![]()

![]()

![]()

This chapter presents the characteristics of the broiler and hog farm households surveyed, including farm characteristics, production performance, and access to inputs and services. Section 5.1 discusses the broiler farms and section 5.2 focuses on the hog farms.

5.1.1 Household Head

Age. The household (HH) head is the decision-maker on the farm. The mean age of the HH head was 42 years. This was more or less even across the sub-samples. (Table 5.1).

Gender. HH heads were mostly men (88%). However, the independent producers differed somewhat from the contract growers in this respect. While almost all contract grower households were headed by a man (95%), about 20 percent of the independent producer households were female-headed.

Civil status. Most of the HH heads were married (84%), with a more or less even distribution across the sub-samples except for commercial contract growers, whose proportion of married HH heads was highest at 94 percent.

Table 5.1 Characteristics of household head/decision maker of Broiler Production, Philippines

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Age (years) |

41.7 |

42.4 |

41.5 |

42.0 |

|

Gender (Male, %) |

77.4 |

96.8 |

82.6 |

93.5 |

|

Civil Status (Married, %) |

67.7 |

74.2 |

78.3 |

87.1 |

|

Education (no. of years) |

10.9 |

11.0 |

13.8 |

13.3 |

|

Main occupation (%) |

74.2 |

90.3 |

91.3 |

93.5 |

|

Secondary occupation (%) |

48.4 |

38.7 |

39.1 |

54.8 |

|

Experience in livestock |

7.6 |

9.8 |

10.0 |

9.5 |

|

Any formal education related to animal science or business management? (%) |

6.5 |

12.9 |

47.8 |

29.0 |

|

Any training in livestock or business management? (%) |

48.4 |

45.2 |

47.8 |

71.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Schooling. There were differences between the smallholder and commercial samples in the HH head’s number of years of schooling. The mean among smallholders was lower at 11 years compared to 14 years for HH heads in the commercial sample.

Occupation. Most of the HH heads reported the broiler business as being their main occupation. The broiler business was, however, significantly more important among the contract growers and independent commercial producers. In these categories, more than 90 percent listed the broiler enterprise as their main occupation.

Among the independent smallholders, about 26 percent of HH heads had involvements other than the broiler business as their main occupation.

Close to half (46%) of HH heads were involved in a secondary occupation outside the broiler business. The incidence of the HH heads having a secondary source of income was highest (55%) among the commercial contract growers.

Farming and business background. Average years of experience of HH heads in the broiler business was lowest for the independent smallholders, at about eight years. The rest of the categories had nine to ten years of experience in the business.

The commercial producers had higher exposure to formal education in animal science or business management. Close to half (48%) of HH heads on independent commercial farms, and close to 30 percent of commercial contract growers, had formal exposure to animal science and business education. In contrast, some 90 percent of smallholder HH heads had no exposure to formal education in these fields.

As to attendance at livestock and business training programs in the last two years, only the commercial contract growers were relatively highly exposed. About 70 percent reported having attended at least one training program. Less than half of the rest of the HH heads had had any exposure at all to such training programs in the last two years.

5.1.2 Spouse of the HH head

Age, gender, civil status, and education. The average age of the spouse of the HH heads was about 42 years (Table 5.2). The mean was more or less even among sub-samples. The spouses were predominantly female.

In terms of number of schooling years, the spouses of commercial raisers had been in school longest with 13-14 years’ schooling on the average. For smallholders, the average was 11-12 years.

Occupation. In terms of the degree of involvement, a greater majority (84%) of the spouses on independent commercial farms considered the broiler business as their main occupation. In the other farm categories, about half of the spouses had main occupations other than the broiler business.

Table 5.2 Characteristics of spouse of household head/decision maker, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Age |

41.7 |

42.4 |

41.5 |

42.0 |

|

Gender (Female, |

77.4 |

96.8 |

82.6 |

93.5 |

|

Civil Status (Married, |

67.7 |

74.2 |

78.3 |

87.1 |

|

Education (no. of |

11.0 |

11.7 |

13.5 |

12.9 |

|

Main Occupation |

48.0 |

50.0 |

84.2 |

51.7 |

|

Level of involvement |

64.0 |

62.5 |

73.7 |

58.6 |

|

Type of involvement |

46.4 |

71.4 |

96.0 |

95.5 |

|

Direct |

53.6 |

28.6 |

4.0 |

4.5 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

For the spouses whose main occupation was the broiler business, engagement in a secondary occupation was not prevalent.

