Markets and value chains Responding to health-conscious consumers

The fruit and vegetables sector plays an important role in providing fresh and nutritious food to consumers around the world, especially in growing towns and cities. The sector generates income not only for producers, but also for the actors along the value chain that links farms to consumers (FAO, 2018). Fruit and vegetables can generate high returns per hectare, making it possible to reduce poverty if the right investment, capacities and services are in place.

This chapter examines various aspects of markets and value chains, including international trade, the links between farmers and domestic markets, and the need for responsible business practices.

International trade

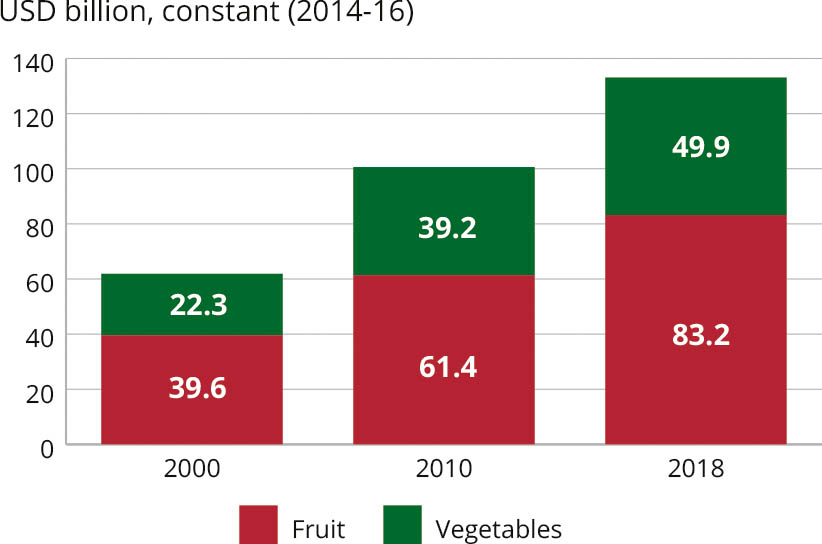

International trade of fresh fruit and vegetables represents only around 7–8 percent of total global production (FAOSTAT), but it still ranks among the most valuable crop and livestock commodity groups (Figure 9). Exports are an important driving force behind the expansion of the fruit and vegetables sector, and they also stimulate domestic production and markets. The growth in exports has significantly outpaced the increase in production: global trade more than doubled between 2000 and 2018 (Figure 10).

Figure 9. World export value of selected agricultural commodities, 2018

Source: FAOSTAT (2020)

Figure 10. Worldwide exports of fresh fruit and vegetables: Total aggregate volume increased by 115 percent between 2000 and 2018

Source: FAOSTAT (2020)

While exported quantities of fresh produce are low compared to the produced quantities, the value of trade means that they have the potential to contribute substantially to both the agricultural and gross domestic products of producing countries. Latin America and the Caribbean and Asia have established themselves as the most important exporting regions, where trade in fruit and vegetables generates important foreign exchange that many low- and middle-income countries can use to import food and other items. Favourable land, climatic conditions and high productivity in many areas of these regions make it possible to produce many varieties on a large scale, and year-round. Many countries in these regions have also invested in institutional capacity development (Fernandez-Stark et al., 2011) and the infrastructure needed to support trade.

Increases in trade have also been made possible through innovations in distribution technology and logistics that have cut transport costs and delivery times. Fresh produce is now available and affordable year-round in many places (Altendorf, 2017). Investments from importing countries in producing countries and bilateral or multilateral agreements have stimulated this trade.

The major importers of fresh produce are the European Union, the United States of America (both are also large exporters), China, Canada, Japan and the Russian Federation. Trade agreements, such as the World Trade Organization Agreement on Agriculture and various regional trade agreements, have led to reduced import tariffs (FAO, 2017b) among other effects, also stimulating growth in trade of the sector (Huang, 2004).

The expansion in global trade is also impacted by rising demand in high-income countries, particularly in the United States and the European Union, the two largest importing blocs. A preference for safe, good-quality, attractively packed fresh produce, a growth in health consciousness, and more widespread awareness of the nutritional benefits of fresh fruit and vegetables all contribute to rising consumption (see Chapter 2).

Campaigns to promote the health benefits of nutrient-rich fruit and vegetables and the growing availability of ready-to-eat products further stimulate demand. Indeed, changing consumer preferences can be seen in the growing year-round availability of fresh items that were once regarded as highly seasonal. For some high-value products, such as avocado, changes in consumer preferences are a key driver of trade expansion. On the other hand, global demand for some other items, including pineapples, mangoes and papayas, is more sensitive to changes in their price and to changes in incomes in importing regions (Altendorf, 2017).

