![]()

![]()

![]()

6.1.1 Household Head

Age. On the hog farms, the mean age of the HH head, or farm decision-maker, was 46 years. The medium independents were a relatively younger group with mean age of 40 years, while the large independents were relatively older at 52 years of age on average (Table 6.1).

Table 6.1 Characteristics of household head, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract Independent |

Medium |

Large Independent |

Contract |

|

|

Age |

48 |

46 |

40 |

52 |

46 |

|

Gender (Male, %) |

78 |

48 |

88 |

47 |

80 |

|

Civil Status (Married, %) |

93 |

78 |

86 |

82 |

80 |

|

Education (no.of years) |

10.7 |

9.9 |

13.3 |

12.3 |

13.8 |

|

Hog raising is main occupation |

54.0 |

91.3 |

58.0 |

64.7 |

70.0 |

|

Has secondary occupation |

62.0 |

52.9 |

62.0 |

52.9 |

26.7 |

|

Experience in raising |

12.9 |

17.0 |

10.3 |

11.1 |

9.3 |

|

Has any formal related to animal business management |

57.5 |

39.1 |

74.0 |

70.6 |

73.3 |

|

Has any training in or business management? |

65.5 |

73.9 |

78.0 |

64.7 |

76.7 |

Source: UPLB-IFPRI LI Field Survey,

Gender. HH heads were predominantly men, except for smallholder contract growers, of which 52 percent were women, and large independent producers, of which 53 percent were women. There seems to be no gender bias in the decision-making aspect of the hog-raising business, although for large contract producers this may be scale-dependent.

Civil status. The HH heads in the sample were mostly married, with a more or less even distribution across sub-samples except for smallholder independents among whom the proportion of married HH heads was highest at 93 percent.

Schooling. The average number of years in school of the HH heads in the smallholder sub-sample was 10-11 years. The HH heads in the commercial sample were relatively more highly educated with 12-14 years of schooling.

Main occupation. Hog production appears to be a more serious business undertaking by contract growers regardless of scale. Smallholders and large contract producers devote, respectively, 91 percent and 70 percent of their efforts to the occupation. This is in contrast to the independents, who devote 54 percent and 65 percent, respectively, for smallholders and large producers.

Large contract growers engage least in secondary occupations (27%) compared to the other subgroups, whose engagement in a secondary occupation ranges from 53 percent to 62 percent. These figures reinforce the observation that hog production is quite a serious business among large contract growers.

Farming and business background. The average years of experience of HH heads in the hog business was highest for the smallholder contract growers at 17 years compared to the rest of the subgroups, whose years of experience ranged from 9 to 13 years.

With regard to education and training, the commercial producers had much higher exposure to formal education in animal science or business management (71-74%), compared to only 39-58 percent for smallholders.

The distribution of attendance at livestock or business training programs in the last two years is relatively even. Exposure is relatively high, at least 65 percent, in each subgroup. Access to training as such appears to be non-discriminatory.

6.1.2 Spouse of the HH head

Age, gender, civil status, and education. The spouses of medium-scale independent producers were a relatively young group, with a mean age of 40 years. The rest varied from 44 to 47 years (Table 6.2).

Table 6.2 Characteristics of spouse of household head, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

||

|

Age |

47 |

44 |

40 |

47 |

45 |

|

|

Gender (Female; %) |

78.0 |

48.0 |

88.0 |

47.0 |

80.0 |

|

|

Civil Status (Married; %) |

93.1 |

78.3 |

86.0 |

82.4 |

80.0 |

|

|

Education (no. of years) |

12.8 |

13.6 |

13.0 |

12.2 |

11.5 |

|

|

Main occupation (%) |

29.6 |

50.0 |

23.3 |

28.6 |

29.2 |

|

|

Level of involvement (%) |

71.6 |

77.8 |

60.5 |

64.3 |

58.3 |

|

|

Type of involvement (%) |

|

|

|

|

|

|

|

Management |

29.4 |

22.7 |

69.4 |

100.0 |

81.3 |

|

|

Direct Production |

70.6 |

77.3 |

30.6 |

0.0 |

18.8 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

The spouses were predominantly women, except for smallholder contract growers (48%) and large independent producers (47%). Their average number of years of schooling was about even across subgroups, at 12-14 years.

Main occupation. The degree of involvement of spouses in the hog production business was highest among the smallholder contract growers, at 50 percent of spouses. For the rest of the sub-samples, the proportion of spouses whose main occupation was the hog production business varied from 23 percent to 30 percent. Spouse involvement is thus observed among smallholders (contract growers in particular), who treat hog production as a serious business engagement.

Spouse engagement in the business. Among smallholders there was a relatively high involvement of spouses of HH heads in the business (72-78%) compared to 58-64 percent among large producers. This further reinforces the observation that spouses and women are relatively intensively involved in smallholder production.

There is quite a difference in the nature and role of spouse involvement between commercial producers and smallholders. While 69-100 percent of the spouses of commercial producers performed mostly managerial work (e.g., supervising, keeping the finances and books), some three-quarters of spouses of smallholders (71-77%) engaged mostly in direct production activities.

6.1.3 Other HH members

The average size of households involved in hog production is more or less even at six persons (Table 5.3).

A relatively higher involvement by other HH members was observed among smallholders (2.0-2.5 members) compared to commercial producers (1.4-1.8 members involved in the business). This may reflect a greater opportunity cost of the time of HH members on commercial farms.

Table 6.3 Household size, number involved in the livestock business, average expenditure, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Household size |

6 |

6 |

6 |

7 |

6 |

|

Number involved in livestock business |

2 |

2 |

2 |

1 |

1 |

|

Average monthly expenditure (PhP) |

10,824 |

9,148 |

13,848 |

19,653 |

19,873 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Average expenditures of smallholder households was 9,000-11,000 pesos monthly compared to 14,000-20,000 pesos for commercial producers. Here, the mean expenditure per month is taken as a proxy for the flow of income from all sources and not just from the hog business.

6.2.1 Area, Livestock, and Major Crops

The average landholdings of smallholders ranged from 0.3 to 1.8 hectares compared to 3.6 to 6.0 hectares of commercial producers (Table 6.4). Landholdings of commercial contract growers were relatively large at an average 6.0 hectares. These figures suggest that ownership of land assets could be key to accessing commercial hog contracts.

Table 6.4 Area of landholding, area for livestock,area for other crops, major crops Hog Production Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

||

|

Area of landholding |

1.8 |

0.3 |

3.6 |

4.4 |

6.0 |

|

|

Area for livestock (ha) |

0.4 |

0.3 |

1.1 |

1.7 |

3.6 |

|

|

Area for other crops (ha) |

1.4 |

0.1 |

2.5 |

2.7 |

2.4 |

|

|

Major crops planted (%) |

|

|

|

|

|

|

|

Fruit trees/tree crops |

35.3 |

50.0 |

41.4 |

38.46 |

47.6 |

|

|

Vegetables |

17.6 |

33.3 |

6.9 |

15.38 |

14.3 |

|

|

Cereals |

17.6 |

0.0 |

20.7 |

30.77 |

9.5 |

|

|

Sugarcane |

11.8 |

0.0 |

13.8 |

15.38 |

9.5 |

|

|

Others |

17.6 |

16.7 |

17.2 |

0.00 |

19.0 |

|

|

Total |

100.0 |

100.0 |

100.0 |

100.00 |

100.0 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

Smallholders devote relatively less land area for livestock (0.3-0.4 ha), compared with 1.1-3.6 hectares for commercial producers. Again, the area for livestock is largest for commercial contract growers (3.6 ha). Regarding the amount of land planted to crops, smallholders had 0.1-1.4 hectares compared to commercial farms with their 2.4-2.7 hectares. These areas were predominantly planted to fruit trees across all the subgroups.