Spouse engagement in the broiler business. In all subgroups, a majority (60%) of the spouses worked or assisted in the broiler business. The nature of their role, however, differed significantly between the commercial producers and smallholders. A large proportion (96%) of spouses on the commercial farms performed some managerial functions (supervising, keeping the finances and books). Engagement in such functions was least common among spouses of independent smallholders (46%), though higher among spouses of smallholder contract growers (71%).

Thus, among commercial producers and contract growers, the spouses performed important managerial functions.

5.1.3 Other HH members

The average household size of the sample was about five (Table 5.3). This average was about even among all subgroups. Involvement in farm business by other HH members was also about the same across the subgroups with an average of two members involved.

Average monthly expenditure was about 10,000-12,000 pesos among smallholders, 15,000 pesos among commercial contract growers, and about 33,000 pesos among independent commercial farms. Average monthly expenditures are taken as a proxy of average monthly income from all sources.

Table 5.3 Household size, number involved in the livestock business, average Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Household size |

5.3 |

5.4 |

5.0 |

4.8 |

|

Number involved in livestock |

2.5 |

2.2 |

2.4 |

2.2 |

|

Average monthly expenditure (PhP) |

9,78 |

11,70 |

33,43 |

15,36 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

5.2.1 Major Crops

There was a higher incidence of crops being grown on the commercial farms (54%) compared to the smallholders farm (34%). Where crops were grown, the average area under crops was about four hectares in independent commercial farms and about one hectare on commercial contract farms (Table 5.4). For smallholders, the area was less than half a hectare (0.4 ha). The most popular crops grown on all farms were fruit trees (up to 32% of respondents).

Table 5.4 Area of landholding, area for livestock, area for other crops, major Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Area of landholding (haa) |

0.5 |

0.6 |

2.3 |

1.7 |

|

|

Area for livestock (ha) |

0.5 |

0.6 |

2.3 |

1.7 |

|

|

Area for other crops (ha) |

0.5 |

0.3 |

4.1 |

1.0 |

|

|

Major crops planted (%) |

|

|

|

|

|

|

Fruit trees/tree |

32.3 |

12.9 |

22.6 |

32.3 |

|

|

Cereals |

3.2 |

9.7 |

3.2 |

3.2 |

|

|

Sugarcane |

|

|

3.2 |

|

|

|

Others |

|

|

3.2 |

|

|

a Area for other crops is outside the area of landholding.

Source: UPLB-IFPRI LI Field Survey, 2002-03.

5.2.2 Land Characteristics

Regarding the land classification of the site of the farms, 70-90 percent of the contract farms were classified as agricultural lands (Table 5.5). Independent smallholder farms were mostly (68%) situated on non-agricultural lands. About half (52%) of independent commercial farms were located on non-agricultural lands.

On the average, the smallholder independent farms were closer to their main output market (11 km). The rest were at least three times farther away. The small farms were also much closer to their source of feed (5 km) than were the commercial farms (31-39 km). Evidently, the independent smallholder farms obtained their feeds from the closest town, while the small contract growers had their source of feed a little father away (11 km). Commercial farms did not source their feeds from the closest town.

In terms of distance to the main output market, the contract growers and independent commercial farms had a main output market far away from the closest town (more than 30 km away on average). The smallholders, in contrast, sell their output at a market much closer to the production site (11 km away). Thus, commercial producers and contract growers appear to have a different output market from the independent smallholders.

Table 5.5 Classification of landholding, distance to main markets for inputs to nearest bodies of water, and to nearest settlement, Broiler Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Land classification |

|

|

|

|

|

|

Agricultural |

32.3 |

71.0 |

47.8 |

87.1 |

|

|

Non-agricultural |

67.7 |

29.0 |

52.2 |

12.9 |

|

|

Distance to main of output (km) |

10.9 |

44.7 |

30.9 |

35.7 |

|

|

Distance to main |

|

|

|

|

|

|

of feed (km) |

4.7 |

11.0 |

39.2 |

30.6 |

|

|

Distance to nearest body of water (km) |

|

|

|

|

|

|

Stream |

0.4 |

1.5 |

0.3 |

1.9 |

|

|

River |

1.4 |

1.1 |

3.6 |

1.4 |

|

|

Lake |

0.2 |

11.5 |

6.5 |

6.3 |

|

|

Distance to nearest settlement (km) |

0.2 |

0.7 |

1.0 |

0.6 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03.

The broiler farms are relatively close to water bodies. For independent smallholders in the sample, the nearest body of water was a lake, about one-fifth of a kilometer away. For independent commercial operations, the nearest body of water was a stream about one-fourth of a kilometer away on average. For contract growers, the nearest body of water was a river one to one-and-a-half kilometers away on average.

