The previous section discussed the business case for motorized mechanization, highlighting its potential to enhance resilience, productivity and resource-use efficiency, and to reduce human drudgery and labour shortages. It also emphasized that, in some circumstances, manual and draught power can still generate progress. This section examines the business case for investing in digital automation technologies. Improvements in productivity, resource-use efficiency and labour savings have been key drivers of the adoption of these technologies. However, they are not without costs, and many require large upfront investments and specific skills and knowledge to operate them effectively. Farmers may also be sceptical about investing in certain innovations if they deviate from traditions and cultural and social norms. In this case, governments and service providers may need to intervene to communicate the expected benefits of investing in these technologies. This may involve trials, experiments and cost–benefit analysis to generate the necessary confidence.

An important challenge in assessing the business case for digital automation technologies in agriculture is the scarcity of information on their profitability. With the exception of motorized mechanization, digital automation technologies are new, and data on their adoption are dispersed and inconsistent (see Chapter 2). Likewise, information about the economic benefits varies widely, depending to some extent on the level of adoption of the various technologies in agriculture.29 For this reason, the discussion herein is based mainly on the findings of two technical studies commissioned for this report.30, 31 These relied, in turn, on 27 case studies, built on interviews with key informants across the world. They thus provide mostly qualitative evidence, based on the experience of digital automation service providers or – albeit to a lesser extent – representatives of agricultural producers. The 27 case studies cover all world regions and agricultural production systems (crops, livestock, aquaculture and agroforestry) and represent novel – yet scalable or already scaled – agricultural solutions related to motorized mechanization and digital automation technologies, targeting small- to large-scale farms. The case studies reflect the perspective of service providers rather than of agricultural producers as the final users. (See Annex 1 for a brief description of each case study and the methodology applied.a)

