- ➔ Forest investment is well below what is required. Financing for the forest pathways needs to increase fourfold by 2050 if the world is to meet its climate, biodiversity and land degradation targets.

- ➔ All sources of funding – domestic government, private and official development assistance – will need to be tapped, and new approaches are emerging. For example, ecological fiscal transfers, implemented in only a few countries to date, amount to 20 times the global official development assistance for forestry.

- ➔ Redirecting socially and environmentally harmful support, and improving the regulatory environment, could release considerable funding for the forest pathways. For example, repurposing agricultural subsidies – currently almost USD 540 billion per year – to include forestry and agroforestry could help avoid the harmful impacts embodied in 86 percent of such subsidies.

- ➔ Getting finance to small-scale producers will be essential for implementing the pathways. Small producers received less than 1.7 percent of climate finance in 2019, and the situation does not appear to have improved since. New finance solutions and investment modalities that suit small-scale producers and reduce inequalities need to be shared and scaled up.

4.1 Despite the high value of forests and trees, investment in them is low. Climate finance for forestry is increasing from a low base

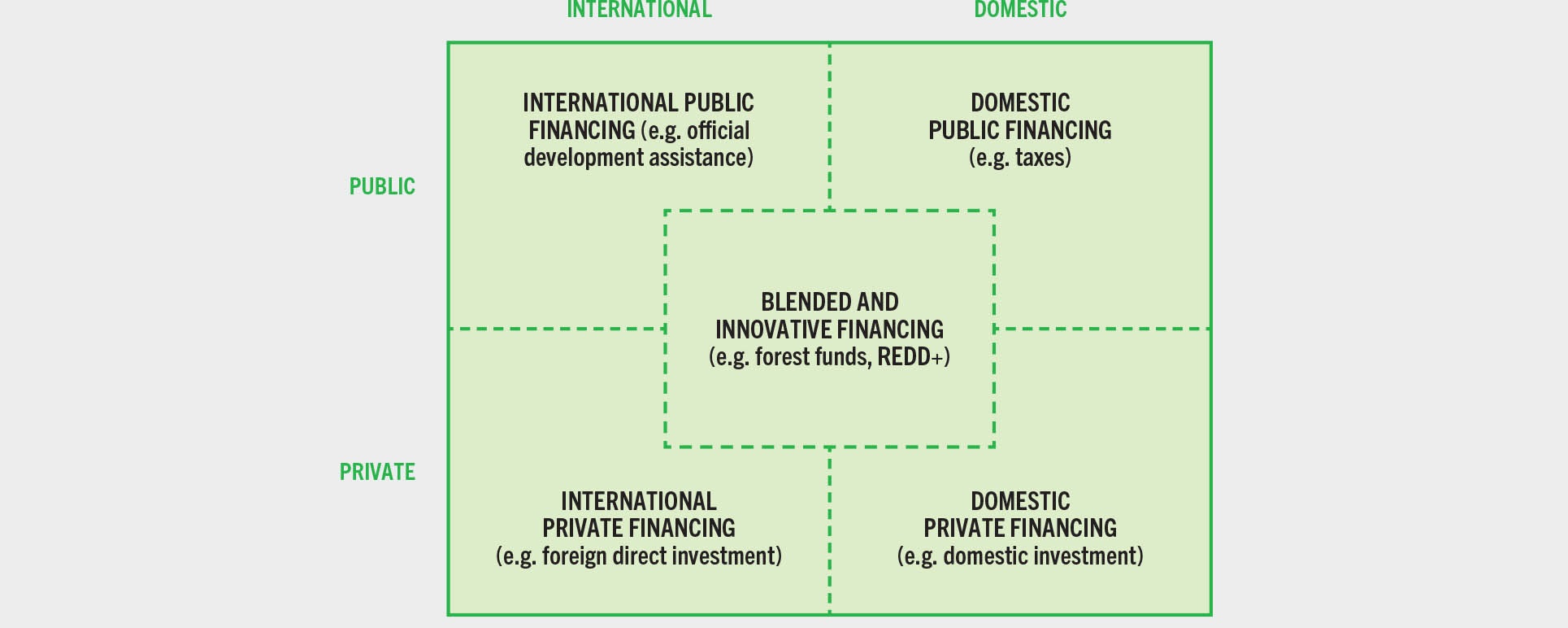

Increasing investment in the three forest pathways described in Chapter 3 requires an assessment of current financial flows, the accurate tracking of how such funds have been allocated, and identifying what must change to both redirect existing money and attract new investment. Financial sources for scaling up implementation of the forest pathways comprise international and domestic public and private resources that can operate separately or in a mix, for example using public money to catalyse private sector investment (Figure 13).