6.2.2 Land Characteristics

In terms of land classification of farm sites, 70 percent of independent smallholder farms were situated on predominantly non-agricultural (e.g., residential) lands (Table 6.5). The rest of the farms were located on predominantly agricultural lands (65-9 4%).

Table 6.5 Classification of landholding, distance to main markets for inputs and output, distance to nearest bodies of water, distance to nearest settlement, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

||

|

Land classification |

|

|

|

|

|

|

|

Agricultural |

29.9 |

65.2 |

72.0 |

94.1 |

93.3 |

|

|

Non-agricultural |

70.1 |

34.8 |

28.0 |

5.9 |

6.7 |

|

|

Distance to main market of output (km) |

15.41 |

3.95 |

62.05 |

75.86 |

70.65 |

|

|

Distance to main source of feed (km) |

6.80 |

2.73 |

34.62 |

70.03 |

61.37 |

|

|

Distance to nearest body of water |

|

|

|

|

|

|

|

Stream/River |

0.74 |

0.32 |

0.43 |

0.44 |

1.05 |

|

|

Lake |

6.39 |

0.03 |

0.61 |

44.50 |

|

|

|

Distance to nearest settlement (km) |

0.21 |

0.27 |

0.81 |

0.75 |

0.82 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

On average, the independent smallholder farms were relatively closer to their main output market (4-15 km), while the commercial producers were located much farther out (62-76 km). Evidently, the independent smallholders were selling their output at a market much nearer their production site (usually the closest town) while the commercial producers had a main output market at some distance away. Smallholder farms were likewise closer to their main source of feed (3-7 km) than the commercial farms, which were at least ten times farther away (35-70 km). However, this proximity of farms to input and output markets does not by any means connote an advantageous access to wholesale markets.

The large contract farms were located at the greatest average distance to the nearest water body (1.1 km), but the rest of the subgroups were relatively close (0.3-0.7 km). Likewise, smallholder farms were closer to residential community/settlement areas (0.2-0.3 km) compared to commercial producers (0.8 km). This reinforces the earlier observation that most smallholder farms were located in non-agricultural areas.

6.2.3 Access to Utilities

Piped-in water supply. Smallholders had a relatively higher incidence of being connected to a municipal piped-in water supply at 44-61 percent. Commercial producers had comparatively little access to this service at 6-38 percent (Table 6.6). However, this finding may simply be a function of the distance from farms to the closest town or residential centers.

Table 6.6 Access to utilities, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Access to piped- in water (%) |

43.7 |

60.9 |

38.0 |

5.9 |

10.0 |

|

Access to electricity (%) |

96.6 |

100.0 |

90.0 |

100.0 |

93.3 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Power supply. Most farms in the sample had access to electrical power supply (93-100%). Producers consider access to power mains as more crucial than connection to public water utilities. Farms can generate their own water supply from private wells at costs that are not prohibitive.

6.3.1 Type of Activity, Scale of Operations, and Production Arrangements

Activity types. Smallholders tend to congregate in particular types of production activities, depending on whether they are independent producers or contract growers (Table 6.7).

Small contract growers specialize in grow-to-finish (Type 3) operations, in which weanlings and feeds are provided by the integrator and the animals are fattened to produce slaughter hogs.

Table 6.7 Distribution (%) by type of activity in livestock production, Hog Production Philippines, 2002

|

PRODUCTION |

SMALLHOLDER |

COMMERCIAL |

|||

|

PATTERN |

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

Type 1: Farrow-to-wean |

33.3 |

0.0 |

4.0 |

0.0 |

0.0 |

|

Type 2: Farrow-to-finish |

47.1 |

4.3 |

64.0 |

47.1 |

0.0 |

|

Type 3: Grow-to-finish |

8.0 |

95.7 |

0.0 |

0.0 |

100.0 |

|

Type 4: Combination |

11.5 |

0.0 |

32.0 |

52.9 |

0.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Close to half (47%) of independent smallholders engage in farrow-to-finish (Type 2) operations and one-third (33%) engage in piglet production (Type 1: farrow-to-weaning). The rest combine the above operations where feasible and desired, with dual output of mostly slaughter hogs and, secondarily, piglets.

Commercial (large) contract growers specialize only in grow-to-finish activities. Medium and large independent producers specialize in farrow-to-finish operations or a combination of activities, with dual output of slaughter hogs and piglets. None engaged in pure grow-to-finish (Type 3) operations and they rarely engaged in pure piglet production (Type 1).

6.3.2 Size of Holdings

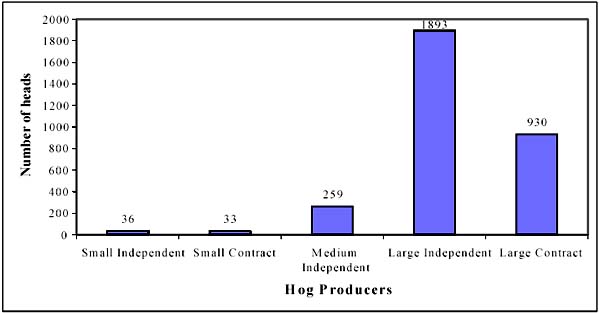

On average, smallholders had 33-37 heads of hogs in their inventory (Figure 6.1 and Table 6.7). This is about one-seventh the inventory size of the medium-sized independents. Smallholder holdings amount to only four percent of the holdings of large commercial contract growers and only two percent of the holdings of the large independents.

Thus, whether under contract or independent, smallholder holdings are extremely small compared to commercial holdings. Among independent smallholders, smaller inventories are held by farrow-to-wean (26 heads) and grow-to-finish (23 heads) operations. Farrow-to-finish and dual output activities have larger inventories (43-45 heads). For identical activities (Type 3), small contract growers held larger inventories (34 heads) relative to independents (23 heads).

Figure 6.1 Size of current inventory by production arrangement and scale of operation, Hog Production, Philippines

6.3.3 Investment

Total investment. Total investment in breeding stock or herds and in facilities and equipment are slight among smallholders as compared to commercial producers (Figure 6.2 and Table 6.8). Among independent producers, smallholders’ average investment, at 153,000 pesos, is only one-eighth that of medium-scale commercial operations and one-fiftieth that of large commercial independents (7.8 million pesos).

Figure 6.2 Value of total investment by production arrangement and scale of operation Hog Production, Philippines 2002

Among contract growers, the average value of investment per farm for smallholders (10,806 pesos) was only 0.6 percent that of the commercial contract growers (1.9 million pesos).