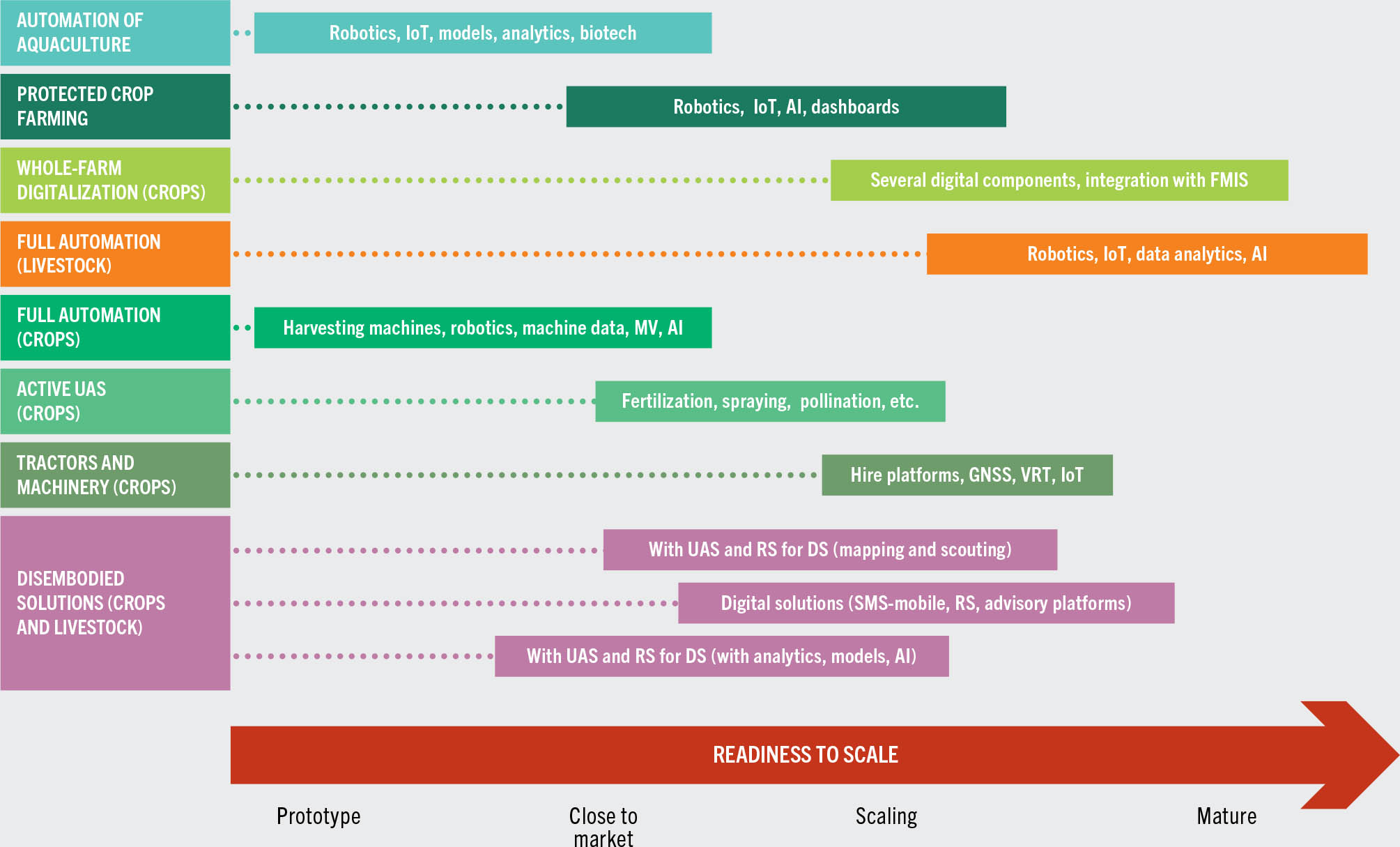

Readiness to scale of agricultural automation technologies: a framework

The technologies in the 27 case studies around the globe vary widely in their readiness for implementation. Figure 6 shows the four stages of readiness to scale of each type of technology. Solutions at the maturity stage mostly relate to livestock automation and whole farm digitalization. Fully automated equipment and machinery adapted to animal production have great prospects in terms of cost savings and raising productivity (see Box 13).

BOX 13The evolution of the business case for robotic milking systems

The adoption of livestock automation technologies is on the rise, especially robotic milking systems in high-income countries.32 Economic benefits can result from both labour savings (estimated at 18–30 percent)33 and increased milk production (10–15 percent per cow).33, 34, 35 Evidence indicates that small and medium-sized dairy farms (100–300 cows) were the first to adopt robotic milking, embraced by younger farmers attracted by better and more flexible working conditions (i.e. that do not require animals to be milked two or three times every day). The business case for milking robots is based more on flexible work schedules and better life quality for smaller farms than on purely economic benefits. There is, however, more recent evidence that larger dairy farms (with over 1 000 cows) are adopting robotic milking systems in response to labour shortages.29 The upfront costs of robotic milking machines make them non-viable for very small farms, found mainly in low- and middle-income countries, where – on the other hand – the technology may be attractive to commercial livestock farms with relatively larger herds.

Among the technologies that are scaling, Figure 6 presents a variety of categories, including disembodied digital solutions (see Glossary), uncrewed aerial systems (UAS, commonly known as drones) and remote sensing, mechanization solutions with global navigation satellite systems (GNSS), variable rate technologies (VRTs), and solutions for protected cultivation. The extensive literature dating back to the 1990s and supporting the business case for technologies using GNSS36 facilitated its adoption. This was not the case for VRT, however, as evidence related to profitability is mixed (see Chapter 2).29

FIGURE 6 The readiness to scale of DIGITAL automation technologies along a spectrum

SOURCE: Ceccarelli et al., 2022.31

Solutions still at the close to market or prototype stages mostly include advanced automation and robotics for both field and protected agriculture, as well as aquaculture, in addition to UAS for sensing and input application. Some technologies have already proved to be profitable and are replacing manual labour in high-income countries, performing a range of tasks from irrigation, pest scouting, harvesting and weeding, to fruit selection and picking; in contrast, there is no evidence of their adoption in low- and middle-income countries.

Many of the solutions are still in the early stages of development and commercialization, and their business case is yet to be determined. From the 27 case studies, some are still at the prototype stage (GRoboMac and Seed Innovations), while others propose solutions at the close to market stage (e.g. Atarraya, Food Autonomy, GRoboMac, Harvest CROO Robotics, Hortikey, UrbanaGrow). There are several cases where solutions are scaling (e.g. Aerobotics, Cattler, Cropin, ioCrops, SeeTree, SOWIT, TROTRO Tractor, Tun Yat) or mature (Lely, ZLTO, ABACO, Egistic and Igara Tea). See Annex 1 for more details on the readiness to scale stage of each technology.

A closer look at the case study results

From a service provider perspective, one of the most important findings emerging from the case studies is that only 10 of the 27 businesses appear to be profitable and financially sustainable. These are in the mature phase (see Figure 6), mostly based in high- or upper-middle-income countries and serving large-scale producers, although exceptions exist (e.g. a tea business in Uganda that targets small-scale tea producers). The fact that most businesses operate in high-income countries – despite sometimes originating in upper-middle-income countries, as is the case of Aerobotics in South Africa, Atarraya in Mexico and Cattler in Argentina – suggests that the business case for investing in these technologies is stronger in high-income countries.

From a user perspective, more than one-third of the case studies suggested that farmers are benefiting from these solutions through gains in productivity and efficiency, as well as new market opportunities. For example, in Uganda a digital solution aimed at improving the productivity and efficiency of tea (Igara Tea) has enabled 7 000 farmers to increase production by 57 percent over five years. A hire service company in Myanmar (Tun Yat) testifies that each farmer using their services generates approximately an additional USD 240 per year; this is primarily due to higher threshing quality and improved handling with fewer post-harvest crop losses.31 In three other cases – one focusing on livestock (GARBAL), another on mechanization hire services for crop production (TROTRO Tractor), and a third on fruit trees (SeeTree) – although evidence of their financial sustainability is still weak, the fact that farmers are already paying for the solutions suggests there is a business case for investing in them. Where information on the business case is lacking, the number of users or investments attracted by a solution can be an indication of its financial sustainability. For example, in five cases, service providers report the number of producers using their services (Aerobotics, Cattler, Egistic, Lely, SOWIT), and in two cases they report the investments the company has attracted (Atarraya and Harvest CROO Robotics).