5.2.3 Access to Utilities

Piped-in water supply. Relatively few of the farms were connected to a municipal piped-in water supply (Table 5.6). The incidence of not being connected, however, was higher for commercial farms (87-96%) than for smallholder farms (61-64%). This is associated with the smallholder farms being located a little closer to town than commercial farms.

Table 5.6. Access to utilities, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Access to piped-in water |

38.7 |

35.5 |

4.3 |

12.9 |

|

Access to electricity |

100.0 |

100.0 |

100.0 |

100.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Power supply. All farms, regardless of scale and production arrangement, had access to main sources of electrical power.

5.3.1 Type of Activity and Production Cycle

The dominant manner of phasing production activities among the broiler farms was the ‘all-in, all-out’ mode, covering 93 percent of the entire sample (Table 5.7).

The contract growers had a higher turn-around rate in the production cycle, and were able to turn out an average 5.3 batches per year. Independent smallholders could manage 4.3 batches per year.

5.3.2 Size of Holdings

Broiler producers were categorized as smallholders (with holdings of 10,000 birds or less) and commercials (with holdings of more than 10,000 birds).

Table 5.7 Distribution (%) by type of activity in livestock production, Broiler Philippines 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

All-in-all-out |

90.3 |

96.8 |

87.0 |

96.8 |

|

Multi stage |

9.7 |

3.2 |

13.0 |

3.2 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

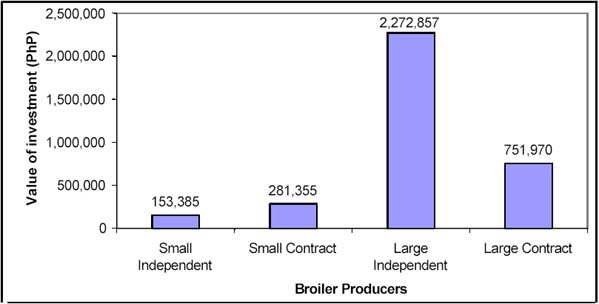

Among smallholders, independents had a very small holding size, with a mean of 1,114 birds. Some farms had as few as 100 birds and the maximum was 5,000 (Figure 5.1 and Table 5.8). Half of the sample had holdings of 500 birds or less. Smallholders with contract arrangements had relatively larger flocks, with a mean of 5,158 birds. Maximum holdings were as high as 9,000 birds, with half of the smallholder contract growers having more than 6,000 birds. Clearly, engagement in formal contracts enabled smallholders to hold significantly larger flocks, in this case close to five times larger than those of independent smallholders evaluated at the mean.

Figure 5.1 Size of current inventory by production arrangement and scale of operation, Hog Production, Philippines 2002

Table 5.8 Size of current flock inventory, value of total investment, and average value of investment per animal, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Inventory size |

1,114 |

5,158 |

29,289 |

20,958 |

|

Total investment |

153,385 |

281,355 |

2,272,857 |

751,970 |

|

Investment per bird (PhP/bird) |

167 |

61 |

91 |

37 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Among commercial producers, the discrepancy between the average holdings of independent producers (29,289 birds) and those of contract growers (20,958 birds) was smaller than that among the smallholders. The independents held as many as 108,000 birds, while the maximum for contract growers was 75,000.

5.3.3 Total Investment and Investment per Animal Head

Total investments. Total investments in breeding stock and in facilities and equipment were quite small among smallholders compared to commercial producers (Figure 5.2 and Table 5.8). Among smallholders, the contract growers’ mean value of investments (281,355 pesos) was close to double that of independent smallholders (153,385 pesos).

Figure 5.2 Value of total investment by production arrangement and scale of operation, Hog Production, Philippines 2002

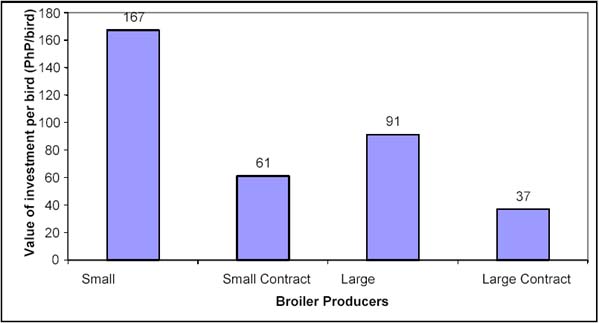

Average investment per bird. On a per bird basis, smallholder independents had the highest investment per bird, at 167 pesos. Large contract growers had the lowest per bird investment, at 37 pesos (Figure 5.3 and Table 5.8). The contract growers tend to have lower value of investments per bird because their integrators provide for the value of their flock.