Figure 13Diversity of forest finance sources

This chapter examines existing public and private financial flows for green recovery and growth (noting that, with the exception of recovery data, all figures are pre-COVID-19 estimates); considers the funding required to meet key global targets; provides examples of how both public institutions and the private sector are increasing support for the three pathways; canvasses instruments that can be used to support small producers in implementation; and suggests options for mobilizing the additional finance needed to transition towards a greener and more sustainable future. As shown in this chapter, evidence indicates at least five high-potential areas for scaling up implementation of the forest pathways – (1) greening public domestic finance; (2) making climate finance work for forest-based approaches; (3) greening financial markets with regulatory and supervisory tools, with the clear positioning of forest-based approaches; (4) developing pipelines of investment-grade projects; and (5) supporting investment in value-added wood processing in countries of origin.

Accurately tracking flows of forest finance is important for efficient resource allocation. At present, however, not all such flows are monitored, which can lead to poor financing decisions. Existing estimates suggest that investment in forests and trees is low relative to the huge value they have for individuals, communities and societies, but there is scope for changing this.

Climate finance flows to forestry almost doubled between 2015 and 2019, but domestic public expenditure on forestry far exceeds it, even in some low-income countries

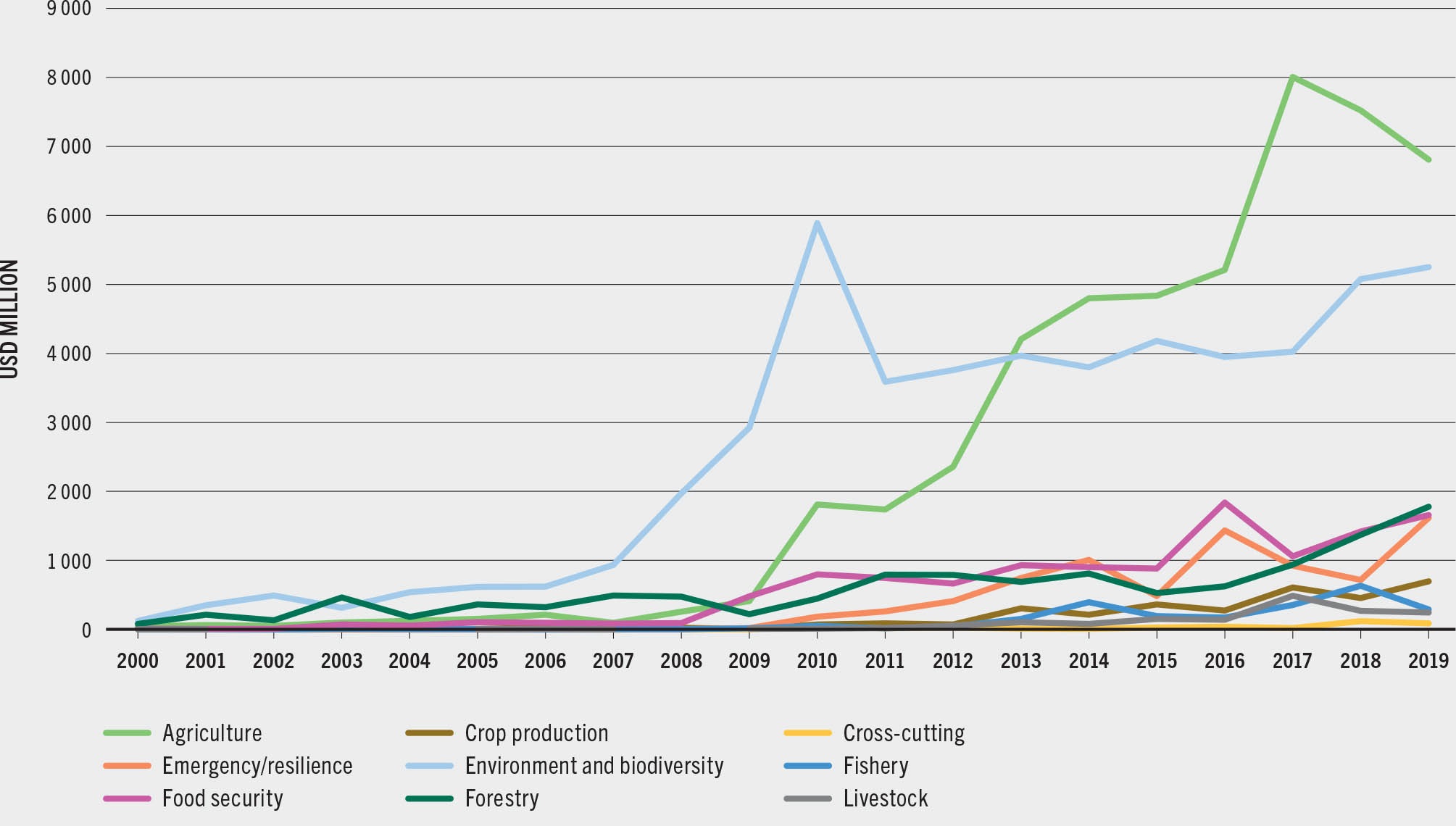

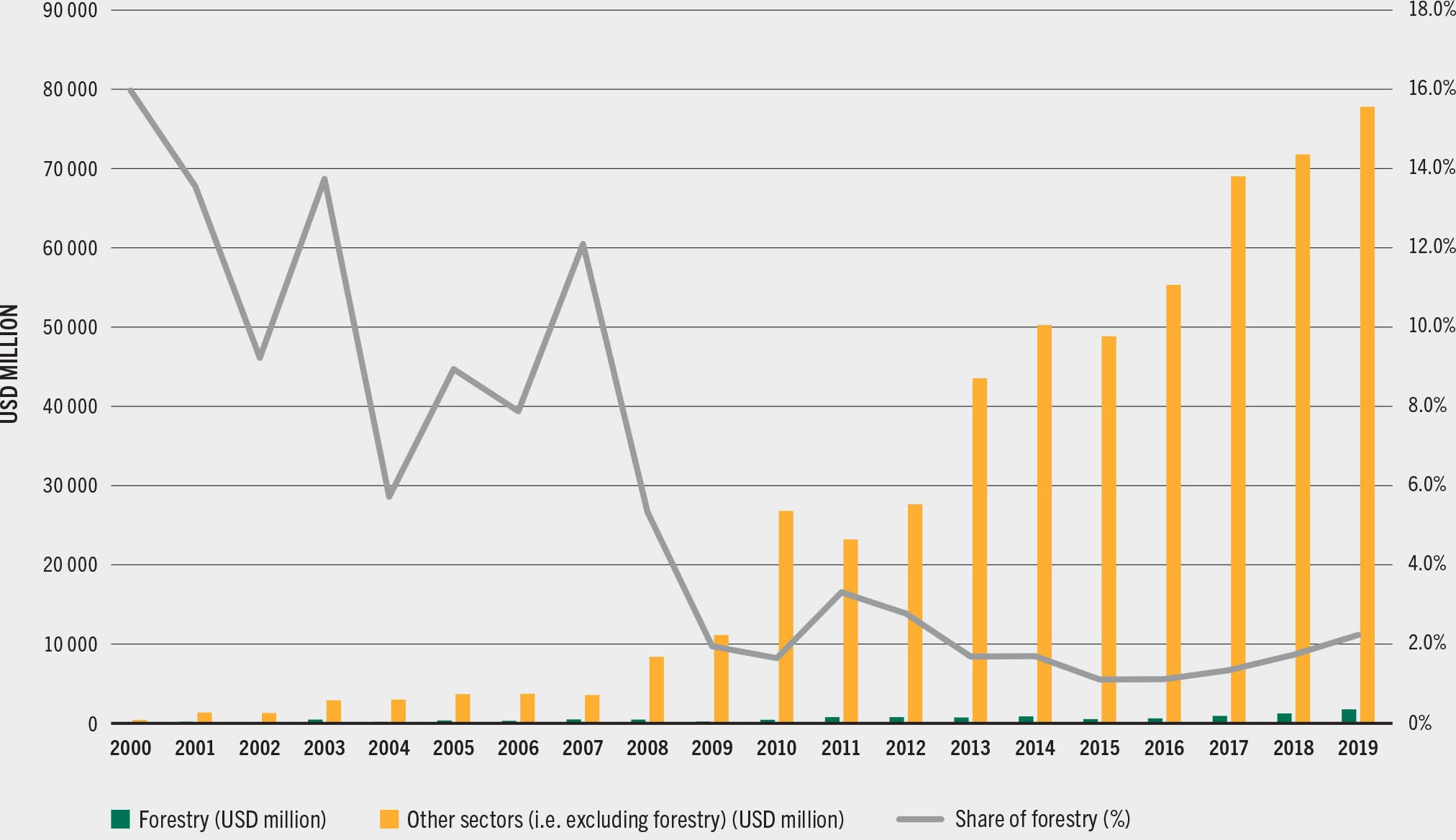

Climate finance data provided by the Organisation for Economic Co-operation and Development (OECD) Development Assistance Committee (DAC) is the most comprehensive and consistent data with global coverage that specifically identifies the forest sector. Data reported by both DAC and non-DAC members can be extracted from the OECD DAC External Development Finance Statistics database,336 which includes official development assistance (ODA), other official flows, private grants and private amounts mobilized. Figure 14 summarizes climate finance flows to forestry compared with other sectors – those to forestry almost doubled between 2015 and 2019 but are still below the level of