Note: At the time of writing (March 2022), the Ukraine conflict adds another level of uncertainty to global value chains and trade. Prices of energy and inputs, including feed for aquaculture, have already started to soar. This is increasing operational costs resulting in higher prices of fisheries and aquaculture products.13Flight cancellations and/or rerouting are placing pressure on cargo capacity and causing further supply chain disruptions and delays in deliveries. The conflict also risks causing profound geopolitical changes with effects on trade relations between the United States of America, Europe, China, the Russian Federation and the rest of the world. This is likely to have a considerable impact on the fisheries and aquaculture sector. The following projections consider only marginally the potential impact of the war. Adjustments will be introduced in future revisions of the projections as impact assessments becomeavailable.

This section presents the medium-term outlook using the FAO fish model (FAO, 2012b, pp. 186–193), developed in 2010 to shed light on potential future developments in fisheries and aquaculture. The fish model has links to, but is not integrated into, the Aglink-Cosimo model used annually to generate the ten-year-horizon agricultural projections elaborated jointly by the Organisation for Economic Co-operation and Development (OECD) and FAO and published each year in the OECD-FAO Agricultural Outlook (OECD and FAO, 2021b). The FAO fish model uses a set of macroeconomic assumptions and selected prices to generate the agricultural projections. The fisheries and aquaculture projections presented in this section have been obtained through an ad hoc analysis carried out by FAO for the years 2021–2030.

The projections illustrated in this section depict an outlook for fisheries and aquaculture production,13 utilization, trade,14 prices and key issues that might influence future supply and demand. It is important to highlight that the projections are not forecasts, but rather plausible scenarios that provide insight into how these sectors may develop in the light of a set of specific assumptions regarding: the future macroeconomic environment; international trade rules and tariffs; the frequency of events and their effects on resources; the absence of other severe events such as tsunamis, tropical storms (cyclones, hurricanes and typhoons), floods and emerging diseases of aquatic species; improved fisheries and aquaculture management measures, including catch limitations; and the absence of market shocks. In view of the major role of China in the fisheries and aquaculture sectors, the assumptions consider continuation of the policy developments in China (FAO, 2018b, Box 31, p. 183) outlined in the Thirteenth (2016–2020) and Fourteenth (2021–2025) Five-Year Plans towards more sustainable and environmentally friendly fisheries and aquaculture. The future of the fisheries and aquaculture sectors will depend on many different factors of global, regional and local relevance. Population and economic growth, urbanization, technological developments and dietary diversification are expected to create an expansion in food demand, in particular for animal products, including aquatic food.13