Among independent smallholders, total investment is relatively lower for grow-to-finish (Type 3) and farrow-to-wean (Type 1) operations, where mean investments were 96,298 pesos and 104,698 pesos, respectively. For the two other types of operations, farrow-to-finish or combinations with farrow-to-finish, investments were 179,245 pesos and 221,334 pesos, respectively.

Table 6.8 Size of current livestock inventory, value of total investments, and investment per animal, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

||

|

Farrow-to-wean |

|

|

|

|

|

|

|

Inventory |

26 |

|

15 |

|

|

|

|

Total Investment |

104,698 |

|

826,518 |

|

|

|

|

Investment per head |

4,092 |

|

5,264 |

|

|

|

|

Farrow-to-finish |

|

|

|

|

|

|

|

Inventory |

45 |

9 |

306 |

2,256 |

|

|

|

Total Investment |

179,245 |

76 |

1,552,659 |

9,978,53 |

|

|

|

Investment per head |

4,009 |

85 |

5,070 |

4,423 |

|

|

|

Grow-to-finish |

|

|

|

|

930 |

|

|

Inventory |

23 |

34 |

|

|

|

|

|

Total Investment |

96,298 |

11,262 |

|

1,907,945 |

|

|

|

Investment per head |

4,110 |

333 |

|

|

2,052 |

|

|

Combination |

|

|

|

|

|

|

|

Inventory |

43 |

|

17 |

1,56 |

|

|

|

Total Investment |

221,334 |

|

835,496 |

5,848,100 |

|

|

|

Investment per head |

5,123 |

|

4,677 |

3,726 |

|

|

|

All |

|

|

|

|

|

|

|

Inventory |

36 |

33 |

25 |

1,89 |

93 |

|

|

Total Investment |

152,560 |

10,806 |

1,294,121 |

7,791,834 |

1,907,945 |

|

|

Investment per head |

4,186 |

33 |

4,989 |

4,117 |

2,052 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

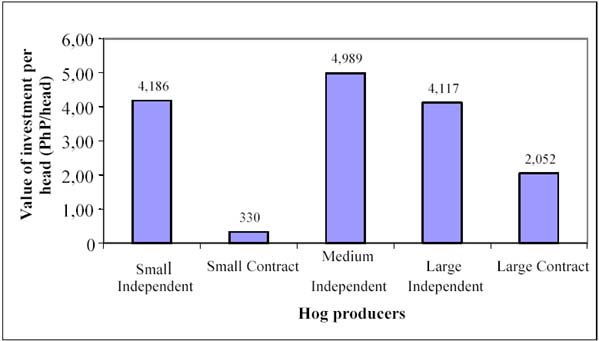

Average investment per head of animal. While total investment differed markedly between smallholders and commercial producers, average investment per animal was quite comparable (Figure 6.3 and Table 6.9).

Among independent producers, investment per head falls with scale only upon reaching relatively large operations (1,000+ heads of inventory). After rising among medium-sized independents, investment per head falls in the large-scale operations, becoming comparable with that of smallholder independents.

Table 6.9 Size of breeding stock, value of breeding stock, and average value of breeding stock investment per animal, Hog Production, Philippines 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

||

|

Type 1 |

|

|

|

|

|

|

|

Total Investment (‘000 PhP) |

50 |

|

444 |

|

|

|

|

Investment per head (‘000 PhP/head) |

7.77 |

|

11.38 |

|

|

|

|

Type 2 |

|

|

|

|

|

|

|

Total Investment (‘000 PhP) |

67 |

|

577 |

3,205 |

|

|

|

Investment per head (‘000 PhP/head) |

7.57 |

|

10.30 |

10.41 |

|

|

|

Type 3 |

|

|

|

|

|

|

|

Total Investment (‘000 PhP) |

|

|

|

|

|

|

|

Investment per head (‘000 PhP/head) |

|

|

|

|

|

|

|

Type 4 |

|

|

|

|

|

|

|

Total Investment (‘000 PhP)v |

63 |

|

303 |

2,080 |

|

|

|

Investment per head (‘000 PhP/head) |

7.92 |

|

10.23 |

9.12 |

|

|

|

All |

|

|

|

|

|

|

|

Total Investment (‘000 PhP) |

56 |

|

484 |

2,610 |

|

|

|

Investment per head (‘000 PhP/head) |

7.41 |

|

10.32 |

9.83 |

|

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

On the whole, contract producers invest less per head than independents. Smallholder contract growers, however, have an extremely low investment level per head of animal.

These figures show that engagement in contract growing relieves the producer of a significant degree of the investment burden. The burden removed is the investment in growing stock.

There is a great divergence between large-scale and smallholder contract producers in mean investment per head of animal. Most large (commercial) contract producers work under fee contracts.

Figure 6.3 Total value of investment per head, by production arrangement and scale of operation, HogProduction, Philippines, 2002

It appears that the integrator demands some minimum set of facilities and equipment before granting such a fee contract. The stringent requirement does not appear to be demanded for the more informal smallholder price or profit-sharing contracts.

6.3.4 Employment of Hired Workers

Smallholder hog production uses predominantly family labor. The mean number of hired workers on contract and independent farms was 0.1 and 0.3 workers, respectively. That is to say, few farms have hired help (Table 6.10).The commercial farms employed an average of 2, 5, and 11 workers, respectively, for medium independent, large contract, and large independent farms.

Table 6.10 Average number of hired workers employed, Hog Production, Philippines, 2002

|

ENTR |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Number of hired |

0.3 |

0.1 |

2.3 |

10.5 |

5.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Table 6.11 Differences in prices paid for weanlings, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract Independent |

Medium |

Large Independent |

Contract |

||

|

Weanling price (PhP/head) |

|

|

|

|

|

|

|

Type 1 |

|

|

|

|

|

|

|

Type 2 |

|

|

|

|

|

|

|

Type 3 |

1,214 |

1,649 |

|

1,933 |

|

|

|

Type 4 |

1,200 |

|

1,000 |

|

|

|

|

All |

1,213 |

1,630 |

1,000 |

1,933 |

|

|

* n=3.

Source: UPLB-IFPRI LI Field Survey, 2002-03

6.3.4 Prices of Purchased Weanlings

The purchase of weanlings for fattening is applicable only to grow-to-finish (Type 3) operations. For this activity, contract growers, regardless of scale, paid higher prices for weanlings than independent producers (Table 6.11). Comparing the different scales of contract growers, the larger-scale producers paid slightly less than small contract growers.

6.3.5 Feeds

Average feed price by type. Feed prices vary by type (booster, pre-starter, starter, grower, finisher, sow feed) (Table 6.12). Within each type, price also varies by feed grade (premium, standard, regular). Weighted prices per kilogram of feed across types of activity reflect differences in feed quality as well as access to wholesale prices.

For farrow-to-wean (Type 1) operations, medium-scale commercial independents paid lower prices (14.9 pesos per kg) for feeds than independent smallholders.