investment needed. There has been a substantial increase in climate-related development finance for all sectors since 2000, but little of this has been directed towards forestry, with the share of climate finance channelled to forestry not exceeding 4 percent of the total between 2009 and 2019 (Figure 15). Pledges made at the 2021 UN Conference on Climate Change may boost funding for forests (see Box 24).

Figure 14Allocations of climate-related development finance to the agriculture, forestry and other land-use sectors

Figure 15Climate finance for forestry

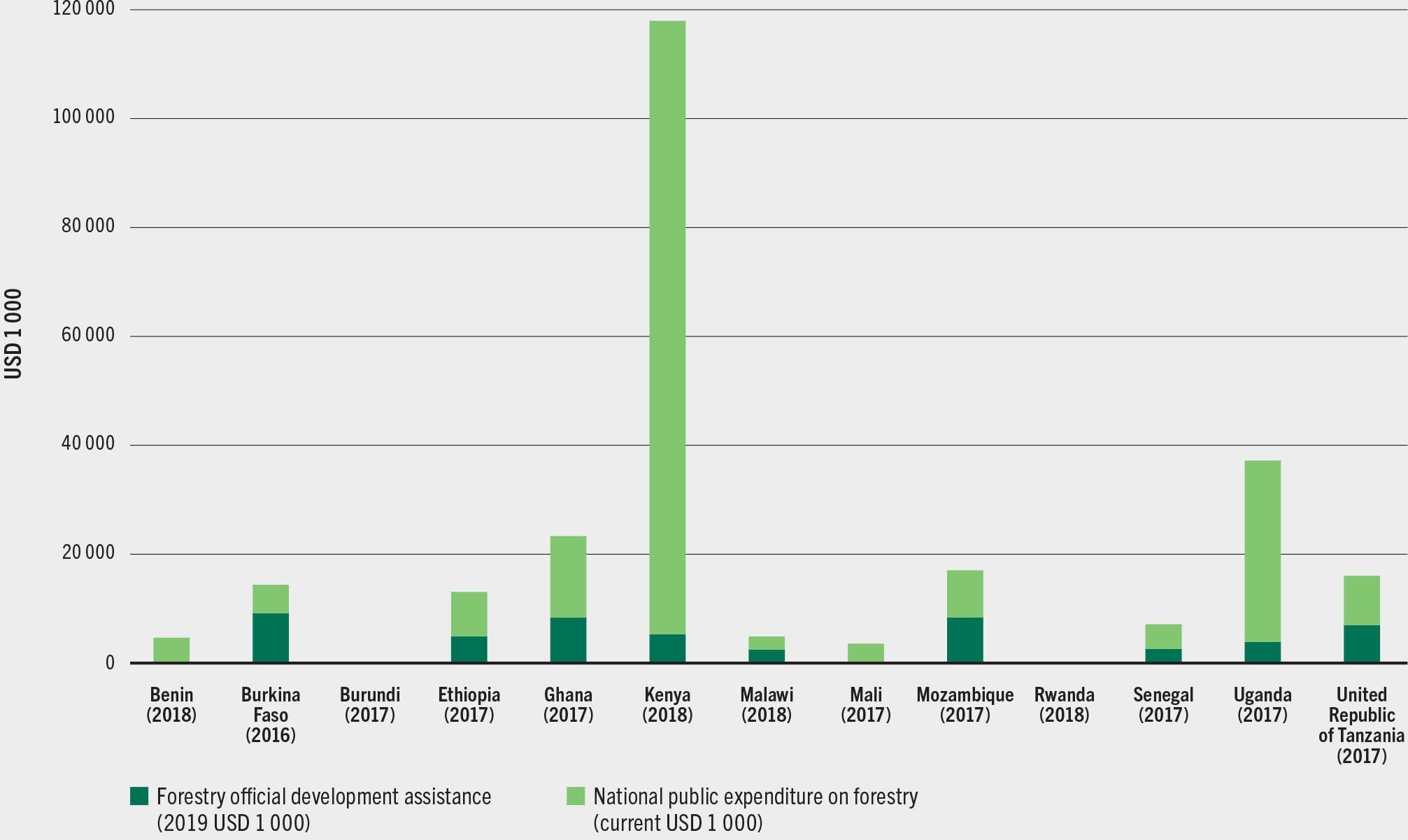

National public expenditure on forests far exceeds that obtained via ODA, even in some low-income countries. For example, an analysis of public expenditure on forestry in 13 sub-Saharan African countries in 2016–2018 (Figure 16) showed that, on average, national governments spent 3.5 times as much on forestry as the amount received as ODA for this purpose. National public forestry expenditure exceeded forestry ODA in all 13 countries except Burkina Faso, Mali, Malawi and Rwanda.j Therefore, policymakers should focus attention more (or at least as much) on domestic finance than on international funding.