Production

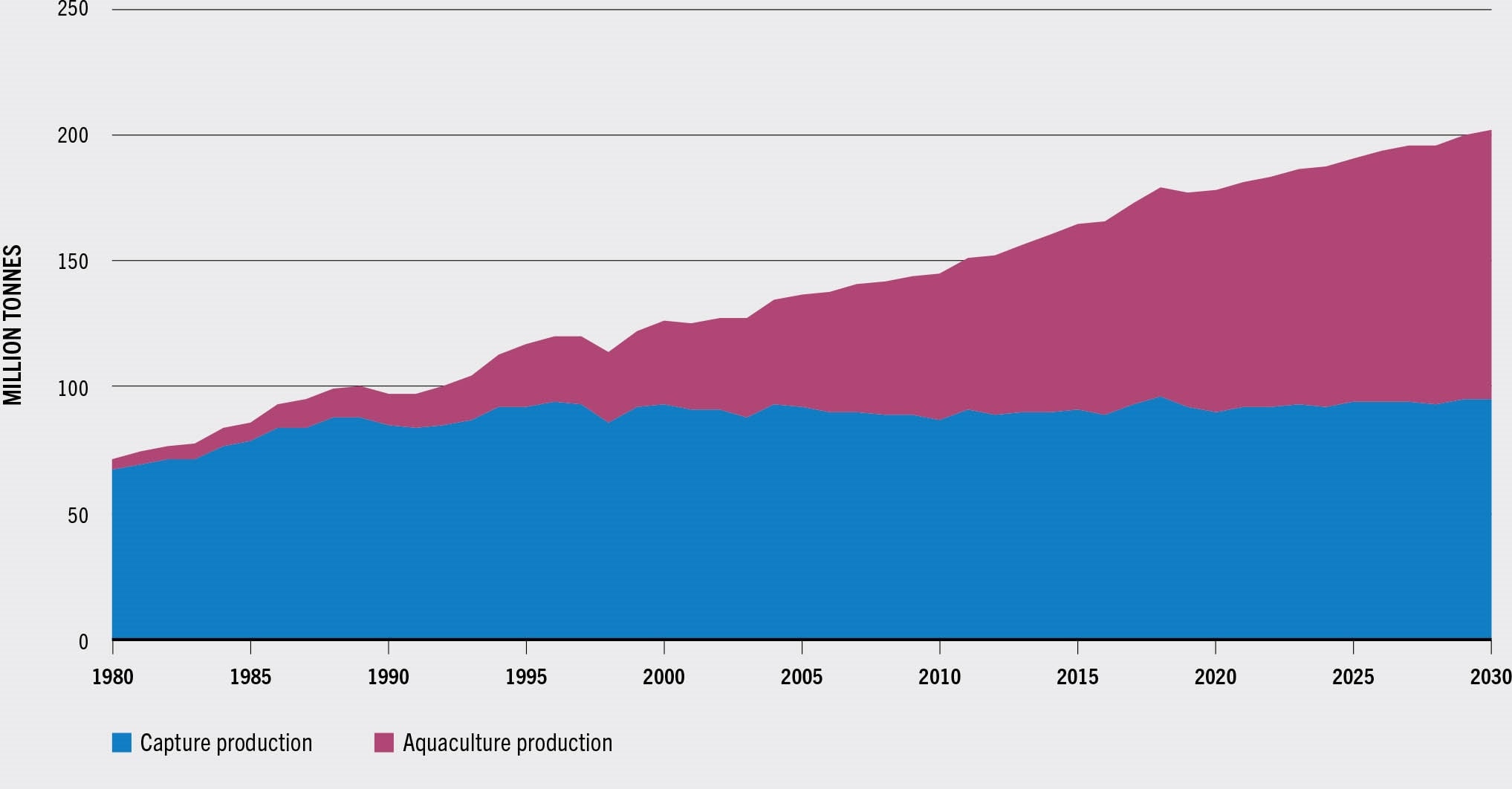

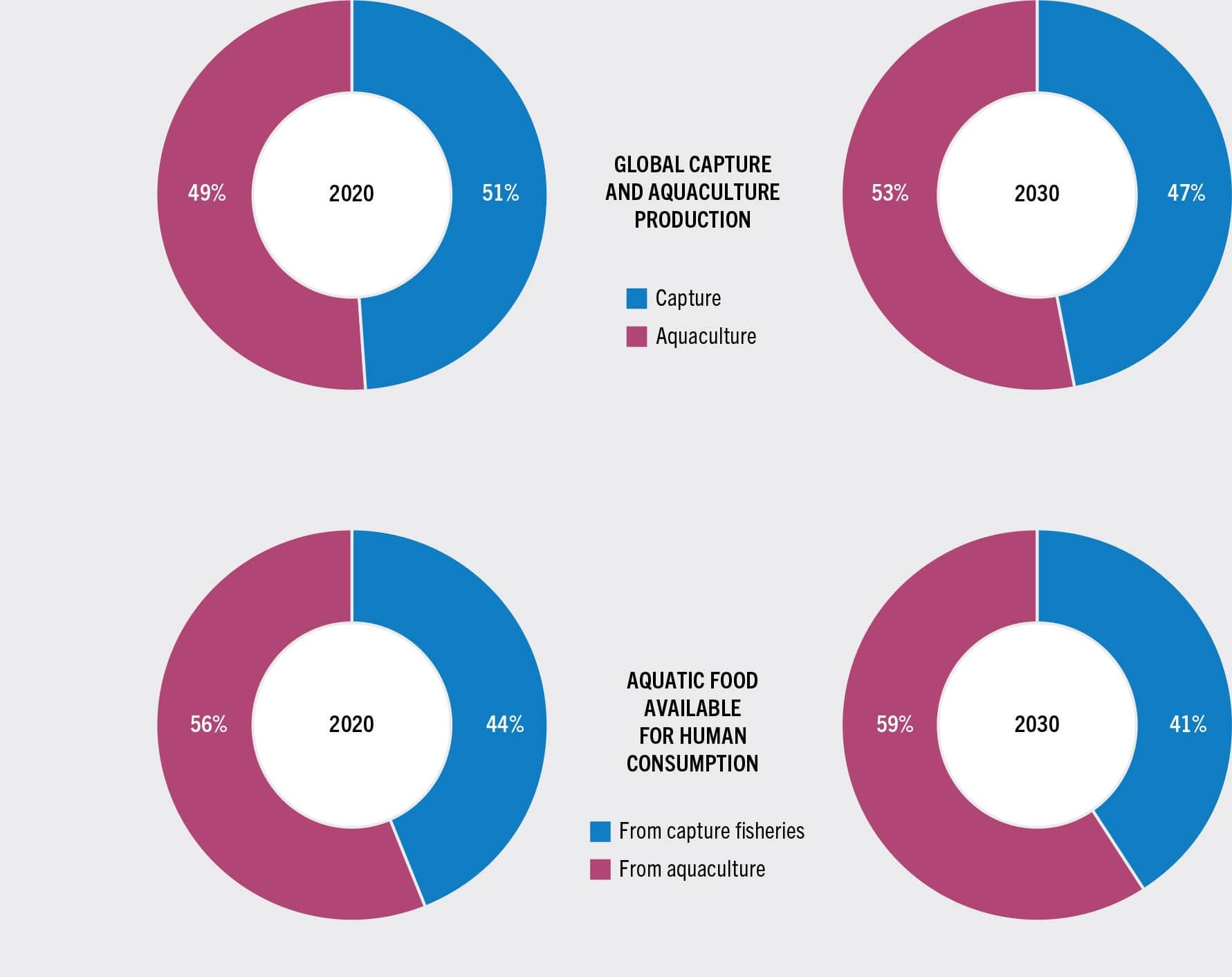

On the basis of the assumptions used, total fisheries and aquaculture production (excluding algae13) is expected to expand further and reach 202 million tonnes in 2030 (Figure 70). This represents an increase of 14 percent relative to 2020 and an additional 24 million tonnes in absolute terms (Table 18). However, while the total quantity continues to increase, both the rate and absolute level of growth are expected to decline compared with the 23 percent growth (33 million tonnes) during the period 2010–2020. Most of the increase in world fisheries and aquaculture production will come from the aquaculture sector, where output should break the 100 million tonnes threshold for the first time in 2027. Aquaculture production is expected to increase to 106 million tonnes in 2030, with an overall growth of 22 percent or nearly 19 million tonnes compared with 2020. The share of farmed species in global fisheries and aquaculture production (for food and non-food uses) is projected to grow from 49 percent in 2020 to 53 percent in 2030 (Figure 71).

FIGURE 70WORLD CAPTURE FISHERIES AND AQUACULTURE PRODUCTION, 1980–2030

SOURCE: FAO.

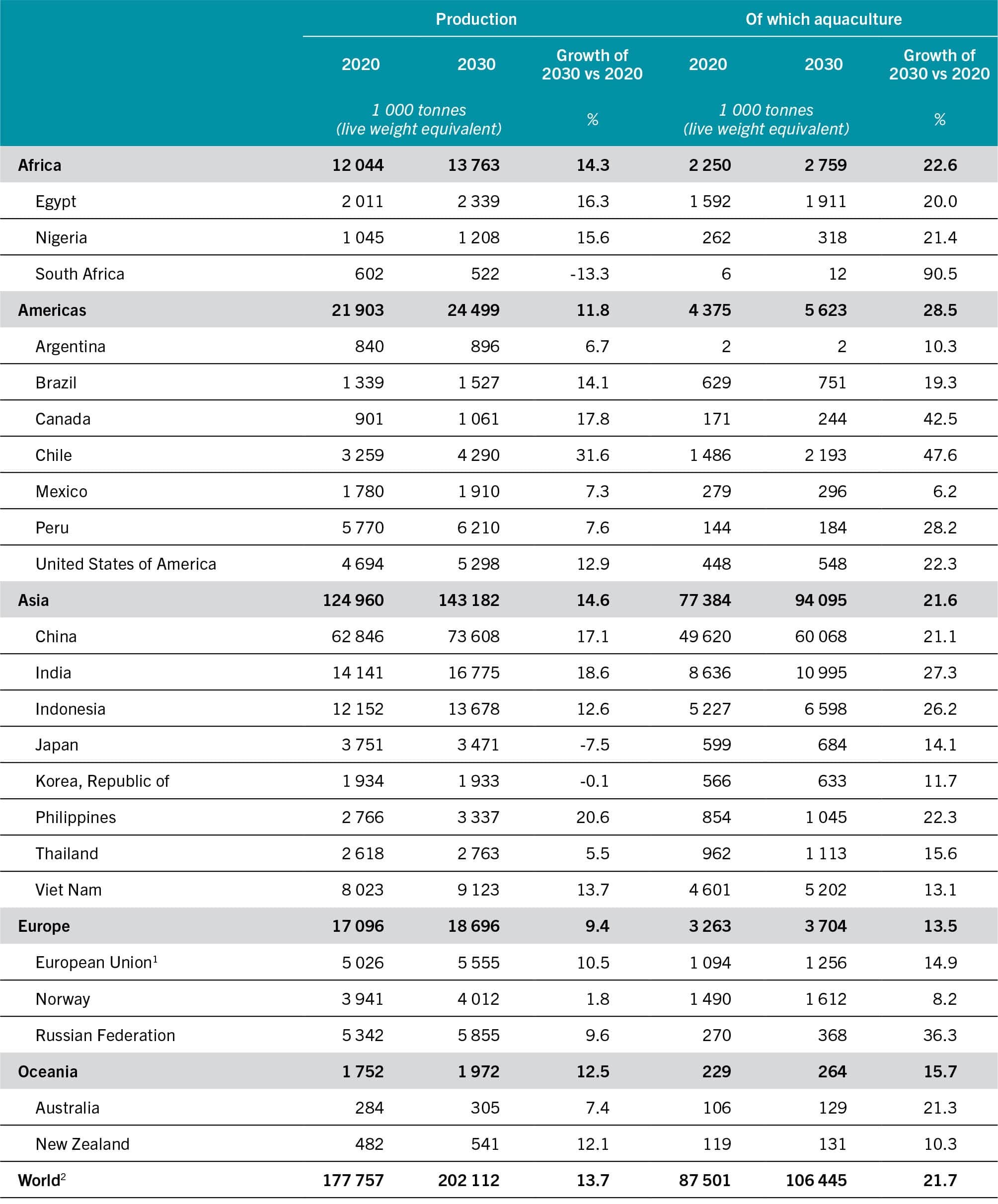

TABLE 18PROJECTED FISHERIES AND AQUACULTURE PRODUCTION TO 2030

NOTE: Excluding aquatic mammals, crocodiles, alligators, caimans and algae.

SOURCE: FAO.

FIGURE 71WORLD CAPTURE FISHERIES AND AQUACULTURE PRODUCTION, 1980–2030

SOURCE: FAO.