Table 6.12 Differences in weighted price paid per kilogram of feed, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract Independent |

Medium |

Large Independent |

Contract |

|

|

Type 1 |

22.27 |

|

14.86 |

|

|

|

Type 2 |

14.61 |

11.31 |

11.80 |

12.07 |

|

|

Type 3 |

14.48 |

11.66 |

|

|

11.56 |

|

Type 4 |

15.05 |

|

13.63 |

13.94 |

|

|

Weighted feed price (PhP/kg feed) |

17.20 |

11.63 |

12.51 |

13.06 |

11.56 |

* n=3.

Source: UPLB-IFPRI LI Field Survey, 2002-03

For farrow-to-finish (Type 2) operations, the commercial producers, as well as small contract growers, paid lower prices on average (11.3-12.1 pesos per kg) than independent smallholders (14.6 pesos per kg).

For grow-to-finish (Type 3) price contract growers, the larger producers paid higher prices for feed (13.1 pesos per kg) than smallholder contract growers (11.7 pesos per kg). The contract growers in general paid lower prices than the few Type 3 independent smallholders.

For Type 4 operations, independent commercial producers paid lower prices for feed (13.6 -13.9 pesos per kg) than independent smallholders (15.1 pesos per kg).

Feed costs per kilogram of output. In piglet production (Type 1), commercial independents incurred higher feed costs per kilogram of output (50.0 pesos) than smallholders (30.2 pesos). This finding is unexpected (Table 6.13).

Table 6.13 Differences in feed costs per kilogram of output by production activity, Hog Philippines, 2002

|

PRODUCTION |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independe |

Large Independent |

Contract |

|

|

Type 1: Farrow-to-wean |

30.20 |

|

49.96 |

|

|

|

Type 2: Farrow-to-finish |

28.50 |

32.88 |

27.65 |

28.43 |

|

|

Type 3: Grow-to-finish |

28.68 |

26.92 |

|

21.98 |

|

|

Type 4: Combination |

30.81 |

|

34.28 |

28.31 |

|

|

All |

29.35 |

27.18 |

30.66 |

28.36 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

In farrow-to-finish (Type 2), no pattern can be established between scale of operations and costs per unit. That the small contract growers incurred the highest feed costs per unit output reflects only one observation.

In Type 3 activities, which are dominated by contract production, the smallholder contract growers had lower feed costs per kilogram of output than independents.

Comparing the different scales of price contract growers, smallholders incurred higher feed costs per unit than large contract growers.

6.3.6 Costs

Cost structure of hog production, with and without contracts. Relatively similar cost structure is observed among independent farms, regardless of scale. On average, feed is the dominant cost component, taking up averages ranging from 77 to 82 percent of total costs (Table 6.14).

Table 6.14 Differences in structure of major cost components, Hog Production, Philippines, 2002.

|

COSTS (%) |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Weanlings |

2.99 |

42.18 |

0.35 |

0.00 |

5.07 |

|

Feed |

76.92 |

53.16 |

82.27 |

81.78 |

4.46 |

|

Labor |

2.10 |

0.27 |

5.41 |

6.30 |

34.13 |

|

Drugs and disinfectants |

7.36 |

1.29 |

4.72 |

7.41 |

8.28 |

|

Depreciation |

1.51 |

0.77 |

2.04 |

1.15 |

16.34 |

|

Other tranport costs |

0.63 |

0.03 |

0.54 |

0.53 |

1.08 |

|

Other operating costs* |

7.69 |

2.22 |

4.23 |

2.49 |

27.15 |

|

Waste disposal cost |

0.80 |

0.07 |

0.44 |

0.34 |

3.49 |

* Other operating costs include water, electricity, rent, and maintenance costs, among others.

Source: UPLB-IFPRI LI Field Survey,

In other cost components, the salient differences between the independent smallholders and commercial farms lie in two areas. First is the relatively higher cost share for hired labor among commercial farms (5.4-6.3%). As smallholders use mainly family labor their cost share of hired labor is 2.1 percent. Second, other operating costs (e.g., utilities and maintenance costs) are higher for smallholders (7.7%) than for commercial farms (2.5-4.2%). This may reflect economies of scale on larger farms.

On the whole, the cost structure of smallholder contract production differs markedly from that on independent farms. It virtually reduces to the difference in cost structure between pure farrow-to-finish (Type 3) operations and those where farrowing operations are also undertaken. The most significant difference is the scaled-down relative importance of feed costs (53.2%) and weanling costs (42.2%) as significant explicit variable cost components in Type 3 activities, in which these two components make up about 95 percent of total costs.

There is also a stark contrast in cost structure between commercial contract farms and smallholder contract farms. This simply demonstrates the difference between the cost structure as borne by the contract grower under a fee contract arrangement in contrast to the costs effectively borne by the contract grower under price contracts. Under price contracts, the costs of weanlings and feeds must be explicitly charged to variable costs, evaluated at market prices of the inputs at the point of harvest and sale, before net income is divided equally between the contract grower and integrator. Under fee contracts, the cost of weanlings and feeds are borne entirely by the integrator. The small positive values for weanlings and feeds under commercial contracts reflect the three large-scale contract growers.

Under fee contracts, the major cost component borne by the grower is hired labor (34%). This is followed by other operating costs (utilities, rentals, maintenance) (27%). Depreciation of facilities is third (16%), highlighting the resources that the contract grower contributes in the cost-sharing arrangement.

Cost per kilogram of output. Among Type 1 operators, the commercial producers had higher average production costs (69.2 pesos per kg) than independent smallholders (44.5 pesos per kg) (Table 6.15). Among Type 2 producers, no pattern was found relating average cost to scale of production, and the means of each scale were similar.

Table 6.15 Differences in cost per unit of output, Hog Production, Philippines 2002.

|

AVERAGE COST (PhP/kg Q) |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract* |

|

|

Type 1 |

44.46 |

|

69.21 |

|

|

|

Type 2 |

34.17 |

54.78 |

33.74 |

35.37 |

|

|

Type 3 |

50.31 |

49.57 |

|

|

49.46 |

|

Type 4 |

39.62 |

|

40.39 |

33.53 |

|

*n=3.

Source: UPLB-IFPRI LI Field Survey, 2002-03

For Type 3 producers-predominantly contract growers-smallholders had about the same costs per kilogram of output as the larger price contract growers. Compared to their few independent smallholder counterparts, the contract growers also had about the same costs per kilogram of output.

For Type 4 producers, the large commercial independents had lower average costs (33.5 pesos per kg) than independent smallholder and medium-scale commercial operations. Between the smallholders and medium-scale commercials, there was no significant difference.

6.3.7 Revenue

Prices received for output. For weanlings or piglets, commercial producers received, on average, higher prices (97.5-112.4 pesos per kg) than independent smallholders (92.5 pesos per kg) (Table 6.16).

Prices received for output. For weanlings or piglets, commercial producers received, on average, higher prices (97.5-112.4 pesos per kg) than independent smallholders (92.5 pesos per kg) (Table 6.15).