5.3.4 Employment of Hired Workers

On average, the number of hired workers per farm was about six on the commercial farms, two on the smallholder contract farms, and one on the small independent farms (Table 5.9). Few smallholder farms have hired help.

Table 5.9 Average number of hired workers employed, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Number of hired labor |

0.5 |

1.8 |

6.1 |

5.2 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Figure 5.3 Total value of investment per bird, by production arrangement and scale of operation, Hog Production, Philippines 2002

5.3.5 Prices of Day-Old Chicks

Smallholders paid relatively higher prices for day-old chicks (15.3 pesos on average) compared to commercial raisers, who could purchase the chicks at average 13.4 pesos each (Table 5.10). Small contract growers, however, paid even higher prices 16.9 pesos per bird, as priced by their small integrators.

Table 5.10 Differences in prices paid for day-old chicks, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Price of day-old chicks (per |

15.3 |

16.9 |

13.4 |

|

|

Price of DOC for fee |

|

0.0 |

|

0.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

5.3.6 Feeds

Average feed price by type. The major feed types used were booster, starter, and finisher feeds. Commercial independent producers paid slightly less than smallholder independents per kilogram of feed (14.2 pesos per kg compared to 14.3 pesos) (Table 5.11). The difference, however, was not statistically significant. This holds true for feeds that commercial producers purchased on the market and for those they mixed on their own. On average, own mixed feeds cost more (14.3 pesos per kg) than feeds bought on the market (14.2 pesos).

Table 5.11 Differences in weighted price paid per kilogram of feed (PhP/kg), Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Weighted feed (PhP/kg |

14.33 |

13.06 |

14.24 |

|

|

Weighted feed price fee contracts (PhP/kg) |

|

0.0 |

|

0.0 |

* Weighted price of feed paid by profit-sharing contract growers.

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Feed costs per kilogram of output. Feed costs per kilogram of output were only slightly lower for large producers, at 29.8 pesos per kilogram live-weight compared to 30.4 pesos for smallholders (Table 5.12). Profit-sharing contract growers pay the full price for feed. Fee contractors purchase feeds on the commercial market, which is why some feed cost values are positive.

Table 5.12 Differences in feed cost per kilogram of output, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Profit Sharing (n=8) a |

Fee Contracts (n=16) b |

Independent |

Contract b |

|

|

Feed cost per(PhP/kg of |

30.3 |

26.8 |

14.0 |

29.8 |

0.9 |

a These are the respondents integrated other than SMFI whose feed cost are paid to their integrator after Excludes additional feed consumption not provided by the integrator.

b Includes additional feed consumption not part of those provided by the integrator.

Source: UPLB-IFPRI LI Field Survey, 2002-03.

5.3.7 Costs

Cost structure in broiler production, with and without contracts. Cost structure is similar for small and large independent farms. Feed costs comprise 65-70 percent of total cost, while outlays for day-old chicks account for about 20 percent of total production costs (Table 5.13).

Table 5.13. Differences in structure of major variable cost components, Broiler, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||||

|

Independent |

n |

Contra |

Independent |

n |

Contract |

|

|

Day-old |

20. |

8.0 |

20. |

19. |

|

|

|

Feed |

65. |

16. |

57. |

70. |

3.0 |

4.1 |

|

Hired |

1.7 |

26. |

7.4 |

2.5 |

31. |

34. |

|

Vaccines and veterinary |

2.4 |

12. |

3.1 |

2.9 |

16. |

13. |

|

Utilities (water and |

2.9 |

31. |

4.5 |

0.8 |

31. |

17. |

|

Facilities and |

1.5 |

20. |

1.7 |

0.4 |

25. |

9.2 |

|

Other |

5.9 |

31. |

5.8 |

3.2 |

31. |

21. |

* Other costs include depreciation, other operating and maintenance cost, and cost of waste disposal, among others.

Surprisingly, small contract growers have a comparable cost structure. This is due to the presence of price contractors who pay for day-old chicks and feeds after harvest.

The commercial fee contractors, however, have an entirely different cost structure. They do not pay for day-old chicks. Some feeds are purchased, but only nominally. Hired labor (34%) and utilities (17%) form the main cost components.

Considering variations in contracts, Table 5.14 shows the respective costs per kilogram of output by scale and type of contract.

Table 5.14. Differences in cost per unit of output, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Average cost (PhP/kg output) |

46.6 |

12.6 |

42.1 |

|

|

|

Profit-sharing |

|

39.8 |

|

|

|

|

Fee contracts |

|

3.1 |

|

2.2 |

|

|

Average cost (PhP/batch) |

87,982 |

|

1,756,627 |

|

|

|

Profit-sharing |

|

75,044 |

|

|

|

|

Fee contracts |

|

35,738 |

|

74,876 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Independent smallholders incur the highest per unit costs (46.6 pesos per kg), followed by independent large producers (42.1 pesos per kg). Profit-sharing (price) contractors incurred per unit costs of 39.8 pesos.