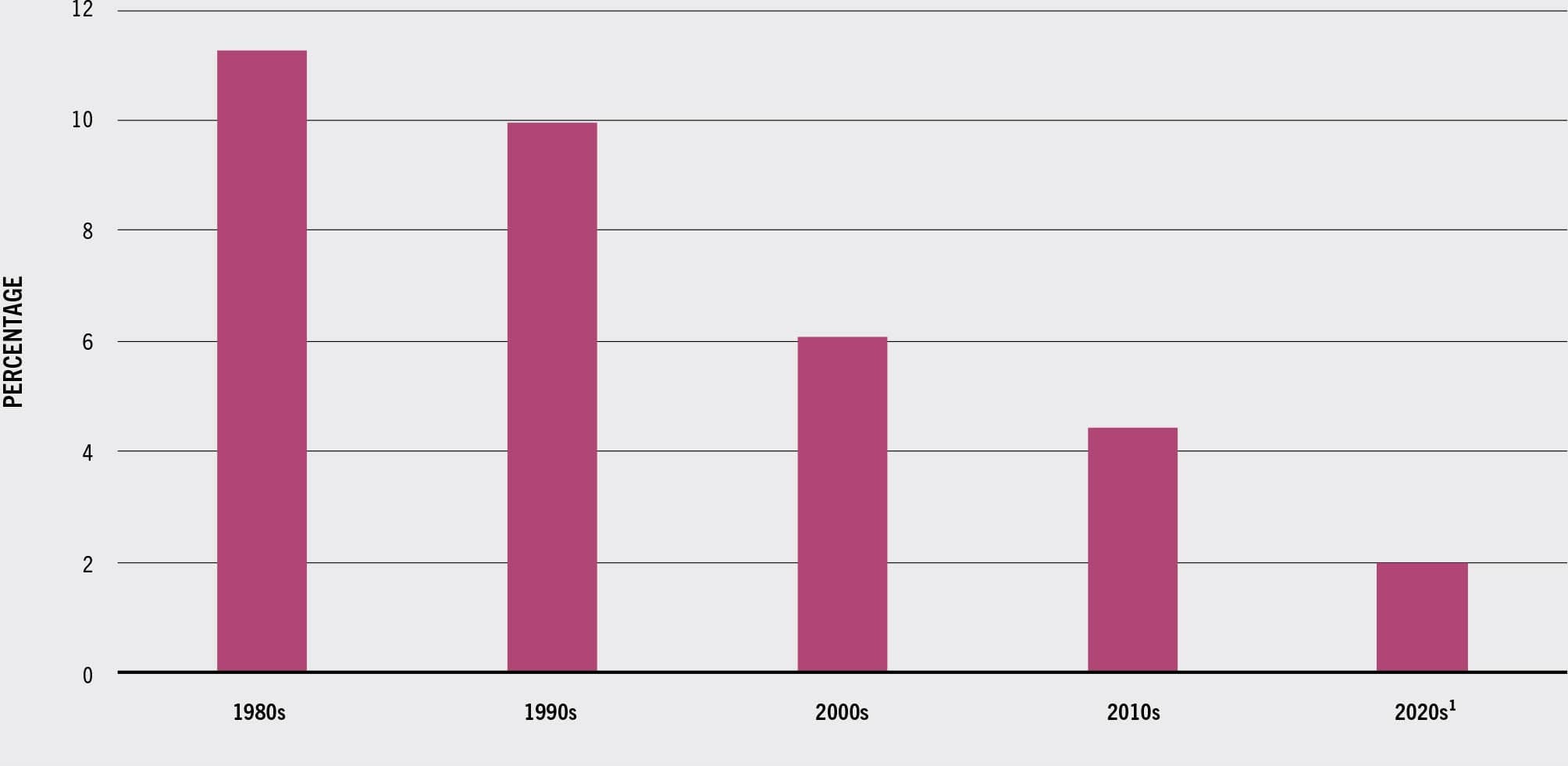

The average annual growth rate of aquaculture production should slow over the next decade to less than half the rate observed in the previous decade, dropping from 4.2 percent in 2010–2020 to 2.0 percent in 2020–2030 (Figure 72). A number of factors should contribute to this slowdown.15 These include: broader adoption and enforcement of environmental regulations; reduced availability of water and suitable production locations; increasing outbreaks of aquatic animal diseases related to intensive production practices; and decreasing aquaculture productivity gains. In particular, Chinese policies are expected to account significantly for the overall reduced growth. Initiated in 2016, these policies are expected to continue the transition from extensive to intensive aquaculture, while at the same time integrating better production with environmental considerations through the adoption of ecologically sound technological innovations, with initial capacity reduction, followed by faster growth. Although China will remain the world’s leading producer through to 2030, its aquaculture production is expected to increase by 21 percent in 2020–2030, nearly halving the 40 percent increase in 2010–2020. China accounted for 57 percent of global aquaculture production in 2020 and this is projected to decline slightly to 56 percent by 2030, despite aquaculture’s contribution to total Chinese fisheries and aquaculture production as it increased from 79 percent to 82 percent in the same period. The projected deceleration of China’s aquaculture production is expected to be partially compensated for by an increase in production in other countries.

FIGURE 72ANNUAL GROWTH RATE OF WORLD AQUACULTURE, 1980–2030

NOTE: Excluding algae.

SOURCE : FAO.