Among independent commercial producers, the large-scale operators obtained significantly higher prices (112.4 pesos per kg) than their medium-scale counterparts. This may reflect a significant difference in quality or genetically identifiable characteristics of piglet output.

Table 6.16 Differences in prices received per kilogram of main output, Hog Production Philippines, 2002

|

OUTPUT |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

||

|

Farrow-to-wean |

92.39 |

|

86.71 |

|

|

|

|

Farrow-to-finish |

|

|

|

|

|

|

| |

Slaughter hogs |

52.10 |

56.00 |

52.51 |

52.46 |

|

|

Grow-to-finish |

|

|

|

|

|

|

| |

Slaughter hogs |

51.86 |

56.65 |

|

|

52.49 |

|

Combination |

|

|

|

|

|

|

|

Weanlings |

92.98 |

|

98.82 |

112.37 |

|

|

|

Slaughterhogs |

55.30 |

|

52.08 |

52.05 |

|

|

|

All |

|

|

|

|

|

|

| |

Weanlings |

92.54 |

|

97.47 |

112.37 |

|

|

Slaughter hogs |

52.62 |

56.63 |

52.37 |

52.24 |

52.49 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

Except for the price contract growers, who receive relatively higher prices, all producers received, on average, similar prices for slaughter hogs (52.2-52.6 pesos per kg).

Regular buyers. The market outlet for outputs in part affects prices per kilogram of output. Regular buyers differ between contract growers and independent producers, regardless of scale. Contract growers let their integrator exclusively market their output (Table 6.17). Commercial producers have a greater proportion of meat dealers/retailers and viajeros as regular buyers. Among independent smallholders, the spread of regular buyers s wider and includes neighbors, aside from meat dealers/retailers and viajeros.

Table 6.17 Differences in distribution of regular buyers for main output, and average prices received, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|||

|

Type 1 |

|

|

|

|

|

||

| |

Has regular buyer |

21.8 |

|

100.0 |

|

|

|

|

Type of regular buyer |

|

|

|

|

|

||

| |

Integrator |

|

|

|

|

|

|

|

Neighbor |

36.8 |

|

|

|

|

||

|

Viajero |

15.8 |

|

|

|

|

||

|

Meat |

42.1 |

|

50.0 |

|

|

||

|

Hotels/fastfood chains |

|

|

|

|

|

||

|

Direct consumers |

|

|

|

|

|

||

|

Hog raisers |

|

|

50.0 |

|

|

||

|

Cooperative |

5.3 |

|

|

|

|

||

|

Total |

100.0 |

|

100.0 |

|

|

||

|

Proportion of output picked-up by regular buyer* |

85.1 |

|

100.0 |

|

|

||

|

Average premium price |

1462.5 |

|

|

|

|

||

|

Average regular price |

1262.5 |

|

|

|

|

||

|

All other types |

|

|

|

|

|

||

| |

Has regular buyer |

69.1 |

100.0 |

93.8 |

94.1 |

100.0 |

|

|

Type of regular buyer |

|

|

|

|

|

||

| |

Integrator |

|

100.0 |

4.4 |

|

100.0 |

|

|

Neighbor |

10.6 |

|

4.4 |

|

|

||

|

Viajero |

31.9 |

|

40.0 |

31.3 |

|

||

|

Meat |

48.9 |

|

51.1 |

50.0 |

|

||

|

Hotels/fastfood chains |

|

|

|

18.8 |

|

||

|

Direct |

2.1 |

|

|

|

|

||

|

Hog raisers |

4.3 |

|

|

|

|

||

|

Cooperative |

2.1 |

|

|

|

|

||

|

Total |

100.0 |

100.0 |

100.0 |

100.0 |

100.0 |

||

|

Proportion of output picked-up by regular buyer* |

69.7 |

100.0 |

77.5 |

79.4 |

100.0 |

||

|

Average premium price |

58.38 |

57.36 |

53.15 |

57.14 |

57.00 |

||

|

Average regular price |

50.38 |

54.43 |

49.08 |

52.71 |

54.00 |

||

* For commercials, the proportion of output sold to the regular buyer was considered.

Source: UPLB-IFPRI LI Field Survey, 2002-03

Almost a quarter of producers lacked regular buyers. Type 1 producers generally sold piglets to neighboring farms. Of all producers, only the large independent commercial producers had access to institutional buyers, such as hotels and fast food chains.

Desired product characteristics. Buyers pay higher prices for output that exhibits particular characteristics. Table 6.18 lists such weanling and slaughter hog attributes. For both weanlings and slaughter hogs, readily visible characteristics appear to dominate over guarantee of genetic properties as criteria for meriting higher prices per unit output.

Table 6.18 Characteristics of output that received higher prices, Hog Production, Philippines 2002

|

CHARACTERISTI |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Weanlings |

|

|

|

|

|

|

Healthy looking (high |

51.6 |

|

71.4 |

80.0 |

|

|

Identifiable/Good breed |

1.6 |

|

14.3 |

|

|

|

Large size |

17.2 |

|

|

|

|

|

Thin back fat |

6.3 |

|

|

|

|

|

Good market |

4.7 |

|

14.3 |

20.0 |

|

|

Don’t know |

18.8 |

|

|

|

|

|

Slaughterhogs (%) |

100. |

na** |

100. |

100. |

na** |

|

Healthy looking (high quality) |

29.0 |

31.8 |

79.5 |

66.7 |

27.3 |

|

Identifiable/Goodbreed |

3.2 |

4.5 |

5.1 |

6.7 |

|

|

Large size |

4.8 |

0.0 |

|

|

36.4 |

|

Thin back fat |

38.7 |

27.3 |

|

|

36.4 |

|

Good market conditions* |

3.2 |

27.3 |

15.4 |

26.7 |

|

|

Don’t know |

21.0 |

9.1 |

|

|

|

|

Total |

100.0 |

100.0 |

100.0 |

100.0 |

100.0 |

* High demand, low supply, no importation

** Not applicable

For weanlings, the description of piglets as “healthy looking” was the dominant characteristic sought by buyers from medium and large independent commercial farms. The market conditions of supply and demand also mattered. For smallholder farms, while “healthy looking” was still significant, close to a fifth of the smallholders had no insight into what properties the buyers gave premium to.

For slaughter hogs, the visual property of “healthy looking” as a desired product characteristic was important across all groups. It was, however, seen as most important by operators of independent commercial farms. Smallholders and large contract growers identified “thin back fat” as a property that commanded higher prices.

Large independent farms and contract growers cited market conditions as playing a significant role in determining output prices.

As in the case of weanlings, again, almost a fifth of independent smallholders were uninformed of what product characteristics commanded higher prices.

Composition of output in total revenue. The division of output between weanlings/piglets and slaughter hogs was determined for the Type 4 (dual output) operators. Type 1 producers market only piglets/weanlings. Type 2 and Type 3 producers market only slaughter hogs (Table 6.19).

