June 2008 June 2008 | ||

|

Food Outlook | |

| Global Market Analysis | ||

|

Market indicators and food import bills

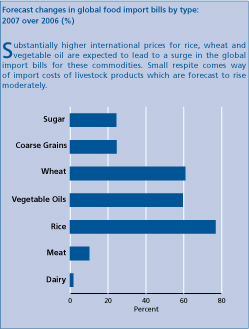

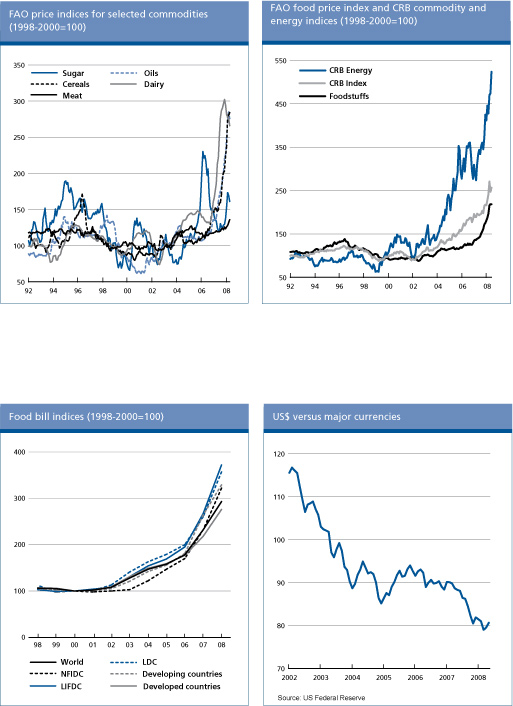

The global cost of imported foodstuffs in 2008 is forecast to reach USD 1 035 billion, 26 percent higher than last years peak. This figure is still provisional as FAOs food import bill forecasts are conditional on developments in international prices and freight rates, which remain highly uncertain over the remainder of the year The bulk of the anticipated growth in the world food import bill would rest on higher expenditures on rice, wheat and vegetable oils, which are all forecast to rise to unprecedented levels from 2007: 77 percent in the case of rice, in spite of a forecast sharp contraction in global rice deliveries in 2008, and around 60 percent for wheat and vegetable oils. Soaring international quotations are mostly responsible but also freight costs, which have nearly doubled for many routes. The combination of rapidly rising prices and higher freight costs is behind the higher global bills for imported coarse grains and sugar, given anticipated reductions in imported volumes, notably for maize. Import bills for livestock products are expected to register smaller gains, owing to moderate increases in global quotations together with subdued trade.

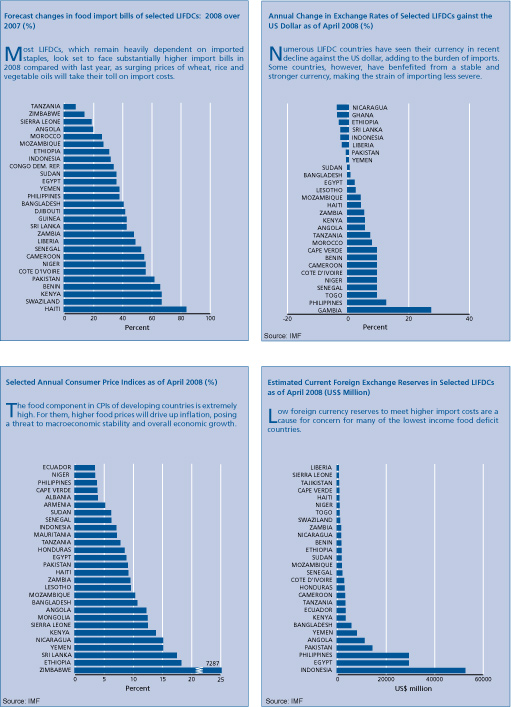

Among economic groups, the most economically vulnerable countries are set to bear the highest burden in the cost of importing food, with total expenditures by LDCs and LIFDCs anticipated to climb by 37-40 percent from 2007, after rising 30 and 37 percent, respectively, already last year. The sustained rise in imported food expenditures for both vulnerable country groups constitutes a worrying development, as on current expectations by the end of 2008, their annual food import basket could cost four times as much as it did in 2000. This is in stark contrast to the trend prevailing for developed countries, where year-to-year import costs have risen far less. Higher food import bills are not necessarily resulting from more imported food. Numerous LDCs and LIFDCs are expected to curtail the procurement of many foodstuffs from international markets, a reaction that in numerous cases does not reflect improved domestic supply prospects. Moreover, food staple inventories have far from recovered in many LDCs which only adds to their vulnerability, especially given the considerable uncertainty in international price prospects. Forecast import bills of total food and major foodstuffs (USD million)

1. The food import bill is based on actual market values of raw and processed goods as opposed to values expressed in primary equivalents. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GIEWS | global information and early warning system on food and agriculture |