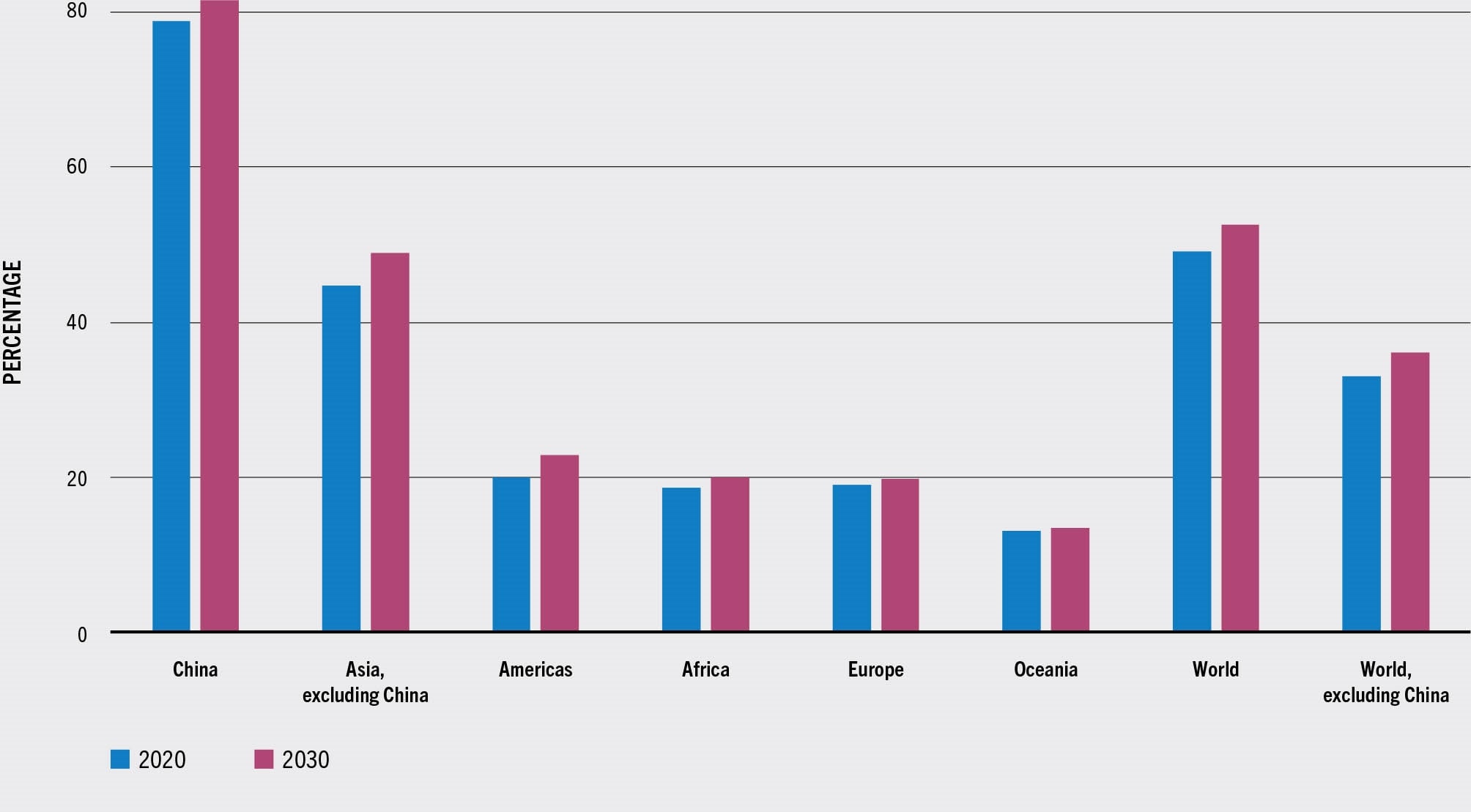

Growth of aquaculture production is projected to continue on all continents, with variations in the range of species and products across countries and regions (Figure 73). The sector is expected to expand most in the Americas (up 29 percent from 2020), Africa (up 23 percent) and Asia (up 22 percent). The growth in Africa’s aquaculture production will be driven by the additional culturing capacity put in place in recent years, as well as by national policies promoting aquaculture fuelled by rising local demand as a result of higher economic growth. However, despite this expected growth, overall aquaculture production in Africa will remain limited, at slightly more than 2.8 million tonnes in 2030, with the bulk (1.9 million tonnes) produced by Egypt. Asian countries should continue to dominate the aquaculture sector (maintaining their share of 88 percent of 2030 global aquaculture production) and be responsible for more than 88 percent of the increase in production by 2030.

FIGURE 73CONTRIBUTION OF AQUACULTURE TO REGIONAL FISHERIES AND AQUACULTURE PRODUCTION

SOURCE: FAO.

All farmed groups of species, will continue to increase, but rates of growth will be uneven across groups and the quantitative importance of different species will change as a consequence. In general, species that require larger proportions of fishmeal and fish oil in their diets are expected to grow more slowly owing to expected higher prices and reduced availability of fishmeal.