Table 6.19 Differences in composition of output in total revenue, Hog Production, Philippines, 2002

|

OUTPUT |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

||

|

Type 1 |

|

|

|

|

|

|

| |

Weanlings (%) |

100.0 |

|

100.0 |

|

|

|

Slaughter hogs (%) |

|

|

|

|

|

|

|

Type 2 |

|

|

|

|

|

|

| |

Weanlings (%) |

|

|

|

|

|

|

Slaughter hogs |

100.0 |

100.0 |

100.0 |

100.0 |

|

|

|

Type 3 |

|

|

|

|

|

|

| |

Weanlings (%) |

|

|

|

|

|

|

Slaughter hogs (%) |

100.0 |

100.0 |

|

|

100.0 |

|

|

Type 4 |

|

|

|

|

|

|

| |

Weanlings (%) |

39.6 |

|

27.2 |

15.9 |

|

|

Slaughter hogs |

60.4 |

|

72.8 |

84.1 |

|

|

|

All |

|

|

|

|

|

|

| |

Weanlin gs (%) |

37.9 |

|

12.7 |

8.4 |

|

|

Slaughter hogs |

62.1 |

100.0 |

87.3 |

91.6 |

100.0 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

For smallholder Type 4 operators, weanling sales made up a significantly greater share of sales (40%) than among commercial raisers (16-27%). Across all scales of operations, weanling/piglet sales were least significant among large-scale commercial producers.

Contract growers obtained revenue exclusively from sale of slaughter hogs; commercial independents obtained revenue predominantly from sale of slaughter hogs (87-92%); and smallholder independents had the highest percentage of revenue from sales of piglets and weanlings (38% of sales).

The relative popularity of piglet production among smallholders, whether specialized or in combination with finishing slaughter hogs, may arise from the more rapid turnover of invested capital, inasmuch as investment per head of livestock is similar across types of activities. Moreover, the purchased feed requirement for piglet production is significantly less than that in the growing and finishing stages of pig production.

Total revenue per farm from sale of output (one cycle/month). Comparing total revenue per farm across scales and production arrangements, total revenue appears to reflect scale of operations. The exception, however, is the commercial contracts, since total revenue reflects only net compensation from the integrator-not total revenue from sale of output.

For the 27 sample commercial fee contract growers, the integrators paid a fixed compensation averaging 3.1 pesos per kilogram of output (i.e., slaughter hogs). This was the amount paid if the producer met the standards on feed conversion ratio (FCR), average daily gain (ADG), and harvest recovery ratio (HR) stipulated in their contracts. If they exceeded the preset standards, the integrator gave them bonuses averaging 0.5 pesos per kilogram of output. However, if they fell below the set standards, penalties were incurred. For the sample farms, an average of 0.5 pesos per kilogram of output was deducted from the fixed compensation. Only 10 out of 27 commercial contracts in the sample were able to avail of the incentives; penalties were imposed on the rest (Table 6.20)

Table 6.20 Compensation received per unit of output, value of incentives, and value of penalties, Hog Production, Philippines, 2002

|

ENTRY |

FEE CONTRACTS* |

|

|

(PhP/head) |

(PhP/kg) |

|

|

Compensation |

268.07 |

3.09 |

|

Incentives (n=10) |

46.88 |

0.52 |

|

Penalties (n=17) |

-38.98 |

-0.47 |

*Large contracts only.

Source: UPLB-IFPRI LI Field Survey, 2002-03

On average, smallholder total revenues were only one-sixth to one-half those of medium-scale commercial operations, and one-twenty-fifth to one-eighth the revenue of the large commercial farms (Table 6.21).

Among the commercial independents, the large-scale operations earned more than four times the revenue of medium-scale commercial farms.

Table 6.21 Differences in total revenue of farm main output, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Type 1 |

18,372 |

|

98,801 |

|

|

|

Type 2 |

59,246 |

32,536 |

307,062 |

1,397,488 |

|

|

Type 3 |

55,207 |

154,736 |

|

|

184,509 |

|

Type 4 |

72,082 |

|

288,786 |

1,093,851 |

|

|

Total revenue from main output (PhP) |

46,477 |

149,423 |

292,883 |

1,236,739 |

184,509 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Among smallholder independents, Type 4 activities generated the largest average farm revenue (72,082 pesos for the cycle/month). This amounted to about four times the revenue obtained from Type 1 (farrow-to-weaning) activity, which generated the least average revenue per cycle/month.

6.3.7 Profits

Profits per kilogram of output. Among independents, the smallholders earned the highest average profit (defined as the excess of revenue over cost) per kilogram of output (26.7 pesos per kg). In comparison, commercial independents earned 19.4-20.4 pesos per kilogram output. This was influenced largely by the relatively high profit per kilogram earned from Type 1 (farrow-to-weaning) smallholders (Table 6.22).

Across activities, Type 3 (grow-to-finish) producers earned the least profit per kilogram of output. This stems mainly from the explicit costing of the weanling stocks, which aside from feeds is a major cost component in Type 3 activity.

Table 6.22 Differences in profits per kilogram from main output, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Type 1 |

44.69 |

|

17.65 |

|

|

|

Type 2 |

18.76 |

-1.20 |

19.26 |

17.39 |

|

|

Type 3 |

1.65 |

2.23 |

|

|

2.33 |

|

Type 4 |

24.52 |

|

19.98 |

23.02 |

|

|

Profit from main output (PhP/kg Q) |

26.69 |

2.08 |

19.43 |

20.37 |

2.33 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Total farm profits. Average farm profits reflect both the scale of operations and profitability. Although profit per kilogram of output was significantly higher for independent smallholders than for commercial producers, total farm profits of independent smallholders was just one-thirtieth those of the large independent commercials, one-ninth those of large contract growers, and one-seventh those of medium-scale commercials (Table 6.23).Among smallholders, the contract growers generated overall only about half the profits of independents. But in Type 3 (grow-to-finish) activity, the smallholder contract growers had close to double the farm profits of the small independents.

Among the independent growers, across all scales and types of activity, farrow-to-finish (Type 2) and combined operations (Type 4) yielded the highest profits per cycle.

While Type 1 (farrow-to-weaning) activity yielded the highest profit per kilogram of output among smallholders, total farm profits were less than half those generated either by Type 2 or Type 4 farms.

Table 6.23 Differences in total farm profits (excess of total revenue over total cost) from main output, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Type 1 |

8,428 |

|

21,s426 |

|

|

|

Type 2 |

22,063 |

-695 |

132,405 |

520,930 |

|

|

Type 3 |

3,940 |

7,070 |

|

|

143,045 |

|

Type 4 |

21,039 |

|

89,800 |

477,473 |

|

|

Total profit from main output (PhP) |

15,942 |

6,732 |

114,332 |

497,923 |

143,045 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Grow-to-finish (Type 3) operations generated the least farm profits among independent smallholders. This activity also had the least profit per unit output. This was also the least popular activity among the independent smallholders. As independents, involvement in Type 3 operations requires shelling out quite substantial cash to purchase a batch of growing stock. In contrast, contract growing arrangements were most popular for Type 3 activity, regardless of scale. Note that in this sample, contract growing in farrow-to-finish (Type 2) ended up with a loss.

Comparing smallholder contract and independent production, it is notable that while total activity revenue was three times higher for contract growers (see Table 6.21), total farm profits were only about half as much as those earned by independent smallholders considering all activity types (Table 6.23).