Figure 16Public expenditure in forestry in 13 sub-Saharan African countries, and forestry official development assistance

SOURCES: FAO Monitoring and Analysing of Food and Agricultural Policies database and Organisation for Economic Co-operation and Development DAC Climate-related Development Finance database, compiled by FAO.

A global analysis by Whiteman et al. (2015) on domestic forest-sector expenditure reached similar conclusions, finding that governments spent approximately USD 38 billion on forest-related activities in 2010.337 The relative importance of domestic public finance for forestry compared with other sources has also been observed for biodiversity finance338 and in a recent compilation of studies on the finance available to support nature-based solutions.339

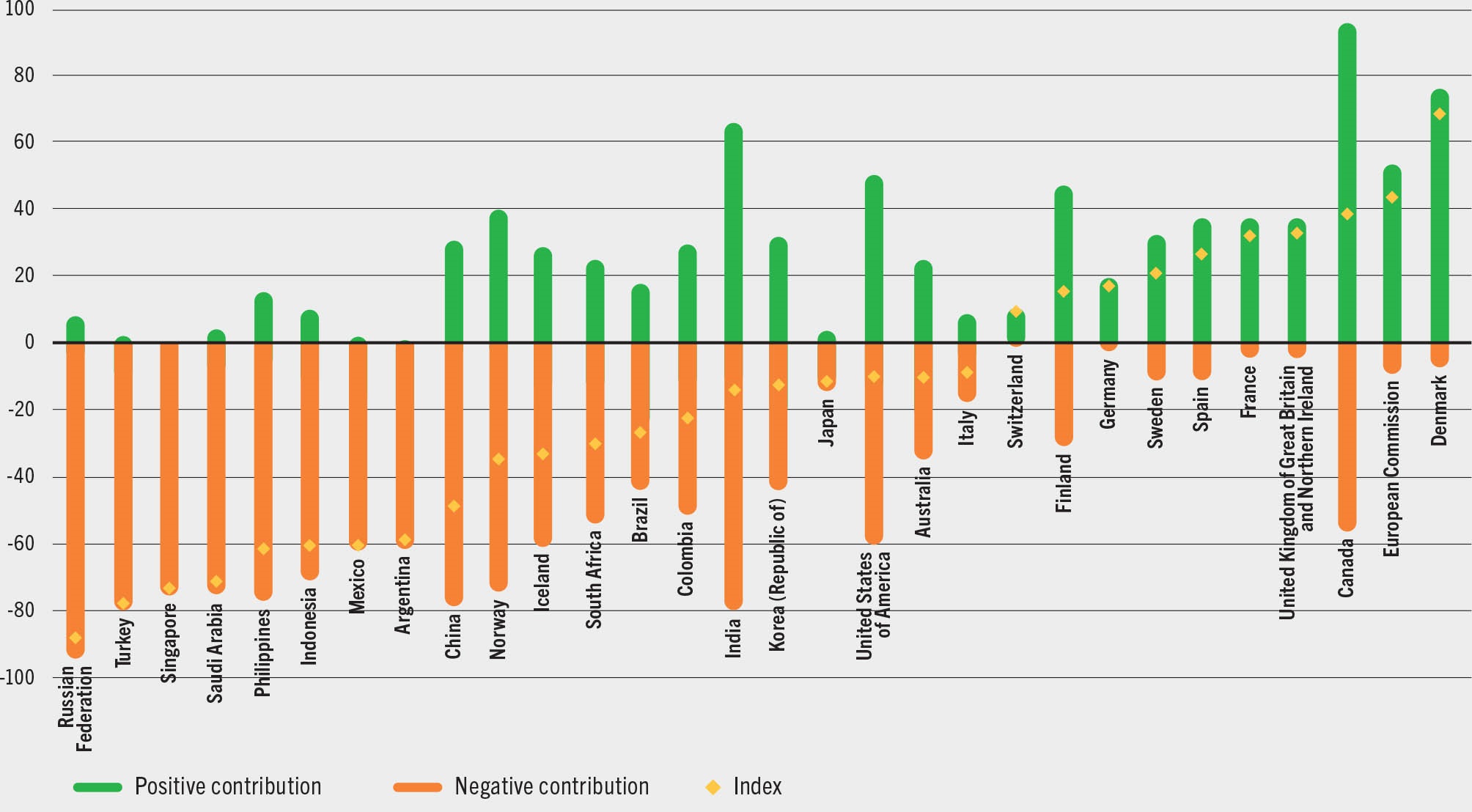

Few pandemic recovery plans have mobilized significant finance for the forest pathways. Increasing such finance is an important opportunity for green recovery