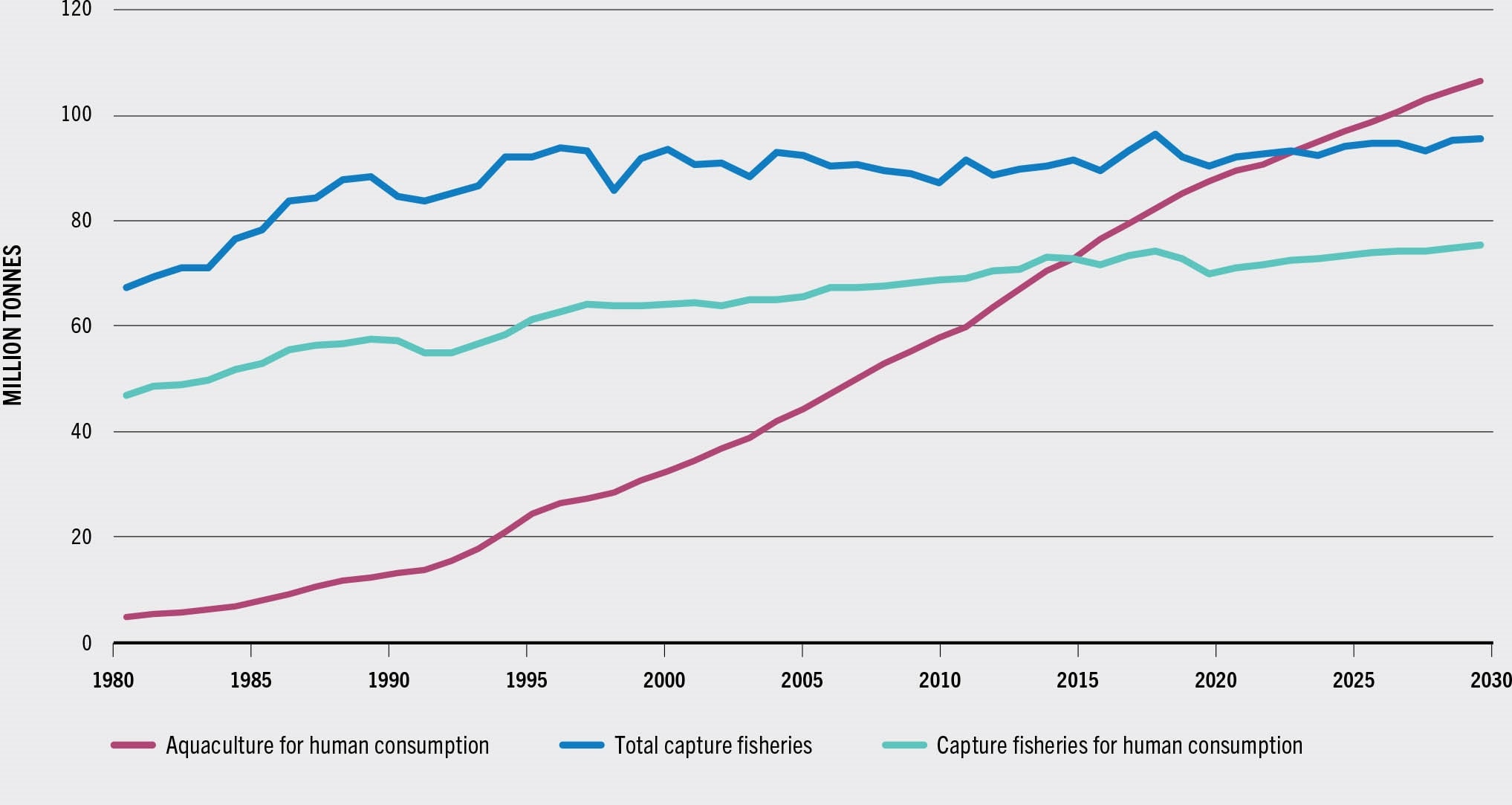

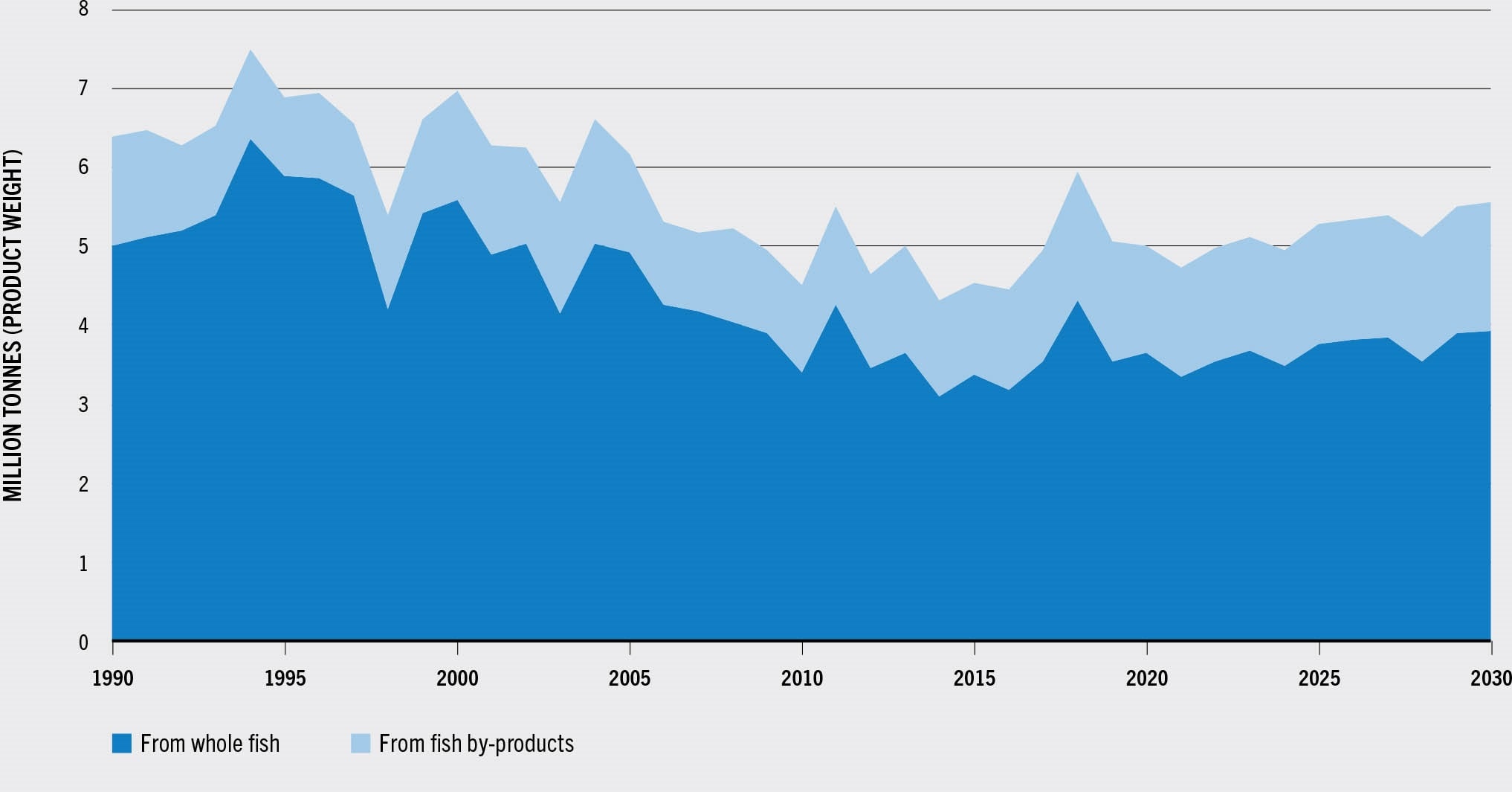

In contrast to the slight decline experienced in 2019 and 2020, capture fisheries is projected to recover during the coming decades, resulting in world capture fisheries production at the end of the outlook period reaching 96 million tonnes, over 5 million tonnes more than in 2020, with an overall increase of 6 percent. However, some fluctuations are expected over the next decade, linked to the El Niño phenomenon, with reduced catches in South America, especially for anchoveta, resulting in an overall decrease in world capture fisheries production of about 2 percent in those years.16 The overall increase in capture fisheries production is driven by different factors including: (i) increased catches in some fishing areas where stocks of certain species are recovering owing to improved resource management; (ii) growth in catches in waters of the few countries with underfished resources, where new fishing opportunities exist or where fisheries management measures are less restrictive; and (iii) improved utilization of the harvest, including reduced discards, waste and losses as driven by legislation or higher market prices of aquatic species for food and non-food products. China is expected to remain the major producing country, even if its capture fisheries production should remain at the levels reached in 2020, as it continues its environmental policies into the next decade. For capture fisheries, China’s policies aim to reduce domestic catches through controls on licensing, reduction in the number of fishers and fishing vessels, and output controls. Other objectives include: modernization of gear, vessels and infrastructure; regular reduction of fuel subsidies; elimination of illegal, unreported and unregulated fishing (IUU fishing); and restoration of domestic fishery stocks through the use of restocking, artificial reefs and seasonal closures. However, this Chinese policy projects to compensate for the expected decline in domestic catches by an increase in distant-water fleet catches. In 2030, production of both fishmeal and fish oil is expected to increase over the outlook period by, respectively, 11 percent and 13 percent compared with 2020, although the share of capture fisheries production reduced into fishmeal and fish oil should decline slightly (17 percent by 2030 compared with 18 percent in 2020). The expected increase in fishmeal and fish oil production is due to the overall growth in capture fisheries production in 2030 compared with 2020, combined with the increase in fishmeal and fish oil production obtained from fish waste and by-products of the processing industry (Figure 74). Between 2020 and 2030, the proportion of total fishmeal obtained from fish waste is projected to increase from 27 percent to 29 percent, while the proportion of total fish oil is projected to slightly decline from 48 percent to 47 percent.

FIGURE 74WORLD FISHMEAL PRODUCTION, 1990–2030

Consumption17

Most fisheries and aquaculture production will be utilized for human consumption and this share is expected to continue to grow from 89 percent in 2020 to 90 percent by 2030. Overall, by 2030, the amount of aquatic food for human consumption is projected to increase by 24 million tonnes compared with 2020, reaching 182 million tonnes. This represents an overall increase of 15 percent, a slower pace when compared with the 23 percent growth experienced in 2010–2020. This slowdown mainly reflects the reduced amount of additional fisheries and aquaculture production available, higher prices of aquatic foods in nominal terms, a deceleration in population growth and saturated demand in some countries, particularly high-income countries, where aquatic food consumption is projected to show little growth (an average annual increase of 0.3 percent in 2020–2030).

Overall, the main factors behind the increase in global consumption of aquatic food will be a combination of high demand resulting from rising incomes and urbanization, linked with the expansion of fisheries and aquaculture production, improvements in post-harvest methods and distribution channels expanding the commercialization of aquatic products.18 Demand will also be stimulated by changes in dietary trends, pointing towards more variety in the typology of food consumed, and a greater focus on better health, nutrition and diet, with aquatic food playing a key role in this regard.

Growth in demand will stem mostly from middle-income countries, which are expected to account for 82 percent of the increase in consumption by 2030 and to consume 73 percent of the aquatic food available for human consumption in 2030 (compared with 72 percent in 2020). About 72 percent of the world’s fisheries and aquaculture production available for human consumption in 2030 will be consumed by Asian countries, while the lowest quantities will be consumed in Oceania. Total consumption of aquatic food is expected to increase in all continents by 2030 in comparison with 2020, with higher growth rates projected in Africa and Oceania (26 percent in both regions), the Americas (17 percent), Asia (15 percent) and Europe (6 percent).

In per capita terms, apparent consumption of aquatic food is projected to reach 21.4 kg in 2030, up from 20.2 kg in 2020. However, the average annual growth rate of per capita consumption of aquatic food will decline from 1.0 percent in 2010–2020 to 0.6 percent in 2020–2030. Per capita consumption of aquatic food will increase in all regions except Africa. The highest growth rates are projected for Oceania (12 percent), the Americas (9 percent), Asia (7 percent) and Europe (6 percent). Despite these regional trends, the overall tendencies in quantity and variety of aquatic foods consumed will vary among and within countries. In 2030, about 59 percent of the aquatic food available for human consumption is expected to originate from aquaculture production, up from 56 percent in 2020 (Figure 75).

FIGURE 75INCREASING ROLE OF AQUACULTURE

SOURCE: FAO.