It must be remembered, however, that price contract grower profits are just half of total activity profits, as the other half goes to the integrator. Thus, considering pure activity profits, average smallholder profits per farm would be more or less equal between contract and independent production considering all activities. Considering Type 3 activity only, per farm contract production profits were three times higher than for independent production.

6.4.1 Access to Credit

Regardless of scale, breeding stocks are not readily obtainable on credit. The implication for smallholder participation in farrow-to-weaning activities is that to initially engage in the business, capital must be obtained from other external sources (not suppliers of breeding stock), or it must be generated from own sources (Table 6.24).

Few independent producers (less than 6%) have access to credit for growing stock. However, growing stock can be obtained under a contract growing arrangement with an integrator.

Table 6.24 Distribution on incidence of obtaining credit for breeding stock, growing stocks and for feeds, Hog Production, Philippines 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Farmers who obtained credit for breeding stock (%) |

0.0 |

na* |

2.0 |

0.0 |

na |

|

Farmers who obtained credit for growing stock (%) |

1.1 |

100.0 |

0.0 |

5.9 |

100.0 |

|

Farmers who obtained credit for feeds (%) |

17.2 |

100.0 |

54.0 |

64.7 |

100.0 |

*na=not applicable

Source: UPLB-IFPRI LI Field Survey, 2002-03

Among groups, the independent smallholders had the least access to credit for feed (17%). In contrast, smallholder contract growers had complete access to feed credit.

6.4.2 Access to production loans

The extremely low incidence of obtaining a loan for production purposes (means of 4- 10%) was not limited to smallholders. Production loans were rare among medium-scale independent commercial producers as well (Table 6.25). In comparison, incidence of obtaining production loans was relatively higher for large independents and large contract growers (24-27%).

The average rates of interest paid among groups ranged from 15.6 percent to 18.2 percent per annum.

Table 6.25 Incidence of obtaining loans for production purposes and interest rates paid, Hog Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Obtained loan for production purposes (%) |

10.3 |

4.3 |

8.0 |

23.5 |

26.7 |

|

Interest rate |

18.22 |

16.00 |

17.50 |

15.55 |

18.03 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Among those who did not apply for credit, a greater proportion of smallholders (31%) did not do so because they thought that they would not get the loan anyway. Fewer commercial-scale producers shared that perception (17-20%) (Table 6.24). The rest who did not attempt to borrow did not need a loan.

When credit is really needed, the institutions or individuals that most respondents said they would approach were the banks (32%), relatives and friends (14%), and a cooperative (12%) (Table 6.26). Interest rates were expected to be highest from the banks (12.8% per annum) and lowest from relatives (3.5% per annum).

Table 6.26 Distribution of reasons for not applying for credit, Hog Production, Philippines, 2002

|

RESPONSE |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Would not get loan (%) |

31.0 |

31.6 |

20.4 |

16.7 |

|

Did not need loan (%) |

69.0 |

68.4 |

79.6 |

83.3 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Table 6.27 Sources of credit if really needed and lowest interest rates per annum expected to be paid, Hog Production, Philippines, 2002.

|

SOURCE OF CREDIT* |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Bank |

34.5 (12.0) |

8.7 (18.0) |

36.0 (10.4) |

47.1 (15.4) |

26.7 (17.1) |

|

Relatives/Friends |

16.1 (4.9) |

21.7 (3.0) |

20.0 (3.6) |

5.9 (0.0) |

10.0 (8.3) |

|

Cooperative |

16.1 (8.3) |

17.4 (10.1) |

10.0 (8.6) |

|

10.0 (11.0) |

|

Credit Program |

1.1 (14.0) |

4.3 (20.0) |

|

|

|

|

Private Lending Firm |

3.4 (30.0) |

|

|

|

|

|

No response |

28.7 |

47.8 |

34.0 |

47.1 |

53.3 |

|

Total |

100.0 |

100.0 |

100.0 |

100.0 |

100.0 |

* Entries in parenthesis are average interest rates per annum. Source: UPLB-IFPRI LI Field Survey, 2002-03

Table 6.28 Incidence of visit by a veterinarian in the last three months, Hog Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Incidence of visit by veterinarian (%) |

24.1 |

65.2 |

60.0 |

82.4 |

83.3 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

6.4.3 Access to Animal Health Services

Veterinarian visits. The incidence of a visit by a veterinarian in the last three months was low for independent smallholders (24%) (Table 6.28). Smallholders on contract reported a relatively higher incidence of veterinarian visits (65%). Medium-scale commercial independents had about the same rate of incidence of veterinarian visits as smallholder contract growers (60%).

Among commercial producers, the large independents and large contract growers had the highest incidence of veterinarian visit in the last three months (83%).

Indications of effects of animal health services. Animal mortality rates appear to be higher, on average, among independent producers (Table 6.29). By scale of operations, small contract growers had about the same animal mortality rates as their larger counterparts. Among independent growers, except for medium-scale commercials, there was no significant difference in mortality rates between smallholders and commercials.

Table 6.29 Mortality rates and major causes of mortality, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

||

|

Mortality rate |

11.90 |

9.73 |

16.05 |

11.80 |

9.74 |

|

|

Major causes of mortality |

|

|

|

|

|

|

| |

Crushed |

45.9 |

0.0 |

23.9 |

15.7 |

0.0 |

|

Disease |

47.3 |

95.2 |

67.3 |

66.7 |

49.3 |

|

|

Injured |

6.8 |

4.8 |

1.8 |

7.8 |

1.4 |

|

|

Scouring |

0.0 |

0.0 |

0.0 |

0.0 |

2.8 |

|

|

Heatstroke |

0.0 |

0.0 |

5.3 |

3.9 |

14.1 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03

6.4.4 Access to Other Services; Delivery of Inputs to Farm

Less than half of the independent producers enjoyed delivery of growing stock to the farms, with smallholders having this service the least (16%) (Table 6.30). A higher proportion of large independent producers (47%) enjoyed delivery services of growing stock compared to medium-scale commercials (32%). All contract growers, regardless of scale, availed of such delivery services.

Table 6.30 Delivery services of growing stock to farm, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Growing stock delivered (%) |

16.1 |

100.0 |

32.0 |

47.1 |

100.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

None of the independent smallholders had feed delivery services to the farms; while contract growers, regardless of scale, enjoyed feed delivery to the farm (Table 6.31). Among independent commercial producers, a significantly higher proportion of large-scale farms (65%) enjoyed feeds/ingredients delivery to the farm, compared to medium-scale producers (36%).

Table 6.31 Delivery services of feeds/feed ingredients to farm, Hog Production, Philippines 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Feeds/feed ingredients delivered (%) |

0.0 |

100.0 |

36.0 |

64.7 |

100.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

As with access to credit and veterinary services, it is apparent that large and medium-scale independent commercial farms have distinct and differential access to production services, with large independents having the greatest and most consistent advantage.