Trade tends to be dominated by large national and multinational firms (Altendorf, 2019) which capture most of the added value. This may limit the potential of the fruit and vegetable export sector to reduce poverty.

Contract farming is one way that farmers can improve their participation in the high-value fruit and vegetables sector, as the approach provides solutions to address small farmers’ challenges related to access to technical assistance, inputs, credit, insurance and market information (FAO, 2015; UNIDROIT, FAO and IFAD, 2015; FAO, 2020d).

Contract farming

The growth in global fruit and vegetable markets opens significant opportunities for farmers, and “[c]ontract farming arrangements are increasingly seen as a means to include smallholder farmers in remunerative markets for added-value foods that are shaped by urbanization and income growth” (FAO, 2020d).

Contract farming is an agreement between one or more farmer(s) and a contractor for the production and supply of agricultural products under forward agreements, frequently at predetermined prices (Eaton and Shepherd, 2001). Farmers undertake in advance to supply given quantities of a product to a buyer at a guaranteed price. The contract may stipulate the volume, quality and timing, the crop variety, production methods (such as the agrochemicals that may be used), packaging, and other details. The buyer may arrange for training, advice, inputs such as seeds and chemicals, and even specialized equipment and labour for land preparation and harvesting, as well as credit to cover the cost of inputs.

Ideally, both sides benefit: the farmer gets a guaranteed market and income, while the buyer is assured of a reliable supply of a quality product. But contract farming carries risks for both sides. The buyer is often in a more powerful position and may impose demands that are too stringent on the farmers. On the other hand, farmers may not honour the delivery of the contracted amounts or quality standards indicated, or may side-sell to buyers offering a higher price at harvest-time (FAO, 2013).

Whether farmers engage in contract farming depends on many factors, including the farmer’s own characteristics, the local situation and farming system, and the needs of the buyer (FAO, 2013, 2020a). A survey of farmers in peninsular Malaysia, for example, found that farmers were more likely to be interested in contract farming for fruit and vegetables if they owned the land they farmed, cultivated a relatively large area, were educated, and believed they would benefit from the contracting arrangements (Arumugam et al., 2017).

Through contract farming, processors, exporters and other midstream actors integrate small farmers into highly profitable national and global value chains. But these are still very limited in scope. Some examples:

- South Africa. Citrus growers have contracts with both an exporter and a juice processor and receive financial and technical support (FAO, 2013).

- Tanzania. An exporter supports vegetable farmers to meet international quality and safety standards (FAO, 2013).

- Nepal. Farmers in remote areas who grow ginger under contract with a processor and exporter report around 58 percent higher net profits than non-contracted farmers (Kumar et al., 2016).

- Mexico. A family-owned frozen-vegetables firm offers small-scale producers contracts and provides them with the inputs, technical assistance and credit in a way that minimizes the firm’s contracting transaction costs (Key and Runsten, 1999).

While contract farming is typically applied to procure produce from farmers for export markets that apply stringent requirements on producers (FAO, 2016), there is some evidence that the approach can also be adapted for improving coordination in domestic food markets, including for high-value produce (Meijerrink, 2010; Soullier and Moustier, 2018).

Linking farmers to domestic markets

Due to high perishability and competitiveness in export markets, most fresh fruit and vegetables are traded and consumed locally or nationally. In Africa up to 96 percent of marketed farm output (including fruit and vegetables) is supplied through the domestic market (AGRA, 2019). In Latin America and Asia, most fruit and vegetables are sold through wholesale markets, fresh food markets, supermarkets and specialized grocery stores (Boza, 2020; ADB, 2019a, 2019b, Ren and An, 2010).