In Africa, per capita consumption of aquatic food is expected to decrease slightly from 9.9 kg in 2020 to about 9.8 kg in 2030. The decline will be greater in sub-Saharan Africa (from 8.6 kg to 8.4 kg in the same period). Despite an expected overall increase in total supply of aquatic food due to increased production and imports, it will not be sufficient to outstrip the African population growth. One of the few exceptions will be Egypt, as the country is expected to further increase its already substantial aquaculture production (up 20 percent in 2030 compared with 2020). The projected decline in per capita consumption of aquatic food in Africa, in particular in sub-Saharan Africa, raises food security concerns because of the region’s high prevalence of undernourishment (FAO et al., 2021) and the importance of aquatic proteins in total animal protein intake in many African countries (see the section Consumption of aquatic foods). The decline may also weaken the ability of countries that are more dependent on aquatic products to meet the nutrition targets of SDG 2 (End hunger, achieve food security and improved nutrition and promote sustainable agriculture), SDG Target 2.1 and SDG Target 2.2.

Trade

The expansion of trade in aquatic products will continue over the outlook period, but at a slower pace than in the previous decade, reflecting the slowdown in production growth, higher fisheries and aquaculture prices (which will restrain overall demand and consumption of aquatic species), and stronger domestic demand in some of the major producing and exporting countries, such as China, which is expected to increase its aquaculture production for the domestic market. Trade will continue to play an important role in the fisheries and aquaculture sectors, notably in terms of food supply and food security. It is estimated that about 36 percent of total fisheries and aquaculture production will be exported in 2030 (31 percent, excluding intra-European Union trade) in the form of various products for human consumption or non-edible goods. Aquaculture will contribute to a growing share of international trade in aquatic food products. In quantity terms, China will continue to be the major exporter of aquatic food, followed by Viet Nam and Norway. The bulk of the growth in exports of aquatic food will originate from Asia, which will account for about 52 percent of the additional exported volumes by 2030. Asia’s share in total trade of aquatic products for human consumption will increase from 47 percent in 2020 to 48 percent in 2030. High-income countries will remain highly dependent on imports to meet domestic demand. The European Union, Japan and the United States of America will account for 39 percent of total imports for aquatic food consumption in 2030, a slightly lower share than in 2020 (40 percent).

Trade of fishmeal and fish oil is expected to increase by 9 percent and 7 percent respectively. Peru and Chile will continue to be the main exporters of fish oil, while Norway and the European Union are the main importers, in particular for aquaculture production of salmonoids. Peru is also expected to remain the leading exporter of fishmeal, followed by the European Union and Chile, while China is the major importer.

Prices

The fisheries and aquaculture sectors are expected to enter a decade of higher prices in nominal terms. Factors driving this tendency include improved income, population growth and higher meat prices on the demand side; marginal increase in capture fisheries production, the slowing growth in aquaculture production and cost pressure from some crucial inputs such as feed, energy and fish oil on the supply side. In addition, the slowdown in Chinese fisheries and aquaculture production will stimulate higher prices in China, with repercussions on world prices. The highest increase is expected in the average price of traded products (33 percent higher in 2030 than in 2020) followed by the average price of aquaculture products (29 percent higher) that will be greater than that of captured products (19 percent, when excluding aquatic products for non-food uses). Prices of farmed aquatic species will also increase owing to higher fishmeal and fish oil prices, which are expected to increase by 11 percent and 1 percent, respectively, in nominal terms by 2030 as a result of strong global demand. High feed prices could also have an impact on the species composition in aquaculture, with a shift towards species requiring less feed, cheaper feed or no feed at all. The higher prices at the production level, coupled with high demand of aquatic food, will stimulate an estimated 18 percent growth in the average price of internationally traded aquatic products by 2030 relative to 2020.

In real terms, it is assumed that all prices, except those of aquaculture production and traded aquatic products, will decline slightly over the projection period, while remaining relatively high. For individual aquatic products, price volatility could be more pronounced as a result of supply or demand fluctuations. Moreover, because aquaculture is expected to represent a higher share of world fisheries and aquaculture supply, it could have a stronger impact on price formation in national and international markets of aquatic products. The major decreases are expected for fishmeal and fish oil prices. Yet, both prices are coming from rather historically high levels and by 2030 fishmeal prices will still be 28 percent higher than in 2005, the year major price increases began. This situation is even more pronounced for fish oil, where the real price in 2030 is expected to be 70 percent higher than that observed in 2005. Considered together, and all else remaining equal, this suggests that converting capture fisheries and fish waste to fishmeal and fish oil will remain a lucrative activity over the period projected.

Summary of main outcomes from the projections

The following major trends for the period to 2030 emerge from the analysis:

- World fisheries and aquaculture production, consumption and trade are expected to increase, but with a growth rate that will slow over time.

- World capture production is projected to grow moderately owing to increased production in areas where resources are properly managed.

- The world’s growth in aquaculture production, despite its deceleration, is anticipated to fill most of the supply–demand gap.

- Aquatic food supply will increase in all regions, while per capita consumption is expected to slightly decline in Africa, in particular in sub-Saharan Africa, raising concerns in terms of food security.

- Trade in aquatic products is expected to increase more slowly than in the past decade, but the share of fisheries and aquaculture production that is exported is projected to remain stable.

- While prices will all increase in nominal terms, they are expected to decline in real terms, except those for aquaculture and trade.

- The new fisheries and aquaculture reforms and policies to be implemented by China as a continuation of its Thirteenth (2016–2020) and Fourteenth (2021–2025) Five-Year Plans are expected to have a noticeable impact at the world level, with changes in prices, output and consumption.

Main uncertainties

The projections presented in this section (see also Box 33) rely on a series of economic, policy and environmental assumptions. A deviation of any of these assumptions would result in different fisheries and aquaculture projections. In the short term, major levels of uncertainty are linked to the COVID-19 pandemic and related effects as global value chains and trade are still recovering, and to the conflict between Ukraine and the Russian Federation. This ongoing conflict is likely to have multiple ramifications for trade, prices, logistics, production, investment, economic growth and livelihoods, causing significant food security repercussions far beyond Ukraine and with major impacts also on the fisheries and aquaculture sectors (Box 34).

