Introduction

In March 2020, the World Health Organization (WHO) declared coronavirus disease 2019 (COVID-19) a global pandemic. Since then, the world has been shaken by a disease that has killed millions of people and rendered tens of millions ill.1 In a matter of weeks, the world’s economy suffered a sharp contraction as a result of the measures implemented in urgency to prevent the spreading of the virus. This led to major consequences for sectors highly dependent on trade, including fisheries and aquaculture. At the regional level, regional fishery bodies (RFBs) reported, inter alia, a negative impact on activities related to monitoring, control and surveillance (MCS) of fishing activities, fisheries and aquaculture research and management. Most countries and regions experienced severe declines in fishery and aquaculture production, employment and prices. Difficulties were reported for fisheries management decision-making and capacity-building owing to postponement of physical meetings, training sessions and workshops (FAO, 2021o). China, Europe, Japan and the United States of America, the four great major markets for aquatic foods,2 were severely hit by the pandemic. Closed borders – with travel restrictions and disruption of imports – affected developing countries that rely on exports of aquatic products2 for foreign exchange earnings.

FAO estimates that 3 billion people cannot afford a healthy diet, with an additional 1 billion if a shock were to reduce their income by one-third (FAO, 2020a). Indeed, the pandemic has posed major challenges to livelihoods, employment, food security and nutrition. Vaccination campaigns and policy responses to COVID-19 enabled global economic recovery in 2021, with an increase in production, trade and consumption of aquatic products (FAO, 2021p). The renewed interest in home cooking, food delivery services and digital retail channels driven by COVID-19 continues to expand (UNCTAD, 2022), although uncertainty remains as to how the sector will reorganize to adapt to a changing market and face the future, given the risk of new variants requiring subsequent restriction measures.