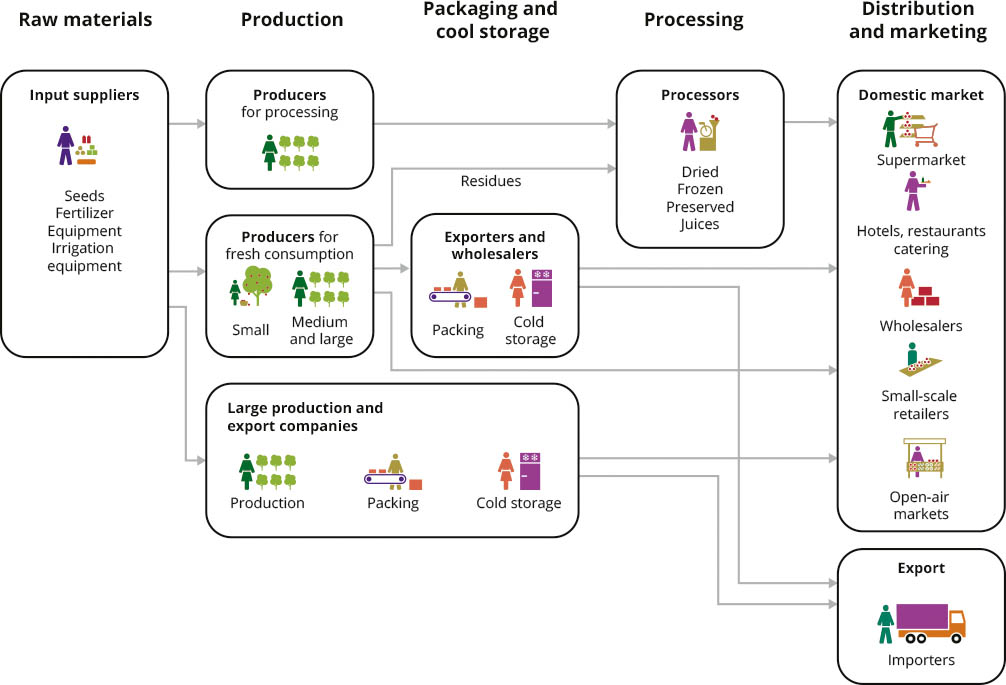

Much of this produce is grown by smallholders for sale through an often-complex system of traders and intermediaries, or sometimes directly to consumers (see Chapter 3). Figures 11 and 12 show value chain maps for selected fruit and vegetables in Ukraine and Uganda. The maps demonstrate the complexity of the linkages between the numerous actors along the value chain, and how the relationships and types of actors vary from one country to another.

Figure 11. Fruit and vegetable value chain in Ukraine

Source: CBI (2015)

Figure 12. Avocado, mango and green beans value chain in Uganda

Source: Dijkxhoorn et. al. (2019)

Domestic and regional food markets are expanding in low- and middle-income countries on the back of population growth, urbanization, rising incomes and a growing middle class, increasing women’s participation in labour markets, and shifts in consumer preferences for food. As income growth leads to major socio-economic changes, parallel shifts in food consumption patterns also take place – a process known as the “nutrition transition”. In the last stage of this transition, the consumption of fruit and vegetables increases (FAO, 2020d).

These trends have been taking place in a number of low- and middle-income countries (Pingali, 2007; Popkin, 2006, cited in FAO, 2020d). Governments can also promote fruit and vegetables programmes, as in India and Brazil, where consumption of mango and papaya has been expanding among an increasingly affluent population (Altendorf, 2017).

These shifting patterns in incomes and food consumption create opportunities for small farmers and small agri-enterprises along food value chains (Reardon, 2015). They give rise to shorter food value chains and distribution channels, creating more opportunities for direct linkages between producers and consumers (Galli and Brunori, 2013). Shorter food value chains may also stem from initiatives such as farmers’ markets or open-air food fairs, which build on consumers’ desire to engage directly with producers. Governments can also promote fruit and vegetable consumption and sustainable production from smallholders through public food procurement for schools and other public institutions (ECLAC et al., 2015). The COVID-19 crisis emphasizes the central role that local food-distribution channels play in ensuring food security (FAO, 2020b).

Value addition

Value addition for fresh fruit and vegetables includes sorting, grading, packaging, transport, wholesaling and retailing, as well as processing activities. It is done by enterprises of various sizes, from micro to large. Some actors perform multiple roles: wholesalers, for example, may play an important role in providing market information for producers and managing postharvest logistics (FAO, 2014). In many countries, supermarkets have a growing share of the retail trade in fresh produce, but the traditional retail sector, which includes local wet markets and roadside stalls, is still central for fruit and vegetable retail and food security in low-income countries (Parfitt et al., 2010).

Strengthening the capacities of the sector can improve market transparency and the quality and safety of food available in domestic markets (Demmler, 2020). In addition, these mid-stream agrifood enterprises also create the biggest market opportunities for farmers domestically (AGRA, 2019).

As with small food producers, small and medium agrifood enterprises also face a number of obstacles when linking to markets (FAO, 2015).

- Access to finance is a longstanding problem for small farmers and agrifood enterprises alike (and not only in the fruit and vegetable sector). The lack of reliable, affordable finance inhibits innovation, growth and employment generation, and constrains the agrifood sector’s capacity to reduce poverty (Beck and Cull, 2014; FAO, 2020d; Fjose et al., 2010; OECD 2017).

- Infrastructure and utilities such as cold chains, appropriate storage and processing technologies, reliable energy and clean water supplies are often inadequate. Their development is hindered by a shortage of investment opportunities, qualified staff, inadequate controls, and fragmented supplies (FAO, 2016).