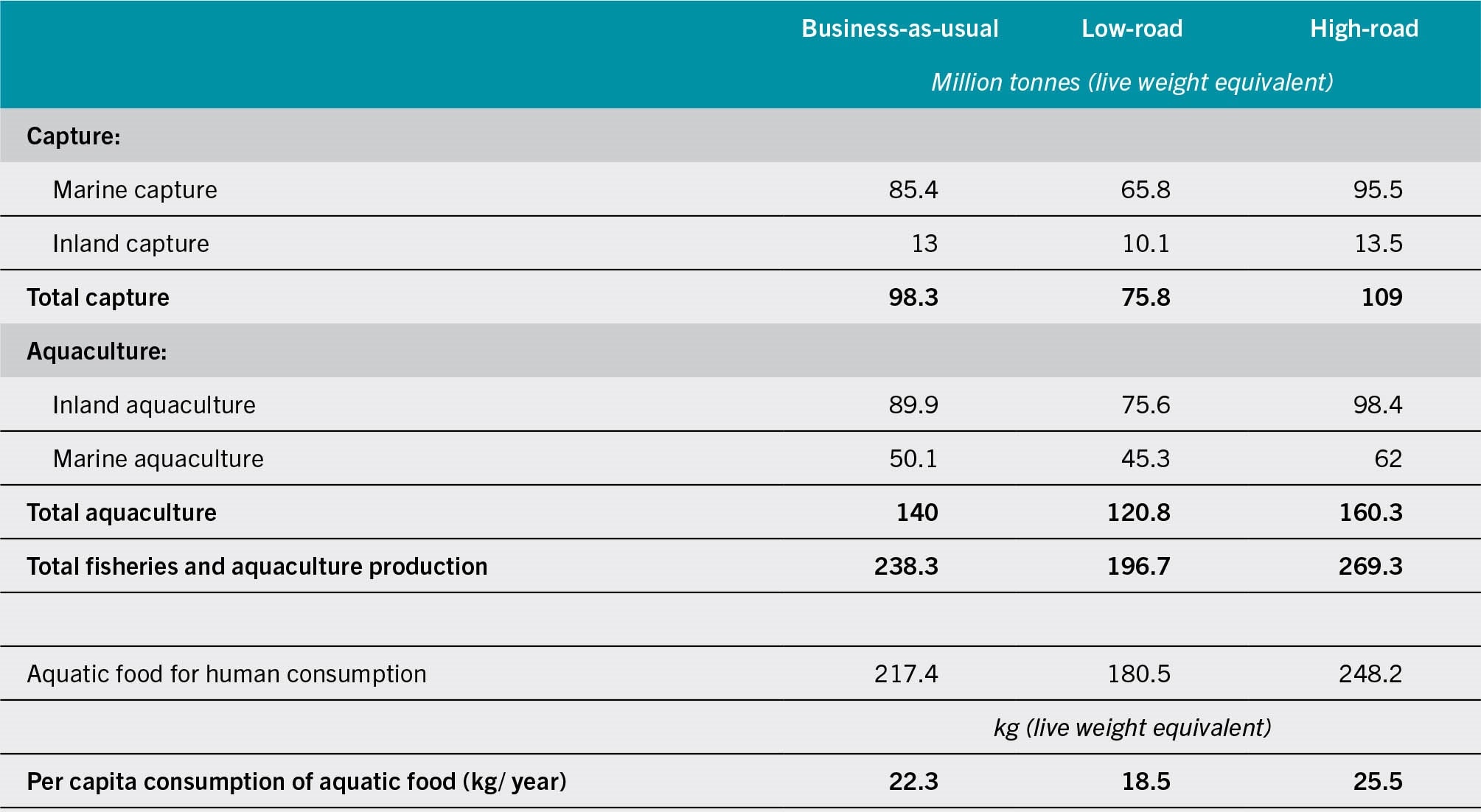

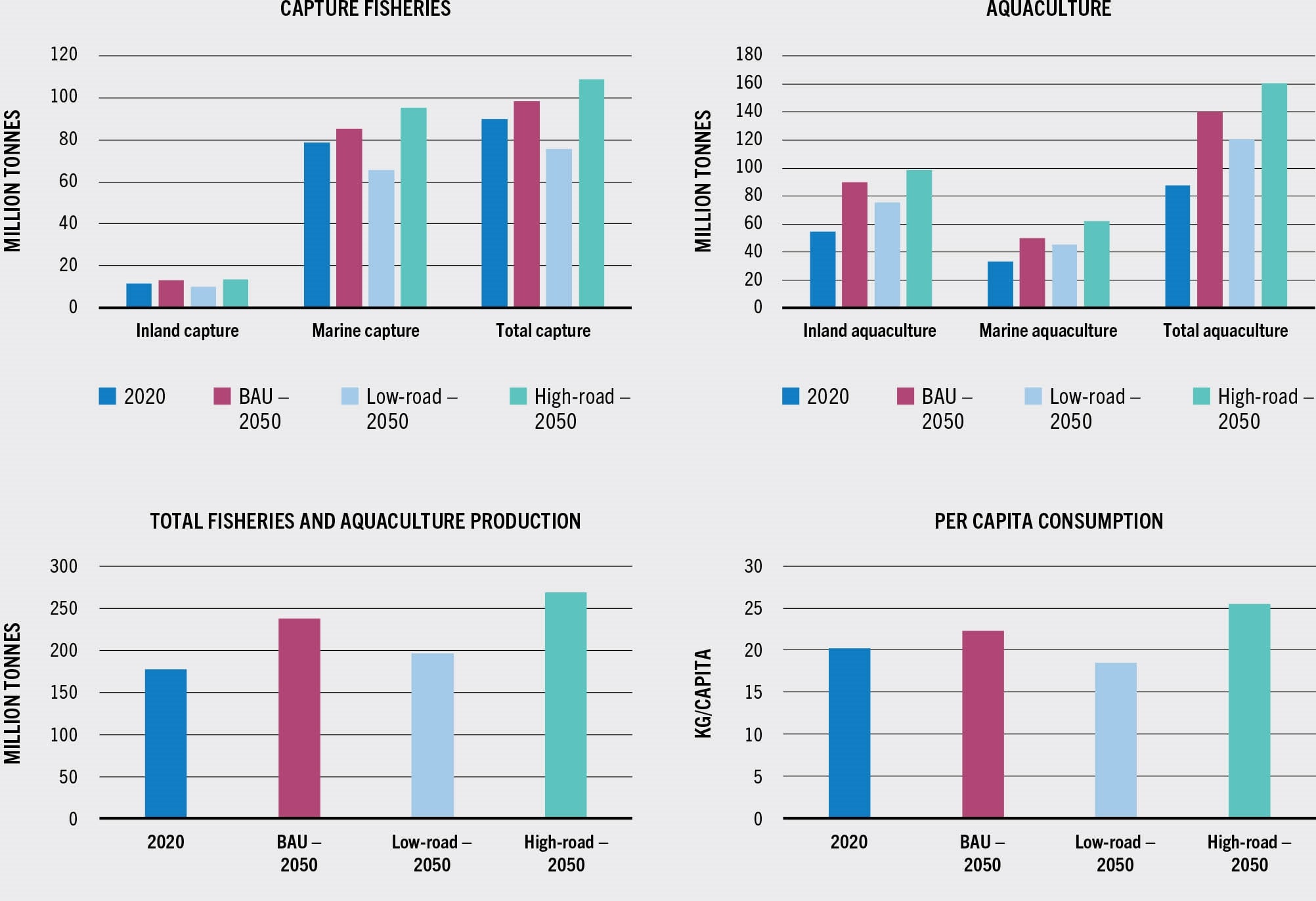

BOX 33POTENTIAL FISHERIES AND AQUACULTURE SCENARIOS TO 2050

FAO has recently conducted preliminary projections to 20501 producing three plausible fisheries and aquaculture scenarios for consideration and action. These projections are based on various expectations of sectoral growth, starting from the results of the FAO fish model included in the OECD-FAO Agricultural Outlook.2 The scenarios are:

BUSINESS-AS-USUAL

This scenario follows trend paths similar to those obtained from the OECD-FAO projections to 2030, with a modest increase in capture fisheries (resulting mainly from improved management) and an important increase in aquaculture (despite slower growth rates compared with previous decades). The scenario points to a slight growth of marine and inland capture fisheries, partially due to better reporting systems for inland fisheries. The percentage of marine capture fisheries not used for direct human consumption should slightly decrease by 2050 compared with 2030 as a result of technological improvements.

LOW-ROAD

This scenario projects several failures in aquaculture expansion and continued use of unsustainable practices, leading to a deterioration in many new ventures, resulting in limited growth of aquaculture and a slight decline in capture fisheries. Capture fisheries, both marine and inland, see a continued deterioration of the resource base every year until 2050. The low-road scenario also foresees a 9.6 percent loss in the 2050 yield, consistent with Representative Concentration Pathway (RCP) 8.5 (“business-as-usual”) projections of climate change impacts.3 The proportion of marine capture fisheries not used for direct human consumption should remain at a similar level as expected in 2031, with no benefit from further technological innovation.

HIGH-ROAD

This scenario projects some positive outcomes, allowing the development and expansion of aquaculture in a sustainable manner. Growth rates are modest but significant, as production increases and reflects more extensive investment in mariculture. A number of positive outcomes are also expected for marine capture fisheries, with growth reaching towards the estimated maximum sustainable yield of oceans and seas and the ambitious target of 95.5 million tonnes by 2050. Inland capture fisheries are expected to grow to 13.5 million tonnes, reflecting better data collection systems and the implementation of management measures, which are currently lacking in many river basins. In addition, capture fisheries (both marine and inland) are subject to a 4.05 percent decrease in 2050 yield, consistent with RCP2.6 (“strong mitigation”) projections for climate change impacts in capture fisheries.3 The percentage of marine capture fisheries not destined for direct human consumption is expected to decrease as a result of technological improvements, including reduced loss and waste.

