the industry. It is estimated that more than 60 % of commercial pig farms in the country have employed AI. Small scale pig holders which have less than 50 sows in the farms may not feasible to employ AI in the farm due to high cost of the AI equipment, less knowledge and skills of operation and still affordable for a few boars in the farms. However, a number of small-scale pig holders have been using AI with a very considerably success.

There have been attempts to introduce commercial hybrid pig breeds into the country but the success was very limited. Zegher and Hy-Por from Belgium, NeuDalland from the Netherlands, and DeKalb and PIC from the United states have been introduced into Thailand during the 70 's, 80 's and 90 's, respectively and non of them have been widely accepted by the farmers. Although genetics of commercial hybrid pig breeds are well controlled and well combined to produce the high performance and high carcass quality market pigs. The animals are always less sturdy in tropical climate and are more expensive than the purebred pig breeds. Acceptance of the classical three-way crossbreds, LR (LW (D, for market pig production have allowed the farmers to design their own breeding program and more selection of pig breed lines to produce more suitable market pigs under their production condition and market demands. In additional, there are more sources of supply of purebred pig breeds than those of the commercial hybrid pig breeds, which allow more flexibility for farmers to manage the pig breeding program of the farms.

It is common for commercial pig farm to adopt high nutritional specification for animal in the farm. High performance/high lean pigs which require higher amount of nutrient (protein, amino acids vitamins and minerals) in a day together with lower feed intake of the animals in the hot weather have forced the farmers to go with high protein and high amino acids diets for optimum growth and maximum lean content of the pigs. There has been a study indicating that although the low feed intake of animals in the tropical climate, optimal growth and lean content as well as the lowest feed cost per gain were archived when growing and finishing pigs have absolute amount of lysine and other amino acids intake according to the requirement in a day (Tables 3.2, 3.3 and 3.4). There are different feed intakes among the pig farms due to the variation of environmental conditions therefore different nutritional specification are required for the optimum production performances and for the lowest cost of production.

Table 3-2 Performances of growing pigs (15 - 50 kg) fed diets containing varied levels of lysine

|

Pig Performance |

Lysine (g/kg) |

|||

|

9.5 |

10.5 |

11.5 |

12.5 |

|

|

Initial wt. (kg) |

17.41 |

16.98 |

17.42 |

17.32 |

|

Final wt. (kg) |

50.38 |

50.06 |

50.38 |

51.99 |

|

Feed intake (kg-d) |

1.45 |

1.42 |

1.45 |

1.48 |

|

Lysine intake (g-d) |

13.78 |

14.91 |

16.68 |

18.50 |

|

ADG (g) |

598b |

624a |

604a |

736a |

|

FCR |

2.44c |

2.29b |

2.10a |

2.20a |

|

Feed cost (Baht/kg) |

7.04 |

7.21 |

7.36 |

7.53 |

|

Cost of gain(baht/kg) |

17.18c |

16.48bc |

15.47ab |

15.20a |

Source: Panacharoensawat (1995)

Table 3-3 Performance of finishing pigs (50 - 90 kg) fed diets containing varied levels of lysine

|

Pig Performance |

Lysine (g/kg) |

|||

|

7.5 |

8.5 |

9.5 |

10.5 |

|

|

Initial wt. (kg) |

50.38 |

50.06 |

50.38 |

51.99 |

|

Final wt. (kg) |

91.43 |

91.83 |

91.81 |

92.26 |

|

Feed intake (kg-d) |

2.18 |

2.23 |

2.26 |

2.29 |

|

Lysine intake (g-d) |

16.35 |

18.96 |

21.47 |

24.05 |

|

ADG (g) |

715b |

795ab |

823a |

862a |

|

FCR |

3.08b |

2.18a |

2.77a |

2.68a |

|

Feed cost (Baht/kg) |

6.27 |

6.43 |

6.59 |

6.75 |

|

Cost of gain(baht/kg) |

19.33 |

18.01 |

18.30 |

18.09 |

Source: Panacharoensawat (1995)

Table 3-4 Performances of growing -finishing pigs (15-90 kg) fed diets containing varied levels of lysine

|

Pig Performance |

Lysine (g/kg) |

|||

|

9.5/7.5 |

10.5/8.5 |

11.5/9.5 |

12.5/10.5 |

|

|

Initial wt. (kg) |

17.24 |

16.98 |

17.42 |

17.32 |

|

Final wt. (kg) |

91.43 |

91.83 |

91.81 |

92.26 |

|

Lysine intake (15-50 kg) |

13.78 |

14.91 |

16.68 |

18.50 |

|

Lysine intake (50-90 kg) |

16.35 |

18.96 |

21.47 |