For fee contractors, costs per kilogram were only 3.1 pesos for small contractors and 2.2 pesos for large contractors.

5.3.8 Revenue

Prices received for output. Average prices received for output varied among the subgroups. Smallholder independents received the highest price, at 48.2 pesos per kg, compared to 41.6 pesos per kg received by the commercial independent producers (Table 5.1.15). Smallholder contract producers received slightly higher prices than large commercials, at 7.8 pesos per kg compared to 6.1 pesos, respectively.

Regular buyers. Meat dealers and retailers form the largest group of regular buyers of smallholder independents (42%), followed by the viajeros (39%), who are wholesale traders/haulers (Table 5.16). Commercial independents relied more on viajeros (57%) than on the local meat dealer/retailer.

For all types of regular buyers, the smallholder independents received the highest price per kilogram output.

Table 5.16 Differences in distribution of regular buyers for main output, and prices received, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Regular buyers |

|

|

|

|

|

|

Integrator |

|

|

|

|

|

|

Fee contracts |

|

100.0 |

|

100.0 |

|

|

Profit sharing |

|

|

|

|

|

|

Viajero |

38.7 |

|

56.5 |

|

|

|

Meat |

41.9 |

|

43.5 |

|

|

|

Others |

19.4 |

|

8.7 |

|

|

|

Average price |

|

|

|

|

|

|

Integrator |

|

6.3 |

|

6.1 |

|

|

Viajero |

45.7 |

|

42.5 |

|

|

|

Meat dealer/retailer |

47.1 |

46.0 |

42.5 |

|

|

|

Others |

50.0 |

46.3 |

49.0 |

|

|

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Output price variation. Broiler producers experienced some price volatility, with higher prices received for some output and lower prices for others and prices varying per batch.

The price variations were generally attributed to physical attributes of the output (weight, full-breastedness), and temporal demand and supply conditions. The degree to which these product characteristics and market conditions affected the various participants varied according to scale of operations and production arrangement.

For smallholder independents, both product characteristics (shape, weight) and market conditions featured prominently in determining the price received. Among the four subgroups, the smallholder independents cited high demand/short supply as the most important in determining when a high price was received (42%) (Table 5.17).

Table 5.17 Characteristics of output for high and low prices by type of arrangement Production and by scale of operation, Broiler Production, Philippines, 2002.

|

ITEM |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Reasons for high price received |

|

|

|

|

|

|

Full |

45 |

39 |

70 |

29 |

|

|

Heavy |

39 |

52 |

74 |

45 |

|

|

Large demand/short |

42 |

13 |

30 |

13 |

|

|

No |

3 |

29 |

13 |

23 |

|

|

Total |

129 |

132 |

187 |

110 |

|

|

Reasons for low price received |

|

|

|

|

|

|

Pointed |

19 |

6 |

52 |

13 |

|

|

Light/thi |

65 |

84 |

87 |

65 |

|

|

Large |

39 |

10 |

17 |

3 |

|

|

No |

3 |

29 |

13 |

23 |

|

|

Total * |

126 |

129 |

170 |

103 |

|

* There are multiple

Source: UPLB-IFPRI LI Field Survey

For large independent producers, product characteristics mattered most in determining the prices received, with full-breastedness and bird weight almost equal in importance. It was in this subgroup that product characteristics featured most strongly.

The large independents ranked second to small independents in reporting conditions of high demand resulting in higher prices received (30%),

For contract growers, the most cited reason for receiving higher prices was heavy weight of output. Smallholder contract growers cited the product attribute of full-breastedness as most determinant of high prices received (39%), more often than their larger-scale counterparts (29%). For both, excess demand hardly mattered in the incidence of receiving higher prices.

When the price received was lower than normal, all subgroups reported the lightness or thinness of broilers as mattering most (74%). Market conditions (excess supply) featured prominently only among the small independent producers (39%). For product characteristics, the pointedness of the breast mattered more among the large independents (52%).

In general, the product attributes of weight and breast shape were important determinants of output prices. Market demand and supply conditions, however, carried greater significance for small independent producers and to a lesser degree for large independents.

Total revenue. Total revenue of contract growers, regardless of scale, reflects net compensation from the integrator and not sales of output. Compensation in fee contracts is fixed per bird, but incentives are provided for better than standard performance, while penalties are imposed on producers who fall below the standard performance set by the integrators. The fixed base compensation for smallholder contract producers averaged 6.4 pesos per kg, while it was 6.5 pesos per kg for large contractors (Table 5.18).