6.4.5 Access to Telecommunications Facilities

Ownership of a cell phone or two-way radio system. In general, access to cellular telephone services or a two-way radio system is relatively high, even among smallholders (70%) (Table 6.32). Access to such telecommunications infrastructure, however, was significantly higher among commercial farms (92-97%).

Table 6.32 Ownership of a cell phone/2-way radio, Hog Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Owns cell phone/2-way radio (%) |

69.0 |

69.6 |

92.0 |

94.1 |

96.7 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Access to public phone system. In contrast to access to telecommunications infrastructure, access to a public telephone system is relatively lower (20-61%) (Table 6.33).

Surprisingly, more smallholders (56%) had access to a public phone system than commercial farmers. Access is least among commercial contract growers (20%) and large independents (29%).

The above, however, does not imply an advantage to the smallholders in terms of communication facilities for obtaining market information. With the development of mobile communications technology and relatively easy access to the same, the significance of public telephone systems has all but vanished.

The pattern of access to public phone systems may simply depict the underdeveloped state of Philippine public telephone systems, particularly farther away from residential areas and peri-urban centers, where smallholders are located.

Table 6.33 Access to a public telephone system, Hog Production, Philippines 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Access to public phone |

50.6 |

60.9 |

46.0 |

29.4 |

20.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

6.4.6 Access to Market Information

Sources of market information varied according to scale of operations and production management. For contract growers, regardless of scale, the integrator or cooperative/integrator served as the dominant source of market information (67-73%). Smallholder contract growers also looked to public markets as an information source. This is to be expected when the main market outlet is the local meat market (Table 6.34).Among independent farms, both smallholders and medium-scale commercial producers cited their neighbors and friends as dominant sources of market information (37%). For smallholders, the second most popular source of market

This is to be expected when the main market outlet is the local meat market (Table 6.34).Among independent farms, both smallholders and medium-scale commercial producers cited their neighbors and friends as dominant sources of market information (37%). For smallholders, the second most popular source of market information was the viajeros (20%). For medium-scale commercials, it was traders’ agents (27%).

Traders’ agents were the most popular source of market information among large independent commercial farms (60%). Second in importance was their own hog raisers’ organization (27%). It is apparent that, apart from the contract growers, the large independent producers are the most formally organized (into their respective hog producers’ associations). In contrast, producers’ organizations as a source of market information were significant to only 10 percent of the medium-scale commercial independents.

Table 6.34 Distribution of farmers by main source of market information, Hog Production, Philippines, 2002.

|

SOURCE OF MARKET INFORMATION (%) |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Medium Independent |

Large Independent |

Contract |

|

|

Media |

13.3 |

4.8 |

12.2 |

6.7 |

4.5 |

|

Neighbors/Friends |

37.3 |

0.0 |

36.6 |

13.3 |

13.6 |

|

Agents |

5.3 |

0.0 |

26.8 |

60.0 |

4.5 |

|

Cooperatives |

0.0 |

|

9.8 |

6.7 |

|

|

Integrator/Cooperative |

0.0 |

66.7 |

0.0 |

0.0 |

72.7 |

|

Public Market |

10.7 |

23.8 |

14.6 |

0.0 |

0.0 |

|

Other farms |

17.3 |

14.3 |

4.9 |

13.3 |

4.5 |

|

Viajeros |

20.0 |

14.3 |

0.0 |

0.0 |

0.0 |

|

Veterinarian |

0.0 |

0.0 |

4.9 |

0.0 |

0.0 |

|

Organization |

0.0 |

0.0 |

9.8 |

26.7 |

0.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03

Consistent with these observations, the medium-scale commercial producers may be more aptly described as ‘scaled-up’ images of smallholder farrow-to-finish or combined operations, rather than as smaller versions of the large-scale independent farms.

The pattern of involvement of smallholders in various types of activity in hog production is consistent with the pattern of investment requirements, profit per unit output, and total farm profits for the respective types of operations. Producers can maximize farm profits by undertaking the whole spectrum of activity: farrow-to-finish or farrow-to-finish combined with the occasional selling of piglets. This enables them to reap the gains from selling slaughter hogs at the optimal time, considering output and feed prices and the opportunity cost of money. To get in the business however, producers must have the initial capital to build the breeding stock (sows). Also, they must be capable of continuously financing feed consumption for up to six months or more after the birth of the piglets.

Another salient points emerging from the overview of hog production activities is that

The engagement of smallholders in a combination of activities (Type 4)-farrow-to-finish and farrow-to-weaning operations-provides flexibility in the timing of the flow of revenue. Income can immediately be realized by selling a portion of the stock as piglets or weanlings. That cash can then be used to finance feed expenditures for the remaining growing stock and for other purposes. To engage in Type 4 operations, a producer must have sufficient scale to exercise flexibility while still remaining a smallholder (e.g., 5-6 sows, 40-50 growing stock).

Not all smallholders with the potential to engage in pig production have the capital to invest in breeding stock on a scale sufficient to generate a continuous flow of income, at least on a monthly basis. Smallholders who are able to get access to some capital are likely to engage in farrow-to-weaning (Type 1) activities. Using mainly family labor and with one or two sows, Type 1 operations allow for the production and selling of piglets at a rapid rate of turnover of capital, with regular feed expenditures mainly for the sow(s) and with ample time left over to engage in other income-generating activities. Type 1 activity may generate the highest profit per kilogram of output (due to the relatively high price of piglets per kilogram live-weight). However, due to the relatively small scale of operations it is insufficient as the primary source of household income. As a sideline activity, Type 1 activity is unlikely to be dynamic in adopting technological advances in breeding, such as high-quality piglets to be used as inputs for those specializing in grow-to-finish activities. For this reason, the market for piglets or weanlings for smallholder independents are the neighboring smallholder pig raisers.

The close to non-engagement by independent smallholders in strictly grow-to-finish (Type 3) operations, in contrast to the almost complete specialization of contract growing in this same activity, points to the risks of solely or independently undertaking this venture. The relative share of the cash cost of stock is highest in this activity. To maximize the profit-generating possibilities of this activity, it is crucial that the potentials presented by technological advances in pig production be exploited, applying advances in genetics, animal nutrition, and animal health. Hence, explicit importance is given to the parameters of feed conversion ratio (FCR) and harvest recovery ratio (HR) in fee contracts. Realizing these potentials, however, requires that smallholder manage their enterprise seriously, strictly as a business.

Contract production is the dominant arrangement for Type 3 operations, regardless of scale. This points to the complementarity of the resources that the smallholders (and other producers) have (i.e., land, facilities, family labor, management capability) and those that a potential investor might have (capital, technology, access to markets) and is willing to risk for some expected return. Average profit per kilogram of output is relatively thin (in fact is thinnest) in Type 3 activity. The production cycle, however, is shortest at three to four months (covering growing and finishing stages only), and the turnover is fastest (up to three cycles per year for the all-in, all-out mode). Thin profit margins are compensated for by the significantly larger scale of operations, particularly in fee contracts. This is demonstrated by the large-scale commercial contract growers (‘large-scale’ and ‘commercial’ are used interchangeably in this report), which generate the second-highest average farm profits among the commercial producers (143,045 pesos from the last cycle).

![]()

![]()

![]()