In terms of consumption, a business-as-usual scenario would allow the apparent per capita consumption of aquatic foods to rise to 22.3 kg by 2050, up from the 20.2 kg estimated in 2020, thus increasing the contribution of aquatic foods to the fight against hunger and malnutrition. Increased per capita consumption, as envisaged by the high-road scenario, reaching 25.5 kg, would theoretically be possible through innovative and intensive aquaculture development, combined with ambitious, effective management of all capture fisheries across the world. On the other hand, failure to address current overfishing patterns, and limited aquaculture growth would potentially result in per capita consumption of aquatic food decreasing to 18.5 kg by 2050, a return to the pre-2012 levels, with a major impact on food security in particular for countries more dependent on aquatic foods in their diets.

The results of these projections are presented in the table.

PROJECTIONS OF FISHERIES AND AQUACULTURE PRODUCTION AND UTILIZATION BY 2050, AS PER THREE DISTINCTIVE SCENARIOS

SOURCE: FAO.

The nature of these projections is not to predict the future, but to provide boundary conditions to enable appropriate action for achieving food and nutrition security (see figure). The business-as-usual scenario, in particular, is considered most plausible by FAO, as it attempts to extrapolate the medium trends estimated by the FAO fish model to 2050. The FAO model uses a set of macroeconomic assumptions and selected prices, and not just projections of growth, but these assumptions become more uncertain as time passes and they need regular adjustment. The low- and high-road scenarios, on the other hand, are designed to enable appreciation of the range of expected possibilities. This envelope of scenarios allows a conversation that acknowledges that the present is not necessarily a good prediction of the future, but also that decisions taken going forward will have significant and quantitative impacts on the contribution of aquatic products to food security and nutrition. The sector will remain crucial for feeding a world that may include 9.7 billion people by 2050, but this contribution may be more significant if the right policy decisions are taken.

2020 VS 2050 IN PRODUCTION AND CONSUMPTION AS PER THE THREE SCENARIOS

SOURCE: FAO.

- 1 UN Nutrition. 2021. The role of aquatic foods in sustainable healthy diets. Discussion paper. Rome. www.unnutrition.org/wp-content/uploads/FINAL-UN-Nutrition-Aquatic-foods-Paper_EN_.pdf

- 2 OECD (Organisation for Economic Co-operation and Development) & FAO. 2020. Chapter 8: Fish. In: OECD-FAO Agricultural Outlook 2020–2029. Paris, OECD Publishing. Cited 20 April 2022. www.oecd-ilibrary.org/docserver/4dd9b3d0-en.pdf?expires=1650400376&id=id&accname=guest&checksum=512B2A7A9D84422B9E01EEA8FB9E4E67

- 3 Barange, M., Bahri, T., Beveridge, M.C.M., Cochrane, K.L., Funge-Smith, S. & Poulain, F., eds. 2018. Impacts of climate change on fisheries and aquaculture: Synthesis of current knowledge, adaptation and mitigation options. FAO Fisheries and Aquaculture Technical Paper No. 627. Rome, FAO. www.fao.org/documents/card/en/c/I9705EN

BOX 34UKRAINE: PRELIMINARY IMPACT OF THE CONFLICT ON THE FISHERIES AND AQUACULTURE SECTOR

BACKGROUND

Prior to the conflict, Ukraine’s total fisheries and aquaculture production was around 87 200 tonnes, 26 700 tonnes from inland waters, 41 900 tonnes from marine waters and 18 600 tonnes from aquaculture. The country’s fishing vessels operated in the Black Sea and the Sea of Azov within the exclusive economic zone of Ukraine and neighbouring countries and in distant waters, in particular in the Atlantic and the Pacific Antarctic. In 2020, the total catch in the Black and Azov Seas was about 20 800 tonnes, harvested by a total of 1 300 vessels.

Most of the 4 000 registered fish farms in Ukraine are small-scale, producing a range of species – predominantly carp, but also catfish, pike and trout – reared in artisanal ponds. Regarding aquaculture in marine areas, there have been no active farms since 2014, as the country’s four shellfish farms and one turbot hatchery were located in the Autonomous Republic of Crimea and the city of Sevastopol, Ukraine, temporarily occupied by the Russian Federation.

Per capita consumption of aquatic food was about 12–13 kg per year, supplied mostly by imports from European countries. Recent years have seen imports increasing, albeit with some major fluctuations, with a peak at over USD 1 billion in 2021. In the same year, exports of aquatic products were valued at USD 66 million. Imports include salmonoids, mackerel, herrings and hakes, with almost one-third (31 percent) from Norway. Exports, on the other hand, comprise mainly salmon and cod fillets, with over one-half destined for several European countries.

IMPACT

According to information provided by the State Fisheries Agency in Ukraine, due to the ongoing conflict and related risks for fishers, all landing sites and ports located on the coast are closed, and marine fisheries activities have been halted. Inland fisheries have been seriously impacted, with activities running at no more than 30 percent of capacity. In some regions (such as Chernihiv, Kherson and Zaporizhzhia) they have stopped entirely, while in others they are ongoing in estuaries, reservoirs and lakes.

Likewise, fish farming in Ukraine has been severely disrupted as a result of the interruption in the supply of fingerlings, feed and other services, damaged infrastructure, and low demand. According to preliminary FAO estimates, should the conflict continue, the economic cost in 2022 would be at least USD 70 million for primary production and most likely three times this figure when including the post-harvest value, in addition to a net loss of USD 66 million previously generated by exports. Loss of imports has heavily impacted consumption of aquatic food. Infrastructure has been seriously affected and all commercial shipping in Ukrainian ports currently halted, with major repercussions for trade to and from Ukraine.

Outside Ukraine, marine fisheries in the Black Sea of neighbouring countries have also been severely impacted. Many fisheries research surveys, and monitoring, control and surveillance activities have been disrupted or completely stopped.

Overall, the conflict in Ukraine is seriously disrupting global markets of fisheries and aquaculture products. The Russian Federation fisheries sector (in 2020, the fifth largest producer of capture fisheries) is highly export oriented. In 2021, its exports of fisheries and aquaculture products reached USD 6.1 billion, up from USD 4.9 billion in 2020. These exports are currently severely disrupted and it remains to be seen what the impact will be in terms of their value and destination. Inflationary pressure on the world economy with rising costs of inputs and operations in major aquatic-food-producing countries are worsening access to investment in a sector already often considered risky for private and institutional investment.

Furthermore, the next decade is likely to see major changes in the environment, resource availability, macroeconomic conditions, international trade rules and tariffs, and market characteristics, which may affect production, markets and trade in the medium term. Climate variability and change, including in the frequency and extent of extreme weather events, are expected to have significant and geographically differential impacts on the availability, processing and trade of aquatic products, making countries more vulnerable to risks. These risks can be exacerbated by: (i) poor governance causing environmental degradation and habitat destruction, leading to pressure on the resource bases, overfishing, IUU fishing, diseases and invasions by escapees and non-native species; and (ii) aquaculture issues associated with the accessibility and availability of sites and water resources and access to credit, seed and expertise. However, these risks can be mitigated through responsive and effective governance promoting stringent fisheries management regimes, responsible aquaculture growth and improvements in technology, innovations and research. In the long term, the implementation of these improvements and of proper management policies can have very positive impacts on total fisheries and aquaculture production as illustrated in the high-road scenario developed by FAO to 2050. In addition, market access requirements related to food safety, quality and traceability standards and product legality will continue to regulate international trade of fisheries and aquaculture products.