The development of many of these technologies is still in the preliminary stages, with the business case yet to be determined. More evidence from cost–benefit analysis is needed to better understand how to tailor technologies to given conditions (see Box 14 for a European example).

BOX 14The impact of a digital orchard sprayer in the European Union: evidence from Poland and Hungary

The European Union has invested EUR 20 million in SmartAgriHubs, which aims to digitize European agriculture. Part of this project is the Smart Orchard Spray Application, designed to leverage smart spraying technologies embedded with internet of things (IoT) devices for the optimization of efficiency and treatment quality in orchards. IoT-enabled sprayers can significantly reduce use of plant protection products by adapting automatically to specific field zones as well as individual plant conditions. The integration of the Smart Orchard Spray Application cloud into farmers’ existing processes and software solutions further increases efficiency, profitability and sustainability of food production. Being traceable, it can also improve food safety and quality levels. Each year, producers are able to save EUR 517/ha on fuel and reduce pesticide costs by 25 percent as well as increase revenue thanks to better decision-making.

SOURCE: IoF, 2019.37

The information gathered to date allows to understand some of the drivers of and barriers to adoption of digital automation. First, a rise in the rate of adoption of a solution suggests not only that the technology can perform the agricultural operations successfully, but also that farmers can handle them. One case study on crop and livestock digitalization (ZLTO) illustrates how agricultural producers often have little time to familiarize themselves with new solutions, especially when not in-built in the machinery; in contrast, when new agricultural machinery is already equipped with GNSS devices, the adoption of this technology – for more precise positioning of the machine during operations – is facilitated.31

One of the main reasons why agricultural producers struggle to employ digital automation technologies is widespread digital illiteracy and lack of awareness of the potential of these solutions. In addition, there is a reluctance to change, generally associated with an ageing farm population. These factors emerge in case studies across the world (Abaco in Europe; ioCrops in the Republic of Korea; Seed Innovations in Nepal; SeeTree in the Americas, Europe and South Africa; TraSeable Solutions in Fiji and other countries in the Pacific; and Tun Yat in Myanmar) and are not confined to low- or middle-income countries. For this reason, generational change is indicated as a driver of adoption, with young farmers perceived as essential to move a family farm towards digitalization and advanced automation. Evidence from three case studies in the Republic of Korea (ioCrops) and the United States of America (Atarraya and Cattler) suggests that young farmers are more attracted by innovations. Capacity building is, therefore, essential to drive adoption.

Another driver of or barrier to adoption is attitude to risk. Two case studies (Aerobotics and Cattler) indicate that large-scale South African and Argentinian producers, respectively, are generally more dynamic and open to digital automation solutions than their counterparts in the United States of America. This is primarily because the latter feel less exposed to market risks, while the former need to be more competitive on the international market. Indeed, the dynamism and risk-taking attitude of the Argentinian and South African producers are probably driven by exposure to international competition, leading to higher adoption of technologies.

Other driving factors – also mentioned in Chapter 2 – include labour shortages (including seasonal, as indicated by GRoboMac, Igara Tea, SOWIT and TROTRO Tractor), safer working conditions and reduced drudgery (see the cases of Lely and SOWIT). An interesting observation by TROTRO Tractor is that labour shortages are a strong adoption driver for female farmers, who have more difficulty finding workers than do male producers. Furthermore, women usually perform operations later as they access machinery only after their male counterparts have finished using it. Solutions like TROTRO Tractor allow women to access equipment independently of its use by men.30 Another interesting finding was that the COVID-19 pandemic was considered to be a driving factor in two cases, because the need to avoid or reduce physical contact increased the value of digital solutions (see Box 15).

BOX 15COVID-19 spurred interest in digital technologies: evidence from two case studies

Of the 27 case studies prepared for this report, two highlighted the role of the COVID-19 pandemic as a particular driver of adoption. TROTRO Tractor, operating in several sub-Saharan African countries, mentioned the pandemic as an important driver of uptake of their services. Their platform enabled crop production in spite of movement restrictions and a system of e-vouchers facilitated adoption.

TraSeable – which offers a mobile app with simple digital tools allowing farmers in the Pacific to keep up to date on current affairs in the agriculture industry – also cited the COVID-19 pandemic as an enabling factor of adoption. The app was released in 2020 and, according to the interviewee, the remarkable increase in downloads has been in part due to the limitations on face-to-face contacts to control the COVID-19 pandemic.

SOURCE: Ceccarelli et al., 2022.31