- Government support for mid-stream actors is also frequently lacking. Ministries of agriculture and extension services focus on up-stream activities by producers, while small-scale mid-stream actors in the value chain fall between the mandates of ministries of trade, industry and commerce (FAO, 2015). Policies and regulations addressing them overlap or conflict, while policies tailored for the manufacturing sector fail to apply to the agribusiness sector with its special concerns: product perishability, unreliable procurement, sensitivity to weather, etc.

Learning from international trade

Domestic value chains can benefit by learning from successes in the international trade of fresh fruit and vegetables. Governments can support the sector by providing institutional frameworks for public–private collaboration, investing in infrastructure such as storage facilities and laboratories, stimulating linkages with research to generate innovations in postharvest operations (e.g., packaging and cold chains), encouraging finance for the sector, and building the competence of producers and managers (Fernandez-Stark et al., 2011). In Chile, such support helped the fruit and vegetable sector to upgrade and become competitive internationally, generating more than 450 000 jobs along the chain – equivalent to 5 percent of the country’s labour force (López, 2009).

Trade policies that stimulate exports can also affect the behaviour of national actors in the value chain. Appropriate policies can foster open borders and promote responsible, transparent national value chains. In the area of food safety and plant health, the agreements of the World Trade Organization strongly encourage the use of international standards as the basis for national measures. This can help to reduce trade costs and allow food to move smoothly between markets.

Responsible business

Employment and work conditions

Policymakers are increasingly looking to high-value food chains, such as fruit and vegetable value chains, to create off-farm employment (Losch, 2012). In rural Africa, farming accounts for around 40 percent of employment (as measured in terms of full-time equivalents). The wholesale, logistics, processing and retail of food and other agricultural products account for a further 25 percent (Dolislager et al., 2019; Arslan et al., 2019), with half of these activities carried out by small and medium-sized enterprises. As the number of mid-stream firms in food-supply chains grow, expectations are that farm output will be stimulated and on-farm employment created (Reardon et al., 2019). These small rural enterprises are more likely to hire vulnerable groups such as women or young people (Dolislager et al., 2019).

Jobs created in the sector should offer decent employment opportunities (Box 4). But value chains for fresh produce are particularly vulnerable to environmental, social and governance risks. The industry has a relatively high proportion of informal workers (casual, migrant or family labour). It is not uncommon to find farms where workers toil long hours in difficult conditions, without adequate health-and-safety safeguards, and without respect for their rights, such as the freedom to form unions. Child labour has been frequently reported, gender equity is a problem, and gender-based violence is common (Cooper, 2015). Crop production can have adverse environmental impacts, especially on large, monoculture plantations that heavily rely on pesticides to protect crops and agrochemicals to preserve products.

Box 4. Decent jobs

Decent jobs are defined as opportunities for work that are productive, respect core labour standards, provide a fair income (whether through self-employment or wage labour) and ensure equal treatment for all. Workers should be able to perform their tasks under safe and healthy conditions and have a voice in the workplace (FAO, 2017a).

To protect vulnerable groups, employees and the environment, companies operating beyond the farm gate and along value chains need to ensure their supplies are procured from sources that adhere to environmental, social and governance good practices by putting appropriate policies and systems in place. Doing so will protect companies at all levels, from small firms to multinationals, from reputational problems. This in turn can help them avoid costly remedial actions and improve relationships with suppliers, business partners and other stakeholder groups, thereby reducing their costs and raising their profitability (FAO, 2020c).

Due diligence

Drawing on various international guidance instruments (Table 1) and applied throughout the value chain, due diligence and responsible business practices can benefit farmers, farm workers, small agri-enterprises, local communities, the environment and society as a whole (OECD and FAO, 2020). Due diligence by companies can also increase the resilience of value chains to external shocks such as COVID-19 (Box 5).

Table 1. International guidance instruments on responsible business practices

Box 5. Due diligence

Due diligence is defined as a process through which enterprises can identify, assess, mitigate, prevent and account for how they address the actual and potential adverse impacts of their activities as an integral part of business decision-making and risk management systems (OECD and FAO, 2016).

This chapter has explored recent trends behind the rapid growth in demand for fresh fruit and vegetables, and notably of tropical fruit. The rise in international trade has been enabled by advances in transportation, storage technologies, trade agreements, rising incomes and shifting consumer preferences. However, if the potential of the sector is to be harnessed for poverty reduction, it is necessary that the right support infrastructure, investment and access to services for small-scale actors across the entire value chain be provided, alongside an enabling environment that protects the rights of vulnerable groups. The relevance of consumer trends is also discussed, as well as the importance of learning from opportunities provided by international trade for domestic market development for low and middle-income countries.