As of May 2021, total spending on recovering from the COVID-19 pandemic amounted to a massive USD 16.6 trillion in 87 of the world’s largest economies, of which USD 2.1 trillion was for long-term economic recovery and USD 420 billion was for green recovery.340 A recent analysis suggested that most recovery programmes will have a negative impact on green sectors, including forestry (Figure 17).341 Although, at first glance, European Union countries appear to have achieved a more positive balance, only 11 of the 27 countries integrate forests directly in their national recovery and resilience plans (through a chapter or subchapter), and an average of only 0.77 percent of the total resources indicated in these plans has been allocated to forests across the 27 countries.342 Two European Union countries – Romania (5.2 percent of the total budget) and Sweden (7.7 percent) – have developed ambitious forest programmes as part of their pandemic recovery plans. Outside the European Union, the Dominican Republic, India, Kenya, Pakistan and Peru have allocated funds for afforestation and reforestation (the restoration pathway), and Argentina and Peru are promoting wood value-added processing and youth employment (the sustainable-use pathway).343

Figure 17Greenness of Stimulus Index, as of 30 June 2021, 30 countries

SOURCE: Vivid Economics & Finance for Biodiversity Initiative. 2021. Greenness of Stimulus Index – An assessment of COVID-19 stimulus by G20 countries and other major economies in relation to climate action and biodiversity goals. (also available at https://a1be08a4-d8fb-4c22-9e4a-2b2f4cb7e41d.filesusr.com/ugd/643e85_f712aba98f0b4786b54c455fc9207575.pdf).

It will also be important to increase adaptation finance for forests. The latest (2020) report of multilateral development banks (MDBs) on climate finance indicated that about 4 percent of adaptation finance from them is channelled to “other agricultural and ecological resources” (including forests).344 Knowing that adaptation finance from MDBs was 24 percent of total MDB climate finance in 2020,345 it is clear that adaptation finance for forests is limited. This matches other recent figures: in 2018, public donor finance for nature-based solutions for adaptation accounted for approximately 0.6 percent of total climate finance flows and 1.5 percent of public climate finance flows.346 Further, it was estimated in 2019 that only 4 percent of total funding commitments from the Adaptation Fund was directed to activities specifically targeting ecosystem resilience.347

Private finance is traditionally the main source of funding for the sustainable-use pathway but is hard to quantify

The private sector is a hard-to-quantify source of finance for the three forest pathways. The UN Environment Programme (2021) estimated that private finance for nature-based solutions accounted for about 14 percent of total flows for this purpose.348 The three largest sources of private financing for nature-based solutions (including forests) in 2019 were sustainable supply chains (relevant to the halting-deforestation and sustainable-use pathways); biodiversity offsets, particularly in developed economies (relevant to the halting-deforestation and restoration pathways); and impact investment funds seeking social, environmental and financial returns (potentially relevant to all three pathways).349 An increasing number of private companies are engaging in forest projects, particularly those on the halting-deforestation and restoration pathways and less so for enhancing sustainable use.350 Some financial flows, such as investments by small producers in their own land, may be significant but are unreported.351

Existing pledges and commitments by private sector stakeholders mostly involve large consumer-facing organizations and financial institutions; the private forest sector, however, is absent or a minor participant in many existing alliances and initiatives on forest conservation and restoration. The private sector is active in initiatives such as the Forest Investor Club (launched at UNFCCC COP 26), the Forests Solutions Group of the World Business Council for Sustainable Development, the World Economic Forum’s Tropical Forest Alliance, the National Alliance of Forest Owners, New Generation Plantations, and Initiative 2020; the private sector presence in many other initiatives is unclear, however.

A challenge in estimating investments for the sustainable-use pathway is the lack of a definition of what constitutes an investment in green value chains.k Investments in processing and utilization (e.g. substituting wood for other energy-intensive and non-renewable construction materials) make it possible to “do more with less” – that is, improve efficiency and reduce waste and dependency on non-renewable and carbon-intensive materials. Yet investments in processing facilities can also exacerbate deforestation and degradation if raw materials are sourced unsustainably.