Table 5.18 Compensation received per kilogram of output, value of incentives, and value of penalties, Broiler Production, Philippines, 2002.

|

ENTRY |

FEE CONTRACTS |

|

|

Smallholder |

Commercial |

|

|

Compensation (PhP/kg) |

6.4 |

6.5 |

|

Incentives (n=14) |

1.0 |

1.1 |

|

Penalties (n=17) |

-0.7 |

-0.9 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

For contract growers who gained incentives (n=14), the equivalent value additionally gained was 1.0 peso per kg by small contractors and 1.1 peso per kg by large contractors.

For those who fell below standards (n=17), the equivalent value of penalties deducted from the base fees was 0.7 pesos per kg for smallholder contractors and 0.9 pesos per kg for large contractors.

Table 5.19 shows the total revenue for the last loading and harvest (cycle). The largest revenue was earned by large independents, at 1.85 million pesos. This was some eight times larger than the revenue earned by the large contract growers. The smallest revenue was generated by the small independents. Their revenue was only five percent that of the large independents.

Table 5.19 Differences in total revenue of farm from main output, Broiler Philippines, 2002.

|

ENTR |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Total revenue |

48.2 |

16.6 |

43.2 |

|

|

|

Profit- |

|

46.3 |

|

|

|

|

Fee |

|

6.3 |

|

6.1 |

|

|

Total revenue |

88,582 |

|

1,850,56 |

|

|

|

Profit- |

|

94,271 |

|

|

|

|

Fee |

|

77,043 |

|

229,001 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-

5.3.9 Profits

Profit per kilogram of output. Table 5.20 shows the profit per kilogram of output and per batch for the different groups of producers. In general, the contract growers earned the highest profit per unit. Among contract growers, the profit-sharing producers earned the highest profit per unit output, at 7.4 pesos per kg. The large fee contracts were second, at 4.4 pesos per kg, followed by the small fee contractors at 3.9 pesos per kg.

The large independents reported the lowest profits per unit, at only 1.3 pesos per kg. These were bettered by the smallholder independents at 3.7 pesos per kg of output.

Table 5.20. Differences in profits per kilogram from main output, Broiler Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Profit from main (PhP/kg |

3.7 |

4.8 |

1.3 |

4.4 |

|

|

Profit- |

|

7.4 |

|

|

|

|

Fee |

|

3.9 |

|

|

|

|

Profit from main (PhP/batch |

3,728 |

41,800 |

103,546 |

|

|

|

Profit- |

|

20,786 |

|

|

|

|

Fee |

|

49,109 |

|

167,793 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Total farm profits (one cycle). The small independents earned the least total farm profits, at only 7,670 pesos (Table 5.1.21). The biggest generator of profits was the large fee contractors, who earned 164,084 pesos for the cycle. This was some 60 percent more than that earned by the large independents. The large contract producers earned four times more than the smaller contractors.

Table 5.21 Differences in total farm profits (excess of total revenue over total main output, Broiler Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Total profit from main output (PhP) |

7,670 |

40,720 |

102,586 |

164,084 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

For the same scale, contract growers generated greater profits. The profits of the smallholder independents were extremely small due to the small flock sizes kept (close to 1,000 birds on average).

Although commercial contractors had smaller flock sizes than the large independents, the large independents’ greater scale of operations did not necessarily yield larger absolute profits.

5.4.1 Access to Credit

The important variable inputs in broiler production are day-old chicks, feeds, and pharmaceuticals. Contract growers automatically obtain these inputs on credit. Among independent growers, however, less than 15 percent of smallholders and less than 25 percent of large producers were able to obtain these inputs on credit from suppliers (Table 5.22).

Table 5.22 Distribution on incidence of obtaining credit for day-old chicks, feeds, and vaccines/pharmaceuticals, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Day-old chicks |

9.7 |

100.0 |

17.4 |

100.0 |

|

Feeds |

12.9 |

100.0 |

21.7 |

100.0 |

|

Vaccines/Pharmaceutical |

3.2 |

100.0 |

17.4 |

100.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

A qualification has to be made for commercial producers on the number who were able to get inputs credit. For feeds, only eight of commercial independents depended on the market for mixed feeds; the rest mixed feeds on their own. Thus, the incidence of five commercial independents obtaining feeds on credit implies that more than 60 percent of large independents were able to obtain feeds credit.

5.4.2 Access to Production Loans

Applying for a loan from a commercial bank was extremely rare among broiler producers in the last year (3-7%), with the exception of small contract growers who reported a slightly higher incidence, at 16% (Table 5.23).