Supply chain disruption and related risks

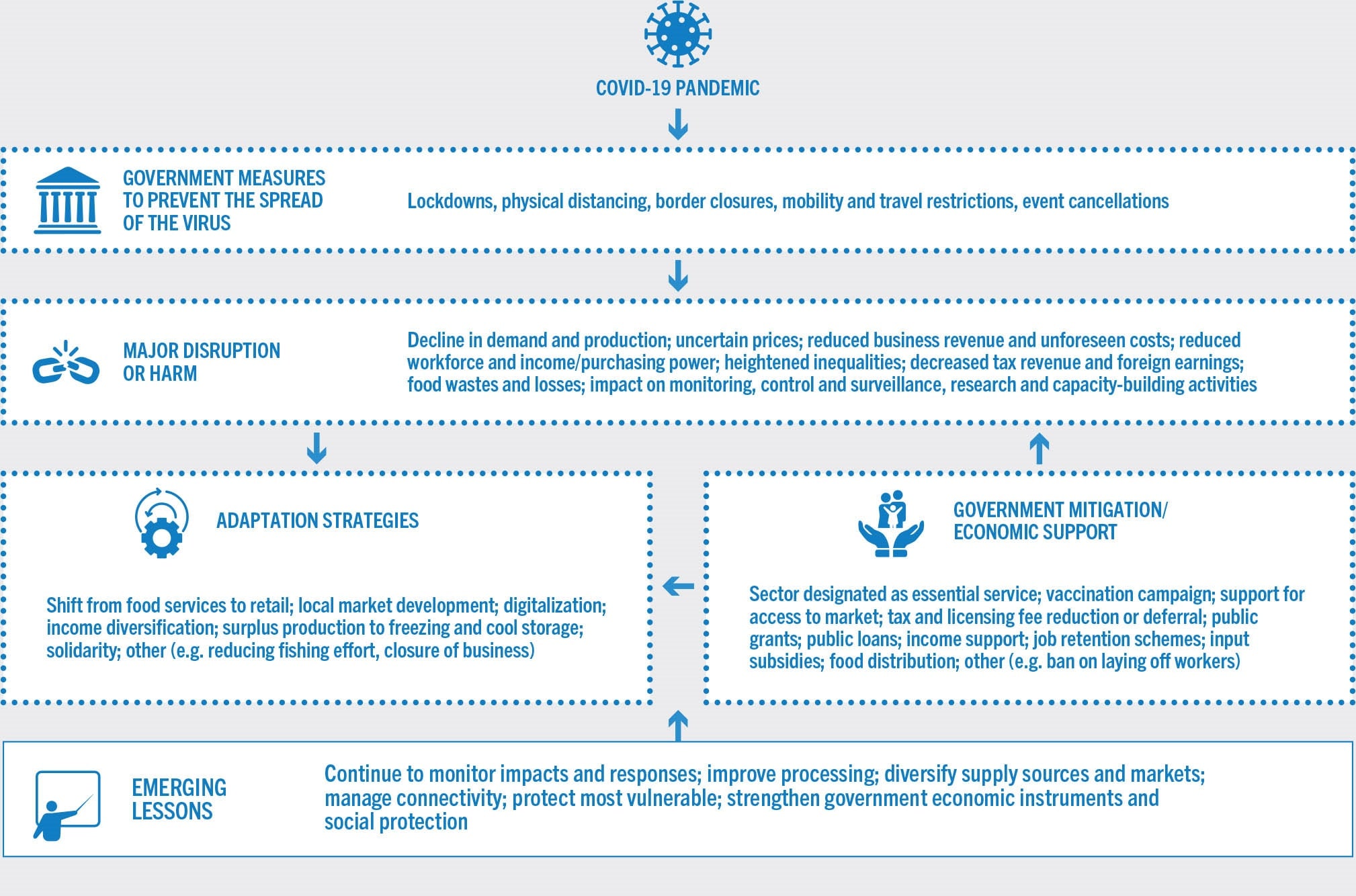

The entire fisheries and aquaculture value chain was severely disrupted as a result of the lockdowns. An external shock such as the COVID-19 outbreak had never before arrived with such speed, and the impact on consumer behaviour and trade globally was unprecedented. The pandemic has revealed the fragilities of aquatic food systems on both the demand and supply sides (FAO and WorldFish, 2021). In European countries, in the short term, perishable food was sold off below cost and/or scrapped, while in the medium term, the capacity to restock was constrained by reduced production and transport capacity. There was a massive shift in sales from food services to retail, resulting in oversupply of food service products and shortages in retail with a subsequent impact on prices (Kent, 2021). In many countries, mobility restrictions totally disrupted the fisheries and aquaculture supply chain, at least during the first months of the pandemic before the sector was gradually recognized as essential, and initiatives were implemented to bring the industry back on track. Mobility restrictions meant that essential production inputs, such as feeds and seed, could not reach farms regularly. Shrimp and tilapia farmers in Central America witnessed a 75 percent drop in demand in both local and international markets. All this resulted in the paralysis of the industry, which experienced overstocking and unforeseen feeding and freezing costs with severe economic impacts, and some production units closed operations (OSPESCA and SICA, 2020).

The impacts of the pandemic on aquatic food systems have varied depending on species, markets and consumer demand, as well as labour force structure and adaptive capacity of both governments and the industry (Figure 67). In general, supply chains dominated by small and medium enterprises (SMEs) were particularly vulnerable to COVID-19 restrictions (FAO, 2021q). In Africa and South Asia in particular, prior to COVID-19, these supply chains were already constrained by insufficient cold storage and processing capacity, poor transportation infrastructure, disjointed input markets, and/or underfinanced suppliers. Large-scale vertically integrated supply chains, in contrast, have generally been less affected, as they are more able to control input and output delivery. The labour-intensive small-scale sector was vulnerable to restrictions on movement affecting workers and to disruptions in input provisioning and transportation (IFPRI, 2021). In South and Southeast Asia, preliminary findings from a survey conducted by FAO and INFOFISH show that the COVID-19 pandemic and lockdowns greatly impacted small-scale fisheries and aquaculture farmers across countries. The restrictions disrupted supply chains and markets, hampered business operations, affected employment, maintained certain inequalities such as that of gender participation, and contributed to fluctuating incomes for households, and to decreased tax revenue and foreign exchange earnings for governments (FAO and INFOFISH, forthcoming).