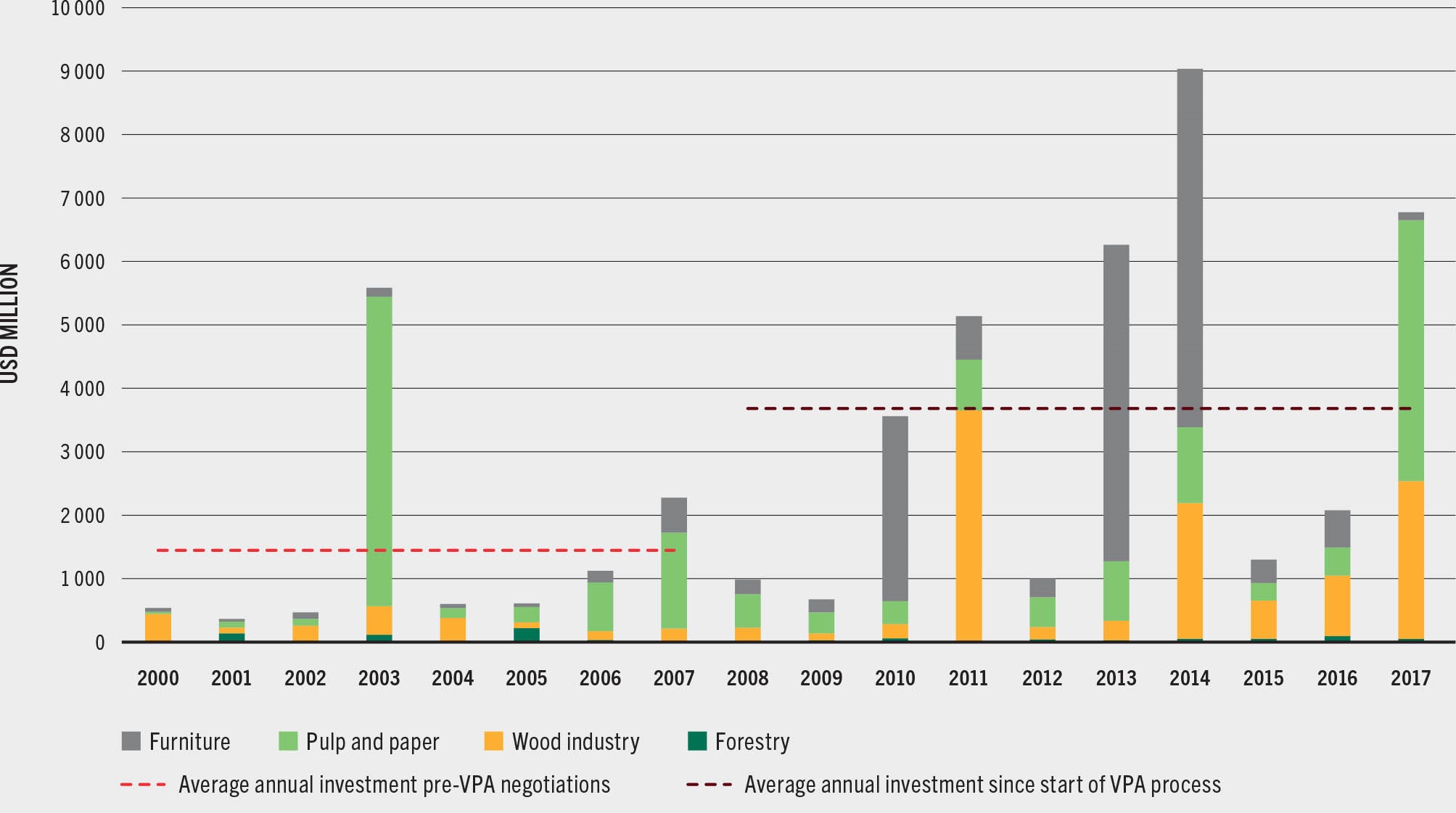

Notwithstanding the above caveat, private investment in forest-based value chains is probably higher than reported.352 According to one (2017) estimate, annual private sector investments in Africa, Asia and Latin America amount to USD 1.5 billion to USD 2 billion in plantations and USD 6.5 billion in wood processing.353 A more recent analysis found that average annual investment in the last several years has exceeded USD 600 million in Viet Nam and USD 3 billion in Indonesia (investments by small and medium-sized enterprises are included in these estimates if they operated formally).354 A noticeable feature of Figure 18 (for Indonesia) is that annual investments in wood processing, pulp and paper and furniture are many times those in forestry. In Europe, 25 countries reported total gross fixed capital formation (i.e. investments) of EUR 3.2 billion in 2015, equivalent to about EUR 20 per ha of forest; of this investment, 74.2 percent was spent on equipment and buildings, 16.3 percent on planting trees to provide regular income, and 9.5 percent on other investments in fixed capital, such as roads, fire prevention and tourist infrastructure.355 For 22 countries for which data were available, gross fixed capital investment increased by 14 percent between 2010 and 2015 (from EUR 2 659 million to EUR 3 035 million).356