Table 5.23 Incidence of obtaining loans for production purposes and interest paid, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Obtained loans for production |

3.2 |

16.1 |

4.3 |

6.5 |

|

Interest rate paid |

27.6 |

19.8 |

11.0 |

14.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

The average rates of interest paid ranged among the subgroups from 11.0 percent to 27.6 percent per annum.

Table 5.24 Reasons for not applying for credit, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Would not get loan |

6.7 |

|

|

|

|

Did not need loan |

50.0 |

100.0 |

67.4 |

86.2 |

|

Other* |

43.3 |

|

32.6 |

13.8 |

* Because of high interest rates and risk.

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Among those who had not applied for credit, only seven percent stated that the reason for not doing so was that they would not be granted a loan anyway. The rest who did not attempt to borrow claimed they did not need the loan or they perceived the interest rates to be quite high and risky.

When credit is really needed, most of the respondents across all of the subgroups said they would go to relatives and friends (49%) or obtain it from a bank (35%) (Table 5.25).

Those who thought they could obtain credit from relatives and friends estimated the lowest interest rate they could get as, on average, about 1.3 percent per annum. Those who thought they could get a loan from a bank estimated the lowest interest rate, on average, to be about 13.2 percent per annum.

Table 5.25 Source of credit if really needed and lowest interest rates Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Source of credit if really needed |

|

|

|

|

|

|

Relatives/Friends |

44.8 |

44.8 |

70.0 |

43.3 |

|

|

Bank |

27.6 |

41.4 |

25.0 |

33.3 |

|

|

Coop |

13.8 |

6.9 |

|

3.3 |

|

|

No response |

13.8 |

6.9 |

5.0 |

20.0 |

|

|

Lowest interest rates to be paid (%) |

|

|

|

|

|

|

Relatives/Friends |

0.8 |

2.0 |

0.7 |

1.8 |

|

|

Bank |

9.7 |

14.4 |

13.8 |

14.8 |

|

|

Coop |

15.0 |

3.5 |

|

15.0 |

|

|

Average |

5.5 |

5.5 |

4.0 |

8.3 |

|

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Broiler producers’ estimations of the interest rate they could get from a bank if they needed a loan varied by scale of operations. For smallholders, the average estimate was 13.1 percent per annum. For the large producers, the average estimate was 14.3 percent per annum.

5.4.3 Access to Animal Health Services

Veterinarian visits. Access to animal health services was measured by the incidence of visits of veterinarians, personnel of a breeding or pharmaceutical company, and government extension personnel over the last three months.

In general, the incidence of visits by a veterinarian across all subgroups averaged 72 percent (Table 5.26).

Table 5.26 Incidence of visit of a veterinarian in the last three months, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Incidence of visit by veterinarian (%) |

41.9 |

90.3 |

65.2 |

90.3 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

The incidence of a visit by a veterinarian was least among independent smallholders (42% in the last three months). It was highest among contract growers, at 90 percent for both large- and small-scale operations. For large independent producers, the incidence of a visit was 65 percent.

The high incidence veterinarian visits among contract growers was associated with regular inspections carried out by the integrators according to contract. For large producers, a number may have their own animal health staff.

Indications of effects of animal health services. Animal mortality rates appear to be higher, on average, among independent producers. By scale of operations, small contract producers appear to have consistently lower animal mortality rates than their large counterparts. Among independent producers, smallholders seem to have only slightly lower animal mortality rates than their larger counterparts.

Table 5.27 Mortality rates and major causes of mortality, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

|||

|

Independent |

Contract |

Independent |

Contract |

||

|

Mortality rate (%) |

6.5 |

4.7 |

6.9 |

6.1 |

|

|

Major causes of mortality |

|

|

|

|

|

|

NCD |

|

3.2 |

8.7 |

|

|

|

CRD |

6.5 |

12. |

43. |

9.7 |

|

|

Heatstroke |

45. |

58. |

104. |

67. |

|

|

Colds |

48. |

67. |

69. |

64. |

|

|

Malaria |

3.2 |

16. |

4.3 |

12. |

|

|

Physical |

22. |

19. |

17. |

16. |

|

|

Others |

6.5 |

12. |

30. |

9.7 |

|

a Multiple responses

Source: UPLB-IFPRI LI Field Survey, 2002-03.

5.4.4 Access to other Services; Delivery of Inputs to Farm

Access to services measures the delivery of inputs to the farm. For all inputs (day-old chicks, feeds/ingredients, and pharmaceuticals), access was 100 percent among large contract growers (Table 5.28).