FIGURE 67EXAMPLES OF DISRUPTIONS, ADAPTATION AND MITIGATION STRATEGIES, AND LESSONS EMERGING FROM THE COVID-19 CRISIS

Operators and markets are slowly recovering, but rising freight costs, new border procedures, reduced availability of shipping containers, bottlenecks in big international harbours, and the risk of new variants dampen the medium-term outlook (FAO, 2021p). As a whole, the aquatic food system has managed to adapt and maintain flows of products and supply, but numerous enterprises have gone out of business or are in a precarious position (FAO and WorldFish, 2021).

Work, gender and food security

The pandemic has impacted work, income and associated purchasing power (FAO and WorldFish, 2021; Béné et al., 2021). Four in five workers worldwide have experienced partial or total unemployment or working from home (Tooze, 2021). It has exacerbated the lack of access to adequate food for millions of people, making their food security a huge and persistent problem. Vulnerability to such income shocks is particularly worrisome in low-income countries, where a diet meeting basic energy requirements is beyond the reach of many (FAO, 2021q).

Many studies concur that shocks disproportionately affect vulnerable and marginalized people, and the COVID-19 pandemic is no exception.3 Low-income households, small operators, women, infants and young children, the elderly, persons with disabilities, indigenous populations, refugees, migrants, displaced people and minorities are at greater risk of suffering the adverse effects of the pandemic around the world. Small-scale fishers and fishworkers who rely on seasonal migration have been affected by prohibitions on travel and accommodation (Sowman et al., 2021). Crew change and reduced access to shore services have impacted seafarers, including migrant workers employed on long-distance industrial fishing vessels (Vandergeest, Marschke and MacDonnell, 2021). Many workers in the processing, harvesting and marketing industries have lost their jobs (Alam et al., 2022). Moreover, working on board fishing vessels and in post-harvest handling, packaging and processing has entailed increased risks of virus transmission and outbreaks of COVID-19 among workers because of reduced space and humidity (IFPRI, 2021).

Women’s relatively high representation in the sectors hardest hit by lockdowns has translated into greater declines in women’s employment than in men’s (FAO and WorldFish, 2021). Yuan et al. (2022) investigated the impact on the livelihood of households engaged in the aquaculture value chain in China: family income decreased significantly due to lower wages and reduced business revenue (e.g. the income of all catfish seed producers fell by more than 50 percent), and the families of 30–40 percent of surveyed farmers encountered financial difficulties; furthermore, women faced the increased burden of caring for and educating children due to school closures and were under extra pressure to maintain the basic living conditions of the family. Women account for half the workforce when both primary and secondary fisheries and aquaculture sectors are considered (FAO, 2020a). Nevertheless, they are under-recognized in the industry, despite their crucial role throughout the value chain and in household livelihood and nutrition. Moreover, the secondary sector has been hit particularly hard by the pandemic and this is where most women work. On the other hand, it cannot be understated that women have also emerged as agents of change and leaders in the COVID-19 response (FAO, 2020j, 2021r; Misk and Gee, 2020). In many cases, solidarity has formed the foundation for women to develop coping strategies during the COVID-19 crisis and they have used their skills, knowledge and networks to develop innovative solutions and support each other (WorldFish, 2021). As in all sectors at a global level, concerted efforts are required within the fisheries and aquaculture sector to prevent the pandemic from turning back the clock on progress towards gender equality (Turquet and Koissy-Kpein, 2020). To this end, it is vital to formulate appropriate gender-sensitive mitigation strategies that target economic and health aspects and enhance the resilience of people working in fisheries and aquaculture (FAO, 2020c).

Adaptation strategies

The entire world and the industry (at all scales) were not prepared for such a shock. Nevertheless, some businesses have managed to adapt over time and innovate. Some small businesses have been able to adjust and survive by using e-commerce platforms and modifying their business operations (Stoll et al., 2021; Witteven, 2021). Small-scale fisheries organizations throughout Latin America have adopted innovative approaches to commercialize their products. For example, they set up temporary selling points in spots located close to highly populated urban areas of Chile, Peru, Panama and Nicaragua, and small-scale fish farmers adopted e-commerce and home delivery to advertise and sell their products. Direct sales have developed as new and emerging markets in response to the closure of other markets. In Malaysia, online fish delivery intermediary, MyFishman.com, helped SMEs in fishing and aquaculture sell via fresh fish subscriptions and delivery services, thus avoiding wet markets and direct contact with consumers (IFPRI, 2021). Some changes seem here to stay and there are signs that COVID-19 may favour industry consolidation (Simeon, 2020).