Figure 18Annual increase in fixed assets for medium-sized and large enterprises in Indonesian forest subsectors

SOURCE: Held, C. 2020. The impact of FLEGT VPAs on forest sector investment risk in Indonesia and Viet Nam. Yokohama, Japan, International Tropical Timber Organization.

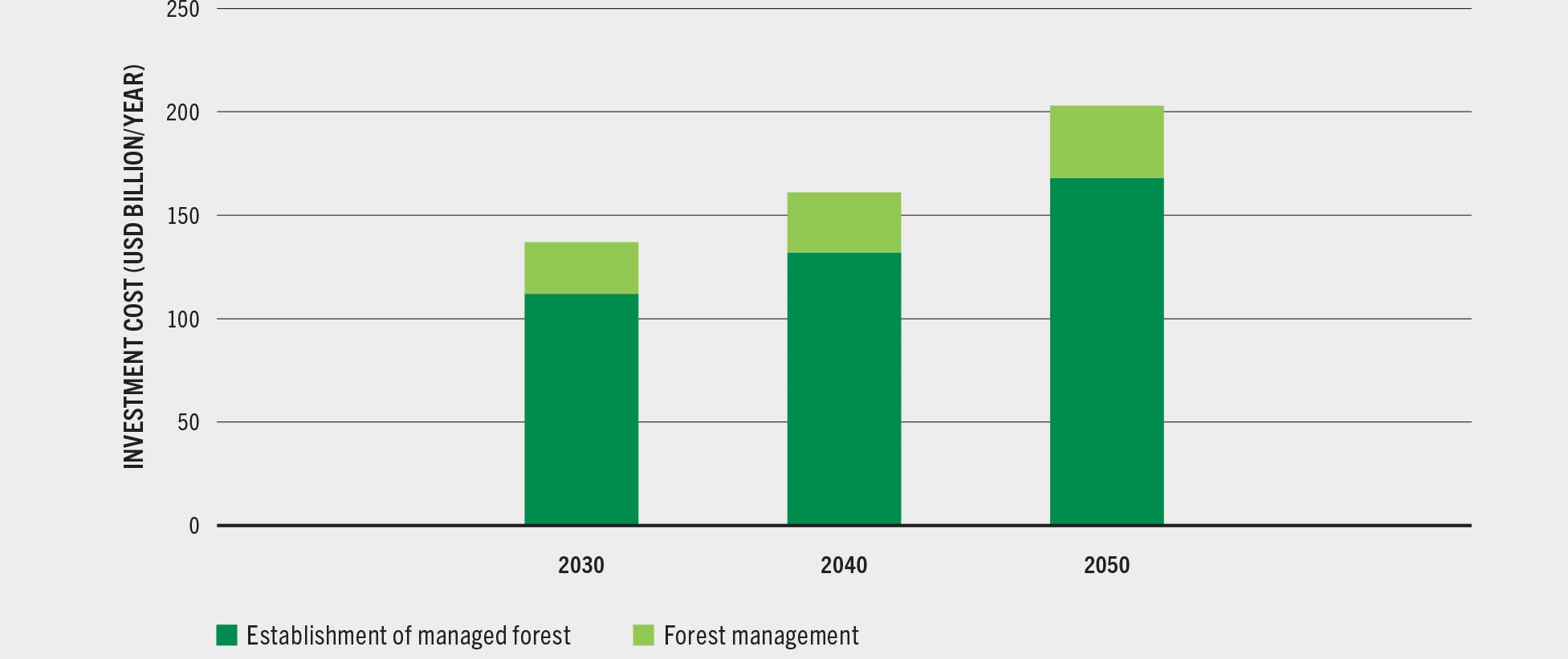

A recent study on financing for the forest pathways indicated that it needs to increase threefold by 2030 and fourfold by 2050 if the world is to meet its climate, biodiversity and land degradation targets, with the necessary additional finance directed to forest establishment and management alone amounting to USD 203 billion per year by 2050 (Figure 19); if peatland and mangrove restoration and silvopasture (a type of agroforestry) are included, the necessary investment increases to USD 400 billion per year by 2050.357

Figure 19Additional investment required in forest pathways under an “immediate action” scenario