Table 5.28. Delivery services of day-old chicks to farm, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

DOCs delivered (%) |

67.7 |

90.3 |

78.3 |

100.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Access to these services was second highest (90%) among smallholder contract growers. The high incidence of access to delivery services is related to these producers’ contracts with their respective integrators.

Significantly less access was observed among independent producers. Access to a delivery service for day-old chicks was 68 percent among smallholder independents, which is lower than that of large independents (78%).

For feed delivery, only a third (35%) of smallholder independents obtained that service, in contrast to almost two-thirds (61%) of smallholder contractors and large independent producers (Table 5.29).

Table 5.29 Delivery services of feed/feed ingredients to farm, Broiler Production, Philippines, 2002

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Feeds/feed ingredients delivered (%) |

35.5 |

61.3 |

60.9 |

100.0 |

Source: UPLB-IFPRI LI Field Survey,

5.4.5 Access to Telecommunications Facilities

Ownership of a cell phone or two-way radio system. Access to cellular phone services was almost universal among producers, being 100 percent among large producers and a little lower among smallholders. This may be attributed to the proliferation of cell phone services (Table 5.30).

Table 5.30 Ownership of a cell phone/2-way radio Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Owns cell phone/2-way radio (%) |

87.1 |

83.9 |

100.0 |

100.0 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

Access to a public phone system. Access to public phone services is generally low (44%) due to the poor phone infrastructure in the Philippines in general, especially outside towns and residential centers. Nonetheless, among the subgroups, access to public phone services surprisingly is higher among the smallholders (48-55%) and lowest among large independents (30 -39%) (Table 5.31).

Table 5.31 Access to a public telephone system, Broiler Production, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Access to public phone (%) |

54.8 |

48.4 |

30.4 |

38.7 |

Source: UPLB-IFPRI LI Field Survey, 2002-03.

The observed pattern of access to the public telephone system may simply reflect the still underdeveloped public telephone infrastructure in the country, especially as one moves farther away from the residential and peri-urban areas where the smallholder farms tend to be located. Moreover, with the advance of mobile phone technology and other telecommunication systems, public phone systems may actually have diminished in significance, particularly for accessing market information.

5.4.6 Access to Market Information

Sources of market information varied among subgroups. For contract growers, the integrators provided the dominant source of information (72%). A distant second was other broiler raisers (37%) (Table 5.32)

Table 5.32 Distribution of farmers by main source of market information, Broiler, Philippines, 2002.

|

ENTRY |

SMALLHOLDER |

COMMERCIAL |

||

|

Independent |

Contract |

Independent |

Contract |

|

|

Integrator |

9.7 |

77.3 |

26.1 |

66.7 |

|

Viajero |

29.0 |

4.5 |

56.5 |

20.8 |

|

Meat dealer/retailer |

25.8 |

|

30.4 |

12.5 |

|

Other broiler raisers |

29.0 |

36.4 |

13.0 |

37.5 |

|

Othersa |

6.5 |

4.5 |

8.7 |

4.2 |

a Refers to information from television and datacon.

Source: UPLB-IFPRI LI Field

For large independents, the viajero was the dominant source (57%) of market information. These producers also obtained information from meat dealer/retailer (30%) and integrators (26%).

Smallholders had no single dominant source of regular market information. They relied on the viajeros (29%), meat dealers (26%), and other broiler raisers (29%).

The class of independent smallholders are producers who operate at an extremely small scale. Although they are grouped into the ‘smallholder’ category together with the small-scale contract growers, their inventory holdings are just a fifth of those operating under contracts.

While smallholders had the lowest value of total farm investments, they had the highest value of investment per bird held. Large contract growers had the least investment value per bird.

Smallholder contracts are of two types: price contracts in which profits at the end of the period are shared equally between producer and integrator and fee contracts in which a guaranteed base fee per bird is stipulated but incentives and penalties are incorporated into the contracts.

The large integrators operate through fee contracts. Small local feedmills and cooperatives operate via price or profit-sharing contracts.

Independent smallholders have extremely small holdings compared with commercial broiler producers. For smallholder contract growers, the possibility of graduating to a commercial contract grower is quite realistic.

Regardless of scale of operations, contract growers realize, on average, much higher profit per kilogram of output than independent operations. This difference becomes all the more significant when we consider that the per unit profit estimated is just a fraction of the actual per unit profits realized; the other part of which goes to the integrator.

Contract growers enjoy significantly higher access to inputs and services than independent producers. Access to inputs and services is least for independent smallholders.

The large-scale independent growers, while making the largest investments, had the narrowest profit margin. Scale is thus no guarantee for higher profits. This group is also extremely vulnerable to adverse market price fluctuations.

![]()

![]()

![]()