In South and Southeast Asia, small-scale fishers, aquaculture operators and fisheries-based business operators responded in various ways depending on the level of restrictions in place, government support (or lack of), and their own resilience and innovation. Overall, their businesses experienced a general decline. However, resilience has been enhanced by diversifying or substituting household income with other agricultural activities, streamlining business costs to the necessary minimum, and embracing online marketing and direct delivery. This shift in business modus operandi is fostering new opportunities for small-scale fishers, aquaculture operators and fisheries-based business operators to have a closer and direct relationship with customers, enabling them to explore new markets and new products (FAO and INFOFISH, forthcoming).

Examples of mitigation strategies provided by RFBs include the rapid increase in the adoption of enhanced electronic monitoring tools for MCS activities, development of ad hoc fishing vessel boarding and inspection procedures, adoption of virtual meetings, establishment of online decision-making processes, online marketing of aquatic products and provision of support for the transition from fresh to value-added processed aquatic food products (FAO, 2021o). Countries such as China launched a national demand and supply platform to connect fisheries and aquaculture producers to processors and buyers, streamlining production with demand, directing surplus production to freezing and cold storage, and facilitating national and international trade (Alam et al., 2022; FAO, 2021s).

Government support measures

To contain the economic consequences of lockdowns and other restrictions, government support for households, businesses and markets took on dimensions not seen since the Second World War. Central banks responded to what the International Monetary Fund has called “a crisis like no other”, with unprecedented interventions to sustain government debt and banks (Tooze, 2021).

The measures adopted to address the impacts of the pandemic were diverse and complex, reflecting the intricacy of the issues addressed, the order of priority and countries’ capacity and resources. They included health, social, economic, education and environmental measures. According to Love et al. (2021), responses by aquatic food system actors and institutions mostly aimed to: (i) protect public health, including the health of fishery sector workers; (ii) support those whose enterprises, jobs and incomes were affected by COVID-19-related disruptions; and (iii) maintain supplies of aquatic products to consumers.

Government support in countries in Latin America ranged from availability of soft and interest-free loans for small-scale operators, tax and licensing fee relief, and fuel subsidies, to temporary suspension of credit obligations. In the United Kingdom of Great Britain and Northern Ireland, it took the form of income support, job retention schemes, bounce back loans and income tax deferral; there were also non-nation-specific measures, such as sea fisheries hardship funds in Scotland, support for the fishing industry in Northern Ireland and assistance from charities (e.g. The Seafarers’ Charity) (Patience, Motova and Cooper, 2021).

Preliminary research in South and Southeast Asia reveals both positive and negative responses from governments. Survey results point to, inter alia, the need for customized and focused government intervention supported by proper regulations, improved gender participation, increased education and awareness on the potential of digital markets and online platforms, while maintaining quality produce and meeting consumer needs. Sustaining the livelihood of small-scale fishers, aquaculture operators and fisheries-based business operators requires concertation with all concerned stakeholders (FAO and INFOFISH, forthcoming).

However, in most countries, support was complicated by limited public funds. Moreover, the fiscal and monetary responses to support vulnerable groups will have important consequences for indebtedness, debt servicing capacity, and debt sustainability more broadly. For example, sub-Saharan Africa experienced a 4.5 percent increase in “pandemic debt”– the debt taken on above and beyond projections due to the COVID-19 crisis (Heitzig, Aloysius Uche and Senbet, 2021). This could have serious impacts on the governance and management of living aquatic resources.

Social protection

The COVID-19 responses show that countries with working social protection systems in place had greater flexibility and could respond by adapting social protection programmes to the impact of the pandemic (FAO, 2021g). Other countries were unable to respond to the needs of communities dependent on living aquatic resources, especially where informality was predominant (FAO, 2020l). Many workers in the fisheries and aquaculture sector are informal with no social protection coverage; they are not registered in mandatory social security schemes, are paid less than the legal minimum wage, do not have a written contract or are self-employed. These individuals include small-scale fishers, migrant fishworkers, ethnic minorities, crew members, harvesters, gleaners and vendors – especially women, who have been the most affected by the pandemic (FAO, 2021g).

Many people who lost their employment were also left without access to income support. Many countries implemented new schemes, while others expanded existing schemes, either horizontally or vertically, by, for instance, increasing the programme’s coverage, relaxing access requirements, expanding the programme’s duration or introducing extraordinary cash transfers. The most common interventions targeting the fisheries and aquaculture sector were temporary social assistance measures, ranging from one-off payment schemes to unconditional cash transfer programmes lasting three months, and including in-kind food transfers. However, financial support was also provided through, for example, fee waivers and input subsidies for baits, ice and fuel, as well as for the provision of seed for aquaculture purposes and the building of aquaculture farms; in addition, technical support was made available to generate jobs and rebuild the sector (FAO, 2021g).

Emerging lessons

The COVID-19 crisis is protracted; its effects are unfolding as new variants emerge. It is essential to continue monitoring, assessing and documenting both the impacts on and the responses of the fisheries and aquaculture sector, in order to inform short-, medium- and long-term strategies and be prepared for new waves.

Among the lessons learned, the COVID-19 pandemic has highlighted the interconnectivity of markets: the disruption of one or more stages of the aquatic supply chain can have impacts that span local, national and international boundaries. Market disruptions can lead to inflation risks (Kent, 2021). Key elements for building resilient aquatic food systems include improving processing, diversifying supply sources and markets, managing connectivity through more robust food transport network and logistics, and allowing a mix of different and heterogeneous suppliers (FAO, 2021q).

Recognizing that fisheries and aquaculture is an essential sector and integral part of the food system in many countries, it is vital to maintain the smooth functioning of all points of the supply chains, supporting food security, income and employment with special regard for the specific challenges faced by vulnerable groups including women and migrant workers (FAO and WorldFish, 2021).

COVID-19 has exacerbated pre-existing inequalities. Small-scale fisheries and aquaculture, SMEs, women and other vulnerable groups (e.g. informal and migrant workers) are increasingly marginalized and need to be properly protected.

The pandemic highlights the need to expand social protection coverage through a comprehensive and inclusive national social protection system that is shock-responsive and adequately covers the sector. Policy coordination and coherence between a range of line ministries at the national level are essential. Social protection programmes should use a gender-sensitive approach throughout the design, implementation and evaluation phases, because they can affect gender dynamics. Social protection schemes can enhance households’ adaptive capacity to shocks and reduce negative coping strategies that would result in long-term detriment to their livelihoods. Social protection can contribute to improved welfare and fisheries management.

Economic support measures enacted by governments depend on the available resources and capacity. In most developing countries, the economic responses have important consequences for national debts because of the pre-COVID-19 debt level, debt servicing capacity and debt sustainability. This could have some impact on the governance and management of aquatic resources. Some recommend revisiting existing institutional mechanisms for debt sustainability and restructuring (Heitzig, Aloysius Uche and Senbet, 2021).

The emerging literature on COVID-19 and climate adaptation suggests that the pandemic impacts the Paris Agreement’s goals of “enhancing adaptive capacity”, “strengthening resilience” and “reducing vulnerability” to climate change, as countries are prioritizing health and economic recovery (UNEP, 2021). It is critical to embed social and environmental considerations (e.g. low carbon, climate resilience) into COVID-19 recovery plans through investment in activities that support blue economic recovery and build adaptive capacity (UNEP, 2021).

Furthermore, it is critical to prepare for multiple known or unknown risks. COVID-19 has added to diverse pre-existing pressures (e.g. fish/shellfish disease outbreaks, extreme weather events, chronic financial constraints), and fisheries and aquaculture management needs to address these through integrated risk management4 approaches. Studying what types of measures and broader interventions have worked in different contexts and how systems have changed, and documenting both longer-term impacts and emerging lessons could help to build specific resilience to the COVID-19 pandemic and general resilience to future shocks or stressors (Love et al., 2021).

On the positive side, the crisis has accelerated the digitalization of the sector, encouraged the e-monitoring and enforcement of capture fisheries, advanced the use of green and clean energies, contributed to the development of local markets, driven fish farmers to better manage scarce production factors such as feeds and highlighted the